This article has been written by Prakash Kumar Yadav pursuing a Diploma in International Taxation and Transfer Pricing course from LawSikho.

This article has been edited and published by Shashwat Kaushik.

Table of Contents

Introduction

Every taxpayer wants to save tax on their income and reduce their tax burden; after all, they have put lots of effort into earning that income. Therefore, every taxpayer looks for a method to reduce their tax liability so that they can fully utilise that income and enjoy that hard earned money.

There are many methods to achieve that tax saving goal. But before applying any method, you have to be very careful, as selecting an illegal method can cause some serious trouble for you. Let’s understand the two methods to reduce your tax liabilities, i.e., tax avoidance and tax evasion and how a taxpayer can use these methods to minimise their tax burden in a legal and right way.

What is tax avoidance

Tax avoidance is a legal method used by taxpayers to reduce their tax liabilities, using the loopholes in the rules and regulations under the act. In other words, tax avoidance is a method to avoid payment of tax by taking advantage of a situation, where rules and regulations are not clearly defined or precise in the act. Although tax avoidance is legal, as there is no violation of the act, it is not advisable as a good practice because taxpayers try to gain an unfair advantage to avoid paying tax.

What is tax evasion

Tax evasion is an illegal method adopted by a taxpayer to escape the liability of paying taxes to the government. It is an unlawful and prohibited activity, and indulging in it can result in penalties, fines, criminal charges, and imprisonment for the taxpayer involved. It is deliberately done by overstating expenses, underreporting income, concealing sources of income and making offshore transactions.

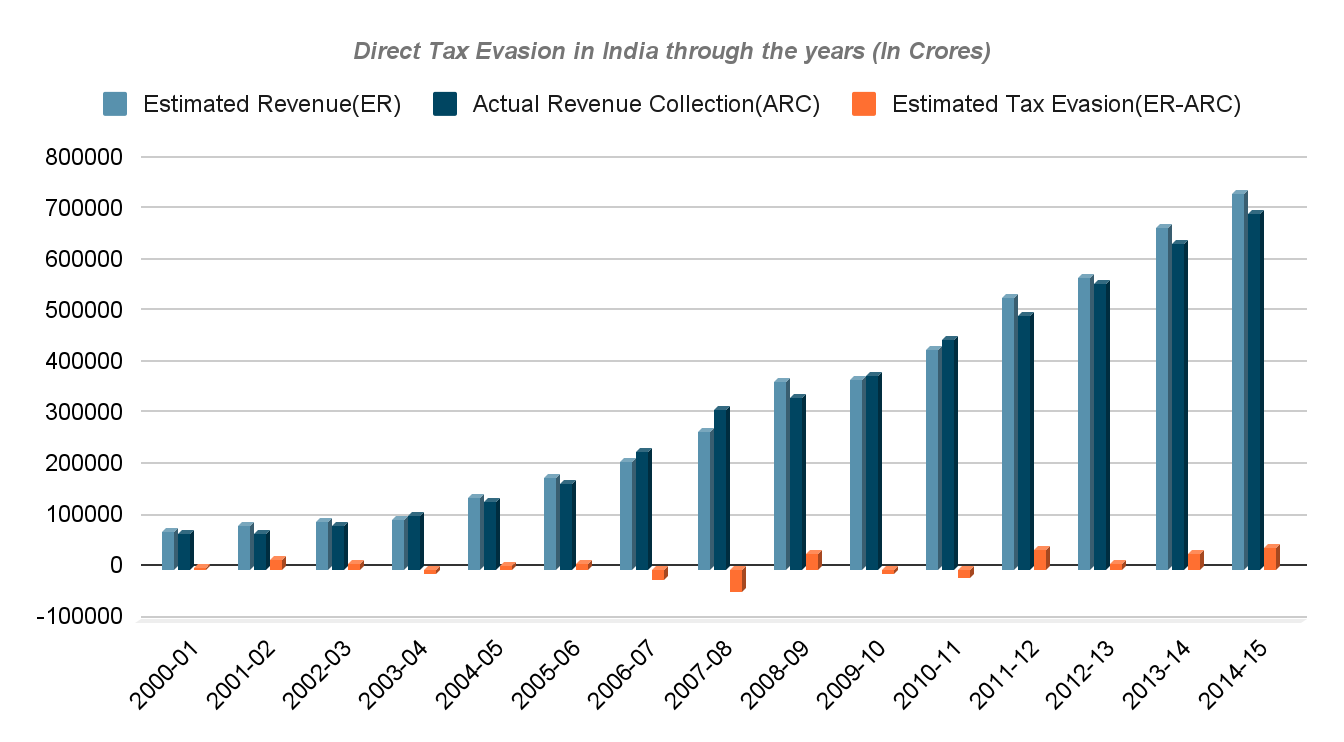

Impact of tax evasion on the Indian economy

As per the Receipt Budget 2024-25, net tax revenue receipts were Rs. 2097785.82 crores out of total revenue receipts of Rs. 2383206.47 crores, which were 88% of total revenue receipts. That means a substantial part of revenue receipts comes from taxes but as per the various estimations, India loses trillions to tax evasion annually. As per the Annual Report of the Ministry of Economic Affairs, Ministry of Finance, Government of India 2016-17, the net estimated tax evasion in direct tax from 2000-01 to 2014-15 was Rs. 1,98,449 crores.

Reasons for tax avoidance and evasion

Tax avoidance and tax evasion have become common factors in higher revenue losses for India. To curb this situation, it’s important to understand the reasons behind tax avoidance and evasion. Here are some points that lead to tax avoidance and evasion in India.

High rate of tax

No one wants to pay a higher income tax; to reduce tax liabilities, every taxpayer looks for legal or illegal ways. This high rate of taxation gives rise to emotions among taxpayers in terms of tax avoidance and evasion.

Complexity in tax laws

As we know, provisions under the acts are not easy to understand for common people. It is very difficult to understand and apply the provisions of the act without the help of professionals. As a result, to avoid the burden of professional charges, taxpayers indulge in tax avoidance and evasion.

Lack of strong tax policies

Failure to make strong tax policies may lead to loopholes and opportunities for taxpayers to misuse the provisions of tax laws to avoid paying taxes.

Weak administration

Tax authorities have limited resources, due to which they are not capable of watching or scrutinising each and every taxpayer. Also, the penalties and prosecution procedures are liberal, which result in gaps for tax avoidance and tax evasion.

Methods of tax avoidance and evasion

Here are some common methods used by taxpayers to avoid paying tax to the government:

Underreporting income

Taxpayers do not disclose their full income to escape payment of tax liabilities. Generally, taxpayers used to receive some part of their income in cash and the other through the banking channel and did not disclose their cash receipts to the department.

Concealment of income

This is the method where full sources of income are not disclosed by taxpayers. For example, a taxpayer has a trading business and also generates rental income from his house property. However, he used to collect his rental income in cash, disclose only trading business income in his return of income, and conceal income from house property.

Overstating expenses

Income is deliberately reduced by falsely claiming higher expenses to evade tax payments.

Offshore transaction

Tax evaders take advantage of loopholes in the provisions of the law in transactions between 2 countries. Vodafone International Holding vs. Union of India (2012) is the landmark caselaw of tax avoidance, where the Supreme Court held that Indian revenue authorities do not have jurisdictional authority to impose tax on transactions between two non-residents where the controlling interest of an Indian company was acquired by a non-resident company.

Creating shell companies

Shell companies are organisations without active operations and significant assets. Tax evaders used to channel their money through shell companies to escape tax payments.

Claiming deductions and exemptions

These are very common methods used by taxpayers to reduce their income in a legal way. There are various deductions and exemptions introduced by the Income Tax Department. By using these taxpayers, they can reduce their tax liabilities, like investments in tax saving instruments, take advantage of deductions under Chapter VI of the Income Tax Act of 1961 and claim all allowable allowances and expenses.

Tax shelters and tax havens

Both are strategies through which income can be reduced. Tax shelters are the instruments and entities where money is invested to generate losses and set-offs from another source of income. While in a tax haven, taxpayers enter into a transaction with a country where rates of tax are lower.

Consequences of tax evasion and tax avoidance in India

Tax evasion is an unlawful activity and is considered a criminal offence or crime. Therefore, consequences are more severe than tax avoidance, which covers penalties and fines, imprisonment, and criminal charges.

Legal provisions for tax evasion and tax avoidance

Penalties fines

- As per Section 270A of Income Tax Act, 1961, there is a penalty of 50% of tax in cases of under-reporting of income and 200% of tax in cases of mis-reporting of income.

- If you fail to keep, maintain or retain books of accounts as required by Section 44AA, penalty of Rs. 25000 can be imposed under Section 271A.

- If undisclosed income is found during the search proceedings under the Income Tax Act, penalty of up to 60% of undisclosed income can be imposed under Section 271AAB.

- As per Section 271B, failure to get accounts audited up to due date under Section 44AB can result in a penalty of 1.5% of gross receipts (subject to maximum of Rs. 1.50 lakh).

- If you fail to furnish a report of CA under Section 92E, a penalty of Rs. 1 lakh can be imposed under Section 271BA.

- If you fail to furnish information as required under Section 92D, a penalty of Rs. 5 lakh can be imposed.

Imprisonment

- As per Section 276BB, imprisonment of 3 months to 7 years is imposed in case of failure to pay the tax collected under Section 206C.

- As per Section 276C(2), imprisonment of 3 months to 3 years in case of willful attempt to evade payment of tax, penalty, and interest.

- As per Section 275A, imprisonment up to 2 years in case of contravention of order made under Section 132(1) or 132(3).

Audit and investigation

Indulging in tax evasion and tax avoidance may lead to an audit and investigation by the Income Tax Department. The Income Tax Act, 1961, has given power to the authorities to initiate audits, investigations, and scrutiny of the assessee in default.

Search & seizure

The Income Tax Department has power to initiate search and seizure when the department has sufficient grounds and reasons for tax evasion and tax avoidance.

Tax laws in India

The tax laws in India are a complex and ever-changing landscape. They are governed by various statutes, rules, and regulations issued by the Central Board of Direct Taxes (CBDT). These laws cover a wide range of taxes, including income tax, corporate tax, and goods and services tax (GST).

The Income Tax Act

The Income Tax Act of India is a comprehensive piece of legislation that governs the levy and collection of income tax in India. Enacted in 1961, the act has undergone numerous amendments over the years to keep pace with changing economic and social conditions. The Income Tax Act is administered by the Central Board of Direct Taxes (CBDT), a statutory body under the Ministry of Finance.

The act applies to all individuals, Hindu Undivided Families (HUFs), companies, and other legal entities that earn income in India. It prescribes the various sources of income that are subject to tax, the rates of tax applicable to different categories of taxpayers, and the exemptions and deductions that are available. The act also provides for the assessment of income, the filing of tax returns, and the payment of taxes.

The Income Tax Act is a complex piece of legislation, and taxpayers are advised to seek professional advice to ensure that they are complying with all the requirements of the law. The CBDT has published a number of guidelines and circulars to help taxpayers understand and comply with the provisions of the act.

The Income Tax Act is an important source of revenue for the Indian government. In the 2022-23 fiscal year, the government collected over Rs. 14 lakh crore in income tax, which accounted for about 20% of the total tax revenue. The income tax collected by the government is used to finance various public services, such as education, healthcare, and infrastructure development.

The Income Tax Act is a vital part of the Indian tax system. It helps to ensure that the government has the resources it needs to provide essential services to its citizens. The act also promotes equity by ensuring that individuals and businesses pay their fair share of taxes.

Corporate tax

Corporate tax is a significant source of revenue for governments, and it is levied on the profits earned by companies. The tax rate can vary depending on the jurisdiction, but it is typically a percentage of the company’s net income. In addition to corporate tax, companies may also be required to pay other taxes, such as sales tax, property tax, and payroll tax.

The purpose of corporate tax is to generate revenue for the government, which can then be used to fund public services such as healthcare, education, and infrastructure. Corporate tax can also be used to discourage companies from engaging in certain activities, such as polluting the environment or exploiting workers.

However, corporate taxes can also have a negative impact on businesses. High corporate tax rates can make it difficult for companies to compete with their international rivals, and they can also discourage investment and job creation. In addition, corporate tax can be complex and time-consuming to comply with, which can be a burden for small businesses.

Despite the potential drawbacks, corporate taxation remains an important source of revenue for governments around the world. It is a way to ensure that companies contribute to the costs of public services and that they are held accountable for their actions.

Here are some of the key features of corporate tax:

- It is a tax on the profits earned by companies.

- The tax rate can vary depending on the jurisdiction.

- Companies are also required to pay other taxes, such as sales tax, property tax, and payroll tax.

- The purpose of corporate taxation is to generate revenue for the government.

- Corporate taxes can also be used to discourage companies from engaging in certain activities.

- High corporate tax rates can make it difficult for companies to compete with their international rivals.

- Corporate taxation can also discourage investment and job creation.

- Corporate tax can be complex and time-consuming to comply with.

Goods and Services Tax Act (GST)

The Goods and Services Tax (GST) is a comprehensive indirect tax levied on the supply of goods and services. It is a destination-based tax, which means that it is levied at the point of consumption. GST is a single tax that replaces multiple indirect taxes levied by the Central and State Governments.

GST was introduced in India on July 1, 2017, and it has brought about a significant change in the indirect tax landscape of the country. GST is a major step towards creating a unified common market for goods and services in India.

Here are some of the key features of GST:

- It is a comprehensive tax that applies to all goods and services, except for a few exempt items.

- It is a destination-based tax, which means that it is levied at the point of consumption.

- It is a single tax that replaces multiple indirect taxes levied by the Central and state governments.

- It is a self-assessed tax, which means that taxpayers are responsible for calculating and paying their own taxes.

- It is a technology-driven tax with a focus on electronic filing of returns and payments.

GST has had a significant impact on the Indian economy. It has made it easier for businesses to do business across state borders, and it has led to a reduction in the cost of doing business. GST has also helped increase tax compliance and reduce tax evasion.

Overall, GST has been a positive development for the Indian economy. It has made the tax system more efficient and transparent, and it has helped to create a more level playing field for businesses.

Here are some of the benefits of GST:

- It has made it easier for businesses to do business across state borders.

- It has led to a reduction in the cost of doing business.

- It has helped to increase tax compliance and reduce tax evasion.

- It has made the tax system more efficient and transparent.

- It has helped to create a more level playing field for businesses.

Landmark case laws on tax evasion

Commissioner of Income Tax vs. Ramkanth Mohanlal Gandhi: (1978) 113 ITR 266 (SC)

In the landmark case of Commissioner of Income Tax vs. Ramkanth Mohanlal Gandhi (1978) 113 ITR 266 (SC), the Supreme Court of India established the principle of “wilful tax evasion” as an essential element of the offence. This principle has had a profound impact on the interpretation of tax laws in India and has been cited in numerous subsequent cases.

The court, in its judgement, held that mere ignorance of the tax law or inadvertent errors would not constitute wilful tax evasion. The court stated that the term “wilful” in the context of tax evasion requires a conscious and deliberate act or omission with the knowledge that it is contrary to the law. The court further held that the burden of proving wilfulness lies with the prosecution, and it must be established beyond a reasonable doubt.

The principle established in the Ramkanth Gandhi case has been applied in numerous subsequent cases. For example, in the case of CIT vs. Hindustan Coca-Cola Beverages Pvt. Ltd. (2017), the Supreme Court held that the assessee’s failure to deduct tax at source from the payments made to its dealers was not wilful tax evasion, as the assessee had a bona fide belief that the payments were not subject to tax deduction at source.

The principle of wilful tax evasion has also been applied in cases involving the imposition of penalties under the tax laws. In the case of CIT vs. B.K. Birla (2008), 175 DTR 1 (SC), the Supreme Court held that the imposition of a penalty under Section 271(1)(c) of the Income Tax Act, 1961, requires a finding of wilfulness on the part of the assessee.

The principle established in the Ramkanth Gandhi case is important as it provides a safeguard against the arbitrary imposition of penalties and prosecution for tax evasion. It ensures that only those who have knowingly and deliberately evaded tax are held liable.

State of Gujarat vs. Rameshchandra Ramniklal Shah

In the landmark case of State of Gujarat vs. Rameshchandra Ramniklal Shah (1983), the Supreme Court of India clarified the meaning of “gross negligence” in the context of tax evasion. This case had a significant impact on the interpretation of tax laws in India and established important principles regarding the culpability required for imposing penalties for tax evasion.

The court held that gross negligence, in the context of tax laws, involves a “conscious and deliberate disregard” of the tax laws, amounting to a “wilful omission” of tax liability. This definition sets a high threshold for establishing gross negligence, requiring a level of culpability beyond mere carelessness or oversight.

The court reasoned that gross negligence requires a higher level of culpability than ordinary negligence because it involves a conscious and intentional disregard of the law. To constitute gross negligence, the taxpayer must have been aware of the tax laws and wilfully failed to comply with them.

This interpretation of gross negligence has been consistently applied by courts in India in subsequent cases. It has ensured that penalties for tax evasion are imposed only when there is a clear and deliberate disregard of the law, and not for mere mistakes or inadvertent errors.

The case of State of Gujarat vs. Rameshchandra Ramniklal Shah has also been cited as a precedent in other jurisdictions, demonstrating its influence on the interpretation of tax laws beyond India. It has contributed to the development of a consistent approach to gross negligence in the context of tax evasion, ensuring that penalties are imposed fairly and in accordance with the principles of justice.

Landmark case laws on tax avoidance

CIT vs. McDowell & Co.

The CIT v. McDowell & Co. case, decided in 1985, is a significant precedent in the realm of tax law. It established the crucial concept of “business purpose” in tax avoidance transactions. The ruling introduced the principle that a transaction cannot be deemed tax avoidance if it is undertaken with a genuine business purpose, even if it also results in tax savings.

The case involved the taxpayer, McDowell & Co., which purchased a series of life insurance policies for its key employees. The premiums paid for these policies were substantial and resulted in significant tax deductions for the company. However, the court found that the primary purpose of these transactions was to preserve the company’s business interests, not solely to obtain tax benefits.

The court reasoned that the insurance policies served a legitimate business purpose by providing financial protection for the company in the event of the death or disability of key employees. The court held that the tax savings were merely incidental to the primary business purpose and therefore did not constitute tax avoidance.

This decision introduced a crucial distinction between tax avoidance and tax planning. Tax avoidance involves engaging in transactions primarily aimed at reducing tax liability, often through artificial or contrived means. In contrast, tax planning involves legitimate business transactions that also result in tax savings as a secondary benefit.

The “business purpose” doctrine established by the CIT v. McDowell & Co. case has been influential in shaping tax law and jurisprudence in subsequent years. It has provided a framework for courts and tax authorities to distinguish between genuine business transactions and those primarily motivated by tax avoidance.

The concept of business purpose has also had implications for tax policy and legislation. It has influenced the development of anti-avoidance provisions and rules aimed at curbing aggressive tax planning strategies. Taxpayers and their advisors must carefully consider the business purpose of transactions and ensure that they are not primarily motivated by tax avoidance to avoid potential challenges from tax authorities.

In summary, the CIT v. McDowell & Co. case established the concept of “business purpose” in tax avoidance transactions. It held that a transaction cannot be treated as tax avoidance if it has a genuine business purpose, even if it also results in tax savings. This decision has had a significant impact on tax law and jurisprudence, shaping the distinction between legitimate tax planning and tax avoidance.

Azadi Bachao Andolan vs. Union of India

In 2003, the landmark case of Azadi Bachao Andolan v. Union of India had a significant impact on the taxation landscape in India. The case revolved around the validity of the General Anti-Avoidance Rule (GAAR) introduced in the Income Tax Act, 1961, which aimed to combat tax avoidance strategies.

The Supreme Court, in its judgement, upheld the validity of GAAR, recognising it as a necessary tool to prevent tax avoidance and protect the integrity of the tax system. Here are the key points of the judgement and its implications:

- Broad interpretation of GAAR: The court interpreted GAAR broadly, stating that it was not limited to specific avoidance schemes but applied to any arrangement or transaction whose main purpose was to obtain a tax benefit that was not intended by the legislature. This broad interpretation provided the tax authorities with a wide scope to scrutinise transactions and assess their tax implications.

- Tax avoidance vs. tax evasion: The court distinguished between tax avoidance and tax evasion, emphasising that GAAR was primarily concerned with tax avoidance, which involves legal but artificial arrangements to minimise tax liability, while tax evasion involves illegal means to evade taxes. GAAR was meant to target sophisticated tax planning strategies that exploited loopholes or ambiguities in the law.

- Principle of substance over form: The court emphasised the principle of substance over form, stating that the true nature and substance of a transaction should be considered rather than its legal form. This principle allowed the tax authorities to look beyond the superficial structure of a transaction and examine its underlying purpose and economic substance to determine whether it fell within the purview of GAAR.

- Safeguards against misuse: Recognising the potential for misuse or arbitrary application of GAAR, the court imposed certain safeguards to ensure that it was used judiciously. These safeguards included the requirement for the tax authorities to provide detailed reasons for invoking GAAR, the right of taxpayers to seek advance rulings, and the availability of an independent dispute resolution mechanism.

- Impact on taxpayers: The Azadi Bachao Andolan judgement had a significant impact on taxpayers, particularly those engaged in complex tax planning strategies. It heightened the scrutiny of transactions and increased the risk of tax assessments and penalties for non-compliance. Taxpayers were advised to carefully review their tax planning structures and ensure that they were in line with the spirit and intent of the law.

- Importance of tax compliance: The judgement reinforced the importance of tax compliance and discouraged the use of aggressive tax avoidance schemes. It sent a strong message that the government was committed to upholding the integrity of the tax system and ensuring that all taxpayers contributed their fair share of taxes.

- Subsequent developments: The Azadi Bachao Andolan judgement has had a long-lasting impact on the Indian taxation landscape. It led to the introduction of additional anti-avoidance provisions in the Income Tax Act, such as the Minimum Alternate Tax (MAT) and the introduction of a specific GAAR regime in 2017. These measures further strengthened the government’s ability to address tax avoidance practices.

Overall, the Azadi Bachao Andolan v. Union of India case established a robust framework for combating tax avoidance in India, ensuring that the tax system remained equitable and efficient and that all taxpayers fulfilled their obligations responsibly.

Conclusion

Tax avoidance and evasion are both downgrading our Indian economy, which impacts our budget, borrowings, public debts, economic stability, and foreign direct investment. To curb this situation, the Government of India has taken some initiatives but as a citizen of India, it is also our prime duty to serve our nation and make some contribution to the stability of the Indian economy. Therefore, every taxpayer tries to escape tax evasion, which may sometimes lead to fines, penalties, imprisonment, and criminal charges. Taxpayers are advised to adopt the tax deduction and exemption provisions specified under the act for the benefit of reducing their tax liabilities and taking themselves away from the harsh provisions of the act.

References

- https://dea.gov.in/budgetdivision/annual-reports

- https://www.lawsenate.com/case-studies/vodafone-international-holding-vs-union-of-india.html

- https://ijcrt.org/papers/IJCRT2312064.pdf

- https://incometaxindia.gov.in/Charts%20%20Tables/Penalties%20and%20Prosecutions.html

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications