In this article, Shreshthi Golchha pursuing Diploma in Entrepreneurship Administration and Business Laws from NUJS, Kolkata, discusses ways of computing short term capital gain.

Introduction

Capital Gain is any profit made on the sale of a capital asset such as house, car, stock, bond, etc. Capital gain can be classified into two categories- long term capital gain and short term capital gain. A long term capital gain arises when the asset is held for a period exceeding 36 months. A short term capital gain is said to arise when the asset is held for a period not exceeding 36 months. The computation of these capital gains is essential to evaluate tax which varies with different gains.

Capital Asset

Capital asset is any asset which usually lasts a long period of time and is not consumed or sold in the normal course of the business. For example, X is a government employee and he purchased a house in May 2017. This will be considered a capital gain. Capital asset can be of two types, on property and securities. Property is any real estate owned by an individual regardless of whether it is related to his/her business or profession. Securities are investments held by an FII as per regulations under the SEBI Act of 1992.

If the transfer of an immovable asset takes place within 24 months of acquiring the asset, it attracts short term capital gain tax. The provision before 2017 required three years of acquisition or purchase of the property which has been brought down to two years since March 2017. For example, X is a government employee. He purchased gold in April 2017 and sold it back on July 2017. Since he sold it within a period of two years, it will be considered a short term capital gain.

Short term capital gain on securities

The sale of securities takes place at a frequent rate than property. Therefore, the transfer of stocks, shares or bonds held within twelve months attracts short term capital gain tax. But this rule is only applicable to certain securities. The unlisted or over-the-counter securities are taxed as short term capital gain only after its trading within 24 months. The former category includes shares (equity or preference) which are listed in a recognised stock exchange in India, units of equity oriented mutual funds, listed securities like debentures and Government securities, Units of UTI and Zero Coupon Bonds. For example, X is a government employee. He purchased equity shares of SBI Ltd. (listed in BSE) in April 2017 and sold the same in June 2017. The shares are capital assets since Mr. X held them for a period of less than 12 months.

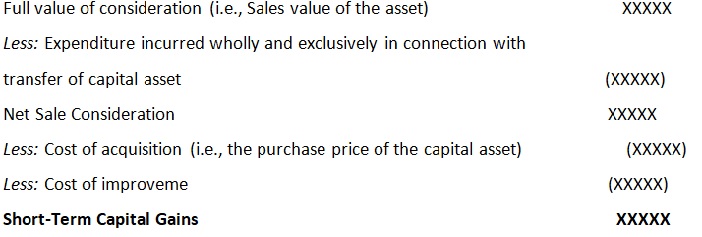

Computation of Short-Term Capital Gains

Short-term capital gain arising on account of transfer of short-term capital asset is computed as follows :

Meaning of Terminologies

- Full value of consideration: Full value of consideration is the value of the asset that the assessor received as consideration for the sale of the property. It may be in cash or in kind.

- Expenditure on Transfer: Expenditure incurred wholly and exclusively in connection with transfer of capital asset such as advertisement, brokerage, commission, stamp duty, registration fees, legal expenses, etc.

- Net Sale Consideration: Net Sale Consideration would be expenditure incurred deducted from full value of consideration.

- Cost of acquisition: Cost of acquisition is the amount at which the asset was acquired or purchased.

- Cost of improvement: Cost of improvement includes post purchases capital expenses on improvement of capital asset.

Illustration: Mr. X is a government employee. In the month of December, 2015 he purchased gold worth Rs. 8,40,000 and sold the same in August, 2016 for Rs. 9,00,000. At the time of sale of gold, he paid brokerage of Rs. 10,000. What is the amount of taxable capital gain?

Gold was purchased in December, 2015 and sold in August, 2016, i.e., sold after holding it for a period of less than 36 months and, hence, the gain will be short-term capital gain.

The gain will be computed as follows:

Full value of consideration 9,00,000

Less: Expenditure incurred on transfer 10,000

Net sale consideration 8,90,000

Less: Cost of acquisition 8,40,000

Less: Cost of improvement Nil

Short-Term Capital Gains 50,000

Short term capital gain on securities

Section 111A is applicable in case of short term capital gain arising on transfer of equity shares or units of equity oriented mutual-funds or units of business trust, which are:

- transferred on or after 1-10-2004 through a recognised stock exchange and

- such transaction is liable to securities transaction tax (STT) i.e. the transaction took place through a registered stock exchange.

When Section 111A is applicable, the gain is charged to tax at15% (plus surcharge and cess as applicable).

Illustration: Mr. X is a government employee. In the month of December, 2015 he purchased 100 equity shares of X Ltd. @ Rs. 1,400 per share from Bombay Stock Exchange. These shares were sold in BSE in August, 2016 @ Rs. 2,000 per share (securities transaction tax was paid at the time of sale). What will be the nature of capital gain in this case?

Shares were purchased in December, 2015 and were sold in August, 2016, i.e., sold after holding them for a period of less than 12 months and, hence, the gain will be short term capital gain. Section 111A is applicable in case of STCG arising on transfer of equity shares or units of equity oriented mutual-funds or units of business trust which are transferred on or after 1-10-2004 through a recognised stock exchange and such transaction is liable to securities transaction tax.

In the given case shares were sold after holding them for less than 12 months, shares were sold through a recognised stock exchange and the transaction was liable to STT, hence, the STCG can be termed as STCG covered under section 111A. Such STCG will be charged to tax at15% (plus surcharge and cess as applicable).

Short Term Capital Gain Exemption

Deductions/exemptions on short term capital gains can be claimed under Sections 80C to 80U of the Income Tax Act. However, the short term capital gains which fall under section 111A cannot claim deduction.

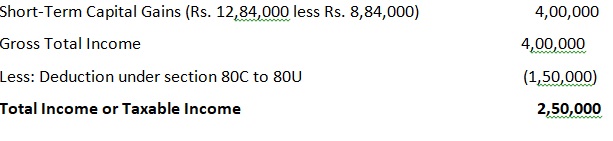

Illustration: Mr. X (age 57 years and resident) is a retired person. He purchased a piece of land worth Rs. 8,84,000 in March, 2016 and sold the same in August, 2016 for Rs. 12,84,000. Apart from gain on sale of land he is not having any other income. He deposited Rs. 1,00,000 in Public Provident Fund (PPF) and Rs.50,000 in NSC . He wants to claim deduction under section 80C on account of Rs. 1,50,000 deposited in PPF and NSC. Can he do so?

Deduction under section 80C to 80U can be claimed on short-term capital gains other than STCG covered under Section 111A. In this case, the gain is on sale of land and, hence, is not covered under section 111A. Hence, Mr. X can claim deduction under Section 80C of Rs. 1,50,000 from STCG of Rs. 4,00,000. The taxable income of Mr. X will be computed as follows :

Short term capital gain on property

If the transfer of an immovable asset takes place within 24 months of acquiring the asset, it attracts short term capital gain tax. The provision before 2017 required three years of acquisition or purchase of the property which has been brought down to two years since March 2017.

For example, X is a government employee. He purchased gold in April 2017 and sold it back on July 2017. Since he sold it within a period of two years, it will be considered a short term capital gain.2.2 Short term capital gain on securities. The sale of securities takes place at a frequent rate than property.

Therefore, the transfer of stocks, shares or bonds held within twelve months attracts short term capital gain tax. But this rule is only applicable to certain securities. The unlisted or over-the-counter securities are taxed as short term capital gain only after its trading within 24 months.

The provision before 2017 required three years of acquisition or purchase of the property which has been brought down to two years since March 2017. For example, X is a government employee. He purchased gold in April 2017 and sold it back on July 2017. Since he sold it within a period of two years, it will be considered a short term capital gain

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications