In this blog post, Aditya Shekhar, who is currently pursuing a Diploma in Entrepreneurship Administration and Business Laws from NUJS, Kolkata gives a detailed analysis of the taxes applicable on a restaurant bill in India.

It has often been observed that a lot of people are dissatisfied with the inflated prices mentioned in the food bill they receive after their meal. Now the bill can be divided broadly into:

-

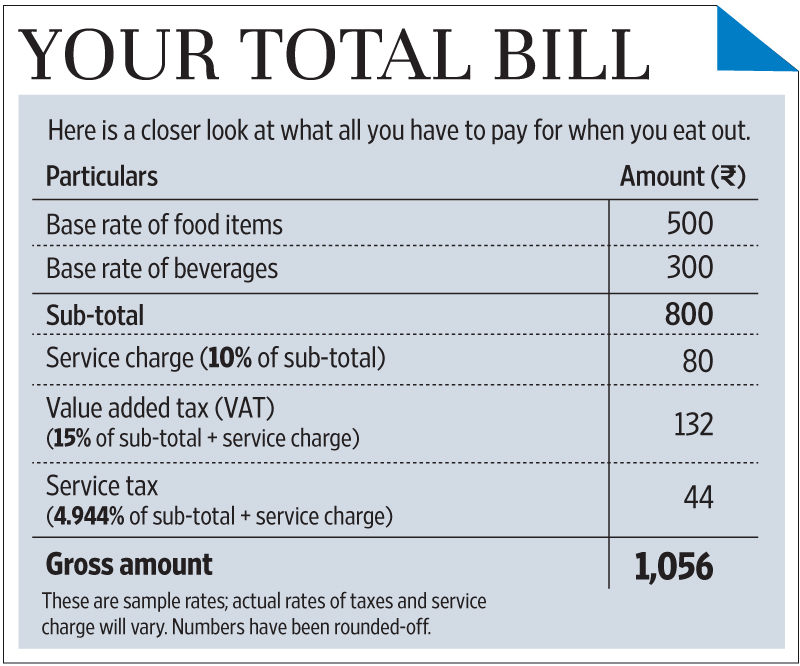

Food item’s cost

It essentially describes the price which is required to manufacture the item and depends entirely on the restaurant.

-

Value Added Tax

Value Added Taxes (VAT) are levied by the state government on the value addition to goods by an entity, who is engaged in manufacturing or distribution process.[1] The VAT is applicable specifically on the food which is made in that restaurant. If the item is packed, then VAT cannot be levied on the same, as it has already been included in the Maximum Retail Price of the item. Additionally, it is the sole discretion of a state to fix the VAT, and it can vary between two different states. Apart from that, VAT imposed on alcoholic beverages is a little higher than the VAT imposed on a food items. Recently, the Uttrakhand High Court in the case of M/S Valley Hotels and Resorts v. Commissioner, Commercial Tax Dehradun[2] gave a landmark judgment in which it held that “where element of service has been so declared and brought under the Service Tax vide Government of India Notification dated 06.06.2012, (i.e. 40% of bill amount to the customers having food or beverage in the restaurant was made liable to service tax) no Value Added Tax can be imposed thereon.” The Hon’ble Court has seemed to have addressed the issue very carefully and held that VAT cannot be imposed on the same value of the transaction.

-

Service Tax

Introduced in 1994, it was initially levied only on a specific group of goods but subsequently, in 2012, its ambit spread out to include everything except the negative list of services.[3] The Service Tax in a restaurant is charged because of the various amenities such as the ambiance, the hospitality and other facilities provided by the restaurant. The Service Tax is given to the central government and is currently pegged at around 12.36% which has been recently increased to 14%. However, since the whole bill can be attributed either to the cost of raw materials or the cost of service, therefore the tax cannot be imposed on the whole amount. Moreover, it is extremely difficult to segregate the service component and material component of the restaurant/house without inviting further litigation. The service tax law presumes a certain portion of the final invoice as the cost of material and balance as the charge of services, which is known as abatement.[4] Therefore it is to be levied only on 40% of the total bill which makes it 4.944% which has been enunciated under Section 2(c) of the Service Tax (Determination of Value) Rules 2006. Service providers are authorized to charge 40% of the bill amount only and 60% of outdoor catering.[5] The other prerequisite thing to be kept in mind while dealing with service tax is that it is applicable only on the restaurants which provide air conditioning services (fully or partially).

-

Service Charge

The restaurant owners levy this charge for the service being provided. This charge has to be displayed properly on the menu card and depends solely on the discretion of the restaurant owner and usually varies from 5% to 10%.

Conclusion

Although, most of the times we are not able to do anything when it comes to the reduction of the bill, certainly a minimal level of vigilance is required so as to ensure that the restaurant authorities do not dupe us. Recently, a lawyer based in Mumbai caught the restaurant authorities for not displaying their service charge on the menu and then later charging the same without proper intimation of the tax details. He went to the police who had no clue about the Sections to be charged against the restaurant authorities. It simply goes on to prove the amount of ignorance we have as taxpayers towards paying our taxes. Similarly, service taxes are not to be levied on takeaways and home deliveries as there is an absence of services. Also, it has become a practice nowadays that restaurants combine the food and beverages prices and tax them equally which is a corrupt practice.

Footnotes:

[1] http://lawsikho.com/learn/NUJS-EABL—-February-2016-batch/NUJS-Diploma-Course-in-Entrepreneurship-Administra/2798/11056 (last visited on June 30, 2016).

[2] http://tbauk.com/Article_Vat/Servive_tax_Vat_on_Resturant.pdf (last visited on June 30, 2016).

[3] http://www.news18.com/news/business/how-restaurants-dupe-customers-in-the-name-of-service-tax-and-service-charges-1083434.html (last visited on June 30, 2016).

[4] http://www.moneycontrol.com/news/tax/knowing-service-tax-service-chargevatrestaurant-bill_5963701.html (last visited on June 30, 2016).

[5] http://timesofindia.indiatimes.com/city/chandigarh/Sec-26-restaurant-charges-excess-service-tax-to-pay-up/articleshow/51131365.cms(last visited on June 30, 2016).

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications