This article is written by Debkripa Burman, a student of LL.B from Rajiv Gandhi School of Intellectual Property Law, IIT Kharagpur.

Table of Contents

Introduction

For more than a decade, the “Blockchain” technology and the crypto-currencies using this technology has been the centrepiece of rigorous debate and discussion and no wonder the legal fraternity is influence by this ‘Tsunami’. The reason is obvious as this new technology is not only trying to replace the traditional existing system of currencies (i.e. dollars, rupees, pounds etc.), it is also trying to influence the existing data storing mechanisms, data protection mechanisms, system transparency. In this article, I will try to make the readers understand the basics of the Blockchain technology, the working of cryptocurrencies such as Bitcoin and the legal complexities regarding the protection of this technology as well as the crypto-currency.

Existing currency systems and its drawbacks

In ancient times, before the invention of any currencies, trade used to happen in the mutual exchange of goods. However, when the trade started happening in the larger community, people realized the existing flaws to that system i.e. the value of goods, which is inherently dependent on the abundance or availability of the good, the labour of production and the demand of the goods, were not same. They needed a common medium that is capable to represent the true value of the product. Currency in the form of metallic coins, notes became that medium of exchange and the regulatory bodies were established to verify and regulate transactions of those mediums efficiently and effectively. One of the primary duties of these regulatory bodies is to verify the prospective transaction and keep a record of those transactions in a ledger.

But as the technology evolved, the process of manually entering the transaction records in a ledger was transformed into digitally inputting the data into a database of a server which is maintained by the financial institution (i.e. banks). The transactions became faster, more convenient and secure. However, this existing system of our time is also not the ideal system i.e. it has its drawbacks—

- As the present system is centrally regulated by a regulating authority (banks, government etc.) they charge a specific amount from every single transaction as a service charge. Therefore, if A is trying to send money to B 100 dollars, B may end up receiving only 98 dollars. The missing 2 dollars is charged by these regulating authorities.

- As these days, almost all the transactions happen digitally i.e. through the internet, there is always a possibility of security threat by hackers. As all the transaction histories, accounts information are stored in the bank server, hacking into the server, altering the data and stealing account information is not absolutely avoidable.

- Another problem that often happens in the traditional system is double-spending. Double spending happens when a person initiates a transaction at the same time to two different persons. Both of the receiving persons may receive the money that the sender intended to send, but the sender may not have the cumulative amount of money in his account that those two persons received.

On the backdrop of these drawbacks, the crypto-currency concept was evolved. Cryptocurrencies are virtual currencies which intends to mitigate the existing drawbacks of the traditional system and provide the consumers with a more secure, robust, charge-free digital transaction system.

The emergence of Cryptocurrencies and the Blockchain technology

In 2009, based on the paper published by Satoshi Nakamoto, Bitcoin was introduced globally as an electronic cash system with an aim to replace the traditional currency systems. Bitcoin was introduced based on an advance data storage management system named ‘Blockchain’ technology. This technology is the heart of every cryptocurrency system out there presently. Therefore, before understanding Bitcoin we need to understand what Blockchain technology is.

To understand the system easily, we will take the help of an example. Let’s suppose you and your friends often go out together and spend money to buy things or have foods. Most of the time one of you will pay for the expenses and later you and your friends settle the monies amongst yourselves. But many times it happens that, you do not settle right away after the payments; rather at the end of each month you settle the payments based on each other’s lending and borrowings.

For this purpose, you may have kept a ledger or record where all the transactions between you and your friends are stored. This type of ledger is generally online and publicly accessible and anyone of you peer, that means your friends in this case, can add any transaction line in the ledger. Now, suppose one of your friends adds a transaction line that you have paid to him some money. But actually, you did not send any such money to him. Then how you or others can prevent that friend to do such things? This is where cryptography comes in. Using cryptography, you and each of your friends will be assigned a pair of private key or secret key (SK) and public key (PK). Where, SK is similar to a PIN of an ATM card, which is not to be shared and PK is visible to anyone. These SK and PK are strings of binary bits and are linked with each other.

When a transaction line is generated, it is joined with the SK generating a ‘Signature’. This Signature along with the transaction line and PK generates a valid transaction line.

Sign (transaction line, SK) = Signature

Verify (transaction line, Signature, PK) = True (if valid)/ False (if invalid)

↑

256-bit binary number

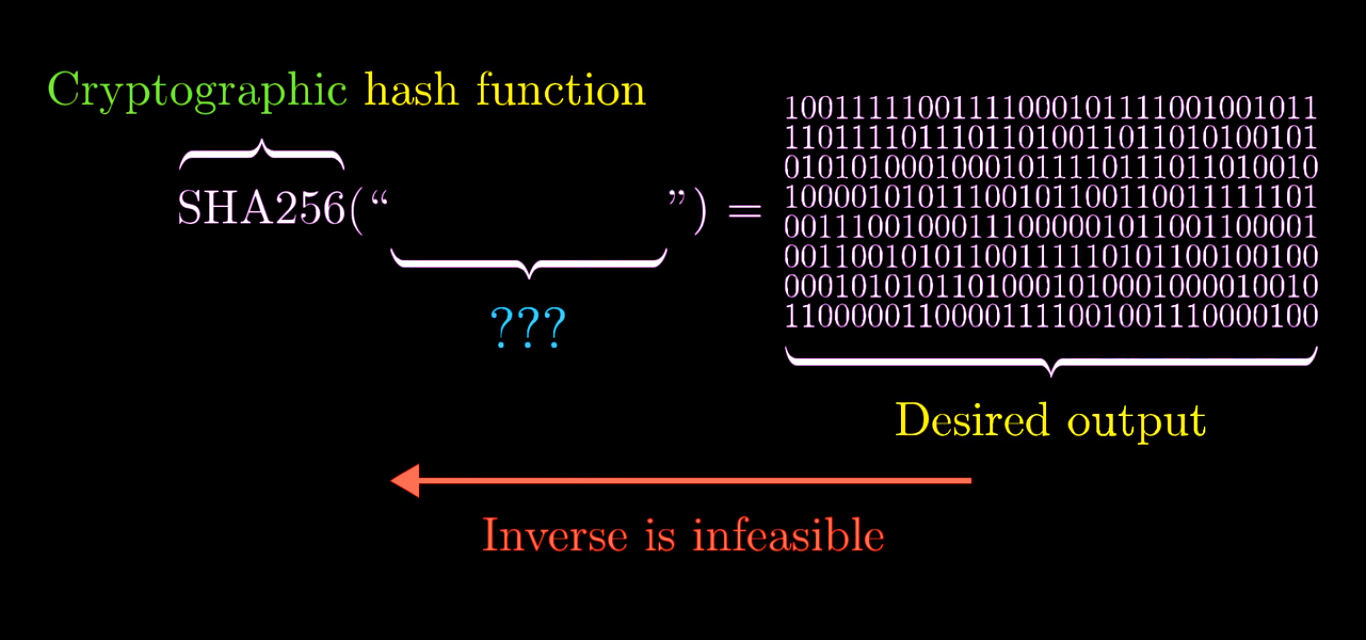

One thing to note that the Signature is 256-bit binary code and even if any one of your friends knows the PK and the transaction line, he needs to find that particular Signature in order to validate such transaction line which is nearly impossible because he may have to guess almost 2256 times to get that particular Signature. Moreover, each transaction line in a ledger is associated with a unique ID. Therefore, a transaction line added in a ledger is valid only when that transaction line is generated by the sender with his unique SK.

Now, as stated that this ledger is online and publicly accessible, the obvious question arises who controls the rules of adding new lines in the ledger. This is where the most significant difference between a crypto-currency system and traditional system appears. There is no central authority like banks to control the rules regarding the addition of transaction line in the ledger; rather everyone in your peer group will have the copy of the ledger (for now, let us take it as ledger for better understanding). Whenever a valid transaction is made by you or any one of your friends, the sender will add the transaction line to his copy of the ledger and broadcast it to the other members of your group so that others can update their ledger copy as well.

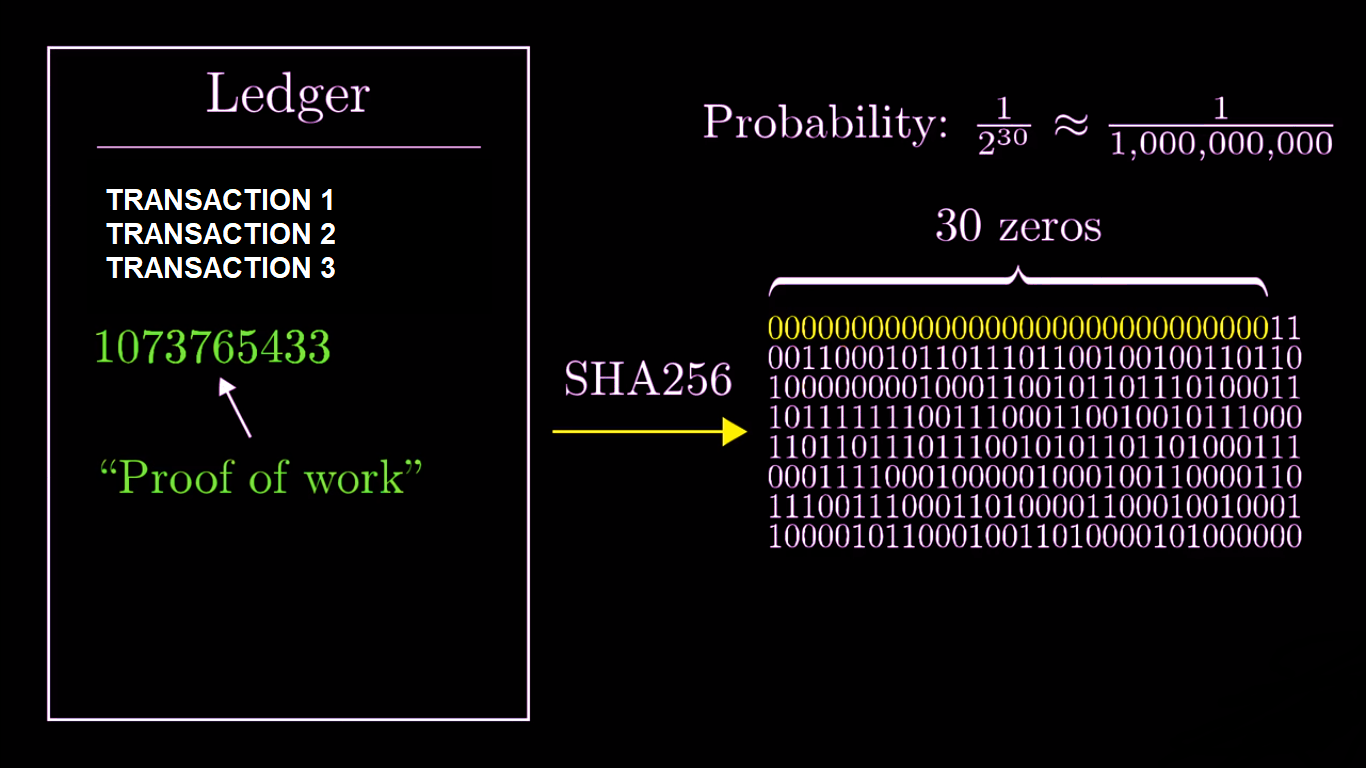

But how will the sender assure that other members of the group also updated their ledger copy with the new transaction line? Also if you are sending or receiving multiple transactions, how to assure others in your peer group will maintain that exact order of transaction? This is where the Miners come in. Miners can also be a part of that peer group, and it can be you or it can be your friend or it can be a group of friends. The work of Miners is to add a unique number at the end of the list of transactions in the ledger which when hashed using a cryptographic hash function (ex. SHA256 hash function) generates a 256-bit code that contains specified bits. This is called validating the ledger by Proof of Work (PoW).

For example, suppose after hashing, the first 30 bits of the desired 256-bit binary output code, must be zeroes (‘0’). The Miners have to find that unique input number or alphanumeric that, after hashing, generates the desired output of 256 binary code whose first 30 bits are zeroes. This involves a huge amount of complex computational work and requires a relatively longer amount of time (almost 230 permutation and combinations). Proof of Work is intrinsically linked to the list of transactions in the ledger.

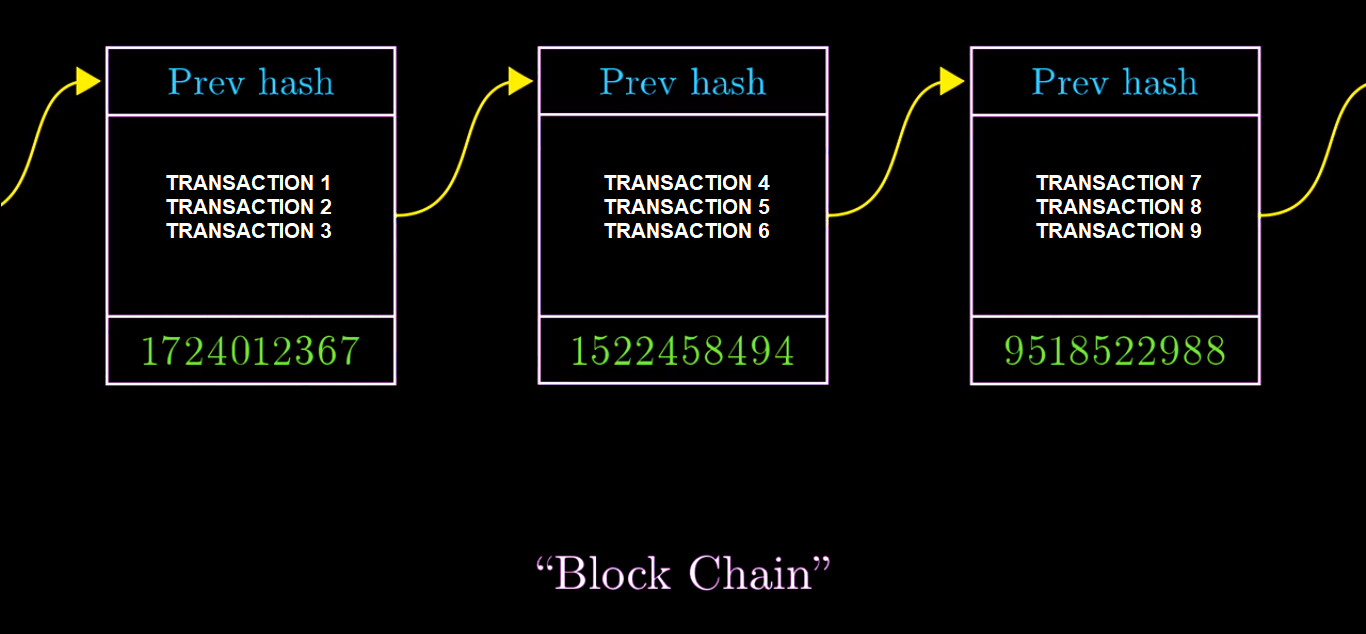

Therefore, if a single change is made to the list of transactions, the resulting 256-bit binary code after hashing will completely change and the process of finding the unique number has to be done again. When this successful hashing is completed, the ledger containing the list of transactions along PoW is turned into a Block. Generally, each Block contains on an average 2400 transactions, after which subsequent transactions are recorded in a new ledger which after being validated by PoW becomes another Block. This way the Blocks containing information are created. Just like a transaction line is validated by the sender with a Signature, a Block is validated by its PoW. Now, each Block contains a timestamp, PoW and the hash code of the previous Block (example: the 256-bit code containing initial 30 zero bits) based on which they are systematically arranged. This arrangement of Blocks in a systematic way creates a Blockchain.

This Blockchain is then shared to each individual in the system and it is periodically updated whenever a new Block gets verified. Therefore, if anyone in your peer group tries to change single information in any Block or change the order of the Blocks, it will create a ripple effect in the entire Blockchain till it reaches the beginning (Genesis Block) and all the works have to be redone again which is practically impossible for a Miner or any other in the peer group and this may lead to the failure of the Blockchain.

Now that Blockchain is somewhat understood, one can now question what is Bitcoin and where it comes from? Simply put, Bitcoin is nothing but a cryptocurrency that records the live transaction history. Bitcoins are generated when a Miner successfully completes a PoW of a Block. It is embedded in the Bitcoin algorithm and the Source Code that when a Miner completes the PoW of a Block he will receive a certain amount of Bitcoins that comes from no one but the system itself and this increases the total number of Bitcoins in the ecosystem. This is the reason they are called ‘Miners’ because they literally create wealth in the system. However, there is a limitation put by the inventors of the Bitcoin algorithm i.e. the rewards gets halved every 2,10,000 Blocks generated by the Miners worldwide. It approximately takes 4 years to generate 2,10,000 Blocks. Initially, it started with rewards of 50 Bitcoins per Block but now it is only 6.25 Bitcoins per Block.

Jan 2009-Nov 2012: 50 BTC

Nov 2012- July 2016: 25 BTC

July 2016- Feb 2020: 12.5 BTC

Feb 2020- Sep 2023*: 6.25 BTC

Total Bitcoins: 210000*(50+25+12.5+6.25+……) = 2,10,00,000

This is the reason it is said that there will never be more than 2.1 Crores of Bitcoins ever. But at the same time, as the reward is halved and it takes approximately 10 minutes to generate a Block, it may take approximately 120 years more from now (around the year 2140) that all the Bitcoins will be mined.

Advantages of Bitcoin over the traditional currencies

- Firstly, Bitcoins or any other crypto-currency systems are decentralized systems unlike traditional currency systems. Every transaction in the traditional currency systems happens through the banks which charge a certain amount in each and every transaction as service charge. While in the crypto-currency system there is no such central authority and therefore there is no such service charge involved.

- Secondly, in the traditional currency systems, a trust issue is involved i.e. you have to trust the bank that the bank will do its job honestly and as transparently as it can. On the contrary, in crypto-currency systems, there is no trust issue involved as each and everyone in the system has the copy of the Blockchain that shows every single transaction happened from the beginning. Therefore you don’t have to trust anyone and that is why it is called a trustless system.

- The chance of hacking the Crypto-currency system or committing fraud is next to impossible. The Cryptographic hash encryptions are so strong that it requires a huge amount of computational powers to reverse engineer and alter any data or any Block in the Blockchain. Plus everyone in the system has a copy of the Blockchain. So even if a hacker becomes successful in modifying the data in one computer, it is absolutely impossible to modify each and every Blockchain copy in that system.

- The problem of double-spending is omitted as both the transactions go into a pool of unconfirmed transactions where the transaction will be approved or rejected after timestamp verification. Even if both of the transactions go through, the transaction with the highest number of confirmation (acceptance of the transaction by the other members in the system) will be added to the Block. And if 6 Blocks added after that Block, containing the questionable transaction, confirms the validity of that transaction, then the sender becomes sure that the other transaction didn’t go through.

Trade Marks protection to Blockchain and Crypto-currencies

First of all, if it is not contradicted specifically, then it is safe to say that Blockchain technology was first introduced into the world through Bitcoins. Therefore, any of the arguments put forth in this section mentioning cryptocurrencies will specifically draw a reference to Bitcoins in particular. I have read two articles written by Arun C Mohan and Bhavik Shukla, beautifully explaining the issues involved concerning the trademarking of Blockchain technology and cryptocurrencies. However, I am of a different opinion than what the authors have put forth in their respective articles. Therefore, I will be dealing with the similar issues that the authors have raised in their respective articles and analyze those issues under the lens of my understanding (it is advisable to read those articles before going through this article). With this presuppositions, we will see what are the issues involved while considering Trade Marks protection to Blockchain and Bitcoins, one by one.

Issue 1: Proprietorship is one of the primary issues involved while considering the Trade Marks grant to the technology or the currency. Blockchain technology is a protocol containing several different algorithms and the Source Code. The Indian Patents Act does not provide protection to algorithms or computer programming per se [section 3(k)]. But “computer programming product” (ex. any apps) having functionality can very well be protected. Therefore in this similar line of arguments, one may very well argue that if a person, who has taken the source code, modified it and then developed an app that lets the user use the system for transaction in a unique way, can it not be patentable? And if that app is granted patent protection and that app is being used in course of trade (in this case, for transactions) can it not be Trade Marked?

In fact, Craig Wright – who at one time claimed to be Satoshi Nakamoto, the alleged founding father of Bitcoin – and his associates have filed over 70 patent applications related to cryptocurrency Bitcoin. More so, Coinbase, a cryptocurrency exchange, has already been granted patent protection by USPTO in few of their technologies related to crypto-currencies. Therefore, if such technologies or currencies are granted patent protection, there is no reason why a Trade Mark protection concerning those technologies or currencies should not be granted if prior use and reputation can be proved.

Issue 2: Control over the system is also another issue that is connected with the issue of proprietorship. The argument that the public Blockchains are not controlled by any entity is not entirely true. As it is already established that cryptocurrency systems are decentralised systems, there is no central authority. However, it is a ‘Consensus’ based system which means that there are rules by which a Blockchain system operates and confirms the validity of the information. There are two types of ‘Consensus’- Proof of Work (PoW) as already discussed and another is Proof of Stake (PoS). Bitcoins use PoW Consensus i.e. a Block is added to the Blockchain if that Block contains valid PoW. Therefore the Miners in a system plays an influential role in the verification of the Blocks and transactions as well. Now, if a Miner or group of Miners in a system holds 51% of the total hashing rate (the rate at which total valid Blocks generated per second in the system) of the system, they control what rules to be followed or which Blocks to be added in the Blockchain. In that situation, if the Miner or group of Miners intends to apply for and adopt a Trade Mark, it can hardly be opposed by anyone.

Issue 3: The issue concerning anonymity is not of so much concern. Anonymity does not concern with proprietorship. If for the sake of argument we consider that, during the registration of trademarks, the proprietor is giving up his anonymity which in turn makes him vulnerable to many security threats including personal protection, then in the same line arguments the traditional banks also should not get registered because it is a threat to their personal protection. Besides as already discussed in the previous sections, the crypto-currency system provides so strong protection that to alter any transaction or doing any fraud it is absolutely impossible to execute such a huge amount of computational work.

Issue 4: Decentralization is the heart of the Blockchain dependant crypto-currency systems. There is no central authority like banks to trust, rather everyone in the system has the copy of the Blockchain that gives the user a full history of all the transactions that happened from the beginning. But as aforementioned in Issue 2, the Miners in the system holds a significant amount of control when it comes to the imposition of rules. If there is any dispute between Miners regarding the imposition of rules, the Blockchain may split into two- one set of Miners validating one sub-chain and another set of Miners validating another sub-chain. This is known as Forked Blockchain or Split Blockchain where previously invalid transactions are held valid by one set of Miners and added to the Block of their sub-Blockchain discarding the other Blocks validated by the other set of Miners and vice-versa. This may also lead to the creation of a new crypto-currency and in turn may lead to trademark registration of such new currency if allowed. Example: in 2017, Bitcoin Cash (BCH) separated from Bitcoin (BTC). Therefore, the paradox of decentralisation is not so easy to overcome just yet.

There is one thing we need to remember while we consider these issues. The purpose of granting trademark is not only to indicate the origin of the goods or services but also to prevent counterfeiting and passing off. The primary purpose of granting trademark protection to Bitcoin or for that matter any other crypto-currency is to prevent counterfeiting and passing off so an unwary cryptocurrency enthusiast does not get cheated. Granting trademark protection will also enable the proprietors to take actions against such frauds in the court of law.

Conclusion

The issue of trademark-ability of the Blockchain technology and the currencies is pertinent and, indeed, the world is not yet quite prepared to gulp the consequences of this technology. However, the popularity it has gained, certainly cannot be overlooked. Law always wants a systematic social structure to avoid confusion and havoc. But the evolution of the internet and the advancements in the digital domain has somewhere shaken the stability of this structure. Thus, the principle that the law sought to adopt in this kind of situation is- one which cannot be prevented, can be regulated. Human beings are full of virtues and vices and sometimes these vices cannot always be prevented.

In this instance, the crypto-currencies certainly has the features to overcome the drawbacks of the existing currency systems and therefore it poses a threat to such traditional systems. The law can provide physical barriers in the societal structure but how will it provide a virtual barrier? Thus, on such occasions, it is better to regulate it than to exclude it. Bringing it under the purview of law is, in some cases, a better choice than keeping it outside the purview of law; there is always some rooms left to hold somebody responsible. Therefore, striking down the RBI’s ban dealing with crypto-currency is, in my opinion, a welcoming decision passed by the Hon’ble Supreme Court of India. In conclusion, I agree that we may not be ready to deal with this ‘Beast’, but we should not miss the opportunity to ‘Apprehend’ it.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

under Muslim Law")

")

Allow notifications

Allow notifications