In this blog post, Khushboo Tatia, a practising Advocate and Solicitor and Proprietor at KTP Legal, Mumbai, a student, pursuing a Diploma in Entrepreneurship Administration and Business Laws from NUJS, Kolkata, describes when businesses should file their advance tax returns and lists the consequences of non-filing of returns.

History of Taxation in India

In India, the system of direct taxation as it is known today has been in force in one form or another since ancient times. Manu, the ancient sage, and law-giver stated that the king could levy taxes. The sage advised that taxes should be related to the income and expenditure of the subject. He, however, cautioned the king against excessive taxation and stated that both extremes should be avoided namely complete absence of taxes and exorbitant taxation. According to him, the king should arrange the collection of taxes in such a manner that the subjects did not feel the pinch of paying taxes.

What is Advance Tax?

Advance Tax is one of the modes of payment of tax and is payable by the assessee in advance in the financial year in which the concerned income is earned.

Why should one pay Advance Tax?

The purpose of collection of taxes in advance is to keep a periodic and systematic flow of liquid funds into the country’s treasury which in turn can be distributed amongst its citizens thereby creating a continuous movement in the cash market. This not only helps the government to prepare for its budget but also track its performance as compared with that of last year and take necessary measures on a timely basis.

On the other hand, from the point of view of a tax payer, it is fairly easier for one to pay taxes in smaller terms, on an instalment basis, rather than paying the liability at 100% at one go.

The Income Tax Act, 1961 (relevant sections)

Sections 207-219 of Income Tax Act 1961 deals with Payment of Advance Tax. Sec 207 states as follows:

“(1) Tax shall be payable in advance during any financial year, in accordance with the provisions of sections 208 to 219 (both inclusive), in respect of the total income of the assessee which would be chargeable to tax for the assessment year immediately following that financial year, such income being hereafter in this Chapter referred to as “current income”.

(2) The provisions of sub-section (1) shall not apply to an individual resident in India, who–

(a) does not have any income chargeable under the head “Profits and gains of business or profession”; and

(b) is of the age of sixty years or more at any time during the previous year.”

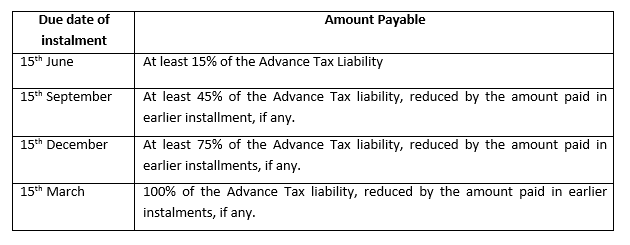

The schedule for payment of Advance Tax is as follows:

However, in the case of an advance tax, the assessee is not required to file any returns with the Income Tax department. An assessee simply pays the taxes during the year based on its self-assessment, which during the filing of its annual Income Tax returns are assessed and realized thereon.

However, in the case of an advance tax, the assessee is not required to file any returns with the Income Tax department. An assessee simply pays the taxes during the year based on its self-assessment, which during the filing of its annual Income Tax returns are assessed and realized thereon.

Who should and shouldn’t pay Advance Tax?

Advance tax is payable by all assessees i.e. individuals, businesses, HUF, LLP, etc. unless specifically exempted under Sec. 207(2). Advance tax is payable in every case where the amount of tax liability of the assessee is Ten Thousand Rupees (₹ 10,000/-) or more.

Further, as per the amendments in the year 2012, all senior citizens not having any income from business or profession were exempted from payment of any advance taxes.

However, if an assessee opts for Presumptive scheme under 44AD and 44AE, the assessee is liable to pay the whole amount of his advance tax in one installment on or before 15th March.

Penalty for Non-payment/Deferment of Payment

Sections 215, 234B and 234C, deal with short/non-payment or deferment of payment of tax by an assessee.

In case the tax so paid is less than 75% of the assessed tax, the assesse shall be liable to pay simple interest @ 15% p.a. from 1st April of the following financial year until the date of regular assessment, of the amount by which the advance tax so paid falls short of the assessed tax. If the assessee defers the payment of tax or the tax so paid is less than 90% of the assessed tax, the assessee shall be liable to pay simple interest @ 1% per month from 1st April of the following financial year until the date of regular assessment. Further, if an assessee fails to pay the tax in accordance with the table above, the assessee shall be liable to pay simple interest @ 1% per month for a period of 3 months on the amount falling short.

Concept: Tax Deduction at Sources (TDS) / Tax Collection at Source (TCS)

Also, there is a concept of TDS & TCS similar to an advance tax, where taxes are deducted during the execution of every transaction and submitted with the government on a periodic basis.

In the case of TDS/TCS, the assessee deducting such taxes are required to file periodic returns with the department, contravention to which interest and penalties shall be levied.

[divider]

Bibliography

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications