This article is written by Shreya Ganapathy pursuing a Certificate Course in Advanced Corporate Taxation from LawSikho.

Table of Contents

Introduction

On December 11, 2018, the Board of Directors Reliance Jio Infocomm Limited approved a composite arrangement between Reliance Jio Infocomm Ltd, Jio Digital Fibre Private Limited, and Reliance Jio Infratel Private Limited. The proposed composite scheme of arrangement received the approval of the National Company Law Tribunal. However, The Income Tax Department raised an objection over the approval granted to Reliance Jio Infocomm Limited’s scheme to hive off its fibre and tower business into two separate undertakings. This article attempts to analyse the proposed scheme and its merits as well as to understand the income tax department’s concerns regarding the same. We will also be looking at the rulings of the NCLT & NCLAT regarding the proposed scheme.

Company background

Reliance Jio Infocomm Limited (a wholly-owned subsidiary of Reliance Industries Limited (RIL) is an Indian public limited company registered under the provisions of the Companies Act, 2013. It is headquartered in Mumbai, Maharashtra while its registered office is in Ahmedabad, Gujarat. The following undertakings were a part of Reliance Jio Infocomm Limited:

- Optic fibre cable undertaking,

- Tower infrastructure undertaking,

- Digital services undertaking.

The above-listed undertakings had differentiated strategies, faced different industry risks; and were part of different market dynamics. They had very different growth trajectories. The nature of competition faced by each of these undertakings was different and distinct. Due to this, a composite arrangement scheme was proposed by the company.

A brief overview of the scheme

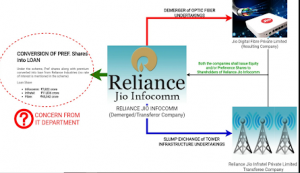

The composite scheme of arrangement presented by Reliance Jio Infocomm Limited (hereinafter referred to as “Demerged/ Transferor Company”), under Sections 230 to 232 read with Section 52 and other applicable provisions of the Act (as defined hereinafter) read with Section 2(19AA) and other applicable provisions of the Income Tax Act, aimed to:

- Demerge (create a separate legal entity to handle a particular part of the business) the optic fibre cable undertaking into Jio Digital Fibre Private Limited (hereinafter referred to as “Resulting Company”) at book value. In lieu of the demerger, the shareholders of the demerged/transferor company would receive equity and/or preference shares of the resulting company on a proportionate basis in the form of consideration.

- Slump sale (transfer as a going concern; lock, stock and barrel) of the tower infrastructure undertaking to Reliance Jio Infratel Private Limited (hereinafter referred to as “Transferee Company”) at book value. The demerged/ transferor company would receive equity and/or preference shares of the transferee company as a consideration for the slump sale.

- Conversion of redeemable preference share capital aggregating to INR 13000,00,00,000, and Securities premium received on the issuance of the said preference shares aggregating to INR 52000,00,00,000 (issued by demerged/ transferor company to its holding company, Reliance Industries Limited for investment in the tower infrastructure and optic fibre cable undertakings) into loans (INR 45342,00,00,000 to refinance the expenditure of the optic fibre cable undertaking, INR 11836,00,00,000 to refinance the expenditure of the tower infrastructure undertaking, and INR 7822,00,00,000 in respect of other businesses).

Proposed benefits of the scheme

The benefits of the proposed composite arrangement scheme were as follows:

- Differentiation of the businesses would lead to enhanced focus on exploiting opportunities in respective businesses.

- Promotion of high-value stand-alone businesses by conversion of cost centric assets into revenue centric assets since the passive infrastructure of the undertakings could be shared with third parties. Services could be provided by these undertakings to third parties as independent entities.

- Providing an opportunity to stakeholders to participate in respective businesses that are specific to their interests instead of a combination of all three businesses.

- Unlocking the true value of the tower infrastructure undertaking and the optic fibre cable undertaking, for shareholders of Reliance Jio Infocomm Ltd.

- Assisting in deleveraging of the balance sheet of Reliance Jio Infocomm Ltd (including reduction of debt, the outflow of interest, and creation of value for shareholders).

The decision of the National Company Law Tribunal

The proposed scheme received the approval of the shareholders and the creditors of the company. A joint petition under Sections 230-232 of the Companies Act, 2013 was moved to seek approval for the composite scheme of arrangement. The demerged/transferor company, resulting company, and transferee company (hereinafter collectively referred to as “Petitioner Companies”) were directed by NCLT, Ahmedabad Bench, to serve a notice to the Regional Director and Income Tax Department for their representations if any. Upon filing such notice, the Regional Director (North Western Region) issued no objection to the scheme. The final hearing was conducted and nobody appeared on behalf of the income tax authorities. The order sanctioning the said scheme was pronounced by the NCLT. This order captured the submissions which were made by the income tax authorities and issued all the necessary directions sought by them.

Concerns raised by the Income Tax Department (supposed disadvantages of the proposed scheme)

The Income Tax Department (hereinafter referred to as the “Department”) challenged the order of NCLT in relation to the third arrangement envisaged through the scheme while suggesting that the matter should not have been adjourned. They contended that while sanctioning the scheme, NCLT did not adjudicate upon the objections raised by them. Aggrieved by the order passed by NCLT, the Department approached the Appellate Tribunal challenging the order of NCLT on the grounds that:

- Petitioner companies wanted to convert the redeemable preference shares into a loan i.e., they wanted to convert share capital into debt. This would not only contradict the well-settled principles of Company law (Section 55 of Companies Act, 2013), but would also result in a reduction of profitability/ or the net total income of the petitioner companies. This in turn would cause a huge loss in revenue to the Department in terms of income tax and dividend distribution tax receivable by the Department.

- Dividend on preference shares is only payable from accumulated profits. But petitioner companies would be liable to pay interest on such loans to their creditors (which wouldn’t have been payable to them if they were shareholders) whether there are accumulated profits or not.

- The proposed scheme failed to identify the interest payable on the loan which would be a charge on the profits of the company. Assuming an interest rate of 10%, the total interest payable would be around INR 780 crore per annum. This would reduce the tax liability by INR 258.16 crores per annum. Such interest payment would lead to the artificial reduction of the total income of the petitioner companies which is not permissible under law and demonstrates a clear case of tax evasion.

- Such conversion of the share capital into debt would result in shareholders becoming creditors. In the capacity of creditors, they can seek repayment of loans given by them irrespective of the profitability of the petitioner companies.

- This scheme was a means for the petitioner companies to achieve what they couldn’t accomplish directly under the law; the scheme would lead to an indirect release of assets by the demerged/transferor company to its shareholders. This would not attract dividend distribution tax, which would have been applicable otherwise under the provisions of Section 2(22)(a) of the Income Tax Act, 1961 which deals with the distribution of assets deemed as dividends.

- Section 2 (19AA) of the Income Tax Act, 1961 requires transfer of the undertaking on a going concern basis. This was not evident from the financial statements of the demerged/transferor company. Since the said scheme did not fulfil the requirement of Section 2 (19AA) of the Income Tax Act, 1961 which defines the term demerger, therefore it could only be considered as a ‘purported demerger’ which doesn’t fulfil the requirements of law.

The Department claimed that the proposed composite scheme of arrangement was a tool disguised as a permissible method of tax planning but was simply a means to avoid and evade the payment of taxes.

Issue under consideration

Whether the proposed scheme was indeed a means to avoid and evade taxes and should have been sanctioned as such by the NCLT?

The decision of the National Company Law Appellate Tribunal

Vide its Order dated 20 December 2019, the NCLAT held that:

- Without placing any evidence on record or substantiating the allegation by appearing before the NCLT, it was incorrect of the Department to hold that the Scheme was designed to give undue advantage to its creditors (erstwhile shareholders) and that the overall intention of the Scheme is tax avoidance or tax evasion.

- The Scheme could ultimately result in some form of tax benefit (tax savings or tax avoidance). However, it is inappropriate to state that the sole object of the scheme is Tax avoidance, or that the intention of the Scheme is to defraud the Department. The mere fact that the Scheme may result in a reduction of tax liability doesn’t constitute a reason for challenging the validity of the Scheme.

- As per various rulings, particularly the decision of the Hon’ble Supreme Court in the case of Miheer H Mafatlal v. Mafatlal Industries Limited, since the equity shareholders, secured and unsecured creditors, and the Regional Director had accorded their approval to the scheme as well as the perusal submitted by the Department, there seemed to be no obstruction for sanctioning the Scheme.

- While sanctioning the Scheme, NCLT has permitted the Department to enquire whether any part of the Scheme violates the provisions of the Income Tax Act, 1961, and to check if any part of the Scheme results in tax avoidance or not. If yes, the NCLT order also gives the Department the liberty to take appropriate action as per the provisions of the Income Tax Act, 1961 during the course of the assessment. The NCLAT pointed out that the petitioner companies have agreed to abide by the principles of law and assist the Department during such assessment. The right of the Department to recover any dues as per the provisions of law remains protected irrespective of the sanction of the Scheme.

- The NCLAT assured the Department that the enforcement of the Scheme would not infringe the rights of the Department to take measures accorded by law to recover any existing liability of the demerged/transferor company. While referring to the ruling of the Hon’ble Gujarat High Court in the case of Vodafone Essar Gujarat Limited v. Department of Income Tax, NCLAT held that:

- Irrespective of the sanction of the scheme, the Department’s right to recover dues in accordance with laws remains protected. The Department is free to take appropriate recourse for recovering any previous or existing liability of any of the petitioner companies. Therefore, the right of the Department to undertake necessary proceedings to recover any tax from petitioner companies remains intact.

- Any pending proceeding against the demerged/transferor company would not be affected due to sanctions given to the Scheme. Therefore, pending cases before the tribunal will not be affected in view of the sanction of the scheme.

This ruling of the Gujarat High Court was further affirmed by the Apex court when it refused to entertain special leave petitions and stated that the Department is free to undertake appropriate proceedings for recovery of tax which is statutorily due from any company.

Since the case in question was fully covered by the decision of the Hon’ble Supreme Court and in view of the fact that the liberty of the Department to undertake necessary actions to ensure petitioner companies compliance with law remained intact, NCLAT therefore, refused to overrule the decision of NCLT.

Further course of action by the department

As per the laws prevailing at present, an appeal against the order of the NCLAT lies before the Hon’ble Supreme Court. However, the Department is not in favour of challenging the verdict of the NCLAT. As per the Chairman of CBDT, the government is looking to reduce tax litigations. The new direct tax dispute resolution scheme “Vivad se Vishwas” has been rolled out with an intention to reduce tax litigation. To achieve this, monetary limits for filing appeals have been raised. Further, numerous circulars have been issued wherein certain judicial decisions have been examined and the Department has decided that those issues will not be contested any further, nor will any further additions to those cases will be made. The Department is also considering the withdrawal of certain cases that have been filed by them. Nevertheless, it has invited an opinion from the Ministry of Law with regards to appeal against the order of NCLAT before the Supreme Court. The opinion from the Ministry is still awaited.

Conclusion

It is obvious that Reliance Industries Limited has spent immense resources in becoming India’s leading Digital platform Company. Entering a completely different league from their existing Oil to Chemical (O2C) Company was never easy and yet, using a bolt-on acquisition strategy, they managed to pave their way into offering a complete digital solution for their customers. The whole exercise of restructuring was done so well that it will naturally result in high-value creation for all stakeholders by leveraging the RIL balance sheet and innovative tax-efficient structures.

NCLAT’s ruling on this matter will prove extremely beneficial in future corporate restructuring processes. The order passed by NCLAT will henceforth be a precedent. We conclude that conversion of preference shares and securities premium collected thereon into a loan is legally permissible during a corporate restructuring process. For a scheme to be rejected on the grounds that it has been designed with an intent to evade taxes, the Department will have to substantiate its claim with proper evidence on record. Generally, while sanctioning a scheme, NCLT grants the Department the liberty to examine the matter in detail and take appropriate actions as per the provisions of law, but there have been instances in the past where some benches of NCLT have rejected similar schemes on the basis of similar objections raised by the Department. It’ll be interesting to watch how the benches of NCLT and the Income Tax Authorities will approach similar schemes to post this remarkable ruling by NCLAT.

References

- Composite-Scheme-of-Arrangement,-as-amended.aspx (ril.com)

- Sanction of Reliance Jio – Demerger and Slum Sale by NCLAT | M&A Critique (mergersindia.com)

- National Company Law Appellate Tribunal (NCLAT)

- Indian Kanoon – Search engine for Indian Law

- Tax dept not in favour of appealing against NCLAT verdict on Reliance Jio (livemint.com)

- Tax Laws & Rules > Acts > Income-tax Act, 1961 (incometaxindia.gov.in)

- Companies Act, 2013 (mca.gov.in)

Students of LawSikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications