This article is written by Dilpreet Kaur Kharbanda. It is an effort to delve into all the aspects of a promissory note, as well as its types and essentials. The main focus of the article is to explain promissory notes from the angle of Section 4 of the Negotiable Instruments Act, 1881. Furthermore, it explains different types of promissory notes and also how a promissory note is different from a cheque and a bill of exchange. A series of precedents is also explained to understand the evolution that the subject has undergone over the years.

Table of Contents

Introduction

Money makes the world go around, is a very commonly used phrase. Every household and every business runs on money, and the most common and old form of exchange is cash. If we pick up an Indian currency note of ₹10, we can find ‘I promise to pay the bearer ten rupees’ written on it. Our minds must be tickled to know what that means. To put it in the simplest words possible, it is a promise made by the issuer, that is, the Reserve Bank of India, to the bearer of the currency note that they would never fail to pay the said amount. The same can be established by reference to Section 26 of the Reserve Bank of India Act, 1934, which provides that the Bank is liable to pay the value of the banknote. A currency note can be said to be a promissory note from the Reserve Bank of India to the bearer of that currency note.

Promissory note finds its place under the Negotiable Instruments Act, 1881. Section 13 of the Negotiable Instruments Act, 1881 defines negotiable instruments as ‘a promissory note, bill of exchange or cheque payable either to order or to bearer’. Negotiability is the main characteristic of negotiable instruments. ‘Negotiable’ means transferable, and ‘Instrument’ means a written document by which something is conveyed from one person to another. When a promissory note, bill of exchange or cheque is transferred to any person, in a way that person becomes the holder thereof, the instrument is said to be negotiated. The definition provided under Section 13 is criticised by few jurists on the basis that it provides what it includes and does not give the exact definition of negotiable instruments and that the Negotiable Instruments Act, 1881 is confined only to the three instruments, that is, promissory notes, bills of exchange and cheques.

The basics of a promissory note, starting from the essential ingredients, to its format, the parties involved, and different types of promissory notes that are made according to the specific needs, are discussed in detail in the article. Furthermore, a difference is drawn between a promissory note and a cheque and between a promissory note and a bill of exchange.

Promissory note under Section 4 of Negotiable Instruments Act, 1881

Section 4 of the Act defines a promissory note as an instrument in writing (not a bank note or a currency note) containing an unconditional undertaking, signed by the maker, to pay a certain sum of money only to, or to the order of, a certain person, or to the bearer of the instrument.

Contents of a promissory note

The basic content of a promissory note is:

- Date: The promissory note should mention the date on which the promissory note is drawn.

- Place: The place should be mentioned in the promissory note, where the note is made or drawn by the promissory.

- Amount: The specific amount of money that is promised by the drawer to be paid, should be clearly mentioned.

- Promise to Pay: An unequivocal promise to pay a specific sum of money has to be mentioned in the promissory note.

- Parties Involved: The names of the drawer (the person who promises to pay the money) and the drawee (the person to whom the payment is to be made) should be clearly mentioned.

- Signature: The promissory note should be signed by the drawer.

- Terms of Payment: The time within which the payment would be made, either on demand or at a particular future date, should be mentioned.

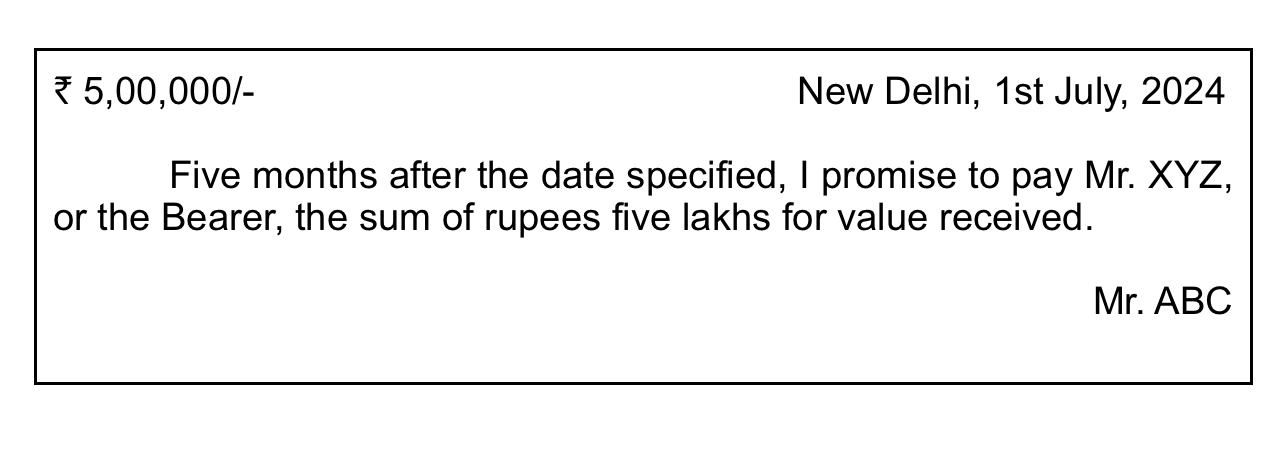

Format of a promissory note

The usual form of a promissory note is as follows:

Essential ingredients

Written form

The very first essential of a promissory note is that it must be in written form. It may be printed or lithographic. A promise made orally does not constitute a promissory note. Additionally, the note should be signed by the maker.

Express undertaking to pay (Promise to pay)

There must be an express undertaking on the part of the maker of the promissory note to pay the amount specified. A mere acknowledgement of the debt is not a promissory note. The same was held in the case of Nawab Major Sir Mohammad Akbar Khan vs. Attar Singh (1936).

At the same time, a mere receipt of money also does not amount to a promissory note, even if it may contain terms of repayment. The undertaking to pay the amount must be expressed and not implied. A reference can be made to the case of Bal Mukund vs. Munna Lal Pammi Lal and others (1970), where the debtor had not expressly promised to pay the specific amount, but there was an acknowledgement of indebtedness with regard to the definite sum of money, which was to be paid on demand, was held to be a valid promissory note under Section 4 of Negotiable Instruments Act, 1881. Furthermore, the amount specified in the promissory should be specific and not a lump sum.

Let’s take an example:

‘A’ promises in writing to pay ‘B’ a sum of ₹50,000 after deducting the rent that ‘B’ owes to ‘A’. For a promissory note to be valid, the amount mentioned in the note should be specific. Thus, in this case, the promissory note drawn by ‘A’ is not valid.

Promise should be unconditional

The promise to pay the money should be completely unconditional and not based on any event or condition. The exception here can be an ordinary condition or an experience of mankind that is bound to happen one day or the other. For example, the death of a person may not be definite, but it is bound to happen. So, if ‘A’ puts up a condition in the promissory note that she will pay the sum specified to ‘B’ after ‘C’ dies, it is a condition but does not make the promissory note invalid because such a condition is bound to happen.

Reference can be made to the judgement of the Kerala High Court in the case of S.S. Namboori vs. Mathai Abraham (1973). The condition posed in the case was that the petitioner agreed to settle the accounts as per the promissory note after the litigation came to an end. The court held that such a condition made the promissory note invalid as the promise was conditional, and it was uncertain as to when the litigation would come to an end, even though it would come to an end someday.

Promise with respect to money only

The promise made in the promissory note must be with regard to the money only. Therefore, a promise made to deliver jewellery in a written form with all the essentials of a promissory note cannot be considered to be a promissory note. Moreover, the amount of money payable must be certain or definite.

Certainty of parties involved

The promissory note must clearly mention the name of both the maker and the payee. Therefore, both parties must be indicated with certainty on the face of the instrument. The reference for the same can be made to the case of Lala Jethji vs. Bhagu (1901), where the promissory note was made in the form of a Khata book. It provided the specific amounts to be paid, but there was no specific mention of whom the amount was to be paid. Therefore, it was held that uncertainty with regard to any of the parties makes the promissory note invalid.

Payable to order

The basic rule of a promissory note is that any person who has the negotiable instrument has the right to recover a definite amount of money. Section 4 of the Act uses the terms ‘to the bearer’ and ‘to the order of’. Payable to the bearer means that any person who has that promissory note can recover the money specified in it. Let’s take an example:

‘A’ gives a signed promissory note to ‘B’ saying that he will pay ‘B’ a sum of ₹5,000/- and delivers that instrument to ‘B’, then in that case ‘B’ can recover the said amount from ‘A’ as a bearer of the instrument.

Payable to order means that the promissory note states the name of the person in favour of whom such a pro-note is made and also uses the words ‘to his order’. From the combined reading of Section 1 of the Negotiable Instruments Act, 1890 and Section 31 of the Reserve Bank of India Act, 1934 clarifies that only the Reserve Bank of India and the Central government have the power to issue promissory notes payable to the bearer on demand. Similarly, a bill of exchange can be drawn payable to the bearer but not on demand. Let’s

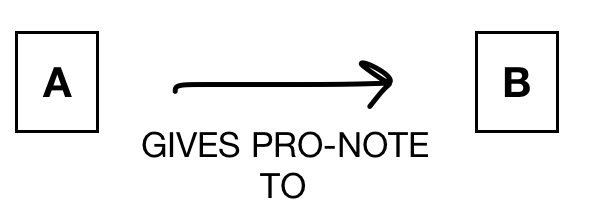

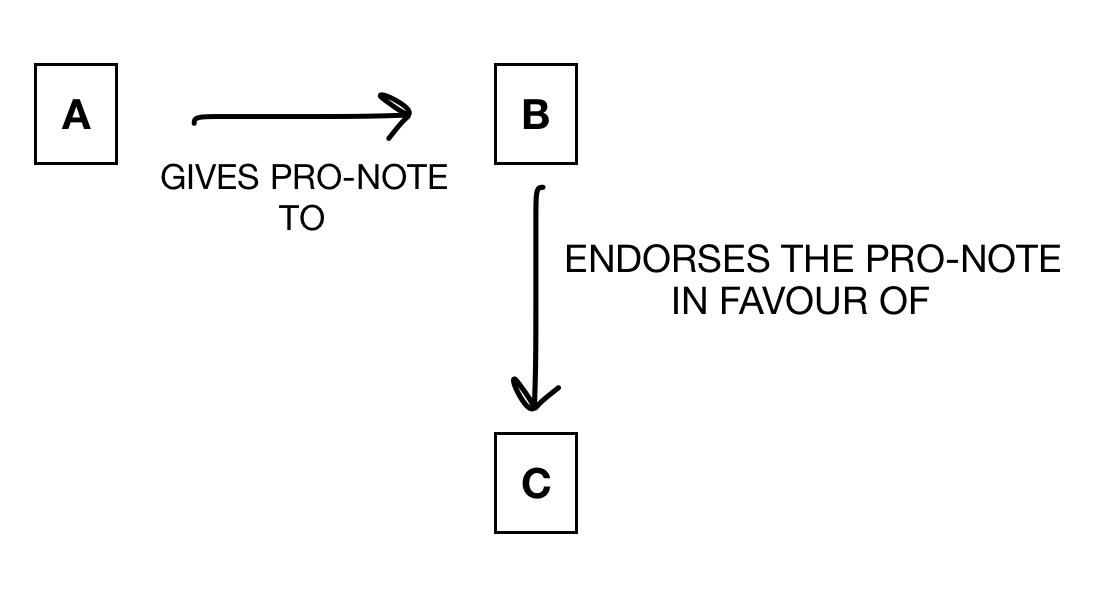

The promissory note states that ‘A’ promises to pay ‘B’ or to his order a sum of ₹5,000/-. Here, in the first instance, the money would be recoverable by ‘B’. However, if ‘B’ endorses at the back of the promissory note and delivers it to ‘C’, then ‘C’ being the bearer of the instrument, on the order of ‘B’, can recover the amount from ‘A’.

Parties to a promissory note

There are two parties to a promissory note:

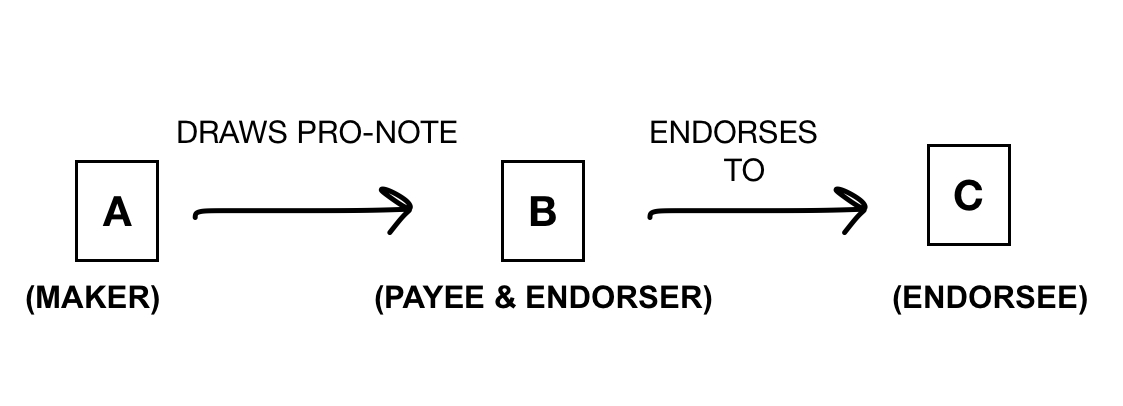

- Drawer: The person who promises (promissory) to pay another person a specific sum of money and draws the instrument is called the drawer or maker of the promissory note.

- Drawee: The person in whose favour a promissory note is drawn or issued is called a promisee or payee or the drawee of the instrument.

If the payee further transfers the right to recover the specified amount mentioned in the promissory note by endorsing it, then the person to whom the right is endorsed is called the endorsee.

Examples

Section 4 of the Act itself provides illustrations to simplify the process of understanding the concept of promissory notes. Let’s take some examples apart from the ones provided in the Section.

- Richard borrows ₹25,000 from Samuel and promises in writing to repay the debt within a month from the date of borrowing.

All the essential elements provided under the Act are met, and hence, this is a valid promissory note.

- Jacob promised to pay Adam ₹2,000 when he won the lottery.

One of the essentialities of a promissory note is that the promise to pay should be unconditional. Hence, the promissory note is invalid due to a condition imposed, and there is no such situation where it can be said that it was bound to happen or that Adam was bound to win the lottery.

- Andrew draws a promissory note mentioning all the amount of debts which are due but does not mention to whom the specific amount of money is payable.

Hence, due to uncertainty as to who the specific parties to the instrument are, the promissory note is invalid as per law.

Types of promissory note

The basic purpose of a promissory note is the same in all the scenarios, but to meet the needs of different circumstances and businesses, promissory notes can be divided into the following types:

Simple promissory note

The most basic yet fundamental type of promissory note is known as a simple promissory note. It forthright involves a promise made by the borrower to repay the amount borrowed from the payee at a specified date with interest (if applicable) and signed at the end. Such a type of promissory note provides flexibility and, at the same time, a legal binding between the parties to the promissory note.

Demand promissory note

This type of promissory note is similar to a simple promissory note, but instead of a specified date mentioned on the instrument, the words used are ‘on demand of the payee’. This means that the lender can demand the amount lent at any time.

Let’s take an example:

‘A’ runs a printing business under the name of Graphic Printers. ‘A’ buys all the required material like ink, flex, and paper from ‘B’ on credit, which is recorded in the form of a demand promissory note. Here, ‘B’ can demand the outstanding payment of the materials from ‘A’ at any time.

Commercial or secured promissory note

Commercial or a secured promissory note is backed by collateral, which means that if the borrower defaults or is unable to repay the amount, that collateral can be retained to recover the outstanding debt. This collateral can be anything, including property, machinery, or any other valuable asset of the borrower.

Let’s understand with an example:

‘A’ secures a loan of ₹25,00,000/- to buy a car. In such a situation, the vehicle (car) would be considered collateral. If ‘A’ is unable to repay the amount on the date decided on in the promissory note, then ‘B’ has a right to seize that car of ‘A’ and can recover the outstanding amount lent.

Informal or unsecured promissory note

As the name suggests, informal or personal or unsecured promissory notes are not backed by any collateral. This type of promissory note works solely on word of mouth or the trust in the person promising to repay the specific amount borrowed.

Let’s understand with an example:

‘A’ borrows a sum of ₹5,000 from her relative ‘B’ and promises to repay the said amount within a month. Here, there is no collateral involved. If, in such a situation, a promissory note is drawn by ‘A’, it would be a personal promissory note that would work solely on the promise made by ‘A’ and the trust imposed on her by ‘B’.

Here, as there is no collateral involved, if ‘A’ does not repay the amount borrowed, the only recourse is filing a civil suit.

Convertible promissory note

In convertible promissory notes, there is an option with the lender to convert the money lent (debt) into equity. Generally, such promissory notes are drawn where investors or lenders put up their money in startups in the hope of substantial future gains.

Let’s understand with an example:

Catherine, owner of XYZ fintech firm, lends a sum of ₹1.5 crore to a fintech startup using a convertible promissory note. If, after five years, the startup does well, then Catherine can choose to recover the money lent (debt) in the form of equity shares of the company.

Such a type of promissory note has a two-way advantage: the startups get their investments, and the investors get an option to have equity participation in the startup.

Student loan promissory note

As the name suggests, a student loan promissory note is drawn by a student with regard to the loan that he or she has taken to finance the education. The major elements of such a promissory note are similar to that of any other promissory note but the difference lies with regard to the repayment schedules, allotment of grace periods for repayment, deferment and forbearance options and other terms that may one way or another makes the entire process a bit lenient for the students.

Let’s take an example:

‘A’ takes admission to Stanford. To pay the tuition fees he takes a loan from ABC Bank and signs a student loan promissory note.

This kind of promissory note may contain terms like a schedule for repayment of the loan by a monthly payment of ‘X’ amount starting four months after graduation for a period of ‘Y’ years. There may be terms providing a forbearance option like temporary reduction or pause in the payments during financial hardships or during his further studies.

Real estate promissory note

A real estate promissory note serves as a legally binding agreement between the borrower of the money, that would be the person who is the buyer or the developer of a property and a lender, which would in a situation involving property would be a bank or a mortgage company or a private investor. Such a promissory note serves a specific purpose where the buyer makes a promise to repay the specific amount to the lender, secured by the real estate property itself.

Investment promissory note

This type of promissory note is mainly used in private investment transactions. An investment promissory note is a promise made by the borrower (a company) to an investor, to repay the specific amount of money that has been invested. It’s a way for a company to borrow money from someone who wants to invest in them. The amount borrowed is invested by the borrower in his company or some project and is repaid with interest to the investor within a specified period of time.

In such cases, the creditworthiness and financial stability of the issuer must be assessed properly before the investment is made.

The borrower of the money often provides the lenders or the investors, with a fixed amount of return and investment opportunities in return for raising capital for the expansion of the company or for completion of any specific project.

Difference between a promissory note and a cheque

| Sr. No. | Basis | Promissory Note | Cheque |

| 1. | Definition | A promissory note is defined under Section 4 of the Negotiable Instruments Act, 1881 as a written promise by the maker to pay a certain sum of money to the payee, either on demand or on a specified future date. | A cheque is defined under Section 6 of the Negotiable Instruments Act, 1881 as a written order directing a bank to pay a specified sum of money from the account of the drawer to the account of the payee. |

| 2. | Parties Involved | There are two parties involved:Maker (one who draws the instrument)Payee (to whom the money is paid). | There are three parties involved:Drawer (writer of the cheque)Drawee (bank)Payee (person to whom payment is made). |

| 3. | Involvement of Bank | The bank is not involved at any stage. | The bank is directly involved in the process, and it is the drawee. |

| 4. | Stamping | A Promissory note must be stamped in accordance with the Indian Stamp Act, 1899. | There is no requirement for stamping in the case of cheques. |

| 5. | Signature | There is a mandatory requirement for the maker’s signature on the note. | There is a mandatory requirement for the drawer’s signature. |

| 6. | Payment | A promissory note can be payable on a future date specified on the instrument, or it can be payable on demand. | A cheque is payable on demand. The cheque issued must be presented for payment within the validity period of three months from the date of its issuance. |

| 7. | Grace Period | There is a grace period of three days from the date mentioned on the promissory note. | There is no grace period in the case of a cheque once it is presented to the bank for payment. |

Difference between a promissory note and a bill of exchange

| Sr. No. | Basis | Promissory Note | Bill of Exchange |

| Definition | A promissory note is defined under Section 4 of the Negotiable Instruments Act, 1881 as an unconditional written promise made by one person to another to pay a specific sum of money, either on demand or on a future date and is signed by the maker | Bill of exchange is defined under Section 5 of the Negotiable Instruments Act, 1881 as an unconditional written order from one person to another, directing the person to whom it is addressed to pay a specified sum of money to a third person or to the bearer of the instrument on demand or on a future specified date. | |

| Parties Involved | There are two parties involved:Maker (one who draws the instrument)Payee (to whom the money is paid). | There are three parties involved: Drawer (one who makes the order)Drawee (to whom the order is made)Payee (to whom the payment is to be made) | |

| Acceptance | There is no need for the acceptance of the drawee in the case of a promissory note. | It is mandatory that a bill of exchange must be first accepted before the payment can be demanded against it. | |

| Type of instrument | It is a promise to pay. | It is an order to pay. | |

| Liability of the party | The maker of the promissory note has the primary and absolute liability. | The liability of the drawer of the bill of exchange is secondary and conditional upon non-payment or non-acceptance of the bill of exchange by the drawee. | |

| Protest of dishonour | Protest for dishonour of the promissory note is not required and no notice is served on the drawer In the case of dishonour of the instrument. | Protest of Dishonour is required if the bill is a foreign bill and notice is mandatory to be served on all the parties concerned with the transaction. | |

| Validity period | A promissory note has a validity for a period of three years that starts from the date of its execution. | A bill of exchange has no validity period. | |

| Copies | There is no legal provision that allows copies of a promissory note. | Bill of Exchange can have copies. |

Important precedents surrounding Section 4 of Negotiable Instruments Act, 1881

Nawab Major Sir Mohammad Akbar Khan vs. Attar Singh (1936)

The Honourable Bombay High Court, while differentiating between a receipt and a promissory note, held that a document may seem to be a promissory note and thus can also seem to be negotiable if there are no elements prima facie mentioned indicating it to be non-transferable.

The court further observed that receipts and agreements are generally not meant to be negotiable. A receipt for money includes the terms for repayment. What the court took into consideration was that the defendants, who were experienced money lenders, did not use the special paper required for a promissory note. Instead, they used a stamp suitable for a simple receipt. Since the document used was mainly a receipt, even with a promise to repay, it cannot be considered to be a promissory note.

Kundan Mal vs. Nand Kishore (1994)

In this case, the honourable Rajasthan High Court, while considering whether the document in question was a promissory note or not, observed that three things should be looked into:

- The intention of the parties at the time of execution of the document,

- Reference should be made to the surrounding circumstances in which the document has been executed and its negotiability in the popular sense, and

- Attention should be paid to the substance of the document.

Taking all the above-mentioned pointers into consideration, a difference can be drawn between a mere acknowledgement or receipt of consideration and a promissory note.

M. Nyamathulla vs. A. Chitaranjan Reddy (2008)

In this case, the division bench of the honourable Andhra Pradesh High Court tried to interpret the difference between a bond and a promissory note. The court went to the extent of explaining the importance of using a comma. The court pressed upon the use of the comma succeeding and preceding the word ‘to the order of’ in Section 4 of the Negotiable Instruments Act, 1881 and observed that the comma used indicates that a specific sum of money must be paid to or to the order of the bearer of the instrument. The honourable court went ahead and exclaimed that had there been no use of a comma in the provision, the present reading of that provision would not have been permissible, and hence, there would have been no difference left between a bond and a promissory note.

The Court further put forth that the legislature clearly intends that a promissory note must include an unconditional promise to pay a specific amount of money to a particular person or to their order. One cannot separate the sentence into two, to mean that the promise can be either to the named person or to their order. Splitting the sentence would make it confusing and illogical. Additionally, the court stated that for a document to be a promissory note, it must include the words ‘to the bearer’ or ‘to the order.’ These words must be read together, not separately.

Mallavarapu Kasivisweswara Rao vs. Thadikonda Ramulu Firm (2008)

In this case, the honourable Supreme Court took into consideration Section 118 (a) of the Negotiable Instruments Act, 1881, which provides that a court is under an obligation to presume that a promissory note was made for consideration till the point something contrary is put forth. Furthermore, the initial burden with regard to the same is on the defendant to prove that consideration is non-existent by bringing on record the facts and circumstances supporting the non-existence of the consideration. The court referred to the judgement of the Supreme Court in the case of Bharat Barrel & Drum Manufacturing Company vs. Amin Chand Payrelal (1999), the court observed that if the defendant can show that it is unlikely or doubtful that there was a valid consideration, or that the consideration was illegal, the burden of proof shifts to the plaintiff. It is then upon the plaintiff to prove that the consideration existed. If the plaintiff fails to do it, they will not get any relief based on the negotiable instrument. However, if the defendant cannot show that there was no consideration, the plaintiff is entitled to the presumption that a valid consideration exists under Section 118(a).

The court in the present case upheld the observation made by the court in the Bharat Barrel case and hence held that as per the facts of the case, the promissory note was duly executed by the defendant, and once the execution of the promissory note has been proved, the benefit under Section 118 (a) of the Act passes on to the appellant because the respondents had failed to discharge the initial burden.

Conclusion

Section 4 of the Negotiable Instruments Act, 1881 deals with promissory notes, which are an effective way of giving and taking loans, making clear the amount borrowed, repayment plan, interest rate, and other details. The precedents set by the courts over the years have widened the scope of the instrument but, at the same time, clarified the minute elements that need attention to differentiate a promissory note from a receipt, bond or mere acknowledgement of payment.

There are benefits of drawing a promissory note as it provides clear and legally binding terms, reduces misunderstandings, and offers legal options if the borrower fails to repay. It is also flexible and much easier to create and understand as compared to the complex loan contracts to a common mind.

However, there are certain downsides. Promissory notes often do not have collateral, which makes it riskier for lenders in the case of a borrower making a default. Another issue is that once the terms are agreed upon, they are hard to change without making a new note. Another downside is the fixed interest rates; they can be bad if the market drops.

Overall, promissory notes are a straightforward and enforceable way to document loans but there is a need for careful consideration of the terms and potential risks that come with it for both the parties involved.

Frequently Asked Questions (FAQs)

Do currency notes fall under the category of promissory notes?

Yes, the currency notes fall under the category of promissory notes. They are bearer promissory notes. The answer to the question may seem contrary to Section 4 of the Negotiable Instruments Act 1881, which provides the definition of promissory notes and specifically excludes currency or bank notes. The reference should be made to the judgement of the Allahabad High Court in the case of Re: Section 25 of Indian Paper Currency Act, 1923 vs. Unknown (1928), where the court specified that drawing a promissory note for the payment of money payable to bearer on demand is specifically prohibited under Section 25 of the Indian Paper Currency Act 10 of 1923. Section 25 has been replaced by Section 31 of the Reserve Bank of India Act, 1934.

Is the principle of Nemodat quod non habet applicable to negotiable instruments?

Negotiable instruments are an exception to the principle of Nemodat quod non habet, which means that a person cannot transfer a better title than he himself has. So, any person taking a negotiable instrument in good faith and for value becomes the true owner of that negotiable instrument, even in a case where he takes the instrument from a thief or a finder of the instrument.

Justice Willis defines a negotiable instrument as “the property which is acquired by anyone who takes it bonafide and for value notwithstanding any defects of the title in the person from whom he took it”.

Thus, it does not matter from whom the instrument is taken. The defect in the title does not pass forward with the instrument provided it is taken in good faith and by paying the value of the same.

Are promissory notes subject to stamp duty?

Promissory notes must be sufficiently stamped with revenue stamps in accordance with the Indian Stamps Act, 1899. Reference must be made to Sections 3, 35, 62 and Item 49 of the Schedule to the Act.

References

- https://blog.ipleaders.in/difference-between-promissory-note-bill-of-exchange-and-cheque/#Difference_between_a_cheque_and_bill_of_exchange

- Avatar Singh, Introduction to Negotiable Instruments: Negotiable Instruments Act, 1881, Eastern Book Company, 2016.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications