")

This article is written by Shreya Kalantri, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from Lawsikho.com.

Table of Contents

Introduction

Takeover happens when the acquirer acquires the target company against the will of the promoters of the company. It generally happens in a hostile manner. When the takeover happens against the wish of the target company a lot of steps are adopted and taken into action to forestall or deter the acquirer from acquiring the target company. There are very few defence strategies that have been recognised in India, whereas in the US there are a lot of recognised defence strategies. Most countries regulate these defences by enacting laws, which are challenged by the acquirer in the official courtroom. Let us now understand the various defence strategies that are used in India.

Defence strategies that are used in India

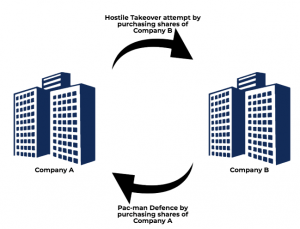

Pac-man defence strategy

In the Pac-man defence strategy, the target company tries to turn things around by trying to take over the acquirer company itself. This form of defence strategy is an expensive defence strategy that might increase the debts of the target company. The shareholders may endure misfortune or get a lower profit for not many years. Possible only when the company is cash-rich and the market capitalisation of the acquiring company is small; that is the share price of the acquiring company is low. However there is one restriction in this defence and that is regulated by Regulation 26(2) of SAST which prohibits the target company to enter into any transaction outside the ordinary course of business, except by the way of Special Resolution.

Example

Company A tries to acquire Company B by acquiring its shares for controlling the company. Company B then realises this and decides to use the Pac-man defence and tries to acquire Company A, seeing that Company A realises the potential risk and abandons its hostile takeover.

White knight defence strategy

In the White Knight defence strategy, the target company goes to another friendly company (third party) requesting them to buy the shares of the target company. It is done with a view that the promoter of the target company will buy back the shares from the friendly company (third party) later. The friendly company has to make a counter bid against the acquirer within 15 working days.

Case law

The East India Hotels (EIH) controlled by the Oberoi family confronted a hostile takeover by ITC hotels, which had acquired 14.98% shares of EIH in the year 2009 and they were about to make an open offer. The trigger point back then was 15%. The Reliance industry acted as White Knight and bought shares of EIH and as soon as ITC touched the trigger point Reliance industry had decided to touch the trigger point too and make a counteroffer. Both the companies were cash-rich and would have had tough competition. Accordingly, ITC chose to not go ahead with a hostile takeover and the East India Hotels were protected by the Reliance industry.

Crown jewel defence strategy

In the Crown Jewel defence strategy, the target company sells the most important asset of the company or has a demerger which makes the target company less attractive to the acquirer. This defence strategy is used to avoid hostile takeover especially of those companies where the asset is the significant strength of the organisation. This diminishes the worth of the target company. There are two major challenges in this defence strategy that is:

- A) According to Section 180(1)(a) of the Companies Act if any company sells its shares 20% or more then it has to do it through Special Resolution.

- B) According to Regulation 26(2) of Substantial Acquisition of Shares and Takeover (SAST) the company has to pass a Special Resolution if it alienates its material asset.

Case law

L&T had an assorted business area out of which one business area was of the cement industry and the Aditya Birla group was keen on it. Aditya Birla group had bought an enormous number of shares of L&T from the Reliance industry and chose to make a hostile takeover of the L&T business as they were interested in its cement business. Seeing this the promoters of the L&T industry and Aditya Birla group had a meeting and L&T chose to demerge its Ultra Tech cement industry and Aditya Birla group got it and consequently Aditya Birla group had released the shares they owned of L&T industry.

Greenmail defence strategy

In this defence strategy, the acquirer buys the shares of the target company and then the target company offers a premium rate to the acquirer to surrender his holdings in the target company back to the promoters of the target company. This strategy should be used only after a cost-benefit analysis.

Case law

In the case of Abhishek Dalmia vs GESCO, Abhishek Dalmia the chairman of Renaissance group decided to make a hostile takeover of GESCO company by accumulating 10.5% shares of GESCO and then made an Open Offer for additional 45% shares in the company at Rs 23 per share. Within a week Dalmia & company had raised the Offer price to Rs 27 per share. Seeing this the target company GESCO decided to make a counteroffer to Dalmia & company and this process of counter offers continued between Dalmia & company and GESCO, finally Dalmia & company had sold their 10.5% shares of GESCO back to GESCO at Rs 54 per share.

Golden parachute defence strategy

A Golden Parachute refers to the separation clause which is an agreement between a company and a high-level executive that provides significant financial benefits to the employee upon termination, especially on the basis of takeover. The provision usually calls for a lump-sum payment or payment over a specified period at full and partial rates of normal compensation. The Golden Parachute contracts can be used as an anti-takeover measure taken by the company to discourage the takeover by any other firm, due to the high cost associated with these contracts. Golden Parachute is practised on a large scale in the USA but not on a large scale in India as there are laws governing compensation for top-level executives termination already in the Companies Act.

Example

Let us assume A is the promoter of the target company. He will have his own set of Board of Directors and then if person B who is the acquirer acquires the company then he will bring his own Board of Directors and will have to pay hefty remuneration to A’s Board of Directors under Golden Parachute and has to also pay for the shares of the target company. So the acquirer B needs to pay a colossal sum and may even bring about misfortune, so he chooses to abandon the possibility of a takeover of the target company.

Poison pill defence strategy

This defence strategy is also known as the shareholders’ rights plan. In this strategy, the company issues the securities with special rights excisable only on the occurrence of a triggering event. These securities grant special rights to existing shareholders to purchase additional stock at a discounted price on that triggering event, say 25% acquisition. Poison pills make it difficult and costly for the acquirer to acquire shares.

Shark repellent defence strategy

This defence strategy has gained popularity in recent times and is also known as anti-takeover amendments. The company makes special amendments in the Article of Association which have to be voted and approved by the shareholders. This strategy consists of changing the articles, bylaws, regulations, etc of the company to make it look less attractive to the acquirer. Companies can amend the Article of Association under Section 31 of the Companies Act. Types of anti-takeover amendments:

- Supermajority amendments

These amendments require shareholder approval by at least two-thirds vote and sometimes as much as 90% of the voting power of outstanding capital stock for all transactions involving a change of control. These amendments make it almost impossible for the acquirer to acquire the shares of the target company.

- Macaroni defence

The firm may issue a large number of bonds with the provision that, if the firm is taken over then they must be redeemed at the stipulated high price.

Buyback defence strategy

This defence mechanism is extremely useful for the promoters of the target company. In this mechanism, the acquirer gives an open offer to the shareholders of the target company meanwhile the promoters of the target company also give a buyback offer to the shareholders of the target company to purchase their shares. Buy-back of shares is governed and regulated under the Companies Act of 1956.

Case law

Mindtree Limited is a software service company and 20.41% of its shares were with V.G. Siddhartha who was one of the first investors in the company but in 2019 to cut down on its debt he sold his shares to L&T. L&T already had a few shares of Mindtree Limited and after acquiring shares from V.G.Siddhartha their total shares reached 29%. Then they had made an Open Offer and acquired 31% more shares and now they had totally acquired 60.6% shares of Mindtree Limited. Mindtree founders planned a Buy Back as they were unhappy with the acquisition but they failed and L&T took over Mindtree Limited.

Conclusion

Takeover defences play an important role in corporate restructuring. As we know in India very few takeover defences are considered and it’s high time we make amendments and inculcate various other defence mechanisms like the ones in the U.S.A. Companies Act has to be more accommodative towards such defences. This would enable takeovers to facilitate the removal of incompetent management and/or traditionally family-owned companies and increase efficiency in a more competitive global market.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications