")

In this blog post, Afzal Sorathiya, a student pursuing a Diploma in Entrepreneurship Administration and Business Laws by NUJS, analyses the legal sources of cost auditing in India.

What is Cost Auditing?

The concept of cost audit has been explained by ICWA Institute as ‘an audit of efficiency of minute details of expenditure, while the work is in progress and not a post-mortem examination, cost audit is mainly a preventive measure, a guide for management policy and decision in addition to being a barometer of performance’.

Cost Audit can be called efficiency audit. It is evidenced by amendment in section 209, which reads. ‘The object of the amendment of the section is to ensure specified company proper records relating to utilization of material labor available which would make efficiency (cost) audit possible’.

What is its Relevance?

The Cost Accounting Record Rules (CARR) and Cost Accounting Report Rules (CART) were introduced in the 1970s and 1980s to reduce the misuse of national resources.

In the recent past, India has experienced reduced public interest because of weak corporate governance thus affecting the trust and confidence of the retail and institutional investors and stakeholders.

Regulatory mechanism in India is being strengthened for each sector and availability of standardized cost data is a pre-requisite for effective functioning of any regulator. More than 80% of international trade disputes today are caused on account of transfer pricing which is based on the cost data to determine the arm’s length price. Thus standardizing and assessing the competitiveness for various industries needs cost data.

Information of cost data is critical in many ways other than transfer pricing like predatory pricing, fixation of margin for the purpose of applying anti-dumping duty, free trade agreement, protection of consumer, sick companies revival and corporate governance.

Cost Audit gives an assurance that the company’s cost accounting records are so maintained that it gives a true and fair picture of the cost of the product/activity.

Advantages of Cost Audit

- A close check is maintained on all wastage, material in stores, etc., and the same are located and reported.

- Production Inefficiency will be identified and converted into monetary terms thus leading to optimum utilization of resources.

- Correct responsibilities of individuals are fixed and management by exception is made possible.

- Budgetary control system and standard costing will be facilitated with Cost Audit by a qualified cost accountant.

- Records will be up-to-date and information made easily available for various purposes.

- Cost Audit can bring to surface number of frauds and errors, which may not be surfaced otherwise. This is attributed to minute examination of records and comparison with standards.

- Cost Audit offers various advantages to share holders, management, consumers and the government.

Appointing Authorities of Cost Audit

A cost auditor may be appointed by:

- Internal authorities, i.e., the management of the company.

- External authorities, i.e.,:

- The Government.

- The Customer.

- Trade association or tribunal.

Based on these appointing authorities the corresponding types of Cost Audit are listed below.

Types of Cost Audit

The main types of Cost audit are the following:

- Cost Audit as an Aid to Management and Directors: This purpose is to ensure that all information that is presented before the management is reliable, relevant, and prompt so that proper action can be taken of the same. It should also be ensured that no information is suppressed.

- Cost Audit on Behalf of a Customer: It is a very old practice to place orders/contracts on Cost + basis, in such cases, the customer decides the final price that needs to be paid after adding profit margin to the cost. In such cases Cost Audit is carried out for the concerned product thus helping in arriving at the cost and then the final price.

- Cost Audit on Behalf of Government: The Government is requested for financial help and protection in lot of cases. In such cases, before concluding anything, the Government may choose to get the Audit done by a Cost Accountant thus ensuring that the decision to be taken would be genuine.

- Cost Audit under Statute: The 1965 Amendment Act has introduced new section 233B in 1956 Companies Act, after which the Central Government can order certain classes of companies to get the accounts audited by a cost accountant who is a member of the ICWAI (Institute of Cost and Works Accounts of India) now known as ICMAI (Institute of Cost and Management Accountants of India). These companies are required to necessarily maintain proper records with respect to the material consumed, labor utilized and all other expenses as defined under Section 209 (or may be amended to date). The aim of this particular type of cost audit may be that the Government wishes to know, as a control instrument, the costs of various goods/services and the expenditure involved. The power to prescribe, the fixed forms in which reports of cost audit are to be made rests with the Government.

- Cost Audit on Behalf of the Trade Association: Trade Associations need to maintain pricing of goods and services at a certain level. For the said purpose, the costing information submitted to the association has to be cross checked. The trade associations have full authority to have the production capacity and the comparison of the efficiency of productive processes.

What is the Qualification of Cost Auditors?

As per the Rule 2 Clause C of the 2014 Cost Records and Audit Rules, a Cost Auditor means a Cost Accountant in practice as defined in Clause B who is appointed by the Board.

Cost Accountant in practice means that the person should hold a valid certificate of practice as defined under the section 6 sub-section 1 of that Act and who is deemed to be in practice under section 2 sub-section 2 and includes a firm or LLP of Cost Accountants.

Thus, only a Cost Accountant as defined under section 2 sub-section: 28 of the 2013 Companies Act with valid certificate to practice is qualified to get appointed as a Cost Auditor.

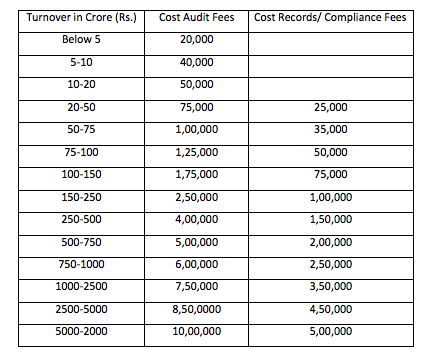

Costs for Cost Auditing:

As defined and decided by the ICMAI Institute the minimum fees for Cost Audit is summarized in the table below:

Applicability of Cost Audit

Rules 1-6 are defined for determining the applicability of Cost Audit as per the Cost Records and Audit Rules 2014, but describing each rule in detail in this article of 1500 words is not possible hence only a brief is mentioned below:

Regulated sectors and Non-Regulated sectors are the categories and a general threshold of turnover of INR 35 Crore or more has been prescribed for companies covered. Micro or Small enterprise as per the 2006 MSMED Act has been taken out of the purview.

For Regulated sectors like Telecommunication, Electricity, Gas and Petroleums, Pharma and Drugs, Sugar and Fertilizers, Cost audit requirement has been made subject to a turnover based threshold of INR 50 Crore for all product and services and at INR 25 Crore for individual product and services. For Non-regulated sector the threshold is INR 100 Crore and INR 35 Crore respectively for all products and services and individual product and services.

What are the consequences of not doing it?

If a company fails to maintain Cost Records, the company shall be punishable with fine ranging from INR 25,000 to INR 5 Lac. Also the officer of the company who is in default is subject to one-year imprisonment or fine ranging from INR 10,000 to INR 1 Lac or both. Hence, it is the duty of the compliance officer to ensure that all the legal compliances with respect to the cost record and cost audit being complied with.

Procedure for Cost Auditing

With respect to the 2013 Companies Act,  the Ministry of Corporate Affairs notified 2014 Companies (Cost Records and Audit) Rules on 30th Jun 2014, which was amended, vide 2014 Companies (Cost Records and Audit) Amendment Rules on 31st Dec 2014. The mechanism with respect to maintenance of cost records, cost audit and appointment of cost auditors has been changed and shall be in accordance with 2014 Companies (Cost Records and Audit) Rules as amended.

the Ministry of Corporate Affairs notified 2014 Companies (Cost Records and Audit) Rules on 30th Jun 2014, which was amended, vide 2014 Companies (Cost Records and Audit) Amendment Rules on 31st Dec 2014. The mechanism with respect to maintenance of cost records, cost audit and appointment of cost auditors has been changed and shall be in accordance with 2014 Companies (Cost Records and Audit) Rules as amended.

The applicability of maintenance of Cost Records and Cost Audit shall be for those sectors which are mentioned in the Tables ‘A’ and ‘B’ * to the 2014 Companies (Cost Records and Audit) Amendment Rules dated 31stDec 2014 notified by the Government vide GSR-1/2015(E) dated 1st Jan 2015.

* Note: The tables cannot be incorporated in this article because of limitation of number of words in the article.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications