This article is written by Kashish Goel, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from Lawsikho.

Table of Contents

Introduction

The life sciences sector is at an inflection point. To prepare for the future and remain relevant in the ever-evolving business landscape, biopharma and medtech organizations will be looking for new ways to create value and new metrics to make sense of today’s wealth of data. By the year 2024, prescription drug sales worldwide are projected to have a compound annual growth rate of 6.9%, with sales expected to breach trillion-dollar market gap by $180 billon to a staggering $1.18 trillion.

In the September of 2014, MERCK & SIGMA-ALDRICH announced that they have agreed to enter into a binding agreement, under which Merck will be acquiring the later for $17 billion and forming one of the dominant players in the $130 billion global life science industry. Combining the resources, they are serving more 300,000 products with a set of ongoing brands and a supply chain.

About the parties

- MERCK:

Merck is a 350-year-old company founded all the way back in 1668 by Friedrick Jacob Merk making it the oldest pharma and chemical company in the world. Among other milestones, one was when the company was publically listed in 1995. The company was handled last by the Merck family in 2000 when, Professor Dr. Hans Joachim Langmann retired as the chairman of the executive board. As of now the Merck is a globally present brand and has more than 50,000 employees working in 66 countries.

- SIGMA-ALDRICH:

This company is a result of a merger that took place in 1975 between Sigma Chemicals Company and Aldrich Chemical company who were in the business of manufacturing bio chemicals and organic chemicals. By 1979 the company claimed a market share of 30-40% in the $100 million market with sales increasing annually by 15%. By this time the company was operating in 125 countries with subsidiaries Canada, Germany, Japan, UK.

Purpose of the deal

The acquisition was made by the Merck group to creat synergy between the two companies and expanding the customer base of Merck Millipore’s into North American Markets like St. Louis, Billerica, MO and MA to the growing markets of Asia. Due to the merger the customers will be benefit from the broader offerings of products that are complementary and capabilities from the leading players in the Life Science industry. This deal created a leading player in the space of life science industry and help the industry to solve toughest problem in life science.

Financial Advisors:

- Merck Group: Guggenheim Securities and J.P. Morgan

- Sigma-Aldrich: Morgan Stanley & Co. LLC

Legal Advisors:

- Merck Group: Skadden, Arps, Slate, Meagher & Flom LLP

- Sigma-Aldrich: Sidley Austin LLP

Timeline of the deal:

- Announcement of deal: 22nd September, 2014

- Conditions to fulfil after closing the deal:

- Regulatory Filings

- Sigma- Aldrich Shareholder approval at the shareholder meetings

- Fulfilment of the other customary closing transaction

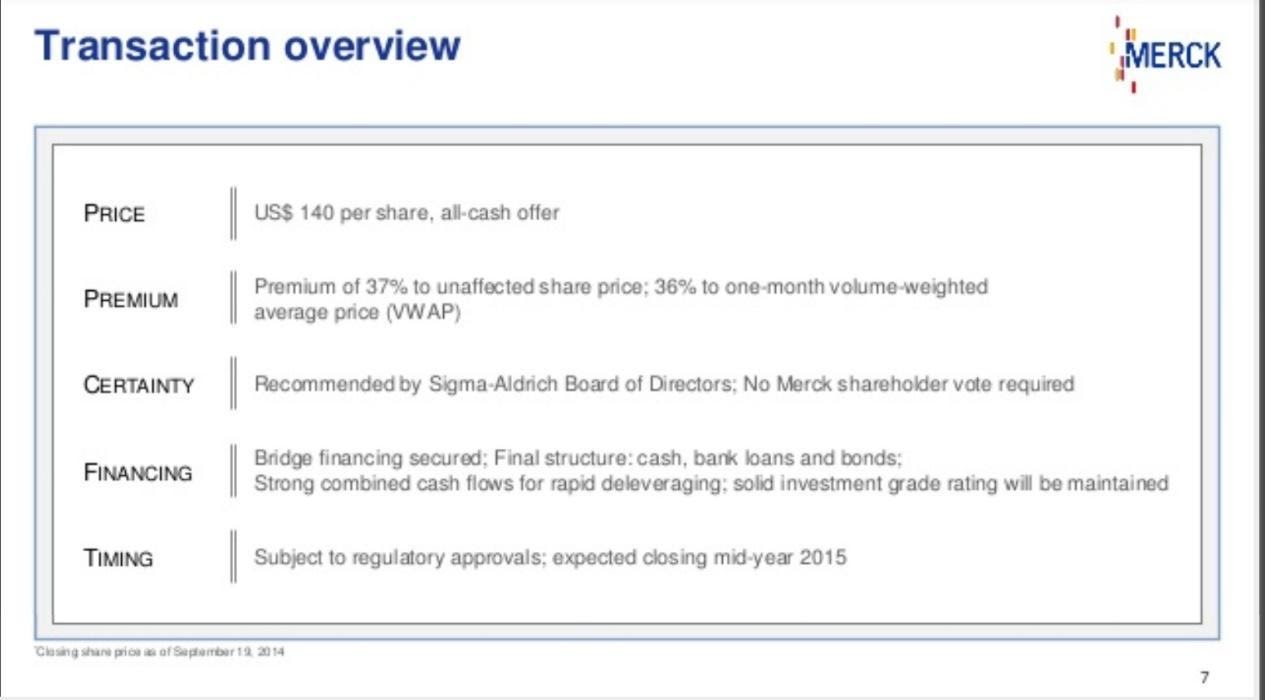

- Expected Closing- Mid-year 2015

- Actual Closing date- 18th November, 2015

According to the then Chairmen of Merck’s Executive Board Karl-Ludwig Kley, “This transaction marks a milestone on our transformation journey aimed at turning our three businesses into sustainable growth platforms”.

Over last 350 years of Merck has integrated many life science businesses with growth potential by combining their strongest operations and processes with owns to provide best support to the consumer and their combined company. Applying the same principle to the Sigma-Aldrich deal is the intention of the executives of the Merck in order to have a seamless integration

One of the condition that the transaction was subjected to the the approval of the shareholders of the Sigma-Aldrich that was done with a whopping 78% as the shareholders were getting a handsome premium of approximately 37% also the acquisition for the group was unanimously been approved by the Board of Sigma-Aldrich in September.

Regulatory approvals

The parties had to get various approvals due to size of the and the financial impact it is going to make in industry economically and financially. As on a press release on 11th August, 2015, Merck notified the world about the progress it has made in order to get the approvals.

Brazil’s Council for Economic Defense (CADE) gave unconditional approval, which was the final outstanding country. This approval becomes effective after a wait period which is common for 15 days. This approval was followed by the antitrust approvals that were given by the competition authorities of Israel (IAA) and South Korea (KFTC).

Securing these approvals in all the relevant jurisdictions brought them close to their bigger goal of transforming the life science industry by increasing the capabilities and better market reach around the world.

As on 10th November 2015, announcement was made by Sigma-Aldrich that they have received the final leg in their regulatory approvals that is from the European Commission (EC). They received their conditional approval in June, that was subjected to the divestments of certain assets from Sigma-Aldrich. In the month of October, some of the assets from the solvents and inorganic business to Honeywell in order to get the approval from EC. This was approved by EC ascertaining all the requirements to get the approval was met.

In reviewing Merck’s acquisition of Sigma, the commission ordered the companies to divest some Sigma assets related to laboratory chemicals. But the companies failed to provide “important” information about certain chemicals related to the commission’s analysis. “Had this project been correctly disclosed to the commission, it would have had to be included in the remedy package,” the commission said.

Merck could be fined up to 1% of its annual worldwide sales depending on the investigation outcome, the commission said.

Merck “has acted in good faith since the antitrust process has begun, and it is committed to a constructive dialogue with the EC,” Merck said in a statement. The company “is confident this issue will be resolved in a satisfactory manner.”

Financing details of the deal

The deal was valued approx. €13 billion an all-cash deal and debt financed. This Financing structure consisted of Mix of bonds, cash and bank loans. Out of the €13 billion, €2 billion was transferred in cash, €4 billion was bank loans and the remaining €7 billion were bonds.

According to the details shared by Merck, based on the financial of the year 2013, combined business would result in the sales north of $6.1 billion, increasing by 79% and EBITDA of $2 billion, an increase of 139%. For the Merck group this would result in the increase in the sale by approximately 19% and improvement of EBITDA by 30% and 33% including expected synergies.

According to the Merger Documents, Merck group will be acquiring all the share outstanding for $140 per share in an all cash deal. $140 represents a significant premium of 37% over the LTP that is $102.37 on 19th September and a 36% premium over the one-month avg. LTP.

Company financials FY 2016

|

€ |

FY 2015 |

FY 2016 |

DELTA |

|

Net Sales |

12,845 |

15,024 |

17% |

|

EBITDA pre Margin (in % of net sales) |

3,630 28.3% |

4,490 29.9% |

23.7 |

|

EPS pre |

4.87 |

6.21 |

27.5%1 |

|

Operating Cash flow |

2,195 |

2,518 |

14.7% |

|

€ |

31.12.2015 |

31.12.2016 |

DELTA |

|

Net Financial Debt |

12,654 |

11,513 |

-9% |

|

Working Capital |

3,438 |

3,486 |

1.4% |

|

Employees |

49,613 |

50,414 |

1.6% |

Commenting on the above data provided by the Merck Group:

- EBITDA margin and pre growth have lead the way for Sigma, organic performance and end of Rebif commission expenses.

- EPS pre additionally supported by Improved financial result.

- Healthy operating cash flow driven by business performance and Sigma.

- Net financial debt reflects string cash generation capabilities and focus on deleveraging.

- Working capital increase due to higher business activity and FX

impact of the deal on the businesses

The deal has a positive impact on the businesses of the both the company strategically, operationally and financially because of:

- Economies of scale- expanding their position in the life science industry

- Increasing the value for the customers:

-

- Broadening the product range and reducing the friction in the business

- Complements process solution product offering

- Closing the market gap that is, expanding in the north American markets

- Using the current research and development and platform so as to perform a global innovation rollout

- It will diversify the revenue stream

- This deal can bring substantial synergy potential and immediately accretive to EPS pre and EBITDA margin for the group

- Investment grade rating will be maintained by the group so as to attract the future potential investors

Conclusion

In my opinion, it was great step by the board of directors of Sigma-Aldrich in order to merge with both group and the decision of both group to accept this merger. This merger not only paid the shareholders of Sigma-Aldrich a very generous premium of 37 % over the market value of the shares but in return whole of North American parts of Asian market open the as a geographical location for the Merck group a 350-year-old chemical company to expand, looking at the financials of the year 2016 comparing it to 2015 we can see nominal growth and are as per the projections during the deal back in 2014. So this merger proved fruitful to all the participants and this includes customer also as they are getting many benefits of the synergy of the two companies by having a wide variety of products of up to 300,000 and at a relatively low prices that can be seen by the financials of the company.

So to sum up this article:

- the deal has given the company’s expanded position in the attractive life science industry that is projected for and sustainable growth.

- Enhancing their value for the customers by strengthening their offerings and reaching and operational excellence all across the board.

- Sigma-Aldrich and Merck Millipore will continue to be the core earning contributors to the Merck group and generates sustainable and growing cash flow.

- this acquisition was in line with the Merck criteria and corporate transformation journey that started in 1668.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications