This article has been written by Pruthvi Ramakanta Hegde. In this article, the author covers the difference between general and particular lien with relevant examples. Also, the meaning of each type of lien and judicial approach with regards to it is also discussed.

Table of Contents

Introduction

In any financial transaction, securing the party’s interest is one of the important aspects. It becomes even more important when a loan is advanced and there might be a risk of non-payment. In such circumstances, there are certain remedies available under the law. One of the remedies is the concept of “lien”. The risk of non payment and non performance of the duties can be reduced by this concept.

In the concept of lien, a person or entity has the right to retain possession of another’s property. This right continues until the debt or obligation is fully satisfied. The concept of lien is governed as per the provisions of the Transfer of the Property Act, 1882 (hereinafter referred to as ‘TP Act’) and the Indian Contract Act, 1872. The lien is divided into two types that includes general and particular lien. Both kinds of the lien aim to protect and secure the payment and performance of specific obligations. However, they are different in their scope, application and rights they confer on the creditor.

Before discussing the difference between general lien and particular lien, let’s first understand the meaning of lien.

Meaning of lien

The term lien is not defined under the Indian law. However, we all know that many enactments have discussed the concept of lien. One such enactment is the Indian Contract Act 1872, and the Sale of the Goods Act, 1930. In general terms we can say that a lien means keeping the possession of the property of the person until the loan owed by such person is cleared.

In other words, a lien is a legal claim on property or assets that acts as security for a debt. Accordingly, the person who lent the money, or someone with a legal decision (such as a court-appointed receiver), has a right to hold or take the asset until the debt is repaid.

Main purpose of a lien

One can simply state that the main purpose of a lien is to ensure the loan or obligation is fulfilled.

For instance, when a person takes out a mortgage to buy a house, the bank or lender places a lien on the property. The lender has a legal claim to the house as collateral for the loan. If the borrower fails to repay the mortgage, the lender can enforce the lien by foreclosing on the property and selling it to recover the loan amount.

According to Cambridge Dictionary, lien means holding the property belonging to others until they have fully paid the debt amount which they owe. Generally lien is divided into two types as per the Contract Act. They are general and particular lien. These types of lien are recognised under Section 171 and Section 170 of the Indian Contract Act, 1872 respectively.

Let’s now move forward and discuss the key distinctions between general and particular lien.

Differences between general lien and particular lien

Meaning

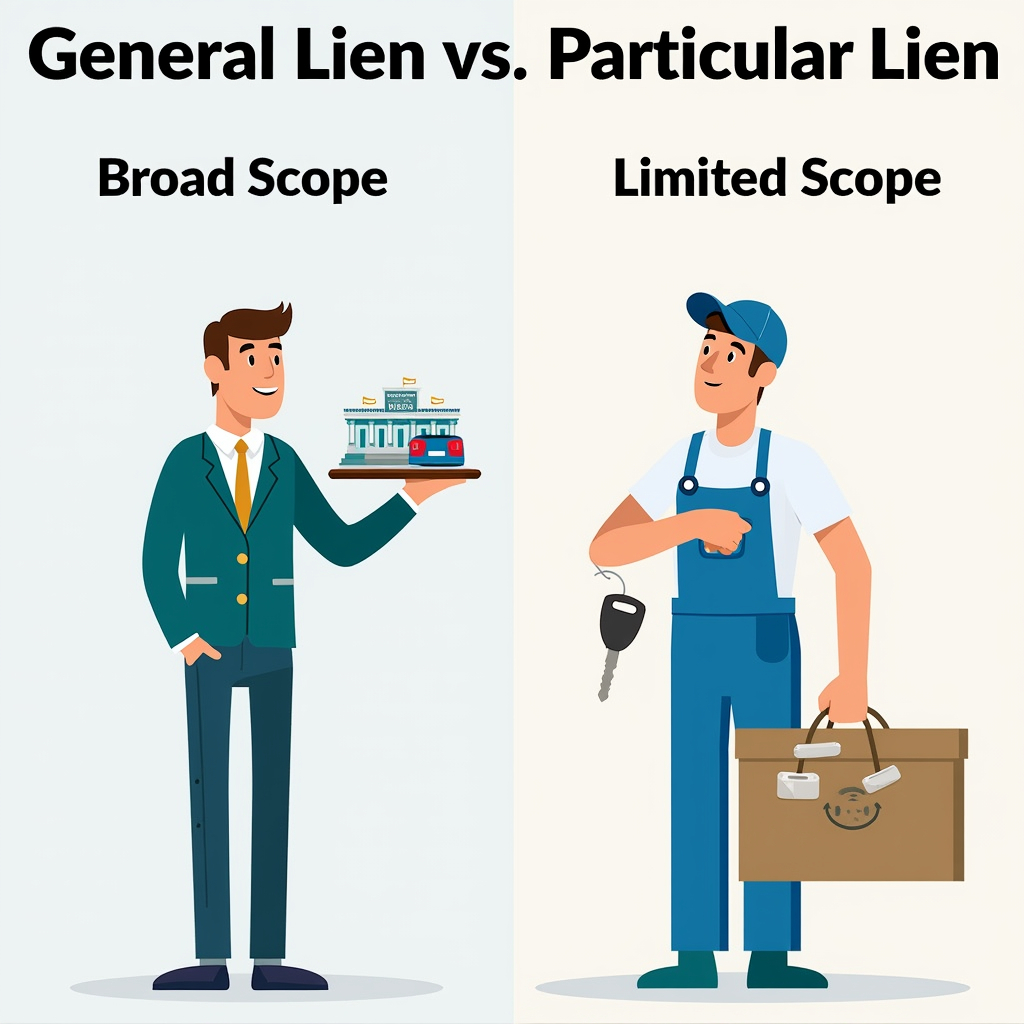

General lien

General lien means a legal right exercised by the certain professionals by retaining the property of the others until a debt or obligation is settled by them. Moreover, in general lien creditors can retain any property in their possession until any outstanding debt owed by the debtor is paid. Unlike a specific property, a general lien is not limited to a specific property.

For example, bankers can exercise this right over the assets of their clients for all outstanding fees. This is not just fees related to a specific item of work.

Particular lien

A particular lien is a legal right that allows a person, usually a creditor, to retain possession of a specific property until a particular debt or obligation related to that property is settled. This type of lien only applies to the specific property for which the debt arose.

For example, if a mechanic repairs a car, they may have a particular lien over the car. It means they can hold onto the car until the repair bill is paid. The lien is limited to the car and it does not extend to other assets of the owner.

Scope

General lien

The scope of a general lien is broad and extensive. It covers all property and assets that belong to the debtor. This includes not only the assets they currently own but also any future assets they may acquire. The creditor has the right to keep the debtor’s property until all the entire debt is repaid. Thereby, this lien gives the creditor a great level of protection.

Particular lien

A particular lien is more limited in scope as compared to a general lien. It applies only to specific property or assets directly related to the debt or service in question. The creditor can retain possession of the specific asset until the payment for the particular service is fulfilled. Unlike a general lien, a particular lien does not cover all of the debtor’s assets. It only covers the specific item or property that is connected to the debt. Particular liens are restricted to specific assets that directly relate to the debt or service.

Examples

General lien

To clarify the idea of a general lien, the following examples can be considered:

- If a customer has an overdraft, the bank may use a general lien on all assets and funds belonging to the customer. This means the bank can hold onto the customer’s assets until the overdraft is completely paid off.

- When a person does not pay their taxes, the government can place a general lien on the taxpayer’s property. The government may then seize and sell these assets to recover the tax debt.

- In certain cases, lenders can acquire a general lien on a business’s assets as security for a loan. This allows the lender to retain possession of the business’s property until the loan is fully repaid.

Particular lien

Here are a few examples that highlight how a particular lien operates:

- If a mechanic repairs a vehicle and the customer fails to pay for the service, the mechanic can place a lien on the vehicle. The mechanic is entitled to hold onto the vehicle until the customer pays for the specific repair work.

- An artisan, such as a jeweller or tailor, can hold onto a customer’s item (e.g. jewellery or clothing) if payment for services or labour provided is not made. This lien only applies to the specific item that was worked on.

- A transporter or shipping company can exercise a lien on goods they have delivered if the customer has not paid the shipping charges. The lien only covers the particular goods that were transported.

Legal recognition

General lien

Section 171 of the Indian Contract Act, 1872 talks about the general lien. However, this Section does not define what is general lien. As per the Section, certain professionals like bankers, factors, wharfingers, attorneys of a High Court, and policy brokers have a special legal right called general lien. If someone gives their property to these professionals for any reason, in such situations these professionals have the right to keep those goods until all the debts are fully paid. This right applies to the total amount the person owes, not just the specific payment related to those goods.

From the above Section it can be understood that a general lien means right to hold onto someone else’s property until a debt or claim is paid. General lien gives certain people the right to hold on to goods until the full payment has been made to them. Such people can keep the properties even if the debt has nothing to do with those properties.

For example, if someone gets a bank loan and gives them their valuables as collateral. The bank can keep their valuables not just until the loan is satisfied but also for any other debts they owe to the bank. It might be like fees or another loan.

Also, a wharfinger, who is a person that stores goods at a port, has the right to keep the stored goods until all dues related to storage and other services are paid.

This right to hold goods is an absolute right for these professionals, unless there is an agreement explicitly stating something different.

M. Mallika vs. State Bank of India & And Anr. (2006)

Facts

In the case of M. Mallika vs. State Bank of India & And Anr. (2006), the appellants took loans and filed complaints against the State Bank of India. They argued that the bank failed to return their title deeds despite the fact that they had cleared the loan amounts. The bank, however, contended that the appellants still had outstanding dues as guarantors for other loans.

Issue

The main issue of this case was whether the bank has the power to keep the title deeds in accordance with the general lien provided under Section 171 of the Contract Act.

Judgement

The National Consumer Disputes Redressal after hearing both parties’ arguments held that the bank is entitled to exercise a general lien over the title deeds. In addition to that, the court also explained that although Section 60 of the TP Act permits a mortgagor to reclaim documents upon full payment. On the other hand, Section 171 of the Indian Contract Act, 1872 permits the bank to retain documents as a security for any unpaid debts.

Krishna Kishore Kar vs. United Commercial Bank And Anr. (1981)

Facts

In the case of Krishna Kishore Kar vs. United Commercial Bank And Anr. (1981), the plaintiff, Krishna Kishore Kar, had deposited a margin money amounting to Rs. 1,83,500 with United Commercial Bank. This deposit was meant to secure various transactions and debts. However, the plaintiff later settled all dues with the other defendant, related to those debts. Despite the settlement, the bank retained the margin money, by claiming a general lien over it.

The lower court ruled that a portion of the margin money was to be refunded to the plaintiff. Nonetheless, the bank continued to assert its right to retain the margin under a general lien.

Issues

- Whether the bank could claim the plaintiff’s margin money under a general lien, even after the plaintiff had settled his dues?

- Whether a general lien could be applied to the margin money deposited by the plaintiff despite an express contract defining its purpose and limitations?

Judgment

The Calcutta High Court held that the bank could not claim the margin money under a general lien. It was observed that while a general lien grants bankers the right to retain a customer’s assets until debts are cleared, it is not applicable in all cases. Specifically, when an express contract is in place that defines the purpose and scope of the deposited funds.

This contract limits the bank’s ability to apply a general lien. In this case, the margin money deposit was governed by an express contract that specified its purpose and restricted the application of the general lien. Therefore, since the plaintiff had already settled the dues related to the margin money, the bank had no legitimate claim over it. The court ordered that the bank must refund the margin money to the plaintiff.

Particular lien

Section 170 of the Indian Contract Act, 1872 does not specifically define the term “particular lien”. However, it describes the concept of a particular lien. Section 170 talks about a situation where a bailee has done work by using his/her labour or skill on the goods. In such situations, the bailee has the right to retain the goods until they are paid for the specific services which they provided with respect to those goods.

From the above Section, one can understand in general that a particular lien means it is the right of a person to retain the possession of the specific goods until payments are made for the services which were provided. This kind of lien applies to the particular goods but does not apply on any general balance of accounts or any other debts.

For instance, in order to cut and polish a rough diamond, ‘A’ gives it to the jeweller and the jeweller does the work. The jeweller can hold on to the diamond until A pays for the services. Here the jeweller’s right is limited to the diamond given only, as the services were provided in relation to that particular diamond.

If A gives cloth to B (tailor), to make a coat from it. But B promises to give A three months’ credit, then B cannot hold on to the coat until payment is made. This is because there was an agreement for credit, the tailor has no right to keep the coat. It can be understood that one can keep up the goods only when there is no explicit agreement between the parties.

Enforcement

General lien

A general lien gives the creditor the right to retain any property in their possession until all debts owed by the debtor are paid. It does not matter whether the property relates to the specific debt or not. In the general lien, the creditor may retain possession of multiple items of property. In this lien, property is not just the one that is related to the particular debt. The general lien applies across all assets in the creditor’s possession until the debtor’s general obligation is paid in full.

For example, a banker may exercise a general lien over all securities or funds held on behalf of a client if the client owes the bank any money.

Particular lien

A particular lien applies only to the specific item of property that is directly related to the debt or obligation. The creditor can retain possession of the specific property until the associated debt is paid. This lien can be enforced when the debtor refuses to pay the debt amount, the lienholder may be able to sell the specific property to recover the debt. But this typically requires following legal procedures or obtaining court approval, depending on the jurisdiction. The lienholder cannot claim any other property of the debtor for unrelated debts.

For example, if a borrower pledges gold to secure a loan, the lender can retain possession of the gold until the debt is cleared.

Advantages

General lien

- Creditors have more protection with a general lien. This is because they can seize any of the debtor’s assets to recover the debt, not just specific items.

- Creditors do not need to prove that the property is directly connected to the debt. They can make it simpler to enforce compared to a particular lien.

- In cases where a debtor has both general and specific liens on their property, the general lien usually takes priority and is settled first.

- General liens are less common than specific liens and the rules about them may change depending on the location.

Particular lien

- The creditor knows exactly which property they can take to settle the debt, as it is tied to a specific asset only.

- Since the creditor does not need to go through all the debtor’s assets, it is quicker to enforce compared to a general lien.

- It is considered more fair because the creditor can only take the property directly connected to the debt. Thus it protects other assets.

- With a particular lien, the debtor’s other assets that are not related to the debt are safe.

- If there are multiple liens on the debtor’s property, a particular lien is usually settled before a general lien.

Disadvantages

General lien

- Creditors may find it challenging to locate and seize specific assets to cover the debt. This is because this lien applies to all of the debtor’s possessions.

- The wide range of assets that can be seized under a general lien. This may leave the debtor with very few resources. Thus it makes it hard for them to cover basic living expenses.

- Creditors may face more time and expense in enforcing a general lien. It becomes time-consuming especially if legal help is needed to identify and seize assets.

Particular lien

- The lien only covers the specific asset or property it is attached to. So it does not protect other debts or assets.

- If the asset is lost or damaged, the creditor may not recover the full amount they owed.

- The asset’s value might decrease over time, which could make it harder for the creditor to collect the full debt amount.

- If the debtor fails to repay, the creditor might not be able to get the full payment owed.

- Taking legal action to seize the property takes a lot of time and money for the creditor.

- When the property is sold, a particular lien holder may not get paid first if other liens take priority.

Judicial pronouncements

General lien

Bank of Bihar vs. State of Bihar & Ors (1971)

Facts

In the case of Bank of Bihar vs. State of Bihar and Ors (1971), the bank is the appellant which provided advances to the Jagdishpur Zamindari Co. Ltd. (defendant no. 2) under a cash credit system. As a way of security, the company pledged the sugar bags to the bank. These sugar bags were stored in warehouses, and banks had the keys to such warehouses.

In 1949, the state of Bihar seized 1,818 bags of sugar from the warehouse. It was done as per an order issued by the Rationing Officer and the District Magistrate Patna. The bank, as a pledgee, held that the sugar as security against its loan to defendant no. 2.

Later sugar was sold, and the sale proceeds were deposited in the government treasury. The Cane Commissioner attached the amount under the Bihar and Orissa Public Demands Recovery Act, 1914 for sugar cess arrears owed by the Bhita Sugar Factory. This factory had a business arrangement with defendant no. 2. The bank sued the State of Bihar and the Jagdishpur Zamindari Co. Ltd., for the purpose of either to return the sugar or compensation for the value of the seized sugar.

Issues

The main issue was whether the bank, as a pledgee, has a right to exercise general lien over the seized sugar or not?

Judgement

Initially the Trial Court decided in the favour of the bank. It stated that the bank’s rights as a pledgee were not taken away by the government while seizing the sugar. The court further ordered the state of Bihar to pay Rs. 93,910 with interest to the bank. However, when the case was appealed, the Patna High Court disagreed with the Trial Court decision. It ruled that the bank had no right to claim the sugar or the money made from its sale. This is because the action by the government by seizing property was lawful. Similarly, such money obtained from selling those seized assets was used to pay off outstanding debts related to the sugar cess.

While on appeal before the Supreme Court it disagreed with the decision of the Patna High Court. The decision of the Supreme Court was in favour of the bank. It said that the bank had the right to exercise the lien by keeping sugar as a security for the loan amount. The government’s seizure did not take away the bank’s right to the sugar. Therefore, the government had to compensate the bank for the value of the seized sugar.

The City Union Bank Limited vs. C. Thangarajan (2003)

Facts

In the case of The City Union Bank Limited vs. C. Thangarajan (2003), the City Union Bank filed a suit in 1986 to recover Rs. 2568.15 from Kumaraswamy, Chellapappa, and Thangarajan. It is based on a promissory note executed for a Rs. 4,000 loan which was taken in 1983. Thangarajan denied borrowing money and stated that he had no dealings with the bank regarding the loan.

Thangarajan, a respected Tamil Pandit, filed a suit against the Bank to recover Rs. 11,053, including interest on a fixed deposit (FD) and damages of Rs. 10,000 for reputational harm. He had deposited Rs. 10,000 in 1985, but when he attempted to withdraw the amount through Vijaya Bank, the City Union Bank dishonoured the request, and claimed a lien over the FD due to Thangarajan’s alleged loan liability.

Issue

The main issues were:

- Whether Thangarajan was liable for the loan along with the other defendants?

- Whether the bank could exercise a general lien on Thangarajan’s FD for recovery of the alleged loan?

- Whether Thangarajan was entitled to damages for reputational harm?

Judgement

The Trial Court found that Thangarajan had signed the promissory note, and that made him liable for the loan. However, the court also ruled that by filing a separate suit for recovery of the loan, the bank had waived its lien over the FD. The court awarded Thangarajan Rs. 13,055 for his FD and Rs. 2,000 as damages for the harm to his reputation. Both the bank and Thangarajan appealed. But the appellate court upheld the Trial Court’s decision, and held that the bank could not exercise a general lien without an express contract or authorisation from Thangarajan.

M.Shanthi vs. Bank of Baroda (2017)

Facts

In the case of M.Shanthi vs. Bank Of Baroda (2017), the petitioner took a loan of Rs. 47 lakhs from the Bank of Baroda in 2013. The petitioner lent property documents as security for those loan amounts. She was regular with payments until 2015, when she faced financial difficulties. Further she was ready to pay the loan amount and she wanted to get her property back. Meanwhile, the bank refused and claimed the right to keep the documents. They further argued that she was also a guarantor for another loan amount which was related to CMS Educational Trust. This trust had a large outstanding amount.

Issue

The issue in this case was whether the bank could legally keep the petitioner’s property documents for a loan she had guaranteed, even though it was not related to her own loan. Further whether the bank could use a general lien to hold the documents after her personal loan was repaid.

Judgment

Orissa High Court observed that as per Section 171 of the Indian Contract Act, 1872 bankers have a right to retain any goods bailed to them as security for a general balance of account. This right of lien applies unless there is an express contract excluding it.

The court held that a bank can only exercise the right of lien on the properties that were been given to it by its own customer. However, the bank does not have the right to keep goods or property that belong to someone else, even if the customer is involved in the transaction.

The lien can only be enforced when the balance due relates to the customer’s own account, not the account of other parties, even if the customer is a guarantor. In cases involving partnerships, banks cannot exercise a lien on the private account of one partner for the debts owed by the partnership. The court ordered the bank to release the outstanding dues to the petitioner along with interest.

In this case, the court ruled that the bank had no legal right to keep the petitioner’s gold ornaments. The bank could not rely on its bye-laws or Section 171 of the Indian Contract Act, 1872 in order to hold onto the gold after the petitioner had fully paid off her loans for which the gold was pledged. The court found that the action taken by the Bank was unfair. Therefore, the court cancelled the notice sent by the Bank. Thus the court ordered them to return the gold ornaments to the petitioner immediately. Both parties were told to bear their own legal costs.

Particular lien

Vijay Kumar vs. Jullundur Body Builders And Others

Facts

In the case of Vijay Kumar vs. Jullundur Body Builders And Others (1981), the petitioner, Vijay Kumar, entered into a business relationship with a bank as a guarantee facilitated through fixed deposit receipts (FDRs). The FDRs were provided to a bank as security for a specific bank guarantee.

The dispute arose when the bank attempted to exercise a general lien over the FDRs. Even though the original guarantee had been discharged, it was done in order to cover an unrelated overdraft account balance.

Issues

Whether the bank has the right to claim a general lien instead of particular lien over the Fixed Deposit Receipts when they were specifically pledged for a particular purpose?

Judgement

The court held that while banks generally possess a lien under Section 171 of the Indian Contract Act, 1872, this right can be overridden by a specific contract between the parties. In this case, the FDRs were pledged for a particular purpose which had already been satisfied.

Thus, the bank could only claim a particular lien over the FDRs and not a general lien for other unrelated debts. Thus, the court held the bank’s claim to use the FDRs for settling the overdraft account was invalid.

Summary of difference between general lien and particular lien

| Parameters | General lien | Particular lien |

| Definition | Under this lien it gives the right to a creditor to keep any goods owned by someone else until they pay a due amount.For example, a bank can exercise this lien to various documents if a customer has unpaid loans. | Under this type of lien the person can keep the specific goods until payment for those goods is received. For example, a tailor makes a custom suit for a customer. The tailor has the right to keep the suit until the customer pays for it. |

| Scope | This applies to all types of goods which are not paid. It does not matter what the debt amount is. A bank can use this right across the different types of loans. | This type of the lien is only applicable to certain items. This lien is confined to those specific goods. This lien is confined to specific goods because it is based on the principle that the lien holder has a legal right to retain possession of particular items in order to secure payment for those items. |

| Automatic vs. agreement | This right is not automatically given; it usually requires a written agreement between the parties. | This right comes automatically as per Indian Contract Act, 1872. Here in this type of lien right automatically comes without any special agreement. |

| Right to sell | The holder of a general lien does not have the right to sell the goods to recover unpaid debts. They can only keep possession of the goods until the debt amount is paid. | In a particular lien, the holder usually cannot sell the goods. But they can sell some rights under special circumstances. |

| Common users | Banks and financial institutions often use this type of lien. Also wharfingers and policy brokers can exercise this lien. These entities can retain possession of specific goods or documents until payment is made for their services. | Service providers, like repair shops or storage companies, often use this lien. Additionally, other parties such as bailees , agents, pledgees, partners, unpaid sellers, and finders of goods also utilise this lien. |

| Debtor claims | This lien allows claims against multiple debtors. For instance, if a business owes money across different loans, the bank can hold their assets. | This lien is limited to only one debtor. It means that the lien only applies to the individual or entity. |

| Enforcement | The holder can sell any of the debtor’s assets to recover the full amount owed, regardless of the specific goods. | The lien can only be enforced by selling the specific items but not the debtor’s other assets. |

| Termination | A general lien remains in effect until all debts owed by the debtor to the lien holder are settled. | A particular lien is terminated once the specific debt related to the particular goods is paid. |

Conclusion

General lien and particular lien are both ways for creditors to protect themselves. General lien lets the creditors hold the debtor’s property until all debts are paid by the debtor though if those debts are not directly connected to the property. The general lien is commonly used by banks. On the other hand, a particular lien only applies to a specific item of property that is linked to a particular debt.

General liens are broad and cover all debts between the parties. In general liens, multiple financial transactions may occur over time. This approach provides security for creditors by retaining assets of the debtors until all amounts owed are cleared by them. However, particular liens on the other hand focus mainly on a single, specific debt. This makes them limited in scope. However, both types of liens are important in their own approach.

Frequently asked question (FAQs)

Can a lien be exercised on the personal property?

Yes, lien can be placed on personal properties such as cars, jewellery, or equipment.

What is the difference between the lien from a mortgage?

In a mortgage, for the loan amount property is used as collateral. A mortgage is also a type of lien. But in a lien, it can apply to various types of property and debts. It is not only confined to mortgages. A mortgage is also a kind of property in which the owner gives someone a legal claim on their property as security for a loan. A lien, on the other hand, is a legal right to hold or claim the property, because of an unpaid debt.

What is the effect of selling the property with a lien?

If a property with a lien is sold by the person, the lien holder’s interest needs to be paid by that person. In other words the lien holder can still claim the property even after the sale.

References

- https://blog.ipleaders.in/critical-analysis-of-the-importance-of-lien-and-its-kinds/#:~:text=A%20 general%20 lien%20is%20a%20right%20to%20create%20the%20 possession

- https://blog.ipleaders.in/right-of-lien/#:~:text=What%20is%20Lien?%20Lien%20in%20its%20primary%20sense%20is%20a

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications