This article has been written by Vijay Shekhar Jha.

Introduction

Background

Recent forecasts by the International Air Transport Association (IATA) acclaimed that India is set to become the third-largest aviation market by 2025.[1] This prediction appears totally unfounded and highly implausible when one gets alive to the shocking figures revealing the harsh reality that none of our airline companies is earning the profit. According to the latest CAPA study “the Indian aviation industry is expected to lose $1.65-1.90 billion this financial year.”[2] This fact becomes more appalling when coupled with the fact that last year, even the market leader, the much-admired IndiGo, had declared a quarterly loss for the first time since going public in 2015.[3] All aviation companies when asked about the main culprit for their burgeoning losses, gave the unanimous reply that incoherent tax regime coupled with a tax hike of Aviation Turbine Fuel (ATF) is adding insult to their injury. On the top of it, what rubs salt in the wound is the government’s decision of levying 18% GST on our domestic MROs with no input tax credit (ITC) while conferring full custom exemption on the import of aircraft parts and testing equipment for maintenance, repair and overhauling of aircraft used for operating scheduled and non-scheduled passenger air transport services, scheduled air cargo services, and charter services. Thus, naturally, all our domestic aviation companies are getting their aircrafts’ MROs done in countries like Thailand or Sri Lanka where no service tax is levied on MRO. In this background, it is no wonder that in 2016, domestic airlines reportedly spent about $950 million on aircraft maintenance and servicing, but only 10% of the business came to Indian MRO companies.[4]

The relevance of the study

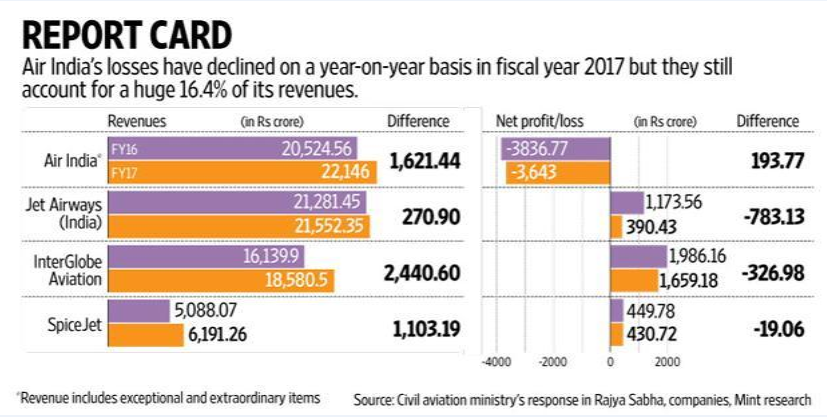

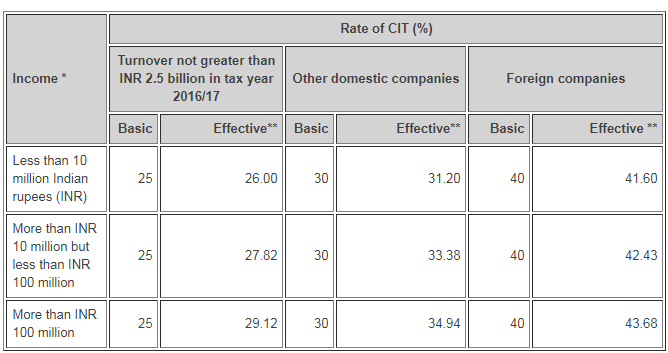

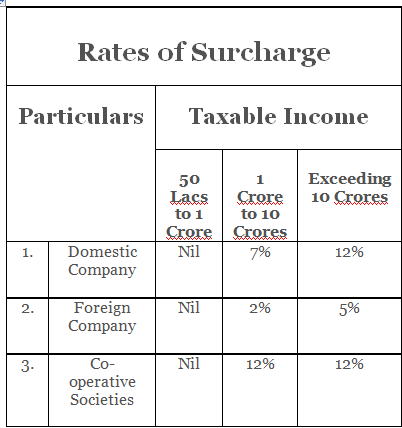

Reason for the pitching of revisiting of the provisions of Income Tax Act, 1961 from the perspective of aviation companies, can be discerned from the data undermentioned in the following tables:

Table.1 (Above shows how different airlines companies are suffering loss in.

Table 2-Tax Rates for Corporate Assessee for the A.Y. 2019-20[5]

Table 3- Rates of Surcharge for Corporate Assessee for the A.Y. 2019-20[6]

(*The health &education cess at the rate of 4% shall be computed on aggregate of Income-Tax and Surcharge.[7]

Thus, from the Table 1, 2 & 3 it becomes very clear that our tax scheme (including both direct & indirect tax) may have become very onerous (as income tax of 30%(on resident company) or 40%( foreign company)+ Surcharge + Education Cess + 40 % Indirect Tax[8] (owing to non –inclusion of ATF in the GST regime as Government has not notified levy of tax on ATF till date in accordance with Section 9(2) of CGST Act,2017 & Section 5(2) of IGST Act,2017) for our aviation sector esp. aviation companies especially in the context of their persistent heavy loss; Here, we must be mindful of the fact that had it been the case of one or two companies then the revisiting was patently not required, it is because the whole sector is languishing under the weight of loss revisiting of tax provisions has become urgent, as already mentioned, tax regime plays a paramount role in the flourishing or strangling of businesses in India and thus, if we fail to come alive to their plight in time and do not provide them with the necessary financial prop & legal relaxation (of which tax constitutes a substantial part) it would not be implausible to infer that our aviation sector might collapse and our dream of becoming world’s top aviation market will simply become a pipedream.

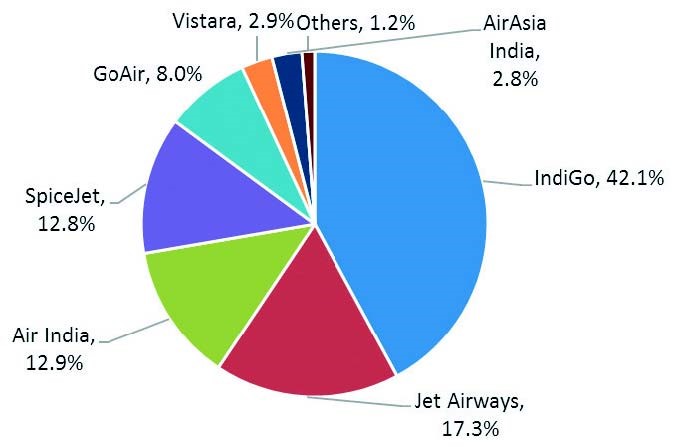

Chart A -Market Share of Scheduled Domestic Airlines March 2016[9]

Thus, this article will deal with following problems :

- What are the relevant provisions in Income Tax Act, 1961 that have a direct and intimate bearing on our aviation sector?

- Whether those provisions strike a balance between the revenue interest of Government and profit earning interest of business entities engaged in aviation sector?

- Which expired provisions of Income Tax Act 1961 should be revived so as to provide much needed fillip to our business entities engaged in aviation sector?

Understanding Provisions of Income Tax Act, 1961 having a direct bearing on Indian Civil Aviation Sector

In this chapter researcher while dealing with beneficial various under mentioned provisions of the ‘act’ has made observations highlighting as to which provisions are beneficial to aviation companies and in which provisions ambiguity persists; consequently, has made suggestions & comments to resolve those ambiguities.

Corporate Tax

As per Income-tax Act,1961 ‘income’ of the resident company as defined u/s 2(24) of the said act shall be exigible to income tax on their worldwide income as stated u/s 5(1) of the act. And, as mentioned in section 6(3) a company is said to be a resident company either if it is an Indian Company i.e. company had got incorporated in India or the place of its effective management(POEM) is in India (explanation to section 6(3) defines POEM). But, rate of tax at which the income of the resident Airlines Company is levied in India is provided in the Finance Act presented at the outset of every financial year, which For the assessment year 2019-20 is 30%; however, this tax rate of 30% drops to 25% if turnover or gross receipt of the resident company does not exceed Rs. 250 crore in the previous year 2016-17.[10]

Income under the head “Profits and Gain of Business or Profession”

Under section 28(1) of the ‘Act’ profits and gains of the business, Airlines Companies are chargeable to tax.

- Profits & Gains

As stated by Lord Halsbury in the famous case of Gresham Life Assce Soc v Styles[11] that the word ‘Profits ’is to be understood in its natural and proper sense which no commercial man would misunderstand.[12] This above principle that “Profits should be understood in the commercial sense” was followed by the Bombay High Court in the case of Aruna Mills Ltd. V CIT (1957)31ITR 153(Bom)[13] wherein the court said

“there may be an expenditure or there may be a loss which may not be an admissible loss under any specific provision of the statute and yet such an expenditure or loss would have to be allowed in order to determine what are the true profits of the business, and it is the duty of everyone who has anything to do with taxing business people to understand what are the principles of commercial expediency. Unless one understands these principles it is difficult to make a proper assessment, on a business or a businessman.”[14]

Thus, if there is a direct and proximate nexus between business operation and the loss or, it is incidental to it, then loss is deductible since without the business operation and doing all that is incidental to it, no profit can be earned.[15]

- Section 28(1)(iv) – This sub-section of sec.28 states that

“The value of any benefit or perquisite, whether convertible in money or not , arising from business or the exercise of a profession”

Q.) So, the question that crops up in the mind is, if public banks at the behest of government waive loan advanced to some of the extremely loss stricken aviation companies or if the Government pays to creditor banks on behalf of aviation companies, then, would that amount paid by Government or waiver of loan be chargeable under this sub-section?

So, from above-mentioned problem following two situations arise:

Situation No.1– Government making the payment on behalf of airline companies

This situation has been clarified by the Supreme Court in the case of Sahney Steel & Press Works Ltd. v CIT[16] wherein court held,

“where the payment is made by the Government which is in the nature of Subsidy given to the assessee for carrying of his trade or business, is a trading receipt.”

And, it is a matter of common understanding that trading receipts are exigible to tax. Thus, payment made by the government on behalf of loss ridden airline companies will fall in this sub-section.

Situation No.2- Waiver of Loan

In order to fully comprehend this situation it is indispensable to have a look at following two Supreme Court cases:

CIT v. Ramaniyam Homes (P.) Ltd.[17]– Concise facts of the case were as follows:

- The assessee was indebted to a bank. Under a one-time settlement, the bank waived a certain amount of interest and principal amount out of total dues.

- Assessing Officer held that amount of waiver of the principal amount of loan was to be treated as income under section 28(iv).

On the above factual Madras High Court held that

“it is not the actual receipt of money, but the receipt of a benefit or perquisite, which has a monetary value, whether such benefit or perquisite is convertible into money or not, which is what is covered by section 28(iv).

The waiver of a portion of the loan would certainly tantamount to the value of a benefit. This benefit may not arise from ‘the business’ of the assessee. But, it certainly arises from ‘business’. The absence of the prefix ‘the’ to the word ‘business’ makes a world of difference.”

But, the above opinion of the Madras High Court was negated by Supreme Court in the case CIT v. Mahindra And Mahindra Ltd.[18], wherein court held that “ benefit which is received has to be in some other form rather than in the shape of money” and since by dint of waiver of loan the assessee became in possession of extra cash free from any encumbrance at his disposal thus, the court held that very condition that the benefit as stated u/s 28(1)(iv) must not be in cash form was not fulfilled. It is in this light court denied the applicability of this subsection.

Here, it is to be noted that, since in this case the assessee did not claim deduction u/s 36(1)(iii) of the act, therefore, Supreme Court did not accept the department’s argument that waiver of loan tantamount to “cessation of trading liability ” as mentioned in section 41(1). Had the assessee claimed deduction u/s 36(1)(iii) then, it would be very difficult to see what would have been the final outcome of the case?

Comment- Here, it is very pertinent to note that section 56 (1)(vi) ‘Income from Other Sources’ will not apply to present cases of waiver of loan or granting of subsidy by the Government in that cl.(vi) explicitly states that this clause will levy tax to only those gifts received without consideration by individuals or a HUF. Thus, airline companies cannot be charged under this provision.

Section 28 (via) read with section 145A -dealing with conversion or treatment of inventory into a capital asset has come under the tax net.

“FMV of inventory[19] as on date on which it is converted into, or treated as, a capital asset determined in the prescribed manner[20].”

Suggestion

Though, FMV(defined u/s 2(22B)) of inventory, when converted into capital asset, has been brought under the tax net by finance act 2018 but, the deduction as to the cost of inventory has nowhere been provided between section 30 to 43D; it can be argued that this cost of inventory can be deducted u/s 37 as expenses incurred wholly and exclusively for business, still the proponents of this argument would agree if this deduction is mentioned explicitly it will certainly clear the cloud of uncertainty and accordingly will lessen the possibility of future litigation.

- Current Repairs- Section 31

This provision grants deduction in respect of current repairs and insurance of machinery, plant used for purpose of the business. The current repair should be such so as to restore the plant or machinery into the original form. However, such improvement which does not substantially change the identity of the plant or machinery should be allowed as a deduction under this section.[21]

Suggestion:

Section 43(3) gives out the inclusive definition of the term ‘plant’ but unlike ‘ship’ it does not explicitly include ‘aircraft’ within its fold. It may be argued that since the definition is inclusive the term ‘aircraft’ is already covered in the definition of ‘Plant’ as ‘Plant’ in ordinary sense, includes whatever apparatus which is used by a businessman for carrying on his business for want which carrying out of business is not possible[22], but for the sake of certainty, the term ‘aircraft’ just like ‘ship’ must also be included in the sub-section.

- Depreciation- Sec.32

The concept of depreciation is that any asset, on account of normal wear and tear, is required to be replaced at a point of time in future. Therefore, to enable a business to meet the cost of such replacement, the wear and tear is permitted to be calculated at a notional percentage of the cost/ WDV (as defined u/s 43(6)) of the assets.[23]

Section 32 (1) provides depreciation of both tangible (buildings, machinery, plant or furniture) & intangible asset, which is owned both wholly or partly and used in the previous year for the purpose of business. In case of any block of an asset, the depreciation is computed on the WDV at a prescribed rate of the block as on the last day of the previous year as mentioned in section 43(6) of the act.

Here, it would be pertinent to note that “Block of Assets” defined u/s 2(11) means a group of assets falling within a class of assets comprising both tangible and intangible assets as stated in section 2(11). Rates of depreciation for Aeroplanes & Aero engines for AY 2019-2020 are 40 %.[24]

Under section 32(2), subject to section 72(2) and 73(3) aviation companies can carry forward and set off unabsorbed depreciation.

Suggestion1:- Section 32(1)(iia) gives additional deduction of 20% of actual cost on new machinery or plant (acquired and installed after 31s March 2005) purchased by the assessee engaged in the manufacture of any article or thing but this beneficial provision has not been extended to purchase of new aircrafts. Owing to India ambition of increasing its extant aviation market it is necessary to extend the benefits of this provision to Airline companies as well.

Suggestion 2: (Revival of Investment Allowance u/s 32A)

As predicted by IATA, India is set to become third largest aviation market of the world; to make this come true Government is pitching for creation of new airports and thus, in this backdrop, needless to say, airline companies will be purchasing more aeroplanes in pursuance of this policy of expansion. It is in this background, there is an urgent need for the revival of Section 32A which deals with Investment Allowance to be given to Airline Companies on a new purchase of Aircraft. An argument in favour of resuscitation of this provision gets more support as its sub-section (4) which enjoins the benefit receiving company to reap 75% of the benefit allowed back into the system by purchasing more new aircraft.

Suggestion 3- In the background as mentioned above , it is also very important to revive section 32AB which deals with ‘Investment Deposit Account’ (expired in the year 1990) as it helps the Airline companies to claim deduction under sub-section (1) of this section on utilisation of money for the purchase of new aircrafts as credited in the said account. Here, it is worthwhile to note that an aviation company cannot avail the benefits of both provision viz. sec 32A and Sec 32AB as mentioned in section 32AB(10).

Deduction u/s 35AD

This section grants investment-linked incentive by allowing 100% deduction i.r.o capital expenditure expended wholly and exclusively for the purpose of specified business. Clause (c) to Sub-section (8) of this section defines ‘specified business’ which includes developing or operating & maintaining or developing, operating and maintaining any infrastructure facility.

Furthermore, ‘infrastructure facility’ as defined in explanation to Section 35AD- (8)-(ba) also entails ‘airport’ within its fold. Thus, this section is of great significance for those companies engaged or to be engaged in the development of infrastructure of airports on PPP model including up-gradation of facilities inter alia the development of Communication, Navigation and Surveillance (CNS) facility, Air Traffic Management (ATM) systems. Here, it is worth mentioning similar provision can also be seen in Section 80IA but as per sub-section (3) of this section, assessee cannot avail benefits of both these two provisions.

Loan advanced by Parent Company to Subsidiary Company

Deduction u/s 36(1)(iii) – This clause makes an allowance in respect of interest paid on capital borrowed for the purpose of the business, profession or vocation.

Deduction u/s 37 –This clause makes an allowance (not covered under section 30 to 36) i.r.o expenditure incurred wholly and exclusively for the purpose of business.

Disallowance u/s 40A(2)– This clause disallows expenses or expenditure where such payments are made to relatives or close associates of the assessee, and Assessing Officer is of the opinion that such expenditure is excessive or unreasonable having regard to legitimate business needs of the assessee’s business.

Q.) Here, the problem that is contemplated to be dealt is ‘If a parent aviation company takes a loan from a bank at some interest and later advances interest-free loan to sister subsidiary aviation company, can it claim a deduction for the loan advanced to its subsidiary aviation company?’

The answer lies in the two decisions of the Supreme Court, which has been collated as under:

(i) S.A. Builders Ltd.v. Commissioner of Income-tax (Appeals), Chandigarh[25], wherein assessee had advanced huge amounts as interest-free loans out of its cash credit account in which there was a huge debit balance to its sister concern and claimed a deduction of interest paid to the bank u/s 36(1)(iii). Supreme Court allowed deduction claimed by the assessee stating that where the scheme of advancing interest-free loan to sister concern is not a device to avoid tax and if passes muster of commercial expediency test the loan advanced must be allowed.

In so far as section 37 is concerned Court made following important observation:

“22. In our opinion, the decisions relating to section 37 of the Act will also be applicable to section 36(1)(iii) because in section 37 also the expression used is “for the purpose of business”. It has been consistently held in decisions relating to section 37 that the expression “for the purpose of business” includes expenditure voluntarily incurred for commercial expediency, and it is immaterial if a third party also benefits thereby.”

(ii) Hero Cycles (P.) Ltd. v. Commissioner of Income-tax (Central), Ludhiana[26], wherein court resorting to ‘commercial expediency test’ allowed deduction under this clause to the assessee who had granted loan out of assessee’s own surplus funds to its sister concern and held that

“Once it is established that there is nexus between expenditure and purpose of business revenue cannot justifiably claim to put itself in arm-chair of businessman or in the position of Board of Directors and assume the role to decide how much is reasonable expenditure having regard to circumstances of the case.

It was noted that advance to the subsidiary company became imperative as business expediency in view of undertaking given to financial institutions by the assessee to effect that it would provide additional margin to the subsidiary company to meet working capital for meeting any cash losses.”

Comment– Here, it is to be noted that though in this case loan was advanced to director of the sister concern yet when the court found the transaction passed muster on the touchstone of “Commercial Expediency Test”, it did not disallow the assessee’s claim. But, it is submitted this conundrum has not been fully resolved as uncertainty still hovers as to what may and what may not amount to ‘commercially expedient’ and such uncertainty in the miserable condition in which our aviation companies cannot be allowed to continue. Thus, it is suggested Parliament must explicitly exempt these inter-corporate loans in respect of aviation companies.

Section 44BBA

This is a special provision regarding the computation of profits and gains of non-residents engaged in the business of operation of aircraft and the amounts mentioned under sub-section (2) shall be exigible to tax at the rate of 5% under the head PGBP.

This is a welcome provision as it resolves the problem of operation of aircraft by non-resident aviation companies for want of which they would have otherwise undergone the traumatic & confounding application of Section 9 of the act (as to ‘business connection’), DTAA (as to permanent establishment ‘PE’) & section 195 of the Act read with section 201 (as to ‘TDS’ in case payment made to non-resident)

Comment- Such special provision for the resident company is not possible in the present scheme of tax, as u/s 5 of the act worldwide income of resident is charged to tax.

- Income Under the Head “Capital Gains”

- Basis of Charge(Section 45(1)

Following are the essential conditions for taxing capital gains:

- There must be a capital asset (as defined u/s 2(14)) which is held by the assessee ;

(short term capital asset is defined u/s 2(42A) and Long term capital asset is defined u/s 2(29A))

- The capital asset must have been transferred by the assessee during the previous year ;

- There must be profits or gains as a result of such transfer, which will be known as capital gains;

- Such capital gains should not be exempt under section 54,54B,54D,54EC,54F,54G,54GA or 54GB

- Capital Asset, when converted into stock in trade, is exigible to capital gains tax u/s 45(2)-

Where the owner of a capital asset converts it into or treats it as, stock in trade of his business, there is no transfer and no gain under the general law, for a man cannot transfer his property to himself or make gain out of himself. However, sec 2(47)(iv) deems such conversion as ‘transfer’ and section 45(2) brings this transfer to tax.[27]

- Transfer of beneficial interest in securities held in dematerialised form is exigible to tax u/s 45(2A): This sub-section provides that the profits and gains arising from the transfer of beneficial interest in a security, of which a depository is registered owner, shall be charged in the hands of the beneficial owner and not the registered owner.[28]

- Capital Gains v Business Income Whether a particular asset is a stock in trade or capital asset does not depend upon the nature of the article, but the manner in which it is held. The same item may be stock in trade in the hands of the assessee who deals in that item.[29]

- Section 47(xvi)

This clause exempts transfer arising in a transaction of a reverse mortgage under the scheme as notified may be notified.

Suggestion– As per the extant Reverse Mortgage Scheme, 2008 notified in 2008[30] the benefits can only be availed by senior citizens. Therefore, in context of the precarious situation in which our airline companies are mired if this scheme is extended to airlines companies with necessary changes it will help them to access liquid money from the bank (which is exempted from tax u/s 10(43) of the act) without losing ownership from the property .

- Section 50– Capital Gain on transfer of depreciable assets forming part of a block of assets

This section brings to tax net the profits received from the transfer of those plants and machinery on which airline companies claimed depreciation u/s 32 in the past.

- Section 50B– This provision levies capital gains tax on the profits generated by the transfer of the undertaking.

- Aviation company & reduction its share capital–

Under section 2(47)(ii) of the act the term ‘transfer’ in relation to capital asset entails ‘extinguishment of any rights therein’; thus, the reduction of share capital amounts to extinguishment of rights as it causes extinguishment of right of shareholder to the dividend and right to share in the distribution of the nett assets upon liquidation.[31]

Thus, if an aviation company which is saddled with the loss, buybacks its share, the shareholders of the company receiving money therein would be exigible to capital gains tax u/s 46A of the Act. Here, it must be noted that reduction of share capital is one of the most effective ways for a company to maintain its financial health but, if the threat of tax is hovering then, the promoters or the holding company may hesitate to undergo this process esp. when undergoing is urgently needed.

Suggestion –

(i)In the background of the above it is suggested that applicability of Chapter XII-DA (S. 115QA to S.115 QC) of the act which has been inserted in the act in the year 2013 which simply put states that the consideration paid by the company for the purchase of its own unlisted shares which is in excess of the sum received by the company at the time of issue of such shares will be charged be to tax and the company will be liable to pay an additional income tax at the rate of 20% of the distributed income paid to shareholder[32] .This provision, with the aim to encourage our loss laden companies to restructure its share capital to minimise their loss, this chapter as far as applicability on Aviation Companies is concerned should be put on hold for six or seven years or till the time our drowning airline companies start showing relatively better financial health.

(ii)As far as section 46A is concerned with the intention to help airline companies revive from losses Government should introduce section 10(34B) which would be on the lines of section 10(34A) which would exempt the income received by the shareholders of airline companies on account of buy-back of shares by the airlines companies(section 10(34A) exempts the income received by the shareholders on account of buy back of companies mentioned in section 115QA).

- Taxation of long term capital gains on transfer of listed securities-(Sec 112A)

Erstwhile, any long term capital gains arising by the transfer of equity securities was exempt from tax by dint of section 10(38) of the act but now if owing to transfer of long term capital asset any capital gain arise of the amount exceeding Rs.1 Lakh then total income as mentioned u/s112A(1) which will be exigible tax u/s 112A(2) of act. Here, it is worthwhile to note that when total income as determined by sub-section (1) when reduced by capital gains is allowed to take benefits of deduction as mentioned under chapter VI-A of the act.

- Exemptions u/s 10(6BB)

With the Government pitching for the expansion of aviation industry by creating 100 or more new airports so as to make airline services accessible to every common person, it is expected that airlines companies will have to purchase around 1000 new fleets.[33] In this backdrop it has become paramount to unravel section 10(6BB) provided as under:

Section 10(6BB)- This provision grants exemption of that income which is derived by a non-resident from an Indian Company engaged in the business of operation of aircraft on account of consideration paid by such Indian company to acquire new aircraft or new aircraft engine on lease in pursuance of agreement entered into after 31st March 2007 and as approved by Central Government (Consequently, exemption provided u/s 10(15A) was withdrawn).

Q.) Generally leasing of aircrafts have been categorised in two types (i) Dry Lease –in which the non-resident lease out only aircraft with no complimentary service facilities (ii) Wet Lease –in which non-resident leases out its aircraft along with service facilities like insurance, crew, maintenance etc. It is in this background question has been raised that section 10(6BB) only exempts dry lease and wet lease on the basis of ‘Service PE test’ as applied by Delhi High Court in the case of Centrica India Offshore Pvt.Ltd v CIT[34] is exigible to tax.[35] This view further gets reinforced by Note 25 discussed under ‘Paragraph 4 to Article 5’of ‘Model Tax Convention on Income and on Capital: Condensed Version 2014’[36] which is states :

“A permanent establishment could also be constituted if an enterprise maintains a fixed place of business for the delivery of spare parts to customers for machinery supplied to those customers where, in addition, it maintains or repairs such machinery, as this goes beyond the pure delivery mentioned in subparagraph a) of paragraph 4. Since these after-sale organisations perform an essential and significant part of the services of an enterprise vis-à-vis its customers, their activities are not merely auxiliary ones.”[37]

What becomes more concerning is the point that if the above question is found valid then these non-resident companies giving wet lease will have to pay corporate tax of 40% and will not be allowed to avail section 44BBA as they do not operate in the operation of aircraft.

Suggestion- Therefore, it is suggested that CBDT in the exercise of section 119 of the ‘Act ’ should issue circular clarifying this ambiguity. As resident companies are required to cut TDS u/s 195 of the Act before making payment to non resident failing which they would be penalised u/s 201 of the act.

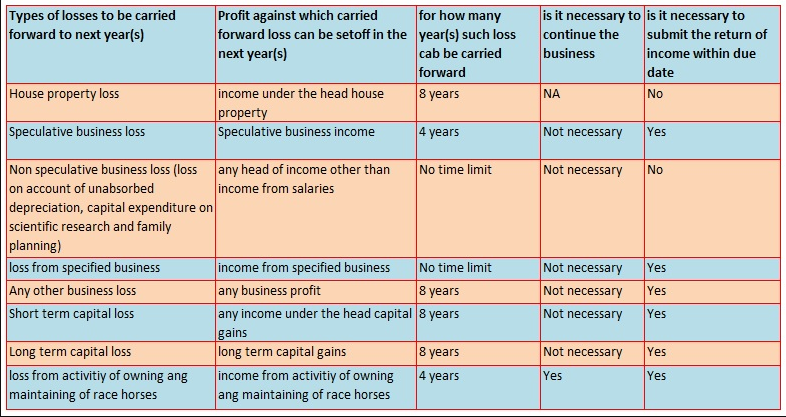

Set-off or carry forward and set off of the loss

Provision related to set off or carries forward and set off of loss as provided under section 70 to 74, has been summarised in the table below.

Table 4– Summary of set off and carry forward of losses.

- Minimum Alternate Tax (chapter –XII-B of the Act)

Section 115JB(1)-In case of company income tax payable shall be higher of the following two amounts:

(i) Tax on total income computed as per the normal provision of the act by charging applicable normal rates and special rates if any income included in the total income of the company is taxable at special rates.

(ii) 18.5% of book profit (book profit is to computed as per explanation 1 to S. 115JB(1) & (2))[38]

Section 115JAA- MAT credit – This provision allows tax credit in respect of tax paid on deemed income under MAT provisions against tax liability in subsequent years. Here, it must be noted that MAT credit will be allowed only in that previous year in which tax payable on the total income as per normal provisions of the Act is more than tax payable u/s 115JB.[39]

Section 115JB(3)

Once provisions of MAT are applicable, it does not allow unabsorbed depreciation or loss to be deducted from the book profit, but allows carrying forward of such unabsorbed depreciation or loss to subsequent years for claiming set off as per provisions of the Act.

Suggestion-

This section penalises the so called ‘zero tax’ companies unfairly ignoring the total fiscal burden discharged by the company and adverting only to income tax. Thus, despite being aware to the state of affairs in which our aviation sector is mired in, it would be highly unfair & immoral on the part of government to further saddled them with ponderous tax schemes like MAT; therefore, it is suggested that all airline companies should be spared from MAT till all their unabsorbed losses (including unabsorbed depreciation) are set off against future book profits.

Deduction

(i) Section 80-IA

This section provides deduction of an amount equal to 100 % of the profits and gains for ten consecutive AY from the business carried out by any enterprise or undertaking i.r.o developing or operating & maintaining or developing , operating and maintaining any infrastructure facility.

Here, it is worth noting that infrastructure facility as defined in explanation to Section 80 –IA (4)- (i) also entails ‘airport’ within its fold. Thus, this section is of great significance for those companies engaged or to be engaged in the development of infrastructure of airports on PPP model including inter alia the development of Communication, Navigation and Surveillance (CNS) facility, Air Traffic Management (ATM) systems.

(ii)Suggestion –Regarding updating of Section 80IB of the Act:

Though section 10(6BB) incentivises non-resident in case they sell their aircrafts to resident companies on lease by exempting their income earned from these lease transactions, but it fails to provide any bounty to resident company. This lacunae can be plugged with the introduction of a new sub-section like ‘(6A)’ to section 80IB which would be on the lines of sub-section 6 to Sec. 80IB, which gives deduction of 30% of profits and gains to resident companies being the owner of a ship engaged in the business of shipping whose Gross Total Income includes any profits and gains derived from the business of such ship.

(iii) Suggestion– Regarding the updation of Sec 80JJAA in favour of Airline Companies:

Presently, under section 80JJAA, an amount of 30 percent of additional wages paid to new workmen is to be allowed as a deduction for a period of three years beginning with year in which workman is employed. Thus, in the context of expansion of aviation market it is suggested that in the sub-section (1) to Section 80JJAA “profit and gains derived from business of the operation of aircraft ” should be added as soon as possible.

Payment made by airline companies to AAI

Q.) Whether payment to Airport Authority for availing services like aircraft parking, aircraft landing will fall in rent or royalty or contractual payment simpliciter?

- If such payment is categorised as “Rent” then Companies has to make TDS of 10% u/s 194I of the act + 2% additional TDS if they have used any ‘plant’ or ‘machinery’ owned by AAI

- If such payment is Royalty then companies are required to cut TDS of 10% on the payment u/s 194J.

Failing which they will be penalised u/s 201 of the act.

On this Issue Courts’ stance has been that :

(i) If predominant objective is providing facilities and services then it is not ‘Rent’ (rather Royalty).[40]

(ii) If predominant objective is providing land or building for use then it amounts to rent.[41]

Suggestion-In this background, it will be very heartening if CBDT in exercise of the power u/s 119 clarifies this issue by issuing relevant circular.

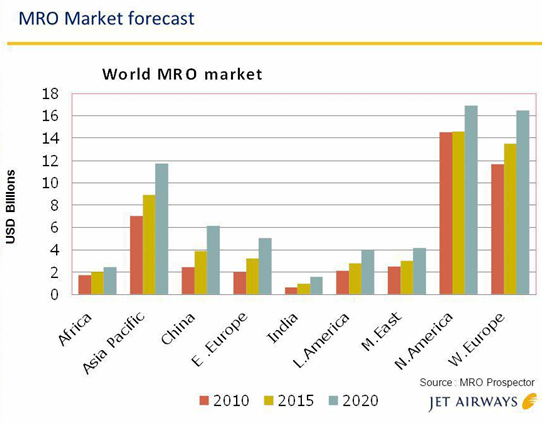

Provisions having a bearing on MROs

With the expansion of aviation market in India it has become imperative to increase both the number of airports and number of carriers in India. As already mentioned that airline companies in a bid to match up the rising expectation have proposed to purchase around 1000 carriers in India . With this, it becomes indispensable that we must revive our dwindling MRO industry for want of which we will lose immensely as if properly developed the MRO industry can be a game changer in the revival of aviation industry.

Table 5 – MRO Market forecast[42]

With the aim to function in a hassle free manner MRO service rendering companies want to open up their business in SEZ, therefore, it has become matter of high priority that we must pay a revisit to SEZ Act 2005 and Rules with the objective to develop these areas in a more business friendly manner.

Presently, in order to develop sector specific SEZ it is necessary to have fulfilled the area requirement of 100 hectares.[43]Moreover, from MRO perspective it will also be very critical to have land which abuts airports so that aircrafts can easily be sent for MRO purposes. In this aspect, every state has to help MRO companies in bespoke land acquisition.

Apart from the above discussed provisions some provisions under mentioned would have a direct bearing on the operation of MRO service providers in India:

a.Tax Provisions related to SEZ which MRO service providing companies may resort to:

(i) Section 10AA- Under this section all units established within a SEZ are eligible for a deduction of 100% of profits and gains derived from the export of goods, articles or from services for first five years and 50 % of profits and gains of the business for the next five years subject to creation of a SPECIAL Economic Zone reinvestment reserve Account to which this 50% of the Profits is to be debited.

(ii) Section 54GA- This provision provides for exemption of capital gains on transfer of assets in case of shifting of industrial undertaking from urban area to any SEZ.

(iii) Section 80-IAB – This section is applicable to any person being ‘developer’ of SEZ and it provides for 100% deduction of profits and gains derived by an undertaking or an enterprise which is engaged in the development of SEZs for 10 consecutive AY.

- Suggestion regarding Section 80IA & 35AD:

With the aim to bolster up the industry of MRO in India, it is suggested that definition of ‘infrastructure facility’ must include “repair to aircrafts” within its fold in the lines of ‘business of repairs to ocean going vessels’ as mentioned u/s 80-I(1) of the Act.

- Payment made for MRO –whether FTS or not

In the case Ishikawajma Harima Heavy Industries Ltd. V Dir of Income Tax[44],apex court had held that there must be sufficient territorial nexus between Income of non-resident and territory of India. Court had also emphasised that not only service utilised in a business must be in India but also have to be rendered in India.[45]

The explanation 2 to sub-section (2) of section 9 of the act (added in the year 2010), has done away with the requirement of business connection or rendering of services in India with regard to inclusion of FTS or Interest or Royalty in the total income of Non-Resident; what remains a moot matter is whether payment made for MRO by resident companies to Non-Resident Companies fall within the purview of FTS or not. As if found FTS, then the Airline Companies will have to cut TDS u/s 195 before making payment to non-resident MRO provider; not doing will cause them penalty/s 201 of the Act.

Reliance on this issue can be placed on Supreme Court’s decision in CIT v. Kotak Securities Ltd[46] in which court held that if the services is bespoke and has been provided taking special requirements of the customer with the effect that customer on the basis of such service has the option to avail enduring benefit in his business then, the service provided by non -resident can be said to be “Fees for Technical Services”. Therefore, going by the observation made by the Apex Court, it can be safely inferred that MRO provided by a foreign company will fall in the purview of FTS.

Conclusion

From the above discussion, it can be safely stated all the changes as have been suggested is indispensable for the successful revival of our aviation companies for want of which we will never be able to successfully free our aviation companies from the shackles of loss. Here, it is important to submit that researcher is not advocating that tax reforms/ updation is the panacea of this gargantuan conundrum, but at the same time, it would be preposterous to dream & conclude that our aviation market will be among the world’s top flourishing market if we let this grim situation to continue. In this context, it is paramount that we must come to our senses and discern the point that this expansion of our aviation market will be nothing but a hollow ostentation until we actually reorient ourselves and work so as to make the bedrock of the aviation industry viz. airline companies & MRO service providing companies robust again. Thus, in this background, there is an urgent need of tax overhaul in favour of aviation companies in keeping with various suggestions proposed in this paper.

At the beginning of this research the researcher has proposed the following hypothesis:

- Most of the provisions of Income Tax Act,1961 regarding aviation sector have become redundant and there is an urgent need to update tax provisions in favour of aviation companies.

Throughout the research this hypothesis has been put through extensive examination in the background of available data and literature and wherever necessary researcher has given suggestion to improve extant provisions. At the conclusion of the research, the researcher finds the above hypothesis to hold true.

Endnotes

[1] Rhik Kundu “Aviation will grow in double digits in India for many years to come” ,www.livemint.com (March 25, 2019,11:00 AM)

[2]V. Kumara Swamy “Why the Indian aviation industry is nosediving” , www.telegraphindia.com (March 25, 2019,11:00 AM)

[3] Mihir Sharma, Bloomberg “ Opinion | Why Indian airlines keep struggling to take off ”, www.livemint.com,(March 25, 2019,11:00 AM)

[4] Mihir Misra, “Aviation MRO companies want 18% GST scrapped ”, https://economictimes.indiatimes.com, (March 25, 2019,11:00 AM)

[5] “Budget 2018-19: Tax Rates for AY 2019-20” , www.taxmann.com , (March 25, 2019,11:00 AM)

[6] [6] “Budget 2018-19: Tax Rates for AY 2019-20” , www.taxmann.com , (March 25, 2019,11:00 AM)

[7] Ibid

[8] Soumeet Sarkar ,“Jet Fuel Under GST Will Help Airlines Only If…”, www.bloombergquint.com, (March 25, 2019,11:00 AM)

[9] “India’s airlines report combined profit of USD 122 million: CAPA India Aviation Outlook 2017/18”, http://www.travelbizmonitor.com, (March 25, 2019,11:00 AM)

[10] “Income Tax Rates for AY 2019-20 / FY 2018-19” https://taxguru.in ,(March 25, 2019,11:00 AM)

[11] 3 TC 185 (HL)

[12] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.676

[13] (1957)31ITR 153(Bom)

[14] Dr. Girish Ahuja, Professional Approach to Direct Taxes Law & Practice, 34th Edition, Bharat Law House 2016, p.210

[15] Commonwealth Trust(India)Ltd. v CIT 242 ITR 593 (Ker)

Dr. Girish Ahuja, Professional Approach to Direct Taxes Law & Practice, 34th Edition, Bharat Law House 2016, p. 218.

[16] (1997) 228 ITR 253(SC)

[17] [2016] 384 ITR 530 (Mad)

[18] 284 ITR 669(SC

[19] “Inventory and Related Terms” , https://cleartax.in (March 29, 2019,11:00 AM)

Shishir Sinha ,“Rules notified to determine ‘Fair Market Value’ for conversion of inventory into capital assets”, www.thehindubusinessline.com (March 29, 2019,11:00 AM)

[20] Rule 11UAB of the Income Tax Rules,1961 provides the manner of determination of fair market value of the inventory which has been converted into the capital assets or treatment as a capital asset.

[21] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.715

[22] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.731

[23] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.729

[24] “Depreciation Rates for Financial Year 2019-20 & Assessment Year 2020-21” , https://www.bankbazaar.com (March 25, 2019,11:00 AM)

[25] 288 ITR 1 (SC)

[26] 2007 (288) ITR 1 (SC)

[27] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.1125

[28] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.1125

[29] Dr. Girish Ahuja, Professional Approach to Direct Taxes Law & Practice, 34th Edition, Bharat Law House 2016, p.442

[30] Notification No. 93/2008

[31] Kartikeya V. Sarabhai v. CIT, 228 ITR163 (SC)

[32] Arvind P Datar, Kanga & Palkivala-The Law & Practice of Income Tax, Tenth edition ,Lexis Nexis 2014, p.1890

[33] “India’s aircraft orders to exceed 1,000 with Jet Airways’ imminent order; infrastructure a problem” , https://centreforaviation.com (April 1, 2019,11:00 AM)

[34] (2014)44 taxxmann.com 300(Delhi HC)

[35] Ashish Karundia, Law & Practice relating to Permanent Establishment,2015 Edition, Taxxman Publication, p. 235

[36] OECD (2014), Model Tax Convention on Income and on Capital: Condensed Version 2014,

OECD Publishing.

http://dx.doi.org/10.1787/mtc_cond-2014-en

[37] OECD (2014), Model Tax Convention on Income and on Capital: Condensed Version 2014,

OECD Publishing.

[38] Dr. Girish Ahuja, Professional Approach to Direct Taxes Law & Practice, 34th Edition, Bharat Law House 2016, p.925

[39] Dr. Girish Ahuja, Professional Approach to Direct Taxes Law & Practice, 34th Edition, Bharat Law House 2016, p.927 para 2

[40] Asstt. CIT (TDS) v. Pushpak Logistics (P.) Ltd [2016] 66 taxmann.com 266/157 ITD 471 (Rajkot – Trib.)

[41] Japan Airlines Co. Ltd. v. CIT (2015) 10 SCC 591.

[42] “MRO Strategy for the Airline In-House”, https://slideplayer.com (April 1, 2019,11:00 AM)

[43] “How to Start an SEZ?”, https://www.indiafilings.com (April 1, 2019,11:00 AM).

[44] (2007) 288ITR 408(SC)

[45] Dr. Girish Ahuja, Professional Approach to Direct Taxes Law & Practice, 34th Edition, Bharat Law House 2016, p. 65

[46] (2016) 11 SCC 424.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications