This article is written by Vishakha Bhatnagar, pursuing Diploma in M&A, Institutional Finance and Investment Laws from LawSikho.

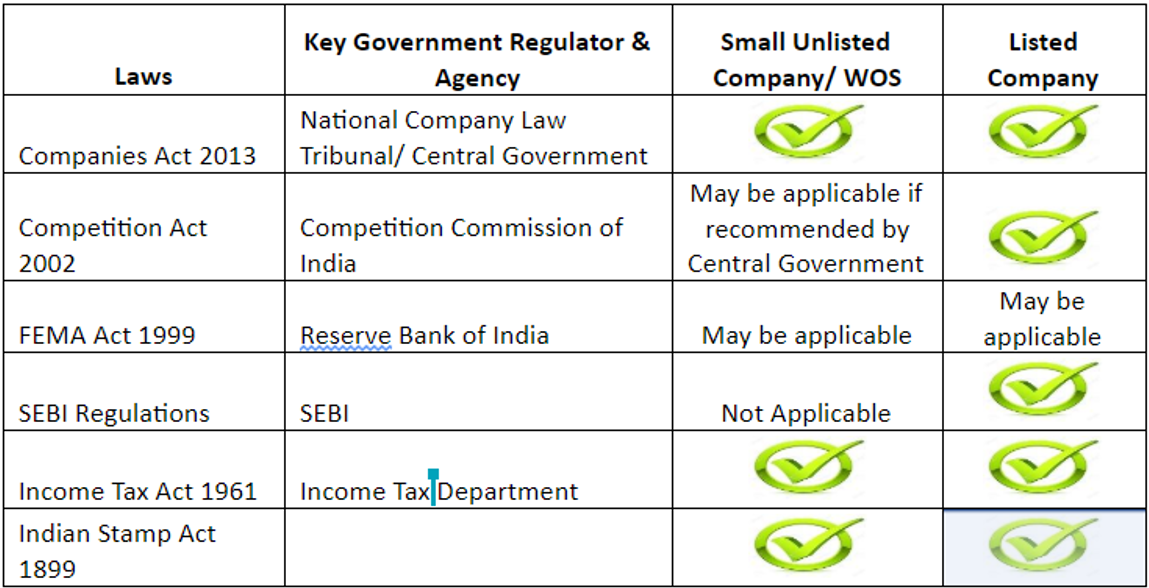

Mergers are governed by the following key laws and regulators in India. The key differences between mergers in listed and non listed companies arise due to compliance to provisions of Companies Act and requirements and compliance to SEBI regulations. While compliance to SEBI regulations does not arise for merger/ demerger of 2 non listed companies, when a non-listed company merges/ de-merges from a listed company or vice-versa SEBI regulations kick in.

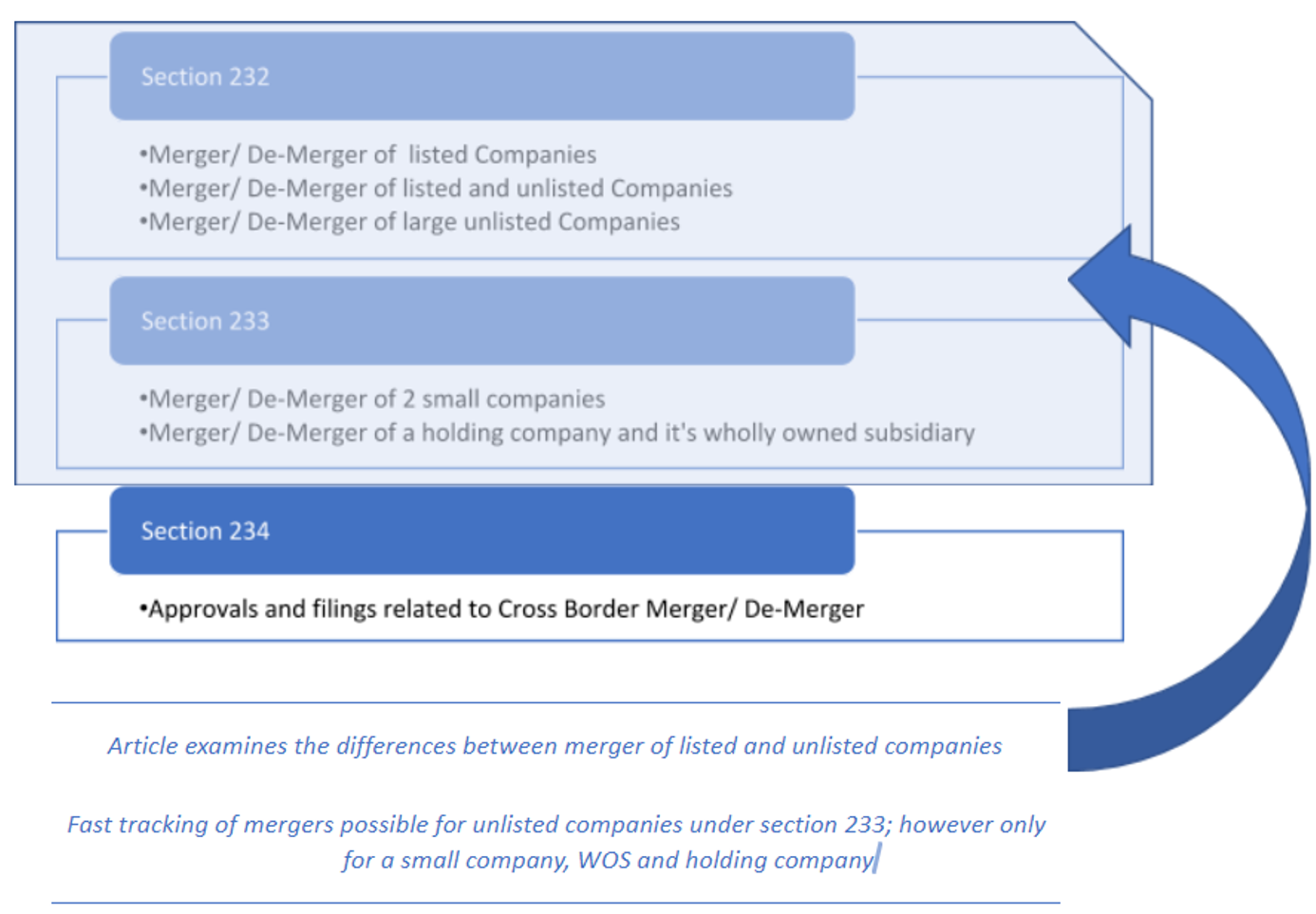

Mergers will fall into the following categories based on class of the merging company – listed or unlisted and foreign or domestic. While Sections 230-240 of Companies Act deal with mergers and demergers, sections 232 to 234 deal basically with statutory filings, regulations and approvals required for mergers and demergers based on class of merging or demerging entity.

Key principles governing Sections 230 through 234:

- Protection of minority interest and public money in the form of retail shareholding in public limited companies

- Protection of creditor interest

- Fast Tracking Merger of small companies, holding companies and subsidiary

In this article, I will limit myself to examining the differences between merger of listed and unlisted companies – Procedural differences between sections 232 (pertaining to listed and unlisted companies) and 233 (pertaining to small non listed companies and wholly owned subsidiary)

Section 233 of Companies Act intends to fast track mergers of small companies, holding companies and subsidiary. Thus section 233 does not apply to all unlisted companies. Therefore it is important to understand the definition of Small Companies as per Companies Act, section 2(85).

Small Company is any company other than public company whose paid up share capital cannot be more than 5 crores and revenue cannot be more than 20 crores.

The procedure for merger/ demerger as per section 233 is laid down below

- The scheme of arrangement is approved by the transferor and transferee company in their respective general meetings by members holding at least 90% of the total number of shares.

- The respective companies will then convene the meeting of their creditors giving the proposed scheme of arrangement which is to be approved by board with a notice of 21 days.

- 90% of the creditors by value must approve the scheme.

- Each of the companies file a declaration of solvency with the registrar and Official Liquidator of the place where the registered office is situated.

- The transferee should file a copy of the scheme with the Registrar, the official liquidator and the Central Government

- The registrar and official liquidator must notify any objections to the scheme and Central government within 30 days failing which the scheme is deemed approved by them.

- In case any objection is received it must be addressed and again approved by board as per step 1.

- After receipt or non-receipt of the objection from registrar or official liquidator if the Central Government decides that the scheme is not in public interest it may file an application within 60 days with NCLT citing the reasons due to which the Central government believes that the scheme should be considered as per procedure laid out in section 232.

- If Central Government does not raised any objection within 60 days of receipt of NOC from registrar or Official Liquidator, the scheme is deemed to be approved.

- 90% of shareholders are required to approve the scheme

- 90% of creditors by value are required to approve the scheme

- Central Government can approve the scheme without any judicial intervention

- Approval process can be brought down to 90 days in case of no comments of observation from registrar, official liquidator and Central Government

All Companies listed or Non Listed not qualifying under section 233 must follow merger/ demerger route as laid out under section 232– 4 key differences between section 232 and 233

Section 232 applies to all companies listed or non listed not qualifying under section 233. Section 232 is aimed at protecting minority interest and ensuring adequate regulatory oversight. There are 4 key differences from section 233 that are enumerated as under:

- NCLT is the approving authority as per section 232 instead of Central Government in case of section 233

- The draft scheme has to be approved by a 3/4th majority by the shareholders and creditors of the merged entity as per section 232. In case of section 233 it had to be approved by 90% of shareholders and creditors.

- As per section 232, the scheme and documents as prescribed have to be filed with multiple agencies – registrar, RBI, industry regulatory body, SEBI, NCL, their observations and objections incorporated into the scheme making it a 6-12 month process. As per section 233 the filing has to be made with registrar, official liquidator and Central Government.

- Additional documentary requirements apart from draft scheme of arrangement are required for NCLT to direct to convene a meeting of creditors

-

- Valuation Report from certified Valuer

- A supplementary financial statement if the accounting statement of last financial year is more than 6 months old

- A report adopted by directors of merging companies explaining the impact of merger on each class of shareholder, promoter holdings, key management personnel laying out the exchange ratio and specifying difficulties if any during valuation.

- SEBI Regulations

While SEBI regulations do not apply to non listed entities, they do come into play in case of merger/ demerger of listed company into or from a non-listed company. SEBI has released several circulars overhauling the scheme of arrangement/ amalgamation requirement for listed entities – September 3, 2009, February 4, 2013, November 30 2015, March, 2017 and January 2018. The January 2018 circular makes amendment to the March 2017 circular based on representations from various stakeholders to ensure that:

- The processing of Scheme of Arrangement is expedited by doing away with redundant filings

- It gives flexibility for continuity of business operations and listing while the process is being carried out

- Prevent misuse of the Scheme of Arrangement to bypass regulatory requirements

So what are the key amendments in the January 2018 circular with respect to merger/ de-merger of listed companies into listed or unlisted entities?

- Exemption of application of circular to merger or de-merger of wholly owned subsidiary into or from the parent. Draft scheme to be filed with stock exchange for information only – Earlier the exemption was available only in case of merger now it is extended to de-merger

- In case of scheme of arrangement between listed and unlisted entity the earlier circular mandated that in the post money shareholding at least 25% will be held by non promoter entities. It is clarified in the latest circular that this 25% limit shall be computed on a fully diluted basis. Earlier 25% limit application was on post money undiluted.

- In case of scheme of de-merger of listed company into unlisted company, the entire pre-money share capital of unlisted issuer (seeking listing) will be subject to lock in conditions (20% of promoters for 3 years and balance for one year). The current circular extends to unlisted companies which was missed out in the earlier circular

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications