In this blog post, Devyani Pokhriyal, a recent Law Graduate and a student pursuing her Diploma in Entrepreneurship Administration and Business Laws from NUJS, Kolkata, describes the need for stamp duty on issuance and transfer of shares.

Stamp Duty in India

Stamp duty is a tax collected by the government on the transfer of property. Tax is a means of earning revenue by the government for the welfare of the society as a whole, so the Indian Stamp Act was enacted to secure the revenue of the government by collecting stamp duty. The Indian Constitution has empowered the State Government to amend the stamp act for its application by their jurisdiction. Under Section 3 of Indian Stamp Act, 1899 it is stated that any transfer of instrument is bound to the payment of stamp duty.  Payment of stamp duty provides any transfer of instrument a legal recognition and also provides an evidentiary value on the court. It has to be paid by the transferor and in the case of exchange of properties; both parties have to bear stamp duty equally. Duty is paid on or before the date of execution of the instrument in a written form. The payment of duty can be made either through DD or pay order within two months. The jurisdictional sub-registrar should certify it. A stamp paper once used cannot be used again. It is payable before the execution of the document or on the day of execution of the document or on the next working day of executing such a document. Failure to pay stamp duty leads to a penalty which may vary from 2% to 200% per month and also the instrument is not admitted as evidence by the courts.

Payment of stamp duty provides any transfer of instrument a legal recognition and also provides an evidentiary value on the court. It has to be paid by the transferor and in the case of exchange of properties; both parties have to bear stamp duty equally. Duty is paid on or before the date of execution of the instrument in a written form. The payment of duty can be made either through DD or pay order within two months. The jurisdictional sub-registrar should certify it. A stamp paper once used cannot be used again. It is payable before the execution of the document or on the day of execution of the document or on the next working day of executing such a document. Failure to pay stamp duty leads to a penalty which may vary from 2% to 200% per month and also the instrument is not admitted as evidence by the courts.

Stamp Duty on Issuance of Shares

Section 3(a) of Indian Stamp Act states that every instrument mentioned in the Schedule I of Indian Stamp Act which, has not been previously executed by any person, is executed in India; shall be chargeable with a stamp duty of the amount indicated in Schedule I. Payment of stamp duty on issue of shares is in accordance with the provisions of the Stamp Duty Act in respective states as the subject falls under the state list. The stamp duty on the issuance of shares is levied upon the value of shares, and where shares are issued in dematerialized form, the duty shall be levied on the amount of securities issued.[1]

Stamp Duty Paid on Transfer of Shares

On specified transactions and documents stamp duty is paid to the government for the completion of the transfer of ownership of the property. Under the Stamp Act, the central government levies stamp duty on specific transactions of instruments like bills of exchange, cheques, promissory notes, transfer of shares. Under Constitution of India, charging stamp duty is a matter of State list, so the rate of stamp duty on the instruments varies from state to state. If any state does not have any specified stamp duty, then the amount set by central government would be levied.[2]  The stamp duty shall be paid during the time of transactions of the instrument. The stamp duty shall be levied at the time of execution of the instruments.[3]It is necessary to pay stamp at the time of execution of the instrument; as the company will not be able to register the shares unless a proper instrument of transfer duly stamped and executed by or on behalf of the transferor and the transferee has been delivered to the company.[4] The term duly executed[5] means the instrument has to be signed by the transferor and transferee on prescribed form with date of presentation, the other requirements such as particulars of the transferee, attestation by witnesses, date of execution and payment of stamp duty must.

The stamp duty shall be paid during the time of transactions of the instrument. The stamp duty shall be levied at the time of execution of the instruments.[3]It is necessary to pay stamp at the time of execution of the instrument; as the company will not be able to register the shares unless a proper instrument of transfer duly stamped and executed by or on behalf of the transferor and the transferee has been delivered to the company.[4] The term duly executed[5] means the instrument has to be signed by the transferor and transferee on prescribed form with date of presentation, the other requirements such as particulars of the transferee, attestation by witnesses, date of execution and payment of stamp duty must.

The transferor has the legal duty and liability to affix the stamps and cancel the same. But in the day-to-day practice it is the transferee who affixes and cancels the stamps. In the matter of Jainnarain Ram Lundia vs. Surajmull Sagarmull[6], the court observed, ‘With regards to stamp duty, it is not disputed that there was no previous talk between the parties on this point, though ordinarily and as a matter of law, in the case of transfer of shares, it is the vendor by whom the stamp duty is payable.’ Section 29 of the Indian Stamp Act provides that it is the liability of the transferor to pay stamp duty on an instrument of transfer. In the absence of an agreement to the contrary, the expenses of providing the proper stamp shall be borne, in the case of transfer of shares of an incorporated company or another body corporate, the stamp duty to be paid by the persons executing the document.[7]  In Union of India vs. Kulu ValleyTransport Ltd.[8] it was the seller of the shares who was responsible for the payment of the stamp duty. Before the signing the instrument chargeable with stamp duty, stamps must be affixed[9] and whoever affixes the stamps has to cancel it so the same cannot be used again.[10]The Adhesive stamps should be canceled by drawing lines across or in some other way, so that can’t be used again. However, the value of stamp should be visible. If the share transfer deed bear stamps, but it doesn’t cancel, hence transfer can’t be recorded by such transfer deed. Cancellation of Stamp by Company is illegal. If once a company transfers shares by mistake even if the instrument was not duly stamped, it can’t then apply for rectification of members.

In Union of India vs. Kulu ValleyTransport Ltd.[8] it was the seller of the shares who was responsible for the payment of the stamp duty. Before the signing the instrument chargeable with stamp duty, stamps must be affixed[9] and whoever affixes the stamps has to cancel it so the same cannot be used again.[10]The Adhesive stamps should be canceled by drawing lines across or in some other way, so that can’t be used again. However, the value of stamp should be visible. If the share transfer deed bear stamps, but it doesn’t cancel, hence transfer can’t be recorded by such transfer deed. Cancellation of Stamp by Company is illegal. If once a company transfers shares by mistake even if the instrument was not duly stamped, it can’t then apply for rectification of members.

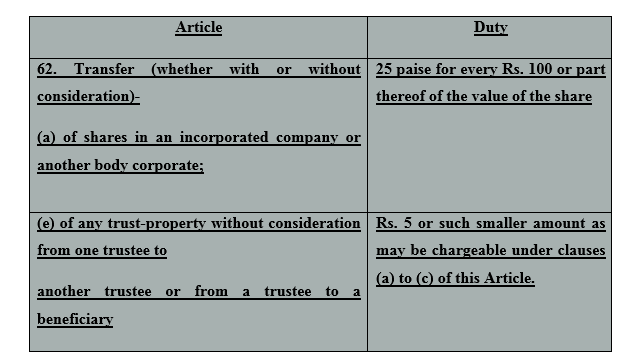

Calculation of stamp duty depends on the rate provided in the stamp act. Stamp Duty is levied at the rate of 0.25% of consideration, i.e., the amount to be paid is 25 paise for a share transfer of Rs. 100. If required, the total amount of stamp duty will be rounded off to the next or upper five paise.[11]

There is no stamp duty on transfer of shares or debentures in a depository scheme. Section 21 of the Indian Stamp Act states that where an instrument is chargeable ad valorem duty in respect of any stock, such duty has to calculate the value of such stock to the average of the value of such stock of such an instrument. When a bank holds shares as security and gets them transferred in its name, a special concessional stamp duty is payable.[12]

In the case of shares that are issued without being stamped or under stamped, the instrument which is under stamped becomes inadmissible as evidence before any authority and the document is charged with the full payment of the stamp duty as per the provision given in the act. The managing director or secretary or another principal officer of the company shall be punishable with fine which may extend to five hundred rupees.[13]Though in the case of under stamping of stamp duty on shares, collector acts as an adjudicator under Section 31 of the Indian Stamp Act, he charges for under stamping and averts invalid instruments.

Under the Indian Stamp Act, stamp duty is payable in the respect of share transfer, when a company or an issuer is liable to pay at the time of issuing securities and when shares are transferred by the person holding the title of ownership of the transferee. According to Section 8A of the Indian Stamp Act, 1899, any securities issued by the means of electronic transfer need not be stamped provided that the company or issuer of the security have paid the duty on the total amount of the security issued by it. In an electronic transfer of shares, depositories act on behalf of the issuer or company for issuance of shares to the prospective buyers. The main contention of Section 8A was to prevent the issuer of the shares from evading the payment of the stamp duty on the issuance of the shares. Also, transfer in cases of registered ownership of shares from the person to depositories or from depositories to a beneficial owner shall not be liable to any stamp duty.[14]

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

https://t.me/joinchat/J_

References:

[1] Stamp Duty on share Certificate – Abhishek Bansal, 30th Nov 2012. http://www.mondaq.com/india/x/202892/Shareholders/Stamp+Duty+On+Share+Certificates[2] Schedule VII, Entry 91 of Constitution of India.

[3] Section 17 of Indian Stamp Act 1899.

[4] Section 56 of the Companies Act 2013.

[5] Section 2(12) of Indian Stamp Act 1899.

[6] 1949 MLJ p. 476

[7] Section 29 of Indian Stamp Act1899.

[8] (1958) 28 Comp. cas. 29).

[9] Section 17 of the Indian Stamp Act 1899.

[10] Section 12 of Indian Stamp Act 1899.

[11] Article 62, Schedule 1 of the Indian Stamp Act 1899.

[12] Stamp duty on transfer of shares- G.S Rao. http://flame.org.in/KnowledgeCenter/Stampdutyontransferofshares.aspx

[13] Section 62 of Indian Stamp Act 1899.

[14] Section 8A(c) of Indian Stamp Act, 1899.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

Where to pay the statmp duty for transfer of physcical share in Bangalore?

For share certificate whose market value is 800.00 what would be the stamp price Rs 2.00 ?

For this case can we stick Rs 2.00 Revenue stamp on SH4 form?

share transfer stamp is applicable at the time of transfer of shares, can easily be purchased from any Post Office.

Entry 63 of the List-II under the seventh schedule of the Constitution of India mentions that rates of stamp duty regarding documents not covered by the Union List shall be under the State List and hence each state stamp act shall mention rates of stamp duties for the issuance of share certificates.