This article is written by Nikita Hora, a final year student at O.P Jindal Global Law School. She is also Working as Reporter and Communication Manager at LiveLaw and an Assistant Editor for iPleaders Blog.

INTRODUCTION

The paper explains in depth about how the Indian companies and the law treat Merger and Acquisition transactions in India. The first part of the paper explains in detail what is Merger and Acquisition and what are the main things that should be kept in mind by the corporation before undergoing M&A transaction. The second part of the paper explains in detail about the regulatory framework in India for the M&A transaction. The third part of the paper mentions about the key point how the M&A transactions are taxed and get tax exemption in India under the Income Tax Act. Last part of the paper mentions about the current scenario, as was discussed in Union Budget of 2015.

WHAT IS MERGER AND ACQUISITION?

Mergers and Acquisitions is a collective term for a variety of different business transactions in which, for example, companies merge or change ownership. M&A is a great way to achieve strategic goals in a short amount of time and with relatively secure and stable result. They lend themselves to realize a big and rewarding time gain (“economies of scale”). Also the reduction of the available time and the acceleration of competitive interactions persuade the companies to act faster proactively and respond to largely unpredictable events.

The strategic objectives could be gaining the market shares, the internationalization and globalization of the company, opening new opportunities for growth, the creation of sustainable competitive advantages or fundamental change in transformation of the company, it activities and focus.

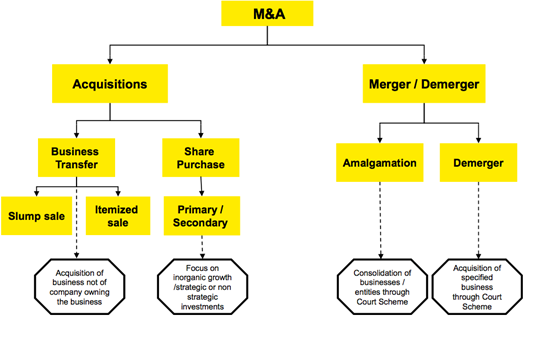

There are phases of the acquisition process which might differ from project to project. The following is the generalized form and sequential order of the M&A.

M&A pose a number of risks in each step of the processes mentioned in the above table. Numerous studies assume a failure rate of up to 75% for M&A transactions.

Mistakes made at the earlier stage usually cannot be fixed at the later stage. For example, if the strategic consideration is incorrect and as a result the paid purchases price is too high, even the most successful integration efforts cannot save the transaction anymore. An acquisition that entails entering into new business units poses special risk for the buyers.

Mergers and their processes are useful if they help to minimize the risk and do not create additional risks. Acquisitions in the related areas are generally proved to be less risky as compared to acquisitions in the new business. Experience shows that the failure rate is greater, when the endeavor is further removed from the known business and existing knowledge.

As for risk minimization, one can pass risk to the negotiating partner through purchasing price. Whether this succeeds depends upon the extent to which both negotiating sides assess the risks in the same way and what bargaining power the negotiating parties have in their hand.

The question why there is such high failure rate can only be answered on a case by cases basis. In general, the following reasons play a role in this:

- Inadequate strategic analysis of the acquisition target

- Unrealistic assessment of the acquisition target

- Over optimistic assessment of market potential

- Over optimistic assessment of the synergy potential

- Overcharged purchase price with correspondingly low return on the capital employed.

- Unmet result expectation / Return on investment

- Lack of integration of the acquired company after the acquisition

- Mismanagement

- Excessive period of negotiations

- Breach of any terms and condition in the agreement.

REGULATORY FRAMEWORK GOVERNING M&A IN INDIA

Parties to a merger or an acquisition may have their own ideas as to how the transaction is to be structured or carried out, or the rights and obligations that each party will understand. However, in order for the transaction to be enforced or upheld in a court of law, thereby giving each party the assurance that the transaction itself would not be rendered immaterial, certain law need to be adhered to.

In M&A transactions importance of consensus cannot be understated. Mostly in all the cases consensus are arrived orally but it is imperative that such consensus be captured in the document in the form of the agreement. The two primary reasons for the documentation of a consensus are:-

- Promise made by either party is often vague and must be reduced to specific rights and obligations in order to avoid ambiguity

- In the event that the parties to merger or the acquisition become involved in a dispute the parties are required to refer the dispute to adjudication

The consensus is subject to a number of laws. Certain laws restrict or prohibit the operation of certain parts of the consensus. Further, even if the consensus is not prohibited or restricted, timely information must be provided to relevant regulatory authorities. In some cases, the consensus cannot be implemented without the sanction of a regulatory authority.

+++++++++++++++++++

The basic of a merger or an acquisition is the transfer of assets and /or liabilities from one entity to another. The transfer of assets and liabilities could take place number of ways.

- By the transfer of assets and liabilities from the target to the acquirer.

- By the transfer of the entity owning the assets and liabilities in its entirety in part, to the acquire

- By the merger of the target entity into the acquiring entity.

In the case of merger and acquisition, the deal is usually implemented by the sale and purchase of the shares, business or the assets of the target or the issue of the shares of the target company in favour of the acquirer. A consensus relating to that transfer of share, business or assets is usually encapsulated in a contract. Therefore, corporation must begin with the Indian Contract Act, 1872 as it lays the cornerstone for the basis of contract enforceability in India and what contracts are valid and what are not.

The transfer or issue of share, subject to the Indian Companies Act, 1965 and Companies Act, 2013 which also contain specific provisions for the merger or amalgamation of companies. There are vast majority of mergers and acquisitions taking place by the transfer or issue of share of companies, hence the importance of Companies Act and its provisions relating to the transfer and issue of share cannot be understated. It is paramount to ensure that the procedure required for a proper transfer or issue of share is met.

There are rare occasions, where an acquisition takes place by the transfer of assets and liabilities owned by the company and not by the transfer or issue of shares of a company, Section 293 of the Companies Act places number of restriction is the sale, lease or disposal of the “whole, or substantially the whole, of the undertaking of the company, or where the company owns more than one undertaking, of the whole, or substantially the whole of any such undertaking” without the consent of the shareholders of the company. In other words, in order to effect the transfer of the whole or substantially the whole of the assets and liabilities of a company, the shareholders of the company must, by a simple majority, consent to the transfer. A question arises as to what is included in term “substantial”. The test to be applied is whether the business of the company may be effectively carried out after the transfer of assets have taken place. This means that even though the assets transferred may not be the whole of the assets of the company, nor substantially the whole, if the business of the company is reduced to a shell after the transfer, the consent of the shareholder would be required.

The shares of a public company are freely transferable under Indian company law subject to certain circumstances which have been set out in the Companies Act. Ordinarily, the broad of a public company cannot refuse the registration of transfer of shares. Conversely, an unlisted, private company may reject registration of transfer of shares. However the transferability of shares in the case of unlisted companies is even more restricted as there is no formal mechanism for the trading of a share, as opposed to a public listed company, the shares of which may be traded on stock exchange.

There are two types of share capital under Indian law- equity (equivalent to common stock) and preference (equivalent to preferred stock). The primary difference between the two types of shares under Indian law is voting power that is attached to each. Preference shareholder, under normal circumstances, cannot participate in shareholder meetings, nor can they vote on shareholder resolutions. Equity shares are equal in terms of voting rights and right to dividend. However, equity shares with differential right is also permitted for private companies. Therefore, for the purpose of the acquisition of the company, the transfer or issue of equity shares is the norm.

If the cases where the target company has been granted a concession by a state government for the construction of highway, subject to the condition that the original shareholder (the promoter) shall retain control (51% of the equity share capital) of the target company. In the course of discussion, it is found that the investment requirement of the company exceeds 49% of the equity share capital, based on the valuation of the target. In such cases, the investor may consider purchasing upto 49% of the equity share capital and the reminder of the investment to be used to subscribe to preference shares, or any other form of security instrument that the company is able to issue.

Companies Act and Contract Act are applicable in every instance of a merger or an acquisition of shares of Target Company, however there may be situations when other legislatures also come into play. In certain cases which may have an adverse effect on competition, a specific merger or an acquisition may trigger the provisions of the Competition Act, 2002 along with its subordinate legislation. In cases of M&A of the listed companies, the Securities and Exchange Broad of India (Substantial Acquisition of Shares and takeover) Regulation 2011 would also be triggered. A cross-border acquisition would attract the provisions of the extant Policy on Foreign Direct investment or the Overseas Direct Investment guidelines.

India has plethora of laws, a number of which are restricted in their application to certain industry sectors. In certain cases, M&A of a target company operating within one of these industries would be subject to the sector-specific laws. For example a concession granted by the Government of India in favour of a generation company is likely to have a minimum requirement as to the percentage of shareholding that the promoters of the company may continue to retain.

HOW ARE M&A TAXED IN INDIA?

Amalgamation means a business combination, attracting the special treatment in the various fiscal statutes. In simple terms, amalgamation is creation of the entity which either took in its fold the existing business of other entities or the creation of a new entity by pooling the businesses of various entities.

Section 2 (1B) of the Income Tax Act contains the definition of amalgamation. At the same time there is no definition of merger in the said Act. The definition in the IT act focuses attention on certain areas. First, the term amalgamation used in the IT Act refers only to amalgamation in relation to the companies and not in reference to any other amalgamation between other forms of legal entities like partnership or sole proprietorship. Second, there are two types of combination (a) merger of one or more company with another company. This is also known as absorptions. (b) merger of two or more companies to form a new company.

At the same time there are certain transactions that are excluded from the definition of amalgamation. They are: one, acquisition of property of once company pursuant to the purchase to such property in simpler words where the property of the company which merges is sold to the other company and the merger is a result of a transaction of sale; second, a distribution of property to another company due to winding up of the transferor company.

There are certain transfers due to vesting which are contemplated as following:-

- All the property and liabilities of the transferor companies before the amalgamation becoming the property of the transferee company.

- Shareholders holding less than three fourths in value of the shares in the transferor company becoming shareholders of the transferee company by virtue of amalgamation other than those already held by the transferor company in the transferee company either by itself or through its nominees.

Lastly the emphasis of the word “before amalgamation” used with regard to the transfer of assets and liabilities.

The most important aspect in the definition of amalgamation is the vesting of all property and liabilities of the transferor company to be transferred to the transferee company by the virtue of amalgamation. Similarly, the IT Act also contemplates atleast 75% of the shareholders of the transferor company becoming shareholders of the transferee company after amalgamation. All the concepts have been borrowed from the UK and the logic is not far to seek. An amalgamation presupposes the pooling of resources meaning thereby, the pooling of all assets and liabilities and continuation of the business without any interruptions. It is on the basis that particular clauses have been drafted so that all the assets and liabilities continue to exist in the hands of the transferee. If certain assets of the transferor company are excluded and not transferred to the transferee company, there cannot be effective pooling resources.

MERGER CONSIDERED AS AMALGAMATION UNDER INCOME TAX ACT

There are three conditions when merger is qualified as an amalgamation under the Income Tax Act. First, all the properties of the amalgamating company immediately before the amalgamation should become the property of the amalgamated company by virtue of amalgamation.

Second, all the liabilities of the amalgamating company immediately before the amalgamation should become the property of the amalgamated company by the virtue of amalgamation.

Third, shareholders holding not less than three fourths (in value) of the shares in the amalgamating company (other than shares already held by the amalgamated company or by its nominee) should become shareholders of the amalgamated company by virtue of amalgamation.

HOW TO CIRCUMVENT THE DEFINITION IN SECTION 2 (1B) OF INCOME TAX ACT?

Before an amalgamation scheme is proposed, the corporation needs to identify whether the definition is completely satisfied. There may be instances where the transferor company may be of the view that not all assets need to be transferred to the transferee company, probably, due to the fact that there is no synergy with respect to those assets.

If a merger proposal is mooted between these two companies, then strictly there may not be any synergy between the sugar business of the transferor and the chemicals business of the transferee. At the same time, if the definition has to be satisfied, then the only alternative is to merge both the companies as they exists at present, as the definition stipulates that all the assets and liabilities of the transferor company should becomes assets and liabilities of the transferee company. The various alternatives, going by the precedents available are ;

- merge both the companies and then later demerge for sugar business. Example is Voltas Allwyn merge and demerge.

- demerge first the sugar business by spinning off to a separate company and only later merge both the companies. Example Sarabhai Group.

TAX CONCESSIONS UNDER SECTION 2 (1B) OF INCOME TAX ACT

The following tax concessions are available if an amalgamation satisfies the conditions of Section 2(1B) and the amalgamated company is an Indian company:

- Non-chargeability of capital gain on the transfer of a capital asset including shares held by a shareholder at the time of amalgamation (Section 47(vi) and (vii)).

- Eligibility of amalgamated company for the deduction in respect of any asset representing expenditure of a capital nature on scientific research (Section 35(5)).

- Eligibility of amalgamated company for the deduction in respect of acquisitions of patent or copyrights (Section 35A(6)).

- Similar deduction in respect of expenditure of know-how as provided in Section 35AB(3).

- Amortization of expenditure for obtaining telecom licenses fees. (Section 35ABB(6)).

- Amortization of certain preliminary expenses (Section 35D(5) r/w Rule 6AB).

- Amortization of expenditure on amalgamation (Section 35DD).

- Amortization of expenditure on prospecting etc. for certain minerals (Section 35E(7) r/w Rule 6AB).

- Writing off bad debts (Section 36(1)(vii)).

- Deduction in respect of any expenditure for the purposes of promoting family planning(Section 36(1)(ix)).

- Computation of written down value of the transferred fixed assets in the case of amalgamated company (Explanation 2(b) to Section 43(6)).

- Continuance of deduction available (Section 80-IA and Section 80-IB).

- Benefit of carry forward and set off of accumulated losses and unabsorbed depreciation (Section 72A)

The Act therefore seeks to extend tax neutral treatment to transactions of mergers and demergers that is however subject to fulfillment of prescribed conditions under the Act.

TAX BENEFITS IN THE CASE OF AMALGAMATION BY WAY OF ABSORPTION

Under the Income Tax Act, the concept of Transferor Company losing its identity in the case of amalgamation by the way of absorption has a great significance. In this case, the corporate personality of the transferor company ceases to exist immediately upon completion of amalgamation. This results in the loss of benefit by carry forward of loss, as under the provision of the IT Act, only the person – the legal entity which has sustained the loss is directly attached to the assesse and not to the business nor the undertaking. Thus, if a sick company merges with a healthy company the loss will not automatically flow to the healthy company. The healthy company can avail the benefits of the losses of the sick company only by obtaining the government approval under Section 72A of the IT Act.

The losses of the sick company become the capital loss and the benefits of right to carry forward is lost to the sick company when its merges with a healthy company. as a legal entity ceases to exist consequent to the amalgamation.

When the sick company merges with the healthy company then the losses suffered by the sick is considered as capital loss in the financial sheet, therefore, sick company gets the right to carry forward its loss. The reason why sick company can do this is because after amalgamation legal entity of the sick company ceases to exist.

CAPITAL GAINS AND AMALGAMATION

Under the provision of Income Tax Act, a capital gain will arise when a capital asset is “transferred”. The word “transfer” is defined under the IT Act in Section 2(47). The word transfer means the sale, exchange, or relinquishment of the assets or the extinguishment of any rights therein or the compulsory acquisition under any law.

Shri N.A Plakhivala in his book The Law and Practice of Income tax Act rules out the incidence of capital gain in the following way. When company A amalgamates with and merges into company B and the shareholder of company A are allotted shares in company B in their own right and not as nominees of company A question arises as to whether those shareholder are liable to tax under the head of Capital Gain. It is clear that such amalgamation does not involve any exchange either within the legal meaning of the term. Whereas the allotment of shares by company B to the shareholder of company A does not involve a transfer of property by either of the two parties to the other. There is no transfer of assets by the shareholder of company A to company B: the transfer of assets of company A cannot be regarded as a transfer by its shareholders. Nor is there any transfer by company B when it allots its share capital to the shareholder of company A. The allotment of shares by the company cannot be regarded as a transfer of property by that company.

The merger does not even involve ‘relinquishment of the assets’ because relinquishment postulates the continued existence of the asset over which the right of its holder are relinquished or surrendered, whereas upon amalgamation the shares in the company cease to exist.

It is important to determine whether this constitutes a transfer under Section 2(47) of the ITA, which would be liable to capital gains tax. According to judicial precedents in this regard, including decisions of the Supreme Court till recently, this transaction did not result in a “transfer” as envisaged by Section 2(47).

In the case of Commissioner of Income Tax v. Mrs. Grace Collis and Another, the SC has held that “extinguishment of any rights in any capital asset” under the definition of “transfer” would include the extinguishment of the right of a holder of shares in an amalgamating company, which would be distinct from and independent of the transfer of the capital asset itself. Hence, the rights of shareholder of the amalgamating company in the capital asset, i.e. the shares, stands extinguished upon the amalgamation of the amalgamating company with the amalgamated company and this constitutes a transfer under Section 2(47) of the ITA.

It is clear that there is no capital gain incidence either in the hand of the shareholder of either the transferor or the transferee company; and also companies inter se.

SPECIFIC EXEMPTIONS WITH RESPECT TO AMALGAMATION

Section 47 of the Income Tax Act provides following transactions will be not regarded as transfer. The following three clauses give specific exemptions with respect to transaction involving amalgamation.

“ Nothing contained in Section 45 shall apply to the following transactions”

(vi) any transfer, in a scheme of amalgamation, of a capital asset by the amalgamating company to the amalgamated company if the amalgamated company is an Indian company;]

[(via) any transfer, in a scheme of amalgamation, of a capital asset being a share or shares held in an Indian company, by the amalgamating foreign company to the amalgamated foreign company, if—

(a) at least twenty-five per cent of the shareholders of the amalgamating foreign company continue to remain shareholders of the amalgamated foreign company, and

(b) such transfer does not attract tax on capital gains in the country, in which the amalgamating company is incorporated;]

There are wide repercussions in the context of global merger due to above exemptions. As evident from the clause, there could be cases where a capital gain incidence may arise on a foreign company holding share in an Indian company. The situation can be avoided and minimized by the following methods :

(a) By taking advantage of the relevant provision of Double Taxation Avoidance Agreement (DTAA) if any entered between the foreign country and India. Under Section 90 of the Income Tax Act, India may enter into DTAA with other countries. These DTAA apply to taxable entities which are’ residents’ in one country but have their source of income in different country thereby sitting out an equitable basis for the distribution of the right to tax different types of income between the country where source of income is located and the country of residence. Therefore the taxation rates applicable to a residence of a state which is party to such tax treaty are relaxed in the event income generated by company in the other contracting State and the assesse is not doubly taxed for the same income generated in one of the contracting states.

(b) By not directly holding the shares in the Indian Company, but instead through another investment company situated in any other foreign country where there will be lesser incidence of capital gain tax.

(c) By setting up transnational subsidiaries in typical tax haven countries like Mauritius where there is capital gain tax on the sale of movable property of a resident irrespective of the size of the property.

UNION BUDGET 2015: TAX PROPOSAL ON M&A TRANSACTIONS

With the focus of the new government moving towards improving the business environment and towards economic growth & development, there will be change in the taxation of M&A landscape as well.

The government has started the work with the retrospective amendment on indirect transfers; there is still lack of clarity on what is ‘substantial’. In that context, only “transfer of a controlling interest” in a foreign entity deriving its value substantially from assets located in India should attract tax in India. A threshold limit of transfer of more than 50% beneficial interest in the capital of a foreign entity and/or transfer of more than 50% voting power of a foreign entity could be prescribed to define “transfer of a controlling interest.”

Further, there could be other exemptions provided in context of taxation of indirect transfers i.e. no Indian tax should be imposed where say for example the shares of the foreign company are listed and traded on a stock exchange outside India or if there are intra-group transfers (where the ultimate control is not transferred outside the group) or the transactions are otherwise not ‘transfer’ as per law (for example – gift) or transactions which do not result in any transfer per se (for example primary infusion in company for acquisition of shares) or shares received by shareholders of a foreign company (having indirect stake in India) under a swap pursuant to foreign companies amalgamation / demerger. To encourage more foreign investments in India, it could be considered to exempt P-Note holders from the applicability of indirect transfer provisions.

Even the government has announced for no tax should be levied on repatriation of funds by the offshore company to its investors on account of dividend distribution, buy back, redemption, capital reduction or liquidation by the offshore company, to the extent the repatriation amount relates to the amount realized by the offshore company on sale of Indian assets on which taxes have been duly discharged, or on which no taxes or lower taxes are due on account of tax provisions or treaty benefits available, as may be applicable.

Recently government has announced that the investor of the offshore company should not be taxed on repatriation of funds such as dividend distribution, buy back, redemption, capital reduction or liquidation but the key point is tax will not be levied to the extent where the repatriation amount by the offshore company is on the sale of Indian assets where tax is duly discharged or there is tax provision or treaty benefits available to the offshore company.

Considering that acquisition through amalgamation is increasing, the benefit of carry forward of losses, pursuant to amalgamation, should be extended to all companies irrespective of the line of business.

Transactions such as transfer of shares in a foreign company by a resident or domestic company pursuant to amalgamation or demerger abroad should be exempted from capital gains tax, provided that such amalgamation or demerger is exempt from tax under the domestic tax laws of the foreign country in which such amalgamation or demerger takes place.

Some other amendments that are required include providing exemption from taxation to transactions such as receipt of shares by amalgamated company or resulting company pursuant to amalgamation or demerger, receipt of shares by Trust on settlement, genuine business/commercial transactions, issue of shares, etc.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications