This article is written by Samrudhi Garnaik, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from LawSikho.

Introduction

This article will provide an overview on Zomato’s journey and how over the years it has moved from a small private company to finally hitting the public market. While looking at the bigger picture, the author will provide you a sneak peek on the funding that Zomato has raised over time and how it has strategically acquired companies. The article will discuss the minimum requirements for raising an IPO and it will walk you through the process of IPO. It will essentially help the readers to understand and gauge the right time for making the big step along with the correct procedure. The author at the end will discuss the potential threats that the company might suffer.

Tracing Zomato’s Journey so far

Zomato was founded in the year 2008 as a private company and the erstwhile name was “Foodiebay”. It later renamed itself, Zomato, in the year 2010. It is a food tech company and initially started as a platform to discover and review restaurants. Later it delved into the food delivery business. Fast forward to 2018, Zomato is trying to capture the entire food business space in restaurants starting from supplying raw materials through its initiative “Hyperpure” to the delivery of the product. In early 2020, Zomato announced the acquisition of Uber Eats in India. It was indeed a very typical and different type of acquisition. Zomato claimed to have acquired Uber eats through a whopping all stock deal of 350 Million USD in lieu of 9.99% shares in Zomato. Uber Eats India is a wholly owned subsidiary of Uber Eats Inc. which is again a fully owned subsidiary of Uber Inc. registered in California. Zomato, Uber Eats and Swiggy are all food tech companies. There has been a cut throat competition between Zomato and Swiggy to remain as the most aggressive player in the market. According to studies, UberEats was never able to compete at par and hence was acquired by Zomato. With the acquisition of Uber Eats, Zomato holds a dominant position of 55% of market share.

Zomato as on date has already done 14 acquisitions and has raised a total funding of $1886.6 million from investors. The current valuation of the company stands at $5.4 billion. Over the period of 12 years, Zomato has established its brand name and has earned a reputation in the global market. Zomato is present in 24 countries and 10,000 plus cities. Zomato has successfully placed itself in the hit list of the investors and the company is mostly backed by venture capital funding. Zomato plans to raise an IPO up to $ 1 billion in the first half of 2021 and with this it is eyeing a valuation of about $8-10 billion. Ahead of Zomato’s IPO, the company has turned itself into a public company and the new name is “Zomato Limited”. With that as the background, now let’s understand what is the first entry barrier that Zomato or for that matter any company would face while entering the IPO market.

Gauge if your company is “IPO READY” vis-a-vis Zomato

In this part we will be discussing the way to determine if a company is “IPO Ready”. The first step that a company has to undertake ahead of an IPO is to turn itself into a Public company. The shareholders must approve the conversion of the company from private to Public via a special resolution and the MOA and AOA must be amended accordingly. All the stipulations with respect to number of members, directors, share capital etc. must be complied with and such must be filed with the registrar within 30 days of the passing of the resolution along with the prescribed fees.

Secondly, in the pre- IPO regime the eligibility criteria for a company to list is twofold. A company has to be eligible as per the conditions stipulated by:

- SEBI

- Respective stock exchanges

- SEBI has stipulated the eligibility norms for companies planning an IPO which are as follows (Section 6 of Issue of Capital and Disclosure Requirements):

-

Entry Norm I (Profitability Route)

a) Net tangible assets of at least Rs. 3 crores in each of the preceding three full years of which not more than 50% are held in monetary assets. However, the limit of 50% on monetary assets shall not be applicable in case the public offer is made entirely through offer for sale.

b) Minimum of Rs. 15 crore as average pre-tax operating profit in at least three years of the immediately preceding five years.

c) Net worth of at least Rs. 1 crore in each of the preceding three full years.

d) If there has been a change in the company’s name, at least 50% of the revenue for preceding one year should be from the new activity denoted by the new name.

e) The issue size should not exceed 5 times the pre-issue net worth.

Alternative routes

To provide sufficient flexibility and also to ensure that genuine companies are not limited from fundraising on account of strict parameters, SEBI has provided the alternative route to the companies not satisfying any of the above conditions, for accessing the primary market, as under:

-

Entry Norm II (QIB Route)

Issue shall be through book building route, with at least 75% of net offer to the public to be mandatory allotted to the Qualified Institutional Buyers (QIBs). The company shall refund the subscription money if the minimum subscription of QIBs is not attained.

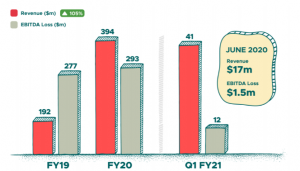

Now, SEBI’S ICDR regulations allow only the profit-making companies to get listed in India. As per the mandate, a company needs to have a minimum 15 crores of pre tax profit. This essentially cuts down on most of the start-ups in India because most of the start ups are loss making entities. Zomato is a venture capital backed start up and has been tremendously doing well as far as revenue and customer acquisition is concerned. Zomato’s revenue for the financial year 2020 grew by 105% to $394 million while the losses soared by 6% to 293 million. However, there is a provision for the loss-making companies to raise an IPO, where 75% of the net public offer has to be allotted to QIB’S only. And only the remaining 25% can be allotted to the Non-Institutional Investors and Retail Investors. But such a provision proves disadvantageous to the companies. A lot of start-up IPOs are lost to NASDAQ due to the stringent requirements of SEBI. Indian start-ups like Yatra & MMT have all listed themselves on the NASDAQ since almost all the start-ups were initially running on loss.

Looking at the SEBI’S requirement, it can be said that since Zomato has never been in profit, therefore it cannot essentially list itself in India via the profitability route. It only has the option to list through the QIB route. But what seems to be a frenzy is whether Zomato will list in India or we will lose Zomato to NASDAQ as already seen in a lot of startups.

-

Stock exchange

The eligibility criteria for listing in NSE or BSE is more or less the same with additional compliances in NSE. The eligibility criteria for listing in NSE are as follows:

- Paid up Capital and Market Capitalisation

Minimum paid up equity capital should be 10 crores (post issue paid up equity capital for which listing is sought is taken into account).

Minimum capitalization of the applicant’s equity should be 25 crores (capitalisation will be the product of the issue price and the post issue number of equity shares. In respect of the requirement of paid-up capital and market capitalisation, the issuers shall be required to include, in the disclaimer clause of the Exchange required to put in the offer document, that in the event of the market capitalisation (Product of issue price and the post issue number of shares) requirement of the Exchange not being met, the securities would not be listed on the Exchange.

- At least three years track record of either the applicant seeking listing; or the promoters/ promoting company, incorporated in or outside India or partnership firm and subsequently converted into a company (not in existence as a company for three years) and approaches the exchange for listing.

- Requirement for promoter– Promoters mean one or more persons with minimum 3 years of experience of each of them in the same line of business and shall be holding at least 20% of the post issue equity share capital individually or severally.

- Following are certain other requirements which a company has to follow to list its share in the stock exchange successfully.

- Company has to submit annual reports of three preceding financial years to the NSE.

- Provide certificate with regards to the following:

- That the company has not referred to the Board of Industrial & Financial Reconstruction (BIFR) &/OR No proceedings have been admitted under Insolvency and Bankruptcy Code against the issuer and promoting companies.

- The company has not received any winding up petition admitted by a NCLT.

- The net worth of the company should be positive. (Provided this criterion shall not be applicable to companies whose proposed issue size is more than Rs.500 crores).

- Satisfy the exchange on the following:

- Redressal mechanism of investor grievance;

- Defaults of payment.

Process to raise an IPO

Now let’s look at the most important segment of the article where we discuss the steps for a company to raise an IPO.

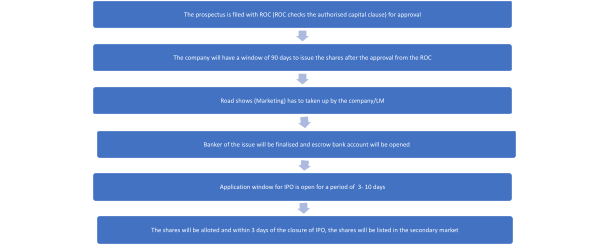

- Hiring an Investment Bank: When a company announces that it wishes to raise an IPO, a lot of investment banks typically approach the company to be their Investment Banker for the IPO and post which the company selects and hires an investment bank (At this stage, Company will enter into a MOU with the IB) and they are called as Lead managers to the issue or Book Running Lead Managers (BRLM). There can be more than 1 LM in an IPO process but the scope of work should be clearly defined in the agreement. The role of the LM starts with due diligence of the company and ends with finally listing the shares in the stock exchange. The investment bank might also be the underwriter for the shares and thus an underwriting agreement must be entered upon.

The below flow chart will explain the pre issue process that is undertaken by the BRLM.

- Price of the Issue: Company can arrive at the share price in two ways:

- Fixed price offer: In this the price of the share has already been fixed by the company. Thereby meaning that the draft prospectus would already have information on the price of the share and the number of shares to be listed.

- Book Building offer: In this, the price of the share has not been fixed by the company and the company provides a band of price. The shareholders bid for the same at the price they feel convenient and the price at which maximum bids come through is considered as the issue price for the company. In a book building offer, the Initial prospectus so drafted is called as Draft Red Herring Prospectus.

The flow chart is the continuation of the process described above.

Zomato has appointed Kotak Mahindra Bank as the lead merchant bank for the proposed IPO and has appointed Cyril Amarchand Mangaldas & Indus law as their legal advisors. Zomato’s CEO, Deepinder Goyal, has mentioned in a press statement that there will be 100% primary offering and no investor is likely to exit the company.

Conclusion

Zomato is a loss-making growth unicorn. Does it not sound very metamorphic to address Zomato as a loss making yet growth Unicorn? Wait, read to find out more. Well, Zomato is one such start-up which is staring at a huge loss, fierce competition and a very tough road to profitability. Yet it will still remain as the lucrative piece of action when its shares hit the market in a few months. There is a similar story in the West as well. The case of DoorDash, a world leader in the food delivery business commands a valuation of $28 billion against an estimated revenue of $2.8 billion which currently stands at a 10x projected revenue. For Zomato, the multiple stands somewhere around 12x. Both the firms are loss making entities.

Recently, Amazon has expanded its food delivery service across Bangalore and it aims to enter the competition in the Indian Market (Read here) and similarly Paytm has joined the race as well. With these giants coming into picture, the competition is definitely going to get fierce and shall convert the market from duopoly to oligopoly in the distant future.

Certain other dynamics that may play a key role in the near future are:

- WhatsApp business and social platforms may contribute in taking away a certain pie of orders from food aggregators.

- Google may enable food ordering from Google search option directly.

- Voice assistant devices of Amazon and Google may be configured to place orders directly.

- Looking at the aggression with which Jio moves forward, it is not far-fetched to say that Jiomart might join the existing race. And similarly, flipkart might too venture into the delivery business soon.

- Restaurant chains might pick up direct delivery by using their own app and website and using third party logistics.

- Switching cost for the customers is almost Nil. And additionally, looking at the Indian market, it can be inferred with certain precision that the customer base of such food delivery business is based on the variable of cheaper and quality food. Therefore, if at a point, Zomato cuts its cost on the discounts, cashbacks etc. it offers, the customer might simply just switch to some other aggregator platform.

With all these risks, Zomato might still do well in the public markets and win its bet majorly because of two reasons:

- Zomato enjoys the first mover advantage and a dominant market share following its acquisition of Uber Eats.

- India is amongst the fastest growing food delivery markets in the entire world.

Well, it’s not really far when Zomato’s share will hit the public market, and how it unfolds would be interesting to watch.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications