In this article, Arijit Bhowmick pursuing M.A, in Business Law from NUJS, Kolkata discusses Valuation of Start-ups.

Introduction

Young companies are hard to value for a number of motives. Some are start-up and idea agencies, with very little revenues and running losses. Even the ones young companies which might be worthwhile have short histories and maximum younger companies are structured upon private capital, to start with owner savings and assignment capital and private fairness afterward. As an end result, many of the same old techniques we use to estimate cash flows, increase quotes and discounts both do no longer paintings or yield unrealistic numbers. In addition, the truth that younger companies do now not live to tell the tale must be considered someplace inside the valuation. In this paper, we observe how first-class to fee young corporations. We use an aggregate of facts on more mature companies inside the commercial enterprise and the agency’s personal traits to forecast revenues, income and coins flows. We additionally set up tactics for estimating discounts for private capital and for adjusting the value these days for the opportunity of failure. In the manner, we argue that the challenge capital method to valuation that is widely used now’s mistaken and ought to be replaced.

Valuing corporations early inside the lifestyles cycle is tough, partly because of the absence of operating history and partly because maximum younger firms do no longer make it thru those early tiers to fulfilment. In this article, we will have a look at the challenges we are facing when valuing young corporations and the quick cuts hired by many who have to estimate the fee of these businesses to arrive at fee. While a number of the guidelines for valuing young groups make intuitive sense, there are different regulations that necessarily cause erroneous and biased estimates of fee.

Young companies in the economy

It can be a cliché that the entrepreneurs provide the energy for economic increase; however it is also genuine that colourful economies have a huge quantity of young, concept companies, striving to get a foothold in markets. In this segment, we will start via taking a have a look at in which young agencies fall within the business lifestyles cycle and the function they play within the usual financial system. We will observe up via looking at a few traits that younger businesses generally tend to share.

A Life cycle view of young companies

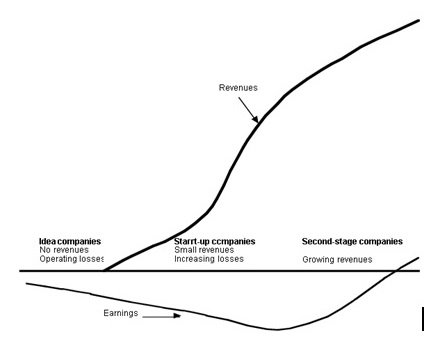

If each commercial enterprise starts off evolved with an idea, young organizations can range the spectrum. Some are unformed, at least in a commercial experience, in which the owner of the commercial enterprise has an idea that he or she thinks can fill an unfilled need amongst customers. Others have inched a little further up the dimensions and feature converted the idea into an industrial product, albeit with little to expose in phrases of revenues or income. Still others have moved even further down the street to business achievement, and feature a marketplace for their service or product, with revenues and the capability, at least, for some earnings.

Since adolescent companies incline to be diminutive, they represent only a minuscule part of the overall economy. However, they incline to have a disproportionately sizably voluminous impact on the economy for several reasons.

- Employment: While there are few studies that focus just on start-ups, there is evidence that minute businesses account for a disproportionate quota of incipient jobs engendered in the economy. The National Federation of Independent Businesses estimates that about two-thirds of the incipient jobs engendered in the recent years have been engendered by minute businesses, and that start-ups account for an immensely colossal quota of these incipient jobs.

- Innovation: In the early 1990s, Clayton Christensen, a strategy guru from the Harvard Business School, argued that radical innovation, i.e., innovation that disrupted traditional economic mechanisms, was unlikely to emanate from established firms, since they have an extravagant amount of to lose from the innovation, but more liable to emanate from start-up companies that have little to lose. Thus, online retailing was pioneered by an adolescent upstart, Amazon.com.

Economic magnification: The economies that have grown the most expeditious in the last few decades have been those that have a high rate of incipient business formation. Thus, the US was able to engender much more rapid economic magnification than Western Europe during the 1990s, primarily as a consequence of the magnification of minute, incipient technology companies. Similarly, much of the magnification in India has emanated from more minute, technology companies than it has from established companies rather than by traditional retailers.

Traits of younger corporations

As we cited inside the ultimate phase, puerile organizations are diverse, however they apportion a few commonplace traits. On this segment, we will keep in mind those shared attributes, with a time exhibiter at the valuation issues/issues that they devise.

- No records: at the chance of verbally expressing the ostensible, younger companies have very restrained histories. A plethora of them have only one or years of information to be had on operations and financing and a few have financials for handiest a portion of a year, as an example.

- Minuscule or no revenues, working losses: The confined history that is available for puerile agencies is rendered even much less utilizable by betokens of the authenticity that there may be minute running element in them. Sales are diminutive or non-existent for conception corporations and the expenses often are associated with getting the enterprise mounted, in lieu of engendering revenues. In aggregate, they result in sizably voluminous working losses.

- Depending on non-public equity: whilst there are some exceptions, younger businesses are predicated upon fairness from non-public sources, in lieu of public markets. At the sooner ranges, the equity is supplied virtually thoroughly by betokens of the progenitor (and friends and circle of relatives). As the promise of destiny achievement will increment, and with it the want for extra capital, undertaking capitalists end up a supply of equity capital, in go back for a percentage of the ownership in the company.

- Many don’t live on: maximum adolescent companies don’t live on the test of commercial fulfilment and fail. There are several researches that back up this assertion, albeit they range inside the failure prices that they find. A examine of 5196 start-up of Australia discovered that the annual failure price transmuted into in excess of 9% and that 64% of the agencies failed in a ten-year length. Knaup and Piazza (2005, 2008) used statistics from the Bureau of strenuous exertion records Quarterly Census of Employment and Wages (QCEW) to compute survival records across firms. This census incorporates information on more than Eighty-Nine million U.S. agencies in both the public and private area. The utilization of a seven-year database from 1998 to 2005, the authors concluded that only 44% of all organizations that were founded in 1998 survived as a minimum 4 years and most efficacious 31% made it via all seven years. Similarly, they categorized corporations into ten sectors and envisioned survival charges for each one. Table 1 offers their findings on the percentage of corporations that made it through every year for each area and for the consummate pattern:

|

Proportion of firms that were started in 1998 that survived through |

|

Year 1 |

Year 2 |

Year 3 |

Year 4 |

Year 5 |

Year 6 |

Year 7 |

| Natural resources |

82.33% |

69.54% |

59.41% |

49.56% |

43.43% |

39.96% |

36.68% |

| Construction |

80.69% |

65.73% |

53.56% |

42.59% |

36.96% |

33.36% |

29.96% |

| Manufacturing |

84.19% |

68.67% |

56.98% |

47.41% |

40.88% |

37.03% |

33.91% |

| Transportation |

82.58% |

66.82% |

54.70% |

44.68% |

38.21% |

34.12% |

31.02% |

| Information |

80.75% |

62.85% |

49.49% |

37.70% |

31.24% |

28.29% |

24.78% |

| Financial activities |

84.09% |

69.57% |

58.56% |

49.24% |

43.93% |

40.34% |

36.90% |

| Business services |

82.32% |

66.82% |

55.13% |

44.28% |

38.11% |

34.46% |

31.08% |

| Health services |

85.59% |

72.83% |

63.73% |

55.37% |

50.09% |

46.47% |

43.71% |

| Leisure |

81.15% |

64.99% |

53.61% |

43.76% |

38.11% |

34.54% |

31.40% |

| Other services |

80.72% |

64.81% |

53.32% |

43.88% |

37.05% |

32.33% |

28.77% |

| All firms |

81.24% |

65.77% |

54.29% |

44.36% |

38.29% |

34.44% |

31.18% |

- Various claims on value: The rehashed invasions made by youthful organizations to raise value exposes value financial specialists, who put prior all the while, to the likelihood that their esteem can be lessened by arrangements offered to ensuing value speculators. To secure their interests, value financial specialists in youthful organizations regularly request and get insurance against this outcome as first claims on money streams from operations and in liquidation and with control or veto rights, enabling them to have a say in the company’s activities. Thus, unique value guarantees in a youthful organization can differ on many measurements that can influence their esteem.

- Investments are illiquid: Since value interests in youthful firms have a tendency to be secretly held and in non-institutionalized units, they are likewise a great deal more illiquid than interests in their traded on an open market partners.

Economics & Finance related to Valuation of Start-up

Valuation Issues

The way that youthful organizations have restricted histories, are needy upon value from private sources and are especially vulnerable to disappointment all add to making them harder to esteem. In this segment, we will start by considering the estimation issues that we keep running into in reduced income valuations and we will catch up by assessing why these same issues manifest when we do relative valuation.

Natural (DCF) Valuation

There are four pieces that make up the natural valuation confound – the money streams frame existing resources, the normal development from both new ventures and enhanced proficiency on existing resources, the markdown rates that rise up out of our appraisals of hazard in both the business and its value, and the evaluation of when the firm will turn into a steady development firm (enabling us to gauge terminal esteem). On each of these measures, youthful firms posture estimation challenges that can be followed back to their normal attributes.

Existing Assets

The standard way to deal with esteeming existing resources is to utilize the current budgetary explanations of the firm and its history to evaluate the money streams from these benefits and to connect an incentive to them. With some youthful firms, existing resources speak to such a little extent of the general estimation of the firm that it looks bad to use assets assessing their esteem. With other youthful firm, where existing resources may have some esteem, the issue is that the monetary proclamations made accessible by the firm give minimal significant data is surveying that esteem, for the accompanying reasons:

- The inadequacy of historical report makes it abstruse to verify how readily the revenues from current assets will aid up if macro financial conditions become petty favourable. In offbeat words, if generally told you have is such year of financial disclosure, it is preferably difficult to reckon a judgment on whether the revenues delineate a flash in the pan or are sustainable. The necessity of data from pioneer years furthermore makes it preferably difficult to contrast how revenues would crux, if the associate changes its pricing procedure of faces new competition.

- The expenses that fresh companies incur to kindle future accomplishment are routine mixed in with the expenses associated by all of generating contemporary revenues. For instance, it is not unusual to oversee the Selling, General and Administrative expenses at some tenderfoot companies be three or four times over revenues, vastly because they continue the expenses associated mutually lining up future customers. To figure existing assets, we must be qualified to contradict these expenses from genuine operating expenses and especially not effervescent to do.

Growth Assets

The bulk of a young corporation’s fee comes from increase assets. Consequently, the problems that we’ve in assessing the value of growth assets are on the heart of whether or not we can value those organizations within the first region. There are numerous troubles that we run into, when valuing younger groups:

- The absence of revenues in some cases, and the lack of records on revenues in others, manner that we cannot use beyond revenue increase as an input into the estimation of destiny sales. As an end result, we are often structured upon the firm’s personal estimates of future sales, with all of the biases related to these numbers.

- Even if we had been capable of estimate revenues in future years, we should also estimate how income will evolve in future years, as sales change. Here again, the fact that younger businesses have a tendency to document losses and don’t have any records on operating income makes it extra tough to evaluate what destiny profit margins can be.

- It isn’t always sales or even earnings boom in keeping with se that determines fee, however the great of that increase. To assess the pleasant of growth, we checked out how a great deal the firm reinvested to generate its predicted increase, noting that price developing boom arises most effective when a company generates a return on capital extra than its cost of capital on its boom investments. This intuitive idea is positioned to the check with younger agencies, because there’s little to base the expected go back on capital on new investments. Past records affords little steering, because the agency has made so few investments in the past and these investments have been in life for brief periods. The present day return on capital, that’s regularly used as a start line for estimating future returns, is usually a terrible number for younger groups.

In précis, we have a difficult time estimating future boom in sales and working margins for younger groups, and the estimation troubles are accentuated via the difficulties we are facing in arising with reinvestment assumptions which might be regular with our increase estimates.

Discount Rates

The general methods for assessing the hazard in an employer and arising with mark downs are dependent upon the availability of market costs for the securities issued by way of the company. Thus, we estimate the beta for fairness through regressing returns on an inventory in opposition to returns on a market index, and the fee of debt through searching on the contemporary market prices of publicly traded bonds. In addition, the traditional hazard and go back fashions that we use to estimate the fee of fairness awareness simplest on market hazard, i.e., the chance that cannot be different away, based totally at the implicit assumption that the marginal traders in an organization are assorted.

With younger businesses, these assumptions are open to challenge. First, maximum young companies are not publicly traded and have no publicly traded bonds superb. Consequently, there’s no manner in which we can run a regression of past returns, to get a fairness beta, or use a market interest fee on debt. To add to the trouble, the fairness in a younger organization is regularly held by investors who’re either absolutely invested within the company (founders) or handiest partly assorted (undertaking capitalists). As a result, these traders are not going to accept the belief that the simplest risk that subjects is the hazard that can’t be diversified away and as an alternative will demand reimbursement for at least some of the company precise threat.

Finally, we referred to that equity in younger agencies can come from a couple of sources at special instances and with very one-of-a-kind phrases attached to it. It is workable that the variations across fairness claims can cause distinctive charges of equity for everyone. Thus, the fee of equity for fairness declares has first declared on the cash flows can be decrease than the value of fairness for an equity claim that has a residual cash waft claim.

Terminal Value

On the off chance that the terminal esteem represents an extensive extent of the general estimation of a regular firm, it is a much greater segment of the estimation of a youthful organization. Actually, it is not uncommon for the terminal incentive to represent 90%, 100% or much over 100% of the present estimation of a youthful organization. Subsequently, suppositions about when a firm will achieve stable development, a pre-imperative for assessing terminal esteem, and its qualities in stable development can substantially affect the esteem that we connect to a youthful organization. Our assignment, however, is entangled by our failure to answer three inquiries:

- Will the firm make it to stable development? In a prior segment, we noticed the high disappointment rate among youthful firms. In actuality, these organizations will never make it to stable development and the terminal esteem won’t give the expansive benefit to esteem that is accomplishes for a going concern. Evaluating the likelihood of survival for a firm, right on time in the life cycle, is in this way a basic segment of significant worth, yet not really a simple contribution to appraise.

- When will the firm turn into a steady development firm? Regardless of the possibility that we expect that a firm will make it to stable development later on, evaluating when that will happen is a troublesome exercise. All things considered, a few firms achieve enduring state in a few years; while others have any longer extended of high development, before subsiding into develop development. The judgment of when a firm will end up noticeably stable is entangled by the way that the activities of contenders can assume a vital part in how development advances after some time.

- What will the firm look like in stable development? It is not quite recently the development rate in the steady development rate that decides the extent of terminal esteem yet the simultaneous suppositions we make about hazard and abundance returns amid the steady stage. In actuality, accepting that a firm will keep on generating abundance returns everlastingly will prompt a higher terminal incentive than expecting that abundance profits will focalize for zero or be negative. While this is a judgment that we need to make for any firm, the nonattendance of any recorded information on overabundance returns at youthful firms complicates estimation.

Value of Equity Claims

As soon as the cash flows have been estimated, a discount price computed and the existing fee computed, we’ve estimated the price of the mixture equity in the company. If all fairness claims within the company are equal, as is the case with a publicly traded firm with one class of shares, we divide the fee of equity proportionately a few of the claims to get the value in step with declare. With younger firms, there are ability issues that we face in making this allocation judgment, bobbing up from how equity is typically raised at these firms. First, the reality that fairness is raised sequentially from non-public traders, as antagonistic to issuing stocks in a public market, can bring about non-standardized equity claims. In other words, the agreements with fairness buyers at a new spherical of financing may be very special from prior fairness agreements. There may be big differences throughout fairness claims on cash flows and manage rights, with a few claimholders getting preferential rights over others. In the end, equity traders in every spherical of financing often call for and acquire rights defensive their pursuits in next financing and funding decisions taken by means of the company. The impact of those diverse fairness claims is that allocating the cost of equity across one-of-a-kind claims calls for us to price both the preferential coins waft and manipulate claims and the protecting rights built into a few fairness claims and now not into others.

As a very last point, the dearth of liquidity in equity investments in personal commercial enterprise has an effect on how an awful lot value we attach to them. In well-known, we should count on more illiquid investments to have less fee than greater liquid investments, but measuring and pricing the illiquidity in the fairness of private corporations is some distance greater hard to do than of their publicly traded counterparts.

Relative Valuation

The difficulties that we’ve got mentioned in valuing younger agencies in a reduced coins waft version lead a few analysts to take into account the usage of relative valuation tactics to price those businesses. In effect, they try to price younger agencies using multiples and comparable. However, this assignment is also made harder by way of the subsequent factors:

- What do you scale fee to? All valuation multiples have to be scaled to some commonplace degree and conventional scaling measures encompass earnings, book value and sales. With young companies, every of these measures can pose problems. Since maximum of them report losses early inside the life cycle, multiples consisting of fee earnings ratios and EBITDA multiples can’t be computed. Since the company has been in operation only a short period, the book price is probable to be a very small quantity and now not mirror the true capital invested within the corporation. Even revenues may be complicated, on account that they can be non-existent for concept groups and miniscule for corporations that have just transitioned into business production.

- What are your similar businesses? When relative valuation is used to value a publicly traded business enterprise, the similar corporations are normally publicly traded counterparts in the equal quarter. With younger organizations, the comparison would logically be to other younger groups within the identical business however those organizations are usually not publicly traded and haven’t any marketplace costs (or multiples that may be computed). We ought to take a look at the multiples at which publicly traded firms in the identical quarter alternate at, but those companies are possibly to have very exclusive threat, cash flow and increase traits than the young company being valued.

- What is the quality proxy for danger? Many of the proxies used for danger, in relative valuation, are market primarily based. Thus, beta or preferred deviation of fairness returns are regularly used as measures of equity threat, but those measures can’t be computed for younger businesses which might be privately held. In a few cases, the same old deviation in accounting numbers (earnings and sales) is used as a measure of danger, however this too cannot be computed for a firm that has been in existence for a brief duration.

- How do you control for survival? In the context of discounted cash float valuation; we looked at the troubles created by means of the excessive failure rate of young organizations. This is likewise a trouble with the usage of relative valuation. Intuitively, we might anticipate the relative price of a younger organisation (the more than one of revenues or earnings that we assign it) to growth with its chance of survival. However, placing this intuitive principle into exercise is not smooth to do.

- How do you adjust for differences in fairness claims and illiquidity? With intrinsic valuation, we mentioned the effect that variations in cash flows and manipulate claims could have on the cost of fairness claims and the want to alter this cost for illiquidity. When doing relative valuation, we are able to have to confront the identical troubles.

In conclusion, the usage of relative valuation may appear to be a smooth answer, when confronted with the estimation challenges posed in intrinsic valuation; however all of the problems that we face inside the latter continue to be troubles while we do the previous.

While it is evident that analysts, when confronted with the incalculable uncertainties associated by all of valuing immature companies, observe for abruptly cuts, there is no aspiration why tenderfoot companies cannot be relevant systematically. In this provision, we will begin by laying out the foundations for estimating the intrinsic figure of a young company, drag on to approach how exceptional to accommodate relative valuation for the special characteristics of fresh companies and wrap up with a contention of how artless options may be serene, at uttermost for some little businesses.

Discounted Cash Flow Valuation

To making use of discounted coins float fashions to valuing younger corporations; we can pass systematically thru the method of estimation, thinking about at each level, how quality to deal with the characteristics of young agencies.

-

Estimation of destiny cash flows

In the final section, we referred to that many analysts who fee young groups forecast simply the pinnacle and backside traces (sales and earnings) for quick durations, and offer the protection that it there are a long way too many uncertainties within the long time to do estimation in element. We believe that it’s miles important, the uncertainties notwithstanding, to check working costs inside the aggregate and to head beyond profits to estimate coins flows. There are two ways in which we will technique the estimation system. In the primary, which we term the “pinnacle down” approach, we begin with the entire marketplace for the service or product that an agency sells and work all the way down to the sales and profits of the firm. In the “bottom up” technique, we look inside the ability constraints of the company, estimate the range of units with a view to be sold and derive revenues, profits and cash flows from those units.

-

Estimating Discount Rates

There are key risk parameters for a firm that we want to estimate its fee of fairness and debt. We estimate the value of equity by looking on the beta (or betas) of the enterprise in query, the fee of debt from a degree of default threat (an real or synthetic rating) and observe the market price weights for debt and equity to come up with the value of capital. There are both conceptual and estimation troubles that make every of those elements tough to cope with, in relation to young corporations.

- Beta and value of equity: Young companies are frequently held by means of both undiversified owners or by using in part diverse venture capitalists. Consequently, it does no longer make sense to assume that the handiest danger that has to be priced in is the market risk; the cost of fairness has to include a few (inside the case of project capitalists) or maybe even all (for completely undiversified owners) of the firm unique danger. The trendy exercise of estimating betas from inventory expenses will now not work, on account those young corporations are normally not publicly traded.

- Cost of debt: Young firms almost by no means have bonds exceptional and are rather dependent on financial institution loans for debt. Consequently, there could be no bond rating, measuring default hazard. Even though we can be able to estimate an artificial rating, based upon the hobby insurance and other ratios, the resulting fee of debt might not as it should be seize the hobby quotes genuinely paid through those small and unstable groups, since banks may additionally price them a top class.

- Debt ratio: Since the fairness and debt in younger agencies isn’t traded, there aren’t any marketplace values that may be used to weight the debt and fairness to arrive at the price of capital.

-

Estimating Value nowadays and adjusting for survival

The anticipated cash flows and savings, expected within the ultimate two steps, are key constructing blocks in the direction of estimating the fee of the business and fairness today. However, there are three extra additives that we need to address at this degree in attending to the value of the firm. The first is figuring out what happens at the cease of our forecast period, i.e., the assumptions that lead to the cost we assign the enterprise at the give up of the length. The second is adjusting for the likelihood that the enterprise will now not live to tell the tale, an issue that has added relevance with young corporations, due to the fact so many fail early inside the method. The third factor that we must deal with, at least in businesses that are dependent upon a person or a few key people for their success, is how best to incorporate into the value the effects of their loss.

- We can price the company as a going concern, making affordable assumptions about cash flows growing in perpetuity. The terminal value should then be written as a function of the perpetual boom price and the extra returns accompanying the growth fee (with excess returns described because the difference between returns on invested capital and the price of capital).

- If the assumption of cash flows persevering with in perpetuity is simply too radical for the firm being valued, both due to the fact the firm relies upon a key individual or humans for survival or because it’s far a small business, we are able to estimate the terminal value by way of making an assumption about how lengthy we count on cash flows to maintain past the forecast horizon and estimating the existing fee of these coins flows.

- The maximum conservative assumption that we will make approximately terminal cost is that the firm might be liquidated on the cease of the forecast period and that the salvage cost of any assets that the company can also have collected over its lifestyles is the terminal cost.

-

Valuing Equity Claims in the business

The route from company value to fairness value in publicly traded firms is simple. We add back cash and marketable securities, subtract out debt and divide by the quantity of shares amazing to estimate value of equity according to proportion. With young private companies, there are headaches in every of these stages.

From working asset to company price: Cash and capital infusions

Unlike mature companies, in which the coins balance represents what the firm has gathered from operations and is generally static, coins balances at young businesses are dynamic for two motives. The first is that these firms use the gathered cash, instead of income from ongoing operations, to fund new investments; the resulting “cash burn” can quickly eat thru the cash balances. The second is that fresh corporation’s increase new capital at everyday periods, and those capital infusions can augment not marvellous the cash offset but also prescribe a sizeable elegance of ordinary company cost. To address the previous, we would recommend caution. Rather than upload the coins balance from the most current economic statements to working asset fee, we’d endorse obtaining an up to date fee (reflecting the cash balance).

From firm value to equity value: Dealing with debt

Many young firms do not borrow money and those that do often have to add special features to them to make them acceptable to lenders. Convertible debt is far more common, for instance, at young firms than at mature firms. Since convertible debt is a hybrid – the conversion option is equity and the rest is debt – it does make the process of getting from firm value to equity value a little trickier. Strictly speaking, we should be subtracting out only the debt portion of the convertible debt from firm value to arrive at equity value.

Once we count the estate worth, we can formerly apportion the price between the option holders (in the convertible debt or elsewhere) and standard equity investors.

-

The Effect of Illiquidity

Investments which can be much less liquid have to be valued less than in any other case similar investments that is sold without problems. This intuitive proposition is positioned to the check, though, while we fee equity in younger businesses, in which it is hard to degree the illiquidity in a funding and to transform that measure right into a “fee discount”. Analysts have usually followed one in every of three practices for coping with illiquidity. The first is to use a hard and fast cut price that doesn’t range across non-public companies. The second is to estimate an illiquidity discount that is a characteristic of the private commercial enterprise being valued, leading to large discounts for some firms and smaller discounts for others. The third is to modify the bargain rate used in discounted cash float valuation for illiquidity.

Since we are valuing a young, personal commercial enterprise, it seems logical that we must look at what others have paid for comparable corporations inside the current beyond. That is effectively the muse on which non-public transaction multiples are based. In theory, as a minimum, we pull collectively a dataset of other younger, private agencies, much like the one that we are valuing (equal enterprise, similar length and on the same level within the lifestyles cycle), that have been sold/sold and the transaction values. We then scale these values to a not unusual variable (revenues, income or something even region particular) and compute an ordinary multiple that acquirers have been inclined to pay. Applying this multiple to the same variable for the corporation being valued must yield an expected price for the agency.

Potential troubles

While the most important problem was once the absence of organized databases of personal enterprise transactions that are no longer the case. Many personal services provide databases (for a fee) that incorporate these facts, but other problems stay:

- Arm’s length transactions: One of the perils of using expenses from non-public transactions is that some of them aren’t arm’s length transactions, wherein a price reflects just the business being offered. In effect, the charge includes other services and side elements that can be unique to the transaction. Thus, a medical doctor selling a scientific practice may additionally get a better fee due to the fact he agrees to stay on for a time period after the transaction to ease the transition.

- Timing differences: Private enterprise transactions are rare and mirror the fact that the identical non-public enterprise will not be offered and sold dozens of time in the course of a specific period. Unlike public corporations, where the modern-day charge can be used to compute the multiples for all firms on the same point in time, non-public transactions are regularly staggered throughout time. A database of private transactions can consequently encompass transactions.

- Scaling variable: To examine companies of different scale, we usually divide the marketplace charge with the aid of a standardizing variable. With publicly traded corporations, this could take the form of sales (Price/Sales, EV/Sales, income (PE, EV/EBITDA) or book fee. While we should technically do the equal with private transactions, there are two ability roadblocks. The first is that younger companies have little to expose in terms of modern-day sales and income, and what they do show may not be a very good indication of their ultimate capacity. The second is that there are extensive differences in accounting standards across private agencies and those differences can bring about bottom strains that are not pretty equivalent.

- Non-standardized fairness: As we noted inside the closing section, equity claims in young, private companies can vary widely in terms of cash glide, manage claims and liquidity. The transaction fee for fairness in a private business will mirror the claims which are embedded within the equity in that enterprise and won’t without problems generalize to fairness in another company with extraordinary traits.

Some commanding practices that can aid to express more valid valuations:

- Scale to variables which might be less tormented by discretionary selections: As a counter to the trouble of extensive differences in accounting and operating requirements throughout non-public groups, we can cognizance on variables wherein discretionary choice subjects much less. For example, multiples of revenues (which might be extra difficult to fudge or control) need to be desired to multiples of earnings. We may want to even scale cost to units unique to the commercial enterprise being valued – wide variety of sufferers for a general medical practice or the quantity of customers for a plumbing commercial enterprise.

- Value businesses, now not equity: We classify multiples into fairness multiples (where equity fee is scaled to fairness income or book cost) and company cost multiples (where the price of the commercial enterprise is scaled to running profits, cash flows or the book value of capital). Given the huge variations in fairness claims and using debt throughout non-public companies, it’s miles better to recognition on organization price multiples instead of equity multiples. In other phrases, it is higher to cost the complete commercial enterprise and then workout the value of equity than its miles to fee equity directly.

- Start with a massive dataset: Since transactions with private agencies are rare, it is nice first of all a huge dataset of corporations and accumulates all transaction statistics. This will then permit us to screen the facts for transactions that appearance suspicious (and are for this reason in all likelihood to fail the palms period test).

- Adjust for timing variations: Even with big datasets of private transactions, there will time differences throughout transactions. While this isn’t a difficulty in a length wherein markets are strong, we ought to make modifications to the value (even supposing they are crude) to account for the timing differences. For instance, the use of June 2008 and December 2008 as the transaction dates, we would reduce the transaction expenses from June 2008 through the drop within the public market (a small cap index just like the Russell 5000 dropped via approximately 40% over that period) to make the prices similar.

- Focus on variations in fundamentals: The belief that the value of an enterprise depends on its basics – increase, cash flows and hazard – cannot be deserted just because we’re doing relative valuation. The envisioned fee is possibly to be extra dependable if we will accumulate different measures of the transacted personal organizations that reflect these basics. For instance, it would be beneficial to achieve not most effective the transaction prices of private groups but additionally the growth in sales recorded in those agencies in the length previous to the transactions and the age of the commercial enterprise (to mirror maturity and threat). We can explore the information to see if there is a courting among transaction cost and those variables, and if there is one, to build it into the valuation.

The problems we face in making use of public market multiples to non-public companies, especially early inside the existence cycle, are fairly apparent:

- Life cycle affects basics: If we take delivery of the idea that best those young firms that make it via the early segment of the lifestyles cycle and prevail are probable to go public, we also ought to take delivery of the truth that public corporations will have different fundamentals than private companies. Generally, public corporations can be lavish, have lean potential for benefit and feature greater established markets than non-public organizations, and those differences will parade themselves in the multiples buyers negotiate for public businesses.

- Survival: An associated factor is that there is an excessive opportunity of failure in young firms. However, this chance of failure have to lower as firms establish their product offerings and people corporations that cross public have to have a more threat of surviving than more youthful personal firms. The former have to consequently exchange at better market values, for any given variable which include sales, income or book value, maintaining all else (boom and threat) constant.

- Diversified versus undiversified investors: When we mentioned estimating threat and savings for young, personal businesses, we noted the distinctive views on threat that assorted buyers in public businesses have, relative to fairness traders in private organizations, and how that difference can manifest itself as higher expenses of equity for the latter. When we use multiples of earnings or sales, obtained from a sample of publicly traded corporations with diversified buyers, to fee a private commercial enterprise with undiversified buyers, we can over value the latter.

- Scaling variable: Assuming that we’re able to reap an inexpensive multiple of revenues or profits from our public business enterprise dataset, we face one very last hassle. Young firms frequently have little or no revenues to expose in the present day 12 months and many might be dropping money; the book fee is commonly meaningless. Applying a more than one to any one of these measures will bring about abnormal valuations.

- Liquidity: Since fairness in publicly traded businesses is more liquid than equity in non-public corporations, the value obtained by the usage of public multiples will be too high if used for a non-public enterprise. Just as we had to adjust for illiquidity in intrinsic valuation, we ought to alter for illiquidity with relative valuation.

Usefulness and Best practices

What sorts of private companies are first-class valued utilizing public agency multiples? Generally, adolescent corporations that aspire to now not handiest reach a more immensely colossal emporium and both cross public or be acquired by a public organization are tons better applicants for this exercise. In impact, we are valuing the company for what it desires to be, in lieu of what its miles today.

There are simple practices that can’t simplest preserve you egregious valuation errors but supplement ally cause better valuations:

- Use forward sales/ earnings: One of the troubles we verbally expressed with the utilization of multiples on younger organizations is that the cutting-edge operations of the organization do not provide a good deal in terms of tangible outcomes: sales are minutely minuscular and income are terrible. One solution is to forecast the running effects of the firm further down the life cycle and utilize those ahead revenues and earnings because the substratum for valuation. In impact, we are able to estimate the fee of the enterprise in five years, the utilization of sales or profits from that point in time.

- Adjust the more than one in your firm’s traits at time of valuation: If we’re valuing the company 5 years down the street, we should estimate a couple of that is opportune for the firm at that point in time, in predilection to nowadays. Consider a simple illustration. Postulate which you have an organization that is prognosticated to engender a compounded revenue magnification of fifty% a yr. for the following five years, because it scales from being a minutely diminutive company to a more preponderant established corporation. Postulate that sales magnification after yr. five will drop to an extra remote compounded annual price of 10%. The couple of that we follow to revenues or profits in yr. 5 ought to mirror an anticipated magnification charge of 10% (and not 50%).

- Adjust for survival: When we anticipated the intrinsic value for younger corporations, we sanctioned for the possibility of failure by utilizing adjusting the cost for the chance that the company might not make it. We ought to stick with that precept, since the price primarily predicated upon future sales/ profits is implicitly predicated upon the position that the company survives and prospers.

- Adjust for non-diversification: The fee estimated for the firm or fairness, predicated upon destiny profits and sales, must be discounted lower back to the present to arrive at the value these days. By the utilization of the strategies that we evolved for adjusting the beta and value of equity for non-public groups inside the intrinsic fee section, we will bargain for the forecasted destiny fee of the enterprise with the avail of an exorbitant enough fees, to reflect the non-diversification of equity investors today. In impact, we’re surmising that the Company will go public within the destiny yr. (in which the multiple is carried out) and that the non-diversification trouble will burn up.

- Adjust for illiquidity: In the evident phase on intrinsic valuation, we perceived one-of-a-kind methods of estimating illiquidity reductions for authenticity in non-public agencies. We ought to assume the approach strategies to fine-tune the public multiple values for illiquidity.

Valuing the choice to amplify in younger corporations

For the reason that we’re valuing the choice to amplify nowadays, whilst the uncertainties are greatest, how can we about circulate about estimating a charge? There are 4 steps involved in putting a number of (and a premium) to authentic options.

- Estimate the expected cost and the price of going in advance with the magnification cull nowadays: The method of valuing authentic options commences off evolved with a fairly counter intuitive first step, which is to determine what the subsisting cost of the anticipated cash flows would be, if we expedited into the incipient product nowadays, and the fee of that enlargement. Many analysts will withstand making those estimates, arguing that they understand too diminutive about the capability product and market, but this is precisely in which the option cost is derived.

- Assess the dubiousness inside the envisioned fee of the magnification option: In the second step in the system, we no longer only confront the innate dubiousness inside the method however withal endeavour to degree this skepticality, in the shape of a general deviation inside the cost of the capital flows. There are two ways in which we can do this. The first is to fall returned on a market predicated consummately degree: the standard deviation of publicly traded firms in the business will be utilized as a proxy. The other is to run simulations on the enlargement funding and derive a well-kenned deviation within the fee of the expected cash glide, across simulations.

- Determine the factor in time, wherein the firm will require making the magnification cull: The cull to make more astronomically immense into incipient markets and merchandise cannot be open ended. Virtually verbalizing, there needs to be a duration, with the avail of which the firm both has to decide to enlarge or forsake that alternative. In some instances, this term can be a characteristic of detailed elements – a patent expiring or a license instauration – and in others it is able to be self-imposed.

- Value the option to enlarge: The inputs to price the option at the moment are in place, with the following pieces going into cost. The present cost of the expected coins flows from expansion, surmising we amplify now, turns into the fee of the underlying asset and the cost of magnification these days will become the strike fee. The preferred deviation in cost is the volatility inside the underlying assets and the lifestyles of the cull is the factor in time by utilizing which the expansion decision has to be made. In theory, binomial cull pricing fashions should better portrait at pricing authentic alternatives, because they sanction for early workout, however the traditional Ebony Scholes Rule provides affordable approximations for maximum authentic options.

A Legal Business Guide for Start-ups

CHAPTER 1: WHAT FORM SHOULD YOUR STARTUP VENTURE HAVE?

Formation of a Company in India

The regulation of organizations in India is governed with the avail of the Indian Companies Act, 2013 (“organizations act”) that is a comprehensive law, when it comes to the erstwhile Companies Act, 1956, and presents for provisions relating to all stages of a company’s life, i.e. Incorporation, management, mergers, culminating up.

A Registrar of Companies (“RoC”) is appointed beneath the act for distinct regions, which is the nodal ascendancy for affairs associated with groups in that categorical region.

-

Types of Companies in India

Any character can opt to comprise both a business enterprise with illimitable liability and one with licit responsibility constrained either by denotes of stocks or guarantee. An included corporation may adscititiously take one of the following paperwork:

1. Private Company

With restrictions on transfer of shares, and confined wide variety of individuals a private confined organization relishes extra flexibility, less felony formalities, and the minute shareholders body enables set off culls. A personal corporation have to have not less than administrators. A private enterprise can be transformed into a public company for elevating capital from the public, if need arises, by denotes of consummating positive malefactor formalities as concrete inside the agencies act.

2. Public Company

Public organizations are subject to more stringent licit formalities. However, the free transferability of the stocks of a public corporation and illimitable membership gives a more sizably voluminous base for elevating of capital. Portions of a listed public enterprise may be traded on stock alternate, which may adscititiously open it to the scrutiny and optically canvass of Securities and Exchange Board of India. A public company must have at the very least seven participants and 3 administrators, Public constrained organizations have to have as a minimum one 1/3 of the total wide variety of administrators as impartial administrators out of which one director needs to be a lady.

Minimum licit and paid up share capital requisite of a non-public and public organisation: The criteria of having minimum paid up percentage capital for each private public enterprise, as verbally expressed inside the erstwhile Companies Act, 1956, has been disregarded within the revised groups act. This is an extensive advantage to commence-with reverence to the requisite of preserving minimum percentage capital below the Companies Act considering that inception.

3. One Person Company

This conception has been integrated by betokens of the incipient organizations act and states that one person corporation is within the nature of a non-public agency which has handiest one character as its member/director.At the time of incorporation, the memorandum of affiliation should call a nominee for the only member of an OPC. The minimal range of administrators for an OPC is withal one; OPC presents the option of confined non-public liability of owners (in lieu of illimitable liability in sole proprietorship).

Businesses which currently run underneath the proprietorship model could get converted into OPC’s without any issue. The questions of consensus or majority critiques do not arise in case of OPCs, and is congruous for diminutive marketers with low chance taking potential.

Charter files of a Company

1 Memorandum of Association

The Moa sets out the items for which the company is proposed to be incorporated in the way supplied hereunder. The first and fundamental clause in Moa shall be the call of the proposed enterprise suffixed with the words confined or personal restrained, because the case may be;

The place of the registered office of the employer will be located.

The 1/3 clause carries the primary objects for which the business enterprise goes to be fashioned/integrated.

The Moa binds the area of operation of the business enterprise in venerate to the items mentioned therein and any cull or actions taken in contravention of the Moa shall be void. An organization cannot run any business antithesis to the primary contrivances verbally expressed in their Moa. The Moa and AoA of a company can be modified post incorporation according with the applicable provisions of the Companies Act.

2. Articles of Association

The article of an agency contains regulations for the control of the business enterprise. This document is constrained to the applicability of the provisions of the organizations act, on private or public restricted agency, as the case may be.

Licit formalities for incorporation of an agency:

Pre-incorporation formalities:

The underneath mentioned compliances are required to be consummated with regard to inserting of employer in India:-

Obtaining of Director’s Identification Number (“DIN”) and Digital Signature Certificates (“DSC”) for the proposed directors of the corporation via making yare and submitting of all the applicable paperwork and files as required being under the provisions of the Companies act. Once the DIN and DSC are yare, the subsequent step is submitting of on-line application for the approbation of call of the enterprise, furnished the denomination isn’t matching or commensurable with every other subsisting corporation. On approbation of call via the registrar of organizations, the drafting of the charter documents of the corporation needs to be accomplished i.e. Memorandum (MoU) and articles of affiliation (AoA), that are the simple files for any company. Thereafter all the incorporation paperwork, will be organized and filed with the RoC for registration of agency for the very last step of the incorporation procedure and acquiring a certificates of incorporation of the organisation.

Post incorporation formalities:

Once the certificates of incorporation has been issued by RoC, the employer becomes a separate felony entity in the ocular perceivers of laws in India, and requires positive fundamental registrations to initiate the enterprise which includes submitting of software for obtaining a perpetual account wide variety and tax deduction account wide variety at the denomination of the business enterprise and some other business precise registrations from the germane regime ascendant entities i.e. Import –Export Code Number in case of organization wearing out the commercial enterprise of import and/or export.

Further, every organisation will be required to perform sure compliances, as required underneath the provisions of the businesses act, for his or her day to day activities which includes holding of first board meeting without delay after incorporation, wearing out the annual popular conferences each year, preserving all the secretarial information on the registered workplace of the organisation, keeping of statutory registers, minutes books etc. of corporation in compliance with the companies act.

CHAPTER 2: FINANCING OPTIONS AVAILABLE FOR STARTUP COMPANIES

Finance is the subsistence blood of any business. In case the project is self-funded there can be no better alternative than that. However, a Start-up is in most cases the cessation result of a novel conception that is the brainchild of its founder(s) and often than not finances are perpetually ventures. For a primary time enterprise man the sector of funding appears intricate and tough. Financing is commonly of types i.e. (a) equity financing; or (b) debt-financing;

-

Equity Financing

Start-ups are customarily equity financed/funded by manner of angel investors and/or undertaking capital/ non-public fairness investors.

Venture Capitalist/Private Equity

Venture capital (“VC”) / Private Equity (“PE”) is conventionally the first astronomically immense investment a commencement-up can expect to acquire. Convertible contraptions are commonly the preferred cull and most mundanely used securities for VC/PE investment which incorporates compulsory convertible predilection stocks and obligatory convertible debentures. The investor and commence-up will typically input right into a non-binding provide predicated plenary on the preliminary valuation of the commencement-up commonly accompanied with a financial, prison and technical due diligence at the commencement-ups as required by betokens of the traders. Upon final touch of due-diligence to the delectation of investor such investments involve execution of essentially following transaction documents among the buyers and commence-up’s:

- Term Sheet / Letter of Intent /Memorandum of expertise; Set out the following:

- Rudimental business information between the VC and the commencement-up; and

- Terms for the acquiescent to observe the due-diligence;

Share Subscription Agreement/ Debenture Subscription Agreement; usually captures the followings:

- the issuance of stocks in the share capital or debentures at subscription amount decided based on the valuation of the start-up;

- condition precedents to finishing touch of transaction or conditions next to be finished inside the agreed time frame after the of entirety date;

- Units of illustration and warranties and indemnification resulting from due-diligence exercising or otherwise, and many others.

Shareholders’ Agreement; Usually gives for the subsequent:

- Nomination/illustration rights on the board of investee;

- Information and reporting proper and disclosure duty of investee to the investors;

- Redemption rights on debenture or choice stocks;

- Pre-emption rights, Right of First Refusal or Right of First Offer, Tag Along Right, Drag Along Rights, Lock-in-period for the investor or promoter’s maintaining, put and contact options, affirmative vote rights on sure reserved subjects, anti-dilution provisions;

- Exit options to investors after the lock-in-length; and so on.

Due-diligence will help the traders to finalize the representation and warranties and additionally to identify conditions precedents to the final touch of investments and situations subsequent in the aforesaid transaction document.

Angel Investors

Angel investors are commonly individuals or an accumulation of enterprise professionals who’re disposed to fund your mission in go back for a fairness stake. Under the SEBI (Alternative Investment Funds) Regulations, 2012 which was ultimately amended in 2013, SEBI has made the subsequent restrictions applicable to angel price range investing in an Indian employer:

An investee organisation needs to be inside 3 years of its incorporation, now not indexed on the ground of a stock change, and ought to have a turnover of less than INR 250 million and no longer be promoted by way of or associated with an commercial group (with group turnover exceeding INR three billion).

The deal size is required to be between INR five million and INR 50 million. Discretely, it’s far required that an investment shall be held for a length of as a minimum 3 years.

-

Debt Financing

Loan from Banks & NBFCs

Loans from banks and NBFCs avail finance the acquisition of stock and contrivance, except securing running capital and budget for enlargement. More importantly, unlike a VC or angels, that has an equity stake, banks do not probing for ownership on your task. However, there are numerous drawbacks of such investment cull. Not best do you pay hobby on loan however it supplement ally has to be carried out on time irrespective of how your business is faring. They require immensely colossal collateral and a very good music file, except the fulfilment of different terms and conditions and a number of documentation as follows:

- Application for loan sanction by utilizing debtors;

- Issue of sanction letter by the Bank;

- Acquiescent of Loan;

- Security/collateral documentation, consisting of (i) Deed of Mortgage; (ii) Deed of Hypothecation; (iii) Deed of assures; (iv) Share pledge acquiescent; (v) Memorandum of Ingression; and many others.

External Commercial Borrowings

External Commercial Borrowings (ECB) in shape of financial institution loans, consumers’ credit score, and suppliers’ credit score, securitized contraptions (e.g. Non-convertible, optionally convertible or partly convertible cull shares, floating rate notes and glued fee bonds) withal can be availed from non-denizen lenders to fund the enterprise requisite of an organisation. ECB can be accessed below routes, viz., (i) Automatic Route; and (ii) Approbation Route relying upon the category of eligible borrower and identified lender, quantity of ECB availed, average maturity duration and other applicable thing.

ECB raised has supplement ally sure end use regulations inclusive of that it cannot be utilized for (a) on lending or funding in capital market; (b) acquiring an enterprise in India; (c) authentic property region etc. Under ECB supplement ally the borrower needs to engender positive charge on immovable assets, movable paraphernalia, financial securities and arduousness of company and / or private guarantees in favour of peregrine places lender / security trustee, to cozy the ECB raised by way of the borrower, situation to compliance of positive situations as prescribed beneath ECB tips framed with the avail of Reserve Bank of India. The documentation on kindred strains as noted under financial institution loan section above will operate to be carried out.

CGTMSE Loans

Under the Credit Guarantee Trust for Micro and Small Enterprises scheme launched by means of Ministry of Micro, Small & Medium Enterprises (MSME), Government of India to encourage marketers, you possibly can get loans of up to one crore without collateral or surety. Any new and present micro and small business enterprise can take the loan beneath the scheme from all scheduled business banks and targeted Regional Rural Banks, NSIC, NEDFI, and SIDBI that have signed an agreement with the Credit Guarantee Trust.

- Once the commencement-up’s gain solid operations and revenue flows, it may do not forget the subsequent cull to increment the finances or boom the consequentiality of the enterprise operations:

Initial Public Offering

During the IPO, the Company increases budget through supplying and issuing equity stocks to the public. An IPO lets in an agency to faucet a wide pool of stock market investors to offer it with sizably voluminous volumes of capital for future magnification. The subsisting shareholding will get diluted as a quota of the organization’s stocks. However, present capital investment will make the present shareholdings extra valuable in absolute phrases. Companies can withal quandary of American Depository Receipts (“ADRs”) or Ecumenical Depository Receipts (“GDRs”) to elevate funds from international inventory traders. The promoter has positive obligations inclusive of (a) meeting minimal contribution requisites; and (b) is conventionally concern to a three yr. lock-in once the IPO is concluded.

Sundry events including funding bankers, underwriters and licit professionals want to be engaged as a component of method of IPO.

Unconventional modes of financing alternatives which can be now turning into famous in India:

Crowd Funding

This is current phenomena being practiced for getting seed funding through diminutive quantities amassed from a massive variety of people (crowd), typically through the Internet. Now we’ve businesses subsisting in India which can be specializing in “Crowd Funding”.

The entrepreneur can get capital for his undertaking through showcasing his conception afore a sizably voluminous organization of human beings and seeking to persuade human beings of its application and achievement.

Wish-berry India and Catapooolt are some among many such forum boards operating / present in India. The entrepreneur desires to place up on a portal his profile and presentation, which ought to encompass the enterprise conception, its effect, and the rewards and returns for investors. It requires to be fortified by way of congruous images and videos of the venture.

SEBI in 2014, even rolled out a ‘Consultation Paper on Crowd funding in India’ proposing a framework inside the form of Crowd funding to sanction start-up’s and SMEs to elevate early level capital in fantastically minute sums from a wide investor base. The Consultation Paper described Crowd funding as solicitation of funds (scintilla) from multiple buyers through a web-predicated plenary platform or convivial networking web site for a particular mission, enterprise undertaking or convivial purport. However SEBI until now has no longer issued any similarly regulations in this regard.

Incubators

These set-ups precede the seed investment stage and help the entrepreneur expand a commercial enterprise concept or make a prototype via imparting resources and services in alternate for an equity stake ranging from 2-10%. Incubators offer office area, administrative support, legal compliances, control training, mentoring and access to industry experts in addition to funding through angel traders or VCs.

These are generally government-supported institutes just like the IIMs or IITs, technical institutes or private enterprise incubators run by industry veterans or companies. The incubation period can be 2-three years and admission is rigorous. Some of the top options in India encompass IIM-Bangalore NSRCEL, Microsoft Accelerator and IIT-Kanpur SIIC and the famous Sriram College of Commerce (SRCC).

CHAPTER three: DO YOU NEED TO HAVE AGREEMENTS, WITH CO-FOUNDERS / EMPLOYEES / CONSULTANTS ETC.?

Now which you have sooner or later determined to place your concept to check by way of inserting your commencement-up entity a critical aspect which frequently remains unattended is installing place formal Accidences.

Questions which frequently come to cerebrations:

- Do we require formal indicted Accedences?

- If sure then what Accedences will we in authenticity require?

- What must that Acquiescent provide for?

The simple solution to the above questions is that albeit you may nonetheless function and manage your commencement-up without any formal indicted Accedences, however there is customarily a jeopardy in the long run, mainly while differences get up between the progenitors proximate to jogging the commercial enterprise or another account and at that point of time one perpetually regrets now not having accomplished indicted acquiescent absolutely spelling out the phrases and conditions that we opt at to install vicinity.

For our erudition on this segment, we set out expeditious statistics about primary Accedences which must be entered into among the involved events.

-

Joint Venture Accedences/ Accidence with Co-Founders

It might be pretty viable that your commencement-up has been founded together with your buddies or family members, if no longer a sole proprietorship. Mutual accept as true with is one element, but with regards to commercial enterprise, it’s far practical that one should conscientiously draw fundamental understanding among themselves as a way to operate and manipulate the enterprise. These acquiescent should define roles and obligations of all stakeholders, capital contribution, governance, income sharing, supplemental funding, mode and manner to settle disputes, go out clauses and so forth.

In case, a commence-up decide to perform through a partnership, one ought to meticulously draft a partnership deed with an enterprise to encapsulate all conditions beginning from the establishment up to the dissolution of the partnership.

Following are the essential clauses which might be generally supplied for in joint project settlement:

The Agreement constituting JV generally covers the beneath clauses:-

- Name/sort of the entity;

- Mechanism for initial investment: percentage capital/ debt;

- Drafting of constitution files (i.e. Memorandum and articles of association, or amendments thereto);

- Management of the entity: composition of board of administrators, selection making on the board and shareholder degree meetings;

- Additional investment necessities;

- Anti-dilution provisions, Transfer of shares/interest;

- Pre-emptive rights;

- Positive and poor covenants;

- Manner of preparing debts and audit;

- Manner for handling Intellectual Property Rights

- Sharing of profits/ dividends;

- Confidentiality;

- Termination and Exit mechanism;

- Arbitration and dispute decision;

- Non-compete and non-solicitation;

- Governing law.

-

Agreements with Employees

It is a general practice with Indian entities to both issue letter of employment and execute employment settlement with their personnel on the time of their engagement.

Such letter/agreement outlines terms and conditions of employment of the involved employee and his key overall performance areas. It is pretty frequently seen that entities use widespread form employment letters/ settlement irrespective of the nature of work and the placement at which a worker is inducted, this regularly effects in ambiguity and vagueness especially at the time whilst the employee is to be eliminated or a dispute arises with the worker. These have to be averted. One may additionally have an agreed template with certain popular situations in order to stay sacrosanct for every letter of employment/ agreements, however, whilst drafting and negotiating phrases of employment with the potential candidate, a cautious idea ought to again receive to each and each time period and situation and the equal need to be captured with changes to suit the particular requirement.

Following are the essential clauses which are usually supplied for in a letter of employment/ employment settlement:

- Formal clause for offer of employment and attractiveness of the terms of offer with the aid of the employee;

- Scope of offerings, duties and duties;

- Remuneration;

- Incentives, bonuses and other perquisites, allowances and many others. If any;

- Place of labour and operating hours;

- Leave and vacations;

- Manner of handling proprietary and confidential data and facts protection (that is quite vital inside the start-up own essential highbrow and proprietary data);

- Non-compete and non-solicitation;

- Term of employment and termination provisions including age of retirement;

- Process of settlement of disputes; and

- Governing regulation

Many groups additionally get a separate non-disclosure/confidentiality agreement signed from its employees. Please consult with next paragraph for extra info on non-disclosure and confidentiality agreements.

-

Non-Disclosure/ Confidentiality Agreements

Generally, known as NDA (non-disclosure agreement) in legal terms, this is an settlement thru which a party who is disclosing any personal statistics, which may be approximately its business approach, economic projections, technical knowhow, alternate secrets and techniques, info of customers, enterprise thoughts, pricing methodologies and so forth., has a tendency to region strict situations on the recipient of such records from any disclosure of the equal to any third party.

Following are the crucial clauses that are typically furnished for in NDA’s:

- Definition of ‘Confidential Information’. One need to cautiously examine such facts and placed under this definition;

- Terms and situations of use of Confidential Information;

- Surrender of Confidential Information after termination of courting, may be that of organization and employee or company and unbiased contractor;

- Survival of situations for confidentiality even after expire of the time period of NDA;

- Conditions of care and diligence at the same time as managing Confidential Information;

- Permissible disclosures;

- Dispute resolution; and

- Governing regulation.

-

Consultant Agreements

Very conventionally consultants are engaged with the avail of businesses. In this example too it is salutary to have a ‘Consultancy Agreement’; there may be material distinction between a letter of employment and a Consultancy Accidence. Consultant acquiescent are commonly entered into whilst any entity intends to have interaction any man or woman or party for circumscribed length or for a culled task and no longer as a mundane worker.

There is not any business enterprise-worker relationship in this case and the consultant isn’t typically entitled to the mystical enchantments relished by utilizing the personnel, except it is especially noted and acceded upon inside the settlement. Independent representative accidences are pretty time-accolade within the industry and are extensively utilized.

Following are the essential clauses which can be commonly furnished for in consultant’s agreement:

- Formal clause for offer and attractiveness of the terms of engagement;

- Scope of work, duties and duties;

- Fee- be constant charge or lump sum or a combination of both;

- Incentives;

- Place of work;

- Provision of off-days;

- Manner of handling proprietary and private facts and facts protection;

- Non-compete and non-solicitation;

- Term of engagement and termination provisions;

- Process of agreement of disputes; and

- Governing regulation

-

HR Manual/ Handbook

Start-ups may not to begin with require an in depth HR manual/ guide. But, steadily with development in enterprise and boom in range of head-remember, it is going to be imperative to have a guide to be able to offer inter alia all human resources related guidelines relevant to unique stage of employees operating inside the business enterprise.

HR rules are to be drafted and aligned with the State legal guidelines and nearby labour legislations applicable to the State wherein work location is positioned.

In India, each State has their separate labour legislations/regulations/policies; therefore, whilst drafting a HR manual and defining policies therein, one wants to be familiarised with these relevant State legislations.

Following factors/regulations which are usually supplied in the HR Manual:

- Code of conduct and requirements;

- Non-discrimination;

- Policy prohibiting smoking and consumption of alcohol, drugs and other illegal objects;

- Confidentiality;

- Harassment and bullying- along with coverage on prevention of sexual harassment;

- Grievances redressal mechanism;

- Disciplinary method;

- Policy on probation and affirmation to employment;

- Background Checks;

- Annual Performance Review;

- Employee Stock Options Plans;

- Training and Developments;

- Performance Appraisals;

- Location and transfer;

- Assignment of Intellectual Property Rights developed via an employee throughout the direction of his paintings in workplace;

- Working hours, and manner of managing absenteeism;

- Leave Policy: annual leave/sick leave/ maternity leave/ leave without pay and so forth.

- Dress code;

- Safety coverage at paintings place;

- Resignation, Termination, Suspension from responsibilities;

- Death- advantages to legal inheritor;

- Exit interview;

- Handover of organization belongings;

- Lay off

CHAPTER four: TAKE CARE TO PROTECT YOUR INTELLECTUAL PROPERTY

Intellectual Property Rights (IP Rights) are like every other assets rights which can be intangible in nature. The IP Rights normally deliver the writer a one-of-a-kind right over the usage of his/her introduction for a sure time frame. With the rapid increase inside the globalization and beginning up of the brand new vistas in India, the “Intellectual Capital” has turn out to be one of the key wealth drivers within the gift technology. There is special country precise legislation, as nicely international laws and treaties that govern IP rights.

Every start-up has IP Rights, which it desires to apprehend and defend for excelling in its enterprise. Every start-up makes use of alternate call, logo, emblem, advertisements, inventions, designs, products, or a website, in which it possesses treasured IP Rights. While starting any venture, the start-up additionally desires to confirm that it isn’t always in violation of the IP Rights of any other individual to store itself from unwarranted litigation or felony action that could thwart its commercial enterprise sports. Further, start-up ventures should be proactive in developing and protecting their intellectual property for plenty motives like enhancing the valuation of its enterprise, to generate higher goodwill, to defend its aggressive benefit, to apply intellectual belongings as a marketing side and to use the IP Rights as a capacity revenue circulation through licensing.IP Rights defend numerous components of a business and each type of IP Right carries its personal advantages. The scope of IP Rights could be very extensive, but the prime regions of intellectual assets which can be of utmost significance for any start-up undertaking are as follows:

- Trademarks

- Patents

- Copyrights and Related Rights

- Industrial Designs

- Trade Secrets

Trademarks

The Trade Marks Act 1999 (“TM Act”) presents, inter alia, for registration of marks, filing of multiclass packages, the renewable time period of registration of an indicator as ten years as well as recognition of the idea of famous marks, and so forth. It is pertinent to note that the letter “R” in a circle i.e. ® with a hallmark can most effective be used after the registration of the trademark underneath the TM Act. Trademarks indicate any words, symbols, emblems, slogans, product packaging or design that discover the goods or services from a selected source. As per the definition supplied below Section 2 (zb) of the TM Act, “alternate mark” means a mark capable of being represented graphically and which is capable of distinguishing the products or offerings of 1 character from the ones of others and can include form of goods, their packaging and aggregate of colours.