This article is written by Rajeev Awasthi, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from Lawsikho.com. Here he discusses ”First hostile takeover tussle in the Information Technology Industry in India”.

Table of Contents

Introduction

Ever wondered what Anheuser Busch InBev and SABMiller, Arcelor and Mittal, Melrose and GKN, Vodafone and Mannesmann, Kraft (now, Mondelez) and Cadbury, RBS and Natwest have in common. Well, you guessed that right, these have all been time tested and formed due to the acquirer reaching out to the shareholders’ of the acquiree company directly and acquiring greater than or equal to fifty-one per cent stake or voting rights in the board of the acquired company. The channel of reaching out to the shareholders directly with the proposal of an open offer when the proposal is not accepted by the acquired companies board is termed as the ‘infamous’ hostile takeover.

Since India’s economic liberalization in 1991, the Indian market has not witnessed many such hostile takeover attempts by listed companies. The term ‘hostile’ is associated with this type of takeover route as the bidders making tender offers opt to by-pass the negotiation channel with the target company’s board in order to seek control. Thus, this route carries with itself the threats of destabilizing the normal operations of the target company at any time, it also threatens the shareholders of the target company as well as the management. Hence, the need to regulate market control in the field of takeover is relatively high.

The Indian economy has witnessed several mergers and Acquisitions post Independence period. The Indian economy witnessed only a handful of M&A Takeovers prior to 1990s. The government devised ways to limit the concentration of economic power through the introduction of policies on balanced economic development and the introduction of Industrial Development and Regulation Act of 1951, Monopolistic and Restrictive Trade Practices, “MRTP” Act of 1969, Foreign Exchange Regulation, “FERA” Act of 1973 etc. The policies were stringent enough for the Indian economy to witness any hostile takeover of its kind. However, after liberalization in 1991 and with policies on decontrol and liberalization and the globalizing economy, the corporate sector witnessed a severe domestic and global competition. The period of recession saw a lot of corporate restructuring happening through M&A more so because of the fact that the organizations wanted to divest those areas of businesses which were not yielding profit and concentrate on the areas of business which yielded a profit. The M&A activity in India has seen some major mergers, acquisitions and/or, amalgamations in the past like Vodafone’s $11.1 bn acquisition of Hutchison Essar, India’s fourth-largest telecom operator. Tata Steel’s $13.2 bn acquisition of European steelmaker Corus was another major acquisition activity of 2007.

Regulatory Provisions in India to comply with during M&A

Adherence to compliance needs to be maintained with respect to the below regulations that have the statutory force of law and are equipped with penalty provisions for violation of any of them:

- “Takeover Code” under the provisions of SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 1997. Corporate Restructuring may be done by M&A, Spin-Off, Leveraged buyouts or through Hostile Takeover.

- Code of Civil Procedure, 1908.

- Indian Trusts Act, 1882.

- SEBI (Prohibition of Insider Tradings) Regulation, 1992.

- Partnership Act, 1932.

Behind the scene picture: David versus Goliath

(How pieces added up for the Indian IT Industry’s very first Hostile Takeover bid)

Understanding the David “Target” of the battle: Mindtree

- Date of Incorporation 05-Aug-1999

- Date of Listing 07-Mar-2007

- Listing Public (NSE, BSE)

- Headquarter Bengaluru, India

- Board Members and Directors:

- Krishnakumar Natarajan Executive Chairman

- NS Parthasarathy Executive Vice Chairman

- Akshaya Bhargava Independent Director

- Manisha Girotra Independent Director

- Apurva Purohit Independent Director

- Pankaj Chandra Independent Director

- Milind Sarwate Independent Director

- Rostow Ravanan Managing Director & CEO

- V G Siddhartha Non-Executive Director

- Subroto Bagchi Non-Executive Director

- Founders:

- Ashok Soota

- Subroto Bagchi

- Krishnakumar Natarajan

- Parthasarathy NS

- Scott Staples

- Revenue US$846.8 Million (FY 2017–18)

- Operating income US$107 Million (FY 2015–16)

- Net income US$62 Million (FY 2016–17)

- Number of employees 20,000 (FY 2018–19)

- Services:

IT, Business consulting and outsourcing in fields of e-commerce, mobile applications, cloud computing, digital transformation, data analytics, enterprise application integration and enterprise resource planning, with more than 339 active clients and 43 offices in over 17 countries, as of 31 July 2018.

(Source: Wiki Mindtree)

Understanding the Goliath “Acquirer” of the battle: L&T

Incorporated in 7-Feb-1946

Listing Public (NSE, BSE), GDR’s listed in LSE, LUX

Headquarter Mumbai, India

Board Members and Directors

-

- A.M. Naik Group Chairman

- S.N. Subrahmanyan MD & CEO

- R Shankar Raman CFO

- N Hariharan Company Secretary

Founders:

- Henning Holck-Larsen,

- Søren Kristian Toubro

Revenue: US$17 billion (2017)

Operating income: US$12 billion

Total Assets: US$32 billion (2016)

Number of employees: 307,053 (March 2018)

Services: Real estate, Construction, Financial services, IT Services

Intent and Route

During a takeover, if the acquirer organization owns 25% of the target organization, it can make an offer to gain control. However, L&T is making a move for a hostile takeover of Mindtree by exploiting a loophole in section 3, clause 1 and section 4 of the Takeover Code of the SEBI and thereby announcing an open offer.

According to the process laid out in the above section:

- Those with more than or equal to 25% stake cannot take over a company unless they make an open offer to acquire the shares and make a public announcement.

- Irrespective one holds or does not hold shares or voting rights, they can only take control of the company once a public announcement of an open offer is made to acquire those shares.

Using the above sections the takeover code permits L&T to make an open offer, without having to own 25% ownership in Mindtree.

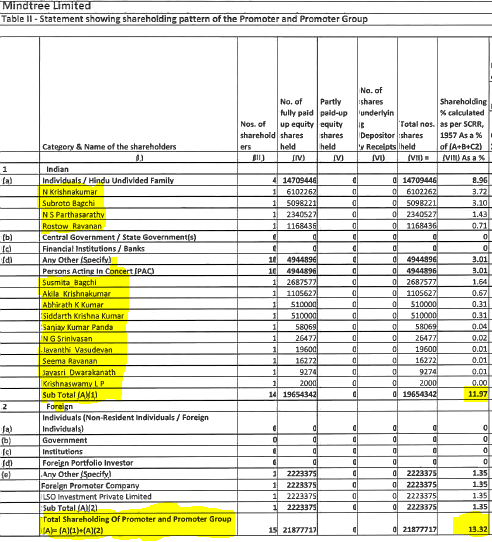

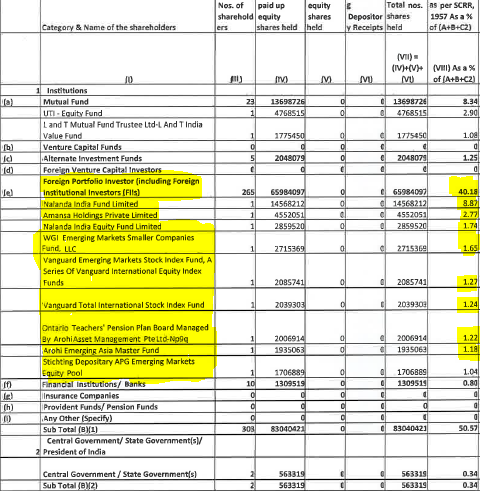

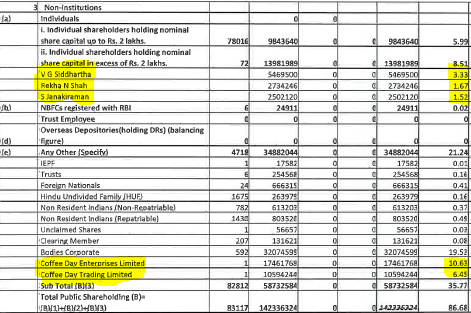

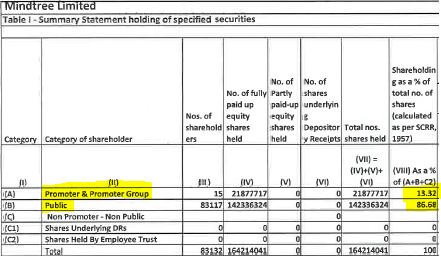

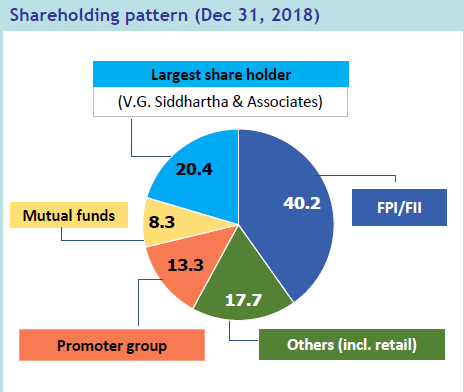

Mindtree Current Shareholding Pattern: Click here (Dec 31, 2018)

Structuring the Deal

The way in which the deal has been structured is in itself very interesting as it involves complete takeover through:

- share purchase agreement (20.32%)

- Market purchases through the stockbroker (15%)

- Open offer (31%)

- L&T decided to not make a voluntary offer after having acquired VG Siddhartha’s stake. It instead decided to go ahead with the mandatory offer route through channelling additional purchases.

The above table shows the current shareholding pattern of Mindtree. On March 19 2019, L&T signed a deal to purchase 20.39% stake from VG Siddhartha the owner of Cafe Coffee Day at Rs. 980 per share and has also placed an order with its broker for the additional purchase of up to 15% of share capital in the market at Rs 980 per share. The share purchase agreement couple with the order L&T placed with the broker breached the 25% threshold and hence, L&T was mandated to make an open offer as prescribed in the SEBI (Substantial Acquisition of Shares and Takeovers) Regulation (3(1) and 4), 2011. Thus L&T additionally announced an open offer to the public shareholders of Mindtree to raise an additional 31% of the outstanding shares pricing them at Rs 980 per share and the deal amount to $1.6 bn. If this gamble from L&T works it will hold a majority of nearly 66% stake in Mindtree whilst the promoters of Mindtree together will hold 13.32%. Other institutional investors viz. Amansa Holdings, Nalanda India Fund, and Vanguard cumulatively hold 50.57%.

The bone of contention to the Board Members of Mindtree & the way forward

It’s now a battle to reach more than 51% holding and beyond to exercise a de jure control…

If we assess the entire scenario, it is evident that the root of the hostile takeover upsprung was due to the fact that the promoters kept a small chunk of the share and eventually VG Siddhartha accumulated a greater portion of the share capital. The board members of Mindtree met on March 20 to discuss if a buyback proposal of all paid equity shares could be considered to fend off the hostile takeover bid from L&T. The independent directors will be bound to think about all the stakeholders and not just the promoters who are averse to this takeover. This ain’t as easy as it sounds as this would require the shareholder approval via a special resolution that is two-thirds of the votes as an open offer has been announced. Siddhartha’s share purchase agreement with L&T will motivate him to vote against the buyback. The Companies Act allows a company to buy back a maximum of 10% of its capital. In case the special resolution passes the proposal, then they can buy up to 25%.

As per the existing norms and regulation that in case the promoter purchases more than 5% or any other buyer purchases more than 25% stake in any listed firm, an open offer is triggered. As such, to purchase another 26% stake the only channel is through an open offer.

Since we are discussing the distribution of the number of shares held and L&T’s motive of achieving the golden figures of 25% and thereafter by open offer achieve 66% stake in Mindtree. It is worth noting the low percentage of shares held by the promoters 13.32% which may be sufficient to thwart a hostile bid.

The regulation requires the target to constitute a committee of independent directors since the promoters and management are always conflicting in the matters of takeovers. Such independent director committee will advise in the best interest of both the parties by weighing in the overall interest of the situation. The independent directors will reach out to the financial advisor to understand if the price offered by the acquirer to the shareholders of the target is fair and reasonable. The advice of the independent directors will only be advisory in nature and not binding but in the best interest of all.

The fiduciary duties laid out in Section 166 of the Companies Act will also be binding on the Directors (including members of the independent committee) of the target. Section 166(2) explicitly states that the independent directors should base their decision not only in the interest of the shareholders but also the other stakeholders which include the creditors, employees and customers. They should weigh in if the takeover is allowed to succeed, it should be beneficial in the long term interest of the company especially in this case where we have seen Mindtree has had a good client base across the globe and is a moral example of good corporate governance.

In case the board of directors in good faith have adopted a view that the hostile takeover offer is not beneficial for the shareholders, they can adopt the process of Revlon Rule and approach any other competitive bidder could be a white knight offering equally good pricing. These might come into play depending on what shape the L&T and Mindtree hostile takeover take.

Will there be a white knight in the fairy tale of Mindtree?

The white knight defence route is permissible under the Takeover Regulations and this has been used in India in the past see here. The regulatory stance on white knight as permitted under the Regulation is that it doesn’t permit the target’s board to prevent a takeover but it provides a choice to the shareholders to choose the more favourable amongst the competing bidders.

According to this Livemint report, large private equity players like KKR and Baring had expressed their interest in Mindtree initially and there are hopes that they might emerge back in the competing offer against L&T’s bid as Mindtree’s white knight. However, as per the takeover regulation a competitive offer has up to fifteen days beginning March 19 to make its offer to the shareholders of Mindtree. The takeover code also requires the competing offer to be at least equal to the holding of the acquirer who makes the first public offer summed with the shares to be acquired by the first acquirer’s open offer. So, the more L&T acquires via the three strategies the greater the stake and the greater the challenge for the upcoming white knight (if any).

The reason for the golden figure to be set at 66%

The one-line answer is that it’s more than required holding for L&T to control Mindtree or even consolidate its earnings. L&T has about 16,000 crores in cash on its balance sheet invested in treasury products and earning a post-tax return of about 5%. L&T had decided to return around 9,000 crores back to shareholders via a share repurchase program or buyback which was not approved by the market regulator SEBI. Hence, when Siddhartha opted to divest his holding it presented the best way for L&T to achieve better ROE. At this point, L&T estimated that with an expense of 10,000 crores from its earnings it can achieve control over 66% of Mindtree which has a market cap tad shy of 16,000 crores.

This era may just belong to Goliath

On April 5 2019, the Competition Commission of India through a tweet approved L&T’s offer of claiming 66.15% ownership in Mindtree on a fully diluted basis, which is being seen as the first step to L&T’s success in its bid of the hostile takeover. L&T is now all set to approach the anti-trust authorities in the US and Germany where Mindtree operates. As for Mindtree, they have formed a body of their independent directors who are lead by Apurva Purohit. They are weighing in all the aspects of the ‘unsolicited’ offer looking into all the relevant facts, circumstances, data and provide an informed view, bearing in mind the interest of all stakeholders in the company. The independent director’s panel has roped in Khaitan and Co, and ICICI Securities as the independent advisors.

Conclusion

Though L&T’s chairman has provided an objective of creating an IT consulting and services giant through a merger of Mindtree, L&T Infotech Ltd, and L&T Engineering Services Ltd. The major theme in this case study which we need to think about was had VG Siddhartha’s holdings in the company not reached to the levels of being the single largest shareholder, even though he was not a member of the board or an independent director the story would not have escalated. Also, the holdings of the promoters in the case of Mindtree was too less when compared to the total outstanding shares available or those with FII’s. To end I would quote the management guru Peter Drucker, “Many problems cannot be solved; they have to be survived.”

Update: L&T was successful to carry out first of its kind hostile takeover of Mindtree. The acquirer was able to buy 31% additional stake through an open offer and gained a controlling stake by increasing its holding to 60%. The offer of 980 apiece shares of Mindtree was subscribed 1.2 times. The longer-term view of the chairman Mr. Naik is, he’s looking to make a software conglomerate by planning a merger between L&T Infotech and Mindtree after 2 financial years. Looking at the financials and technical’s of the company as of Feb 15, 2020 we see that Mindtree made a low on its stock prices of 652 INR on July 22, 2019, but post takeover it’s stock prices have been trading considerably over its 20d, 50d, and 100d exponential moving average. The stock closed at INR 959.9 on Feb 14, 2020, and was trading close to its 52-week high price of INR 995 which it touched on Apr 25, 2019. The price per equity share is 25.35 which are very good compared to its peers like TCS which has P/E of 24.95. The earnings per share are at 37.86 which is way above than the Software Industry P/E of 23.49. The company reported strong financials. The Income which grew from 5325 Cr. in Mar’18 to 7021.5 Cr.in Mar’19 i.e. 32% growth YoY. The diluted EPS also grew by 26% YoY. The current liabilities of the company went down from 958 Cr in Mar’18 to 855 Cr. In Mar’19. Overall the whole process of the takeover was not smooth but the account books and the market do see it very positively.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications