This article has been written by Seerat Kaur, pursuing the Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from LawSikho.

Table of Contents

Introduction

A takeover refers to the acquisition of control over the management of the target company. In layman’s language, the company taking over is the big fish while the target company is the smaller fish. It must be noted that the word ‘takeover’ has not been defined under any act but is a casual routine term for those indulging in this field.

Methods of takeover

Taking over can be done by various methods including the acquisition of shares, holding subsidy route, the debt route, etc. These takeovers can be grouped under two kinds: the friendly takeover and the hostile takeover. While a friendly takeover is an acquisition done by consent and clear intentions, a hostile takeover includes an acquisition where the board of directors do not approve of the transaction. The tender offer, proxy votes, dawn raid, etc. are all strategies to undergo a hostile takeover. An example of the same will help with better understanding:

- Consider that Company X is looking forward to expanding into a new geographical market. So, it approaches Company Y with an offer to purchase it.

- The management including the board of directors of Company B decides that this is not a good idea and thus reject the offer.

- Company X still continues to push for an acquisition. Subsequently, Company X meets the shareholders of Company Y and brainwashes them into voting out the board of directors in the management in order to persuade the replacing board of members to approve the takeover. If the new members agree, then this would be a hostile takeover.

There are also various defence strategies for a hostile takeover. These include:

- Poison pill: Here the target company makes its stocks appear less attractive and profitable by allowing its shareholders to purchase the new shares at a discount. This will lower the equity interest and make the acquirer buy more stocks making the takeover more expensive and repulsive.

- Crown jewels: Disposing of the most valuable assets of the company in order to drive away the acquirer’s interest.

- Golden parachute: An employment contract that guarantees expensive perks and benefits to the board members in order to make them stick with the company and expensive for the acquirer to buy.

- Supermajority amendment: A private amendment in the company’s articles that requires the possession of a larger majority of shares to be eligible to vote in order to approve a merger.

- Greenmail: This refers to when the target company tries to repurchase its shares from the acquirer at a higher premium.

- Pacman: This is when the target company tries to undergo a hostile takeover against the acquirer company as well. It does this in order to scare it away from doing the takeover. The acquiring company may be scared to lose its own shares resulting in it dropping up the takeover.

Takeovers are a rather wide concept. Another model which includes the acquiring of shares from a dissenting shareholder for personal interest is at the company’s managerial level itself.

It is not important that a Company’s management will always have a 100% majority while taking a decision. Several dissents and scuffles arise in this process. In fact, this is also what makes these decisions well discussed and equipped with all the possibilities being considered.

However, a stagnant deadlock is never good during decision making. After all, the process has to be quick, smooth and well organized. The resultant is what is called ‘Drag Along with Rights’. A drag-along right is a provision that gives the majority shareholder the power to force a minority shareholder to join in with his decision. This is different from a ‘tag along right’ which offers the minority shareholder an option to tag along, instead of forcing it on them.

Analysis of Section 235

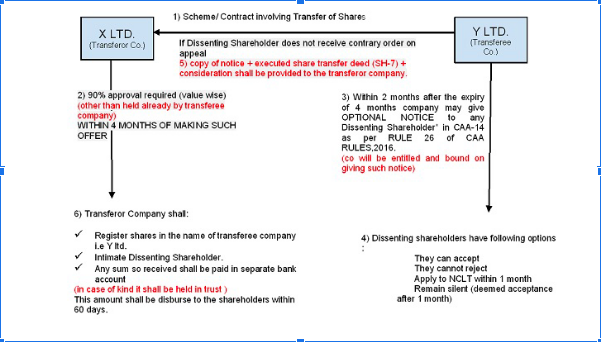

Section 235 of the Companies Act, 2013 provides in the Indian context, a provision to acquire the shares of the dissenting shareholder from the scheme or contract approved by the majority shareholder.

The first clause of this provision explains that in a situation where the scheme or contract involving the transfer of a set number of shares to another company has within 4 months of making that offer, been approved by at least 9/10th of the shareholders, then the acquiring company needs to give a notice (Form CAA 14 Rule 26 of CAA Rules, 2016) to the dissenting shareholders within 2 months after the expired 4 months.

After this notice has been delivered, and the shareholder has failed to send an application to the tribunal within 1 month of receiving that notice, then the acquiring company legally has the right to forcefully acquire the shares of the dissenting shareholder. It shall send a copy of the notice to the target company along with an instrument of transfer which is to be executed on behalf of the dissenting shareholder and also pay the consideration for the same. However, if the tribunal feels that the dissenting shareholder has a right to retain those shares, then further proceedings will take place and the acquiring company will not be allowed to forcefully acquire those shares.

If the tribunal does not find substance in the dissenting shareholder’s pleadings, then it may pronounce its judgement and allow the takeover by the acquiring company. Thereafter, the target company is supposed to:

- Register the acquiring company as the official holder of those shares; and

- Within a month of this registration, inform the dissenting shareholders about the same and the receipt of the consideration which the acquiring company will be paying to them.

It is necessary for the sum paid by the acquiring company to the target company to be held in a separate bank account. Further, this amount needs to be disbursed off to the entitled dissenting shareholders within a period of 60 days.

The fifth clause of this section also brings under attention that this section has a retrospective nature and shall apply to the offers already made before the commencement of this Act.

Complete takeover of unlisted companies

Certain things to keep in mind

Applicability

Section 235 will only be applicable for such individual acquirers or acquiring companies who hold at least 90% of the total shares of the target company or obtain approval by 90% of the shareholders of the target company within a set time period of 4 months from the date of the offer. Only if these conditions are satisfied, the acquiring company can force the dissenting shareholders to sell off their shares without consent.

How is the 90% calculated?

This Section is not for the purpose of take over as that may already be done by becoming the largest shareholder. This section is just one of the two Exit opportunities provided by the Companies Act, 2013. This Exit opportunity focuses on favouring the majority to force the minority to sell their shares.

The other Exit opportunity is that under Section 235(2) which provides for a ‘mandatory notice’ to the minority shareholders.

Thus, the following are not included while calculating the 90% of the shares:

Conclusion

After analysing the provision, it can be said that Section 235 is indeed an exception to the rule that a member cannot be expelled. The court went on to unearth another question that was asked. Is Section 235 unconstitutional? The court clarified that this section is not unconstitutional as the power to acquire the shares of dissenting minority shareholders is not ultra vires the constitution. This was also held in the case of S Viswanathan v. East India Distilleries & Sugar Factories Limited.

So, it is safe to say that this provision has been given by law with a very clear-cut intention to give power to the majority shareholders. As discussed above, it is advantageous in making matters swift and avoiding any stagnant deadlocks between parties. However, the Companies Act 2013 also gives certain protections to the minority shareholders in order to maintain the balance of power. Right to appoint small shareholder directors, right to apply to NCLT for oppression and mismanagement, right to a class action, right to amalgamation and reconstruction, majority of the minority, etc. have been provided.

There is a greater focus on judicial redressal. Their rights can truly be protected only when majority shareholders realise their legal obligations and work together with the minority shareholders during the decision-making process. They should also provide the minority shareholders with adequate opportunities to redress their complaints and grievances at a very basic level. It must be realized that the progress and growth of the company values is the entire management’s righteous endeavour which can only be fulfilled if every shareholder is kept in mind. The minority shareholder’s rights will be actualised only when the rights of the minority stakeholders are upheld in a positive manner.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications