This article is written by Keshav Bhardwaj, pursuing a Diploma in Companies Act, Corporate Governance and SEBI Regulations from Lawsikho.com.

Table of Contents

Introduction

In recent years, the internal auditor played a vital role in making the decision that affects the management or economic resources of the company. At the same time, corporate governance has also gathered extensive attention, because of accounting scandals and corporate breakdowns i.e. Satyam scam, Punjab National Bank fraud. “Satyam scam” raises a big question mark on the corporate governance system, which gives us a lesson that there is a requirement of good Corporate Governance and the Auditing Standard and Regulation. It also further leads to the revolution in the Indian corporate world. Another incident named “Toshiba Scandal”, Toshiba well-known company of Japan emphasizes the relevance of corporate governance & how much role the organization culture plays in quality corporate governance.

With the additional investigations of the scandal, the investigation committee observed that internal auditors can perform their practice freely only if the audit committee is capable enough, free to function. There must be a reporting mechanism for the Internal Auditor to report the same to the Audit Committee.

Before proceeding further, let’s understand the basic meaning of the terms Internal Auditor and Corporate Governance:

Internal Auditor definition:

Institute of Internal Auditors (USA) has defined that:

It is an autonomous, objective assurance and advising activity created to feature value and enhance an organization’s operations. It assists an organization to achieve its purposes by accompanying a systematic, disciplined method to assess and enhance the effectiveness of risk management, control, and Governance Processes. [The same Definition is adopted by the Institute of Cost Accountants of India].

The Internal Auditor is nowhere defined in the Companies Act, 2013. Nonetheless, the same is defined in the Preface to the Standard of Internal Auditor by the Institute of Chartered Accountants of India as defined under:

It is an autonomous management function, which includes a continuous and explanatory assessment of the functioning of an entity with a motive to infer improvements thereto and add value to and empower the entire governance mechanism of the entity, comprising the entity’s strategic risk management and internal control systems.

In simple words, the Internal Auditor is an independent body which keeps a check upon company’s governance, makes risk analysis and builds internal controlled systems within the company. e.g. Internal Auditors team submitted the Risk Assessment Report to the Audit Committee of the company.

Corporate Governance definition:

To understand what Corporate Governance is, let’s first look at the origin of the word Governance. The Governance word originated by joining two words- Gubernare (Latin Word) + κυβερνητικός (Greek Word) = to rule or to steer + Steering. The concept of Steer man- the person at the helm is an expressly valuable insight into the reality of Governance [Source: Ticker (1984:9)]. It’s simply meant to get control over something and to provide direction. For Example, after 10 years of the helm of Company, A intends to retire and B will take the helm in July 2020.

There is no specified definition of Corporate Governance to be strongly agreed upon. There are a variety of definitions recommended. Out of which, the definition agreed by most of the stakeholders was given by Parkinson in 1994. The definition is as follows:

This is a method of guidance and control proposed to assure that the company’s management acts as per the interest of stakeholders.

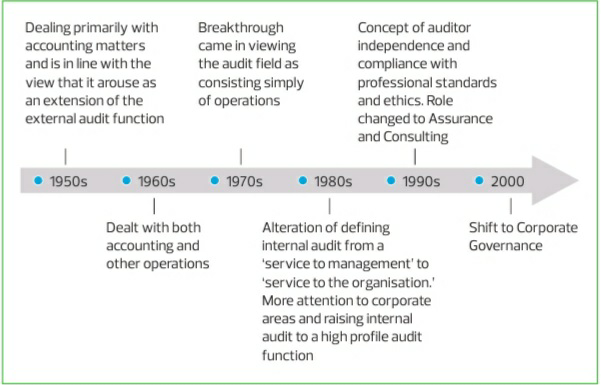

How the role of internal audit shifted to corporate governance over the six decades

Internal Audit – The Changing Landscape

This journey started in the decade 1950s where the Internal Auditor’s primary function was to deal with accounting matters and it evolved as the addition of external auditing functions. In the 1960s, it started to deal with accounting as well as other operations. In the 1970s, there was a development take place keeping in view the auditing only including manageable operations. In the 1980s advancement came to occur, the service of Internal Auditor no more just to provide service to the Management, it extended up to the goal of the Organization. Therefore, the Internal Audit raised the bar to Corporate Areas & High Profile Roles. Finally, in 2000 decade the role of internal auditor shifted to Corporate Governance to maintain all rule and regulation in the interest of Shareholders.

Who can perform the internal audit under Section 138 of the Companies Act, 2013

- The Person to be appointed as Internal Auditor by the Companies should be professional E.g. Chartered Accountant or Cost Accountant or any other professional as recommended by the Board of Directors.

- The term professional has a broader scope, such as Companies Secretary or Lawyer can be appointed as the Internal Auditor to the compliance promptly.

- But there is no set form or method for an Internal Auditor to prepare the reports; hence Companies can decide to conduct according to their size & requirements.

- The Report should comprise compliance and deviation if any and the way to reform the error if found so. The process must be given due weightage so that it examines the affair of the Company truly and fairly.

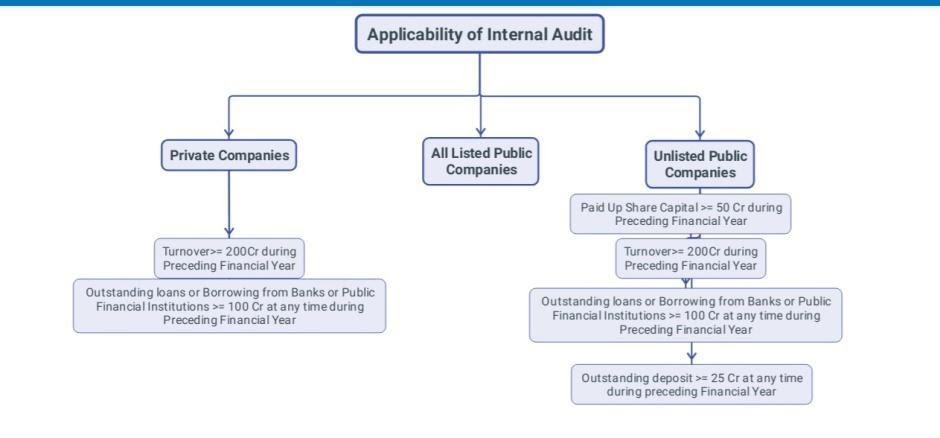

Applicability: Is internal audit necessary for every company

The Applicability of Internal Auditor on Class of Companies is given under Rule 13 of the Companies (Account) Rules, 2014:

The Companies which required mandatorily appointing Internal Auditor are given under:

- Every Listed Company: It applies to all Companies without any specific criteria or threshold.

- Unlisted Public Companies:

|

Serial No. |

Criteria |

Threshold Limits (₹) |

|

1. |

Turnover |

200 Crores or More |

|

2. |

Outstanding loans or Borrowings from Bank for Public Financial Institution |

100 Crores or More |

|

3. |

Paid Up Capital |

50 Crores or More |

|

4. |

Outstanding Deposits |

25 Crores or More |

*Rule to Remember: Divide every level into Half.

- Private Companies

|

Serial No. |

Criteria |

Threshold Limits (₹) |

|

1. |

Turnover |

200 Crores or More |

|

2. |

Outstanding loans or Borrowings from Bank for Public Financial Institution |

100 Crores or More |

*Rule to Remember: Divide every level into Half.

Other provisions to be complied with are:

- The Internal Auditor may or may not be the employee of the Company. The Chartered Accountant considered within its scope whether in the practice or not.

- The Audit Committee connected with the Board shall set down the rule and method for the functioning of the Internal Auditor.

- The Act has given the authority to the Board and Audit Committee to define the duties of the Internal Auditor. There isn’t any specific time frame but it is recommended to conduct audits quarterly for good practice and governance.

Interpretation of the connection between internal auditor and corporate governance

Internal Auditing activities have been developing in corporate entities for many years, but there are still several limitations. An internal Auditor requires keeping a check upon several events for sound Corporate Governance. As per the survey conducted by The Institute of Cost Accountants of India found that 86 percent of the companies have established the Audit Committee in their company. Half of the private companies that aren’t statutorily mandated to form the Audit Committee have formed the equivalent. This is encouraging for the internal auditing profession since this would definitely promote the relatively smaller companies to follow the development. Establishing an Audit Committee by companies is a step towards good corporate governance to assure audit independence, for both the statutory & the internal auditor.

- Internal Audit as an integral part of Corporate Governance: The Various Corporate Bodies like Board of Directors, External Auditors, and Internal Auditors collectively determine the security of Corporate Governance. Internal Auditor requires mitigating several risk factors which are a menace to the accomplishment of the Company’s Objectives. The Internal Auditor monitors the operations, analyzes the processes, and assesses all possible things that may occur appropriately. This indicates the risk factors and existing impediments in internal governance. Then report the same to Management. Therefore, It keeps a check on whether the Corporate Governance Structure has an effective system that aligns with the achievement of the Company’s Objectives or not.

- The role of Internal Audit in developing effective Corporate Governance: Foreign Companies are well known for the fact that to make effective governance it’s essential to appoint Internal Auditors in the Company, also Company sustainable development is integrated with the internal auditing. This is mainly divided into two aspects:

- Internal Audit is an important means to promote effective Corporate Governance: In the modern company policy, clear rights & responsibilities of every Body and Entity are given clear, but Government bodies and entities get separated. Investors or Shareholders are not much aware of the regulation, operations, and unforeseen risks. Potential Investors always look out at the Company’s ability and operations before investing in the Company. The Internal Auditor has discovered a way to deal with these difficulties through autonomous and accurate analysis. It can assess the Company’s performance and direct the resources of the Company. The Internal Auditor is a more familiar Status Quo of the Company; hence it always makes the more appropriate decision.

- Internal Audit and Corporate Governance have a common purpose: Corporate Governance always looks out to balance the investor interest as well as the economic concern of the Company. The Internal Auditor also oversees the operations of the Company and indicates the difficulties of the Company, consequently helping the Company to improve the performance as well as economic growth. Hence, the Company should maintain governance for independence in the working of Internal Auditors as it’s not regulated from Government Rules.

- The impact of Corporate Governance on Internal Audit Environment: The Internal Auditor determines the growth of the Company by effectively reviewing the operations of the Company. To promote the growth of the Company, It is recommended that the Internal Auditor should work independently without any pressure from the Audit Committee. The independence of the Internal Auditor is ensured by effective Corporate Governance.

Barriers in the due process of modern corporate governance

Many Indian companies in this modern world are not able to organize an efficient mechanism for Corporate Governance in their Company. Consequently, many investors found hectic while investing in any Indian Company, which also reflected the Corporate Governance Failure. For Example:- Satyam Scam & Yes Bank Scam have raised the question upon the Corporate Governance of Company as well as Regulatory Authorities. Many such events happened which downgraded the image of India Companies in the Corporate Market. International Finance Corporation and the Hawkamah Institute in Dubai makes available a region-wide corporate governance research. In research it was found that, around 56% companies do not have a proper knowledge of the definition and importance of corporate governance. Moreover, almost all companies (95%) showed that their governance system was required to be enhanced in some aspects.

“In a webinar quick poll of 1,750 internal auditors conducted by Kroll and The Institute of Internal Auditors in July 2020, it was discovered that 65 percent of internal audit professionals opine that COVID-19, working from home, and financial pain would leads to an enlarged risk of fraud. Over three quarters (77 percent) opine that, if internal audits were more involved in strategic fraud risk management, the fraud risk management would develop.”

- Governance Issues in India are much different than issues that are observed in Developed Countries. Indian Regulatory Bodies require giving attention to the Board of Director’s role in Corporate Governance. By making this mandatory, all directors of the Company should be well aware of Governance Rules as said by Protiviti (Global Consultancy Firm).

- Internal Auditors not able to work freely, they are abiding by the Audit Committee which is attached to the Board of Directors. For Example, Toshiba Company’s Internal Auditors did not receive much attention from the Top Management. The Audit Committee of the Company is not efficient in working. Hence, it’s difficult to achieve the required result.

- Internal auditors are not qualitative in work. The Internal auditors are not able to manage audit work along with financial tasks adhere to Professional Ethics, For Example, Andersen Incident to retain a large number of clients or to receive the substantial audit fees, Internal Auditors perform auditing in an unethical manner.

- There is a lack of technical knowledge. The internal auditors are not well aware and the updated technology which results not only did not achieve the proposed outcomes, but further, it takes more time, resources, and other resources.

Ways to strengthen internal audit and improve corporate governance

The efficient Internal Auditing leads to the prevention of fraud or unethical behaviors in the company, which preserve the interest of Shareholders and the Investors. They will be able to apprehend the difficulties existing in the Company. There are many shortcomings which Indian companies require to deal with. Strengthening Internal Auditing is the way to promote the healthy growth of the Company. There are many such companies in the world, in which internal auditor able to balance the corporate governance of the company:

|

Company Name |

Key Challenges |

Key Changes |

|

Butec Holding SAL |

There was no internal audit mechanism. |

Built an internal audit mechanism for analyzing the risk, internal control & direct reporting to the new audit committee. |

|

Dana Gas |

The internal audit role was limited in their ambit and no route to directly report the board. |

Employing an internal auditor and enlarging the function of the internal auditing to make sure coverage of financial and operational activities; reports autonomously to the Board. |

|

Kashf |

The internal audit function was working properly, but there isn’t any mechanism. The internal audit head didn’t report directly to the Audit Committee of Board. |

Built a direct reporting mechanism between the internal audit and audit committee. Also, the internal audit now reports to the Board on a monthly basis. |

|

No route to directly report the board. |

Provide an open communication environment between the audit committee, internal auditors and the board. Company also held meetings between auditors and the board every quarter or as per the circumstance may be. |

For reading more such successful case studies, click here.

There are some ways to strengthen the Internal Audit and Improve Corporate Governance by implementing things as given below:

- Internal Audit can be improved by learning Foreign Advanced Auditing techniques and combining it with National Regulation.

- With the aid of modern technology and computers, Data Model gets established, less Workload, and Quality work in a short span time.

- The Government also requires making rules and regulations to make auditing more Standardized and Professional. Also, improve the laws related to auditing. So, the Internal Auditor work is more organized, independent, and transparent.

- The Top Management of the Company must be well acknowledged with Corporate Governance and make internal rules to promote transparency, cooperativeness, and independence between the Audit Committee and Internal Auditor.

- The Company should regularly organize the training program for making Internal Auditors well aware of modern ways or techniques.

- The Audit Committee should monitor what is and what is expected from the Internal Auditor. After identifying the gap, submit such reports to Internal Auditors from time to time.

- Internal Audit should be allowed to participate in discussions with the Top Management of the Company. The Audit Committee submits a report which reflects the position of Corporate Governance to the Top Management of the Company.

How the Satyam scam, Yes bank scam, or Punjab National bank fraud could have been avoided because of the auditors?

Over the years, many Audit scams have taken place. With due course, regulatory bodies has learnt little from these faults, but still there are lots of things require to deal with, to avoid such scams in future:

- One of the remedies may be to alter the monopolistic role of one institution for financial, tax audit, and other professional bodies.

- Improving the internal control system of the Company.

- Strict punishment for committing fraud.

- Adherence to all the guiding principles of RBI with regard to Know Your Customer (KYC) and lending proposals.

- A dedicated cell within each bank to keep an eye on the company to which they are lending capital or market where products are marketed.

- Triggers should be created for all transactions having any change.

- Reserve Bank of India (RBI) should make sure that the process of reporting Red Flagged Accounts (it was introduced by RBI for taking action on early warning signals, which include raids by regulatory and tax authorities. Once an bank account declared red flagged, banks have to necessarily to finish its forensic inspection within period of six months and settle on decision whether it is fraudulent or not) is being tested considering the parameter at regular time gap that whether a fair stability between all types of errors is being adopted by the banks in this course.

- The holistic assessment has to be made by the Ministry of Corporate Affairs (MCA) i.e. they must assess the reporting disclosure principles of corporate, including banks.

Conclusion

The Internal Auditor empowers Corporate Governance through control and mitigation of risks. It keeps on reviewing the Structures and Procedures of the Company and advises whether it’s healthy for the organization or not. As the risk rises, the Internal Auditor roles are going to expand towards behavioral, Non-Financial Reports, Risk Governance Advisory.

As the companies are moving towards digital the Internal Auditor needs to mitigate all the risks expected to occur in the tech world. With the accumulating pattern of risk created by new technology, geopolitics, cyber-security, and disruptive innovation, a vibrant and agile internal audit function can be an indispensable resource supporting sound Corporate Governance.

Al last, here are the 5 things the Company should ensure, for good governance and to meet the requirement of Stakeholders:

- Whether the Internal Auditor takes part in discussions related to Risk & Governance?

- Is the Internal Auditor appointed at the right position and resourced to accommodate Advisory Service?

- Is the Internal Auditor head free to engage with the Board and Audit Committee without any inconvenience?

- Does the Company provide Internal Auditors with the Cooperative & Healthy environment to shine?

- Does Company have any framework to make the Internal Auditor projects agile and experimental?

References

Rule 13 of the Companies (Account) Rules, 2014

Section 138 of The Companies Act, 2013

INTERNAL AUDIT – THE CHANGING LANDSCAPE

RELATIONSHIP BETWEEN INTERNAL AUDIT FACTORS AND CORPORATE GOVERNANCE

On the Role of Internal Audit in Corporate Governance

INTERNAL AUDITING PRACTICES IN INDIA

Corporate Governance Success Stories

From Satyam to PNB -Audit Mechanism Collapse Is Evident

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications