In this article, Tejaswinee Roychowdhury who is currently pursuing M.A. IN BUSINESS LAWS, from NUJS, Kolkata, discusses Distressed assets situation in India.

INTRODUCTION

An asset of a company is its resource which has an economic value and the potential for future benefit. The balance sheet of a company reports such assets, and they are meant to expand the firm’s value or ease the operations of the firm. [1] These assets also act as financial securities for future as in case of bankruptcy, mortgages, payments of debts, etc., these assets are sold so that the company can try to sustain.

Often, it so happens, that a company which is swimming in unpaid debts is forced by the bank (or in some cases by the order of the Court) to sell their assets. In such cases, the company may go into liquidation or wind up. Such sale occurs at a low price and the reason may be bankruptcy, debt recovery, or regulatory constraints. The assets that are put on such sale are known as ‘distressed assets’. If a debt is sold, i.e., assets or property sold with legal incidents, then such a debt becomes a distressed debt. [2]

Today, companies try to sell their assets before attaining complete bankruptcy. The company issues financial instruments that are known as ‘distressed securities’. These securities include corporate bonds, bank debts, trade claims, and common and / or preferred shares. Owing to their incapacity to meet financial commitments, these instruments are lowly valued. There is, however, an implied risk factor that manages to offer high returns to potential investors. [3] This is the reason there is a growing trend towards investments in distressed assets, distressed asset funds, etc. with an increase in Asset Reconstruction Companies (ARCs), Securitization Companies (SCs) and Financial Institutions (FIs).

THE PRESENT SCENARIO IN INDIA

ASSET QUALITY REVIEW

India’s banking sector has been suffering blow after blow in asset quality management given the fact that multiple large scale and small scale projects ran into hurdles along the way, such as, poor evaluation of project, extensive delays in project, poor monitoring and poor accounting leading to cost overruns, which disallowed the borrowers from repayment of their loans. Mostly the public sector banks suffered severe impacts and there was a slowdown in growth of credit.

Therefore, the RBI, following the European Central Bank’s (ECB) tests on supervising the Euro banks after the big financial crisis, came up with certain effective measures to remedy the situation and deal with distressed assets before it’s too late. Such efficacious methods to lower the stress of distressed assets include lowering the financial stress of the project such as the JLF, the SDR technique (necessitating the banks’ debt-for-equity swap process and change of management in companies), and the 5/25 mechanism (so that loans for long-term projects, such as infrastructure industries and core industrial sectors, are refinanced every 5 years when they have a tenure of 25 years or above).

Further, in order to make an assessment of how effectively the ‘Bad Loan Management Schemes’, drawn up by the bank Boards individually, were working and in order to make sure that the banks were taking proactive measures to clean up balance sheets, the RBI launched an Asset Quality Review (AQR) as a part of the bank’s mandate to improve the banking sector, clean up bad loans and boost the quality of their balance sheets by March 2017. [4]

FACTORS CONTRIBUTING TO DISTRESSED ASSETS SITUATION

The most important factors that contribute to the distressed asset situation in India today include,

- Excessive amounts of leverages and over-investments during strong economic phases;

- A steady and persistent economic slowdown after the Financial Year of 2011, thus, impacting corporate demand;

- An ease of access to the external debt market and depreciation of the value of the Indian Rupee;

- Industry-specific issues, such as issues peculiar to mining / infrastructure / textiles / aviation / iron & steel, to name a few, which added to the distressed asset issue within the banking sector. [5]

SALE OF DISTRESSED ASSETS

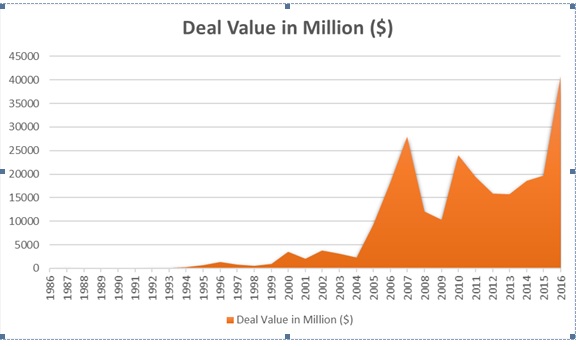

In 2016, a Data Report by Thompson Reuters Eikon shows that Indian Companies’ distressed assets sales have been the highest in the year of 2016 since the liberalization of the Indian Economy. 2016 has seen sale of distressed assets valued at a total of $40.85 billion. A comprehensive chart of the data as collected from 1986 till 2016 (November 7th) has been provided below in Fig 1. This data by Reuters covers the Indian companies’ tangible assets, branches, divisions, operations as well as subsidiaries sold off by parent companies. [6]

Fig 1. Data Report by Thompson Reuters Eikon as on 7th November, 2016. [7]

The sale of distressed assets, as noted earlier, also covers liquidation of companies and bankruptcy of companies. Fig 2 shows the top 10 Indian Companies that have been in the Reserve Bank of India (RBI) defaulters’ list in 2016 (as of April 1, 2016). [8] Further, Fig 3 shows the top 10 Indian Companies that have been in the State Bank of India (SBI) defaulters’ list in 2016 (as of June 30, 2016). [9] These companies, by reason of unpaid debts and bankruptcy, have had their distressed assets sold at comparatively low prices and is fairly responsible for the distressed asset sale boom in 2016 as provided in the Reuters Data. Such companies are also known as ‘wilful defaulters’. A Wilful Defaulter is defined by the RBI as a unit (like a corporation in this case) which has defaulted in making payment or repayment / meeting its payment or repayment obligations to the creditor / lender (mostly banks, LIC, etc.) even when it has the capacity to honour the obligations in question. [10]

| Company

|

Industry | Outstanding

Amt (Cr) |

Wilful

Defaults |

Listed | KeyCreditor (Amt – Cr) | Company Status |

Usha Ispat |

Metals, Mining

|

16911 |

5093 |

Trading Suspended, 2007

|

LIC (8619) |

— |

|

Lloyds Steel |

Steel |

9478 |

6309 |

Yes |

BOI (6724) |

Acquired by Uttam Galva Group

|

|

Hindustan cables Ltd.

|

Telecom cables |

4917 |

0 |

No |

BOI (2439) |

Winding Up |

|

Hindustan Photofilms MFG Co.

|

Photo films |

3929 |

0 |

No |

LIC (1781) |

Wound Up |

|

Zoom Developers

|

Real Estate |

3843 |

137 |

No |

Oriental Bank of Commerce (524)

|

— |

|

Prakash Industries

|

Mining, Steel & Power

|

3665 |

2233 |

Yes |

LIC (2171) |

Operational |

|

Cranes Software International

|

IT |

3580 |

2505 |

Yes |

BOI (3443) |

Operational |

|

Prag Bosimi Synthetics

|

Textile |

3558 |

0 |

Yes |

IDBI (848) |

Operational |

|

Kingfisher

|

Aviation |

3259 |

0 |

No |

PNB (672) |

Wound Up |

|

Malvika Steel

|

Steel |

3057 |

0 |

No |

GIC (2490) |

Wound Up |

Fig 2. Top 10 Indian Companies that have been in the Reserve Bank of India (RBI) defaulters’ list in 2016 (as of April 1, 2016)

|

Name of Company (Wilful Defaulter) and State

|

Outstanding Amount (In Crore) |

|

Kingfisher Airlines (Karnataka)

|

1201.19 |

|

Agnite Education Ltd. (Tamil Nadu)

|

315.45 |

|

Shreem Corporation Limited (Maharashtra)

|

283.08 |

|

First Leasing Co. of India Ltd (Tamil Nadu)

|

235.29 |

|

Teledata Mareen Solution P Ltd (Tamil Nadu)

|

166.85 |

|

Harman Milkfood (Punjab)

|

148.16 |

|

PKS Limited (West Bengal)

|

144.61 |

|

JB Diamonds (Maharashtra)

|

140.96 |

|

Zenith Birla (India) Ltd (Maharashtra)

|

139.59 |

|

MP Shan Text. Pvt. Ltd. (Tamil Nadu)

|

129.48 |

Fig 3. Top 10 Indian Companies that have been in the State Bank of India (SBI) defaulters’ list in 2016 (as of June 30, 2016)

PROCEDURE OF SALE OF DISTRESSED ASSETS – CURRENT RBI GUIDELINES ON SALE OF DISTRESSED ASSETS BY BANKS

The RBI has on 1st September, 2016, issued a notification on “Guidelines on Sale of Stressed Assets by Banks” as a part of the already existing “Framework for Revitalising Distressed Assets in the Economy”. The framework and guideline have been created as a part of the enforcement of and regulations under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI Act).

The Framework covers the sale of financial assets, procedure and norms to be followed during such sale, reasonable valuation of the assets and powers of functionaries and other such persons regarding the decision making procedure towards such sale.

The Framework aims to enhance transparency in the sale of distressed assets. Such transparency, as per the guidelines, are set to be attained in the following way [11] –

- Identifying distressed assets beyond a specified economic value (as determined by the bank) and Special Mention Account classified assets for sale shall be a decision to be taken by the bank’s corporate head office so as to ensure a proper value realisation for the bank by virtue of early identification of such assets.

- The banks are required to identify and prepare an internal list of the assets that are to be put on sale to FIs, ARCs and SCs. This identification procedure should be held at least once every year, ideally, when the year begins and take approval from their Board prior to it.

- The minimum rate at which the ‘doubtful asset’ is to be sold should be reviewed on a periodic basis by the Board / the Board Committee. A view and a documented rationale should be taken on the exit / sale of such asset. As per the above provisions, the assets that are identified for sale should be listed for the purpose of sale.

- It is not necessary that prospective buyers of distressed assets be restricted to ARCs or SCs. Banks may offer assets to other banks / NBFCs or Financial Institutions with the necessary capital and expertise in resolution of distressed assets. In fact, participation of more buyers entails a better price discovery for the assets.

- Since a wide range of buyers are to be attracted, there should be public solicitation of invitation for bids so as to ensure maximum participation from prospective buyers. It is desirable that an e-auction platform be used in such a situation so that there is ease in conducting the auction sale. Further, the auction should be an open process so that there is better price discovery. Banks are required to formulate and lay down policies approved by the Board in this case.

- The banks are required to provide the prospective buyers an adequate time (with a floor of 2 weeks depending on the size of the assets) for due diligence in determining the authenticity of all documents involved, discover frauds, determine the best price according to the market, etc.

- It is required of the banks to have clear and unambiguous policies with due considerations for the valuation of assets that are to be sold at the auction. There must be clear specifications as to internal valuation acceptance and need for external valuation. However, where the exposure is beyond Rs. 50 crores, the bank is required to obtain two external valuation reports.

- The costs of such abovementioned valuation exercises are required to be borne by the bank so as to ensure the protection of the interests of the bank.

- The rate of discount used by the banks in the valuation procedure has to be spelt out and mentioned in the policy. This may either be the cost of equity or the average cost of funds or opportunity cost or any other relevant rate, subject to a floor of the interest rate which was contracted along with any penalty which may be there.

Further, the Framework also provides for restriction on investment by banks themselves in security receipts which are backed by assets sold by them so as to ensure ‘true sale’ of distressed assets and creation of a vibrant distressed assets market, disclosure of investments on security receipts, debt aggregation (where a bank offering the distressed assets for auction sale offers the first right of refusal to the ARCs and SCs that have already acquired the highest and a significant share, matching the highest bid), Swiss challenge method (for placing the Board Approved Policy for auction in light of Paragraph 2 of the annex of the circular [12]) and buy back of financial assets (The guidelines of the RBI do not prohibit banks from taking over certain standard accounts from ARCs and SCs.

Thus, where the ARCs and SCs have successfully executed a scheme for restructuring the distressed assets acquired by them, the banks, using due diligence, have the option to take over such assets after the ‘specified period’, subject to the account performing satisfactorily during such ‘specified period’. Further, banks may frame a policy approved by the Board which contains multiple aspects governing such take over such as type of assets, due diligence requirements, viability criteria, performance requirement of asset, etc. However, it is to be noted that a bank can never take over from ARCs and SCs the assets that they have themselves sold earlier. [13])

INVESTMENTS IN DISTRESSED ASSETS

Distressed assets in India continue to reach alarming levels with every financial year. With such a surge in distressed assets and bad loans, investors in distressed assets are steadily rising to the occasion. Investing in distressed assets is not just beneficial for the banking sector and economy but also extremely beneficial in managing non-performing assets. Additionally, such investors have the potential of ending up as big time winners where they invest at high prices and the business performs better than what was expected of it once the crisis is over. [14] Such investors can be Financial Institutions (FIs), Asset Reconstruction Companies (ARCs), Banks, Securitization Companies (SCs) and even individual persons. Investors can also create funds for the distressed assets which are discussed after ARCs.

ASSET RECONSTRUCTION COMPANIES

In India, mostly ARCs function as distressed asset investors along with a considerable number of SCs. ARCs function somewhat like an asset management company. They transfer the assets they acquire to trusts at the same price and then these trusts issue security receipts to the ‘qualified institutional buyers’ while the ARCs receive management fees from these trusts. In case of any upside between the realized and acquired price, the same is shared amongst the trust beneficiaries (including FIs and Banks) and the ARCs. [15]

This way the ARCs ensure that the banks are able to concentrate on their core business instead of constantly worrying about bad loans. They also help in shaping up industry expertise in arranging loan-resolutions so as to develop secondary markets for distressed assets. ARCs aim to ‘restore the operational efficiency of financially viable assets’ post acquisition and ‘unlock their true potential value or disposing them of for more effective use of blocked funds.’ This way they also stabilize the economy of the country. [16]

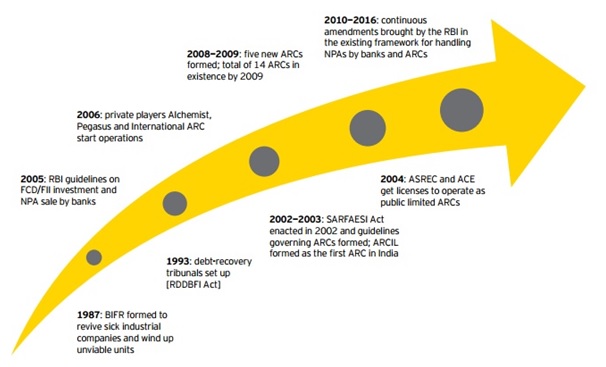

Fig 4 shows the evolution of ARCs in India from 1993 since BIFR formed under the SICA. The BIFR and SICA are discussed at the end of the Article.

Fig 4. ARC Evolution in India. Source – Assocham India, EY, “ARCs at the crossroads of making a paradigm shift”, July 2016 (http://www.ey.com/Publication/vwLUAssets/EY-ARCs-at-the-crossroads-of-making-a-paradigm-shift/$FILE/EY-ARCs-at-the-crossroads-of-making-a-paradigm-shift.pdf)

Some of the top Investors in the Indian Distressed Assets Market include,

Temasek Holdings Pte. Ltd – The Singapore-based firm describe themselves as an equity-only investor wanting to invest in the business of non-performing assets.

Infrastructure Leasing & Financial Services Ltd (IL&FS) – Created a pool with the Lone Star Fund so as to invest almost $2.5 billion in distressed asset purchases.

WL Ross & Co – The US-based firm which also holds a large share in OCM India Ltd, expressed their wish to invest in the textile industry distressed assets.

SREI Alternative Investment Managers Ltd – This Kolkata-based firm is reported to have set aside Rs. 2000 crores in order to invest in debt instruments and assets by buying them.

TPG – The private equity firm has already invested $1.5 billion in India’s distressed assets and are looking to invest more as they see a great investment opportunity in India.

DISTRESSED ASSET FUNDS

While some investors (companies, private equity firms, etc.) invest in distressed assets by buying such assets, transferring them, and by buying loans and debt instruments, there are some investors who choose to set up a fund from where the distressed companies can take easy loans so as to nurture themselves back to health. Such investments are indirect investments.

Often, the Government also helps set up such funds. In fact, it was a bright day for the Indian companies (based in Maharashtra) with distressed assets when Jayant Sinha, Minister of Maharashtra State for Finance, expressed on 31st May, 2016, “We will have a significant stressed asset fund” as reported by CNBC TV-18. It was further reported that there were plans of infusing Rs. 70,000 crores with the help of SBI and some other global funds into the public sector banks for a period of three consecutive financial years starting FY 2016. [17]

Some of the top National and Global Funding Groups include

Piramal Enterprises Ltd – They partnered with Bain Capital Credit, the private equity fund as there seems to be over $1 billion investing opportunity in distressed assets in India.

State Bank of India – The bank, in association with Canada-based Brookfield Asset Management Inc., launched a Rs. 7,000 crores distressed asset fund.

ICICI Bank Ltd – The bank collaborated with Apollo India Credit Opportunity Management LLC in order to apply for an ARC licence, eventually looking forward to setting up a fund for distressed assets.

Apollo Global Management – The US-based global private equity firm partnered with ICICI Venture in 2014 and raised a fund of $825 million for distressed assets.

Tata Capital Special Situations Fund-Trust – It is a funding venture started by the Tata Group and regulated by the SEBI which invests in companies with ‘under-utilized capacities, high leverage, low profitability compared to industry and which have a potential to grow with financial and operating inputs.’ [18]

CONCLUSION

ROLE OF THE JUDICIARY AND ITS CURRENT POSITION

Recently, on 3rd January, 2017, the Supreme Court had directed the Central Government to publish a list of corporate loan defaulters who owe Rs 500 crores or above to various banks in India. The SC Bench comprising of the the-then CJI TS Thakur, Justice A M Khanwilkar and Justice D Y Chandrachud. Despite RBI’s vehement arguments against the same, the Bench opined that the 57 debtors in the sealed cover had defaulted over Rs. 1 lakh crores (as in October, 2016) and it was a ‘phenomenal amount’ which must be disclosed to the public. “Borrowers have taken money from banks and defaulted in repaying the loan. You call this information confidential? It may affect borrowers but how does making information public affect RBI?” [19]– in these words the SC made it very clear that the path that leads up to such massive debts are a matter of public concern as well and therefore, the names of such defaulters should not remain in a sealed cover. This was the opinion of the Bench in a hearing related to Vijay Mallya’s Kingfisher Airlines case after Mallya was able to flee the country taking advantage of such a secrecy.

This opinion of the Supreme Court can very well be described as the Role of the Judiciary in the context of Distressed Asset situation in India. The banks will eventually have to sell the assets of such companies so as to recover the debts. The Bench had further expressed grave concerns about the current scenario in the 34 Debt Recovery Tribunals (DRTs) in India. Just like every other Court, the DRTs too have a massive number of cases pending and debts to be recovered from various large scale and small scale defaulters. While small scale defaulters such as individuals or small businessmen usually have such small scale defaults that need not be required to be recovered from sale of distressed assets, there are definitely cases where the Court decides execution of the decrees / awards vide attachment and sale of the defaulters’ property. Nevertheless, such cases are not treated with enough importance causing them to remain pending over years. Thus, the cases where big corporate loan defaulters owe more than Rs. 500 crores to the banks should be brought to light, as a matter of public policy, and as a tool for creating awareness to help uplift the situation of the DRTs.

Justice Chandrachud pointed out certain statistics that will be helpful in further understanding the situation of the DRTs in India. The DRTs were set up in India in 1993 and by 1995-96, more than 15 lakh cases had been filed by various financial institutions and nationalized banks seeking to recover over Rs. 6000 crores. By October 2015, the DRTs managed to disposed of only about 1.34 lakh cases and recovering Rs. 70725 crores in the process. Currently, more than 70,000 cases are pending in the 34 DRTs across the country which involves more than Rs. 5 lakh crores recovery; and the corporate loan defaulters alone owe more than Rs. 1 lakh crores. It has thus been pointed out by the eminent judge that improvement of infrastructure of the DRTs is more than necessary at this point. Where DRT cases are supposed to be disposed of within 180 days of filing, there are cases that have been pending for over 10 years.

The situation and infrastructure of the judiciary is something on which the Distressed Assets Situation of India depends a lot. The SC Bench pointed out that absence of infrastructure of DRTs is ‘symptomatic of each DRT’ as they lack the manpower and the resources. The SC directed the Central Government to file an affidavit before the Bench with details of a “specific action plan including time-schedules within which the existing infrastructure (of DRTs) would be upgraded so as to achieve the time-frame of 180 days for disposal of claims”. [20]

REHABILIATAION OF COMPANIES (SICA, 1985)

India is the only country in South Asia that has a formal law of rehabilitation of companies vide the SICA enacted in 1985. The SICA empowered the BIFR, a quasi-judicial body, to take appropriate measures for the revival and rehabilitation of potentially viable sick industrial companies and for the liquidation of unviable companies. Just like the Banks’ Asset Quality Reports, the BIFR also makes inquiries to find out if any company has become a sick company and appoints an Operating Agency to prepare reports of the same. The SICA required that when an industrial company becomes sick, the board of directors of such company should make a reference to the BIFR to determine the steps that need to be taken within 60 days of finalization of duly audited accounts for the financial year when it becomes sick. However, no reference can be filed in case the distressed assets have already been acquired by any ARC. Owing to BIFR’s non-punitive and easy going faulted legislative structure, this system under the SICA has fallen into disrepute and the Central Government has strengthened regulations through the banking sector and the Debt Recovery Tribunals along with the SARFAESI Act. [21]

References

[1] Investopedia (www.investopedia.com/terms/a/asset.asp)

[2] Financial Times Lexicon (http://lexicon.ft.com/Term?term=distressed-asset)

[3] Investopedia (http://www.investopedia.com/terms/d/distressedsecurities.asp)

[4] “On swachh balance-sheet mission, RBI to review banks’ loan quality”, Business Line, 9 December 2015; “RBI expects banks to clean up their balance sheets by March 2017”, Mint, 1 December 2015

[5] Assocham India, EY, “ARCs at the crossroads of making a paradigm shift”, July 2016

(http://www.ey.com/Publication/vwLUAssets/EY-ARCs-at-the-crossroads-of-making-a-paradigm-shift/$FILE/EY-ARCs-at-the-crossroads-of-making-a-paradigm-shift.pdf)

[6] Sachin P. Mampatta, Ashwin Ramarathinam, “India sees highest asset sales since liberalization”, Nov 15 2016, Livemint

(http://www.livemint.com/Companies/6DrlXKxx4HtfUD8TBBg9yK/India-sees-highest-asset-sales-since-liberalization.html)

[7] Reuters Data, 7th November 2016 (C:\Users\Tejaswinee\Desktop\download)

[8] Garima Chitkara and Manisha Pande, “RBI Defaulters List: Meet the Top 10”, Apr 26, 2016, Newslaundry (https://www.newslaundry.com/2016/04/26/rbi-default-list-meet-top-10)

[9] Dipu Rai, “Meet SBI’s top 100 wilful defaulters”, 5 Nov, 2016, DNA (http://www.dnaindia.com/money/report-meet-sbi-s-top-100-wilful-defaulters-2270272)

[10] Ibid 8

[11] Paragraph 2, Annex, Guidelines on Sale of Stressed Assets by Banks, RBI/2016-17/56, DBR.No.BP.BC.9/21.04.048/2016-17

(https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10588&Mode=0)

[12] Ibid 11

[13] Paragraph 8, Annex, Guidelines on Sale of Stressed Assets by Banks, RBI/2016-17/56, DBR.No.BP.BC.9/21.04.048/2016-17

(https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10588&Mode=0)

[14] Dan Caplinger, “Distressed Assets: Investing Essentials”, Aug 14, 2014, The Motley Fool (https://www.fool.com/investing/general/2014/08/14/distressed-assets-investing-essentials.aspx)

[15] Ibid 5

[16] Ibid 5, 15.

[17] Aparna Iyer, “Govt planning fund to invest in distressed assets of banks: Jayant Sinha”, 1 Jun 2016, Livemint

(http://www.livemint.com/Industry/6gC3ratQCcciLUT0j88SaN/Govt-looking-at-a-significant-stressed-asset-fund-Jayant.html)

[18] http://www.tatacapital.com/private_equity/ssf_overview.htm

[19] As Quoted by – Dhananjay Mahapatra, “SC: Make public list of corporate loan defaulters”, 4 Jan 2017, TOI (http://timesofindia.indiatimes.com/india/sc-make-public-list-of-corporate-loan-defaulters/articleshow/56322793.cms)

[20] Ibid 19

[21] Sumant Batra, “Insolvency Laws in South Asia: Recent Trends and Developments”, Insolvency Laws – Issues and Perspectives, Edited by P. Satyanarayana Prasad, Amicus Books, The Icfai University Press, 2007. Pg. 193 – 234

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications