Kashish Khattar is a 4th-year student at Amity Law School, Delhi. This article is a discussion revolving around the banking fraud that is plaguing the banking sector and attempts to give out solutions for the same.

Introduction

“The banks are the lifelines of the economy and play a catalytic role in activating and sustaining economic growth, especially, in developing countries and India is no exception.”

- SS Mundra, Deputy Governor of the RBI

Fraud is a real operational risk for the banking system. The Reserve Bank of India (“RBI”) has defined ‘Fraud’ as “A deliberate act of omission or commission by any person, carried out in the course of a banking transaction or in the books of accounts maintained manually or under computer system in banks, resulting into wrongful gain to any person for a temporary period or otherwise, with or without any monetary loss to the bank.”

The latest Financial Stability Report by RBI (here) in June 2018 suggest that the banking system has reported around 6,500 instances involving fraud of around Rs 30, 000 crores in the last fiscal. Several other banking frauds which were reported subsequently have raised several questions about the ability of the PSBs to contain these situations.

Challenges in the Banking System

Banks are known to be the backbones of the economy. It is imperative to keep the banking industry healthy. The following are some of the factors that are challenging the banking sector in the recent years:

- Non Performing Assets – The biggest risk that can be assessed are the rise in bad loans. Bad loans are loans which are not repaid back by the borrower. Hence, they are a total loss for the bank. India’s public-sector banks control about 70% of all the banking assets in the country and they account for the highest exposure to bad loans amounting to USD 150 billion. Banks should focus on the cleaning up of their loan portfolio.

- Advanced Technology – The banks are subject to a lot of pressure due to the advancement of the technology. The upcoming customers, i.e. the youth of the country prefers e-banking and acceptance of technologies such as blockchain has become the norm. Timely technological up gradation of the various features has become a necessity. The privacy and safety concerns regarding the e-banking aspect also have to be looked into.

- Reduced Profits – The banking sector has shown a slowdown in the balance sheet growth in the recent time. Further, PSBs who account for 72% of the total banking sector assets, only come close to 42% share in overall profits.

- Corruption & Balance Sheet management – Various scandals revolving around the banking sector are well known and have only reduced the investor confidence in the management of the company which in turn affects the confidence of the general public towards their banking system. Most of the banks in recent times have tried to delay keeping aside money as provisions for the future NPAs. This is due to the fact that the C-level executives have a short tenure, during the time they want to increase the investor confidence through posting higher net profits. Deferring provisions like these do hurt the banks in the long term. It basically reduces the ability of the bank to withstand financial pressures.

- Crisis in Management – Many PSBs are witnessing their employees retiring recently. Younger employees will now replace the elder, more experienced employees of the bank. This typically happens, at junior levels. As a result of this, there can be a virtual vacuum at the middle and senior levels. The absence of middle management in the banking company can lead to an adverse impact on the banks’ decision-making process.

Click here

Looking for the possible solutions

Let us talk about the various steps taken by the Government to prevent frauds, also listing out some other viable solutions to solve the problem of NPAs:

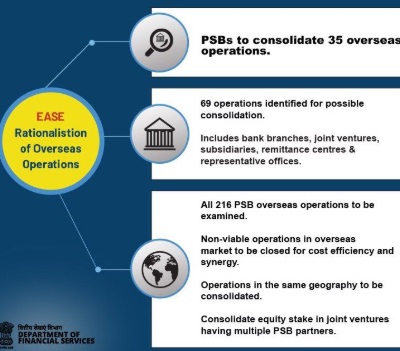

- PSBs have been asked to rationalize overseas operations: The state-owned banks have been instructed to rationalise overseas operations by consolidating non-viable branches which is part of the big plan to a clean and responsive banking system in the country. The consolidation operations include all bank branches, remittance centres and representative offices. It is instructed that this these steps should be taken without affecting the international presence of the PSBs in the respective markets. This is as per the banking sector agenda approved by the PSB Manthan in November 2017, which states that all PSBs will examine the 216 overseas operations they are involved in.

- Parliament passing the Fugitive Economic Offenders Bill into law to help solve the NPA problem of the banking system: The Fugitive Economic Offenders Act, 2018 came into force on 21st April 2018. There have been various laws that deal with economic offenders leaving the country to escape criminal proceedings, it was felt that the existing civil and criminal provisions in the law were not enough to deal with the existing problems in the system. This legislation was mainly passed to bring about a comprehensive new framework to deal with such a problem. On reading the preamble of the Act, it can be asserted that the Act’s main objective is to punish the ‘fugitive economic offenders’ to face the law and it is done through attachment and consequent disposal of property.

- Establishment of the National Financial Reporting Authority (“NFRA”) as an independent regulator for the auditing profession. It has come as a suggestion by the Supreme Court to bring about an independent regulator for the auditing profession. The idea is inspired by the Sarbanes Oxley Act of the United States. It will unburden the load of the the Institute of Chartered Accountants of India (“ICAI”) in terms of keeping an eye on erring chartered accountants. The NFRA will jurisdiction over large and listed companies while the ICAI will be able to exercise its powers over small companies. Section 132 of the Companies Act, 2013 empowers the Centre to set up such an authority. It has jurisdiction over both listed and large unlisted public companies. The NFRA can do the following:

(i) Recommend to the Centre, formulation of various accounting and auditing standards and policies that should be adopted by the companies and auditors;

(ii) Monitor, enforce such standards and policies; and

(iii) Oversee the quality of services of the professions that are associated with the compliance of these standards and policies.

NFRA has been specifically given powers to investigate cases of professional misconduct by CA or CA firms. It can impose a penalty and debar any such entity up to a period of 10 years. The government has stated that the creation of such an authority will improve upon foreign and domestic investments, enhance economic growth, meet international business standards and will ultimately help the government bring in some smoothness in the auditing profession, who has been called as the most important watchdog for economic frauds in the economy.

- YH Malegam Committee was constituted by RBI to look into the rising instances of fraud: RBI constituted this specific committee to look into the whole matter of bad loans, including matters of the effectiveness of audits, classification of bad loans and the rising number of incidents of fraud cases. It is to be headed by YH Malegam, who is a former member of the Central Board of Directors of the RBI. This committee was mainly set up in the wake of Rs. 11,400 Cr SWIFT (Society for Worldwide Interbank Financial Telecommunication) related fraud in Punjab National Bank. Basically, the committee is expected to look into the reasons of the high divergence which is observed in the asset classification and provisioning done by the banks with the help of RBI’s supervision. It will suggest steps which can be taken to prevent incidents like these, identify factors that are leading to the increase in the incidence of cases of frauds in banks and try to give out measures needed to curb these problems. It is also expected to look into the role and effectiveness of the various types of audits that will be conducted in various which will identify, mitigate the incidence of such frauds.

- Project Sashakt: A project which looks to recover from the banking problem plaguing the system. Piyush Goyal, the Union Finance Minister at the time approved Sunil Mehta’s (Punjab National Bank Chairman) suggestions of a 5 pronged strategy to tackle the NPA problem of the PSBs. Project Sashakt is the title of the draft report submitted by Mr Mehta. It was mainly set up to look into the faster resolution of stressed assets. The project typically sets out a plan for the resolution of a bad loan depending on its size. They are listed as follows:

(i) Bad loans which amount to Rs. 50 Cr will be managed by a dedicated vertical or a Steering Committee which is to be set up by the bank itself, which has to ensure that the resolution takes place in 90 days;

(ii) The range from Rs. 50 – 500 Cr, the banks will need to enter into an inter-creditor agreement which authorizes the lead bank to implement a resolution plan within 180 days, including the appointment of turnaround specialists. This is known as the Bank Led Resolution Approach. Under the inter-creditor loan agreement, the lead lender (having the highest exposure) will be authorised to formulate the resolution plan for the turn around of assets which will be presented to lenders for their approvals. If the lead bank is not able to complete the process in 180 days, the asset will then be referred to the National Company Law Tribunal (“NCLT”);

(iii) For the loans above Rs. 500 Cr, they will be dealt with via an AMC/AIF-led process. The panel has proposed the creation of a National Asset Management Company (“AMC”) to take over such NPAs from banks. The main idea is the setting up of an independent AMC supported by institutional funding in stressed assets or AIF. The idea behind AMCs is to help consolidate the stressed assets under the AMC model for better and faster decision making. There can be an option of more than one AMC, which completely the market backed up by private equity. No capital is needed by the government in this process, investors are welcome to invest. It is an open and transparent process; and

(iv) A new role for NCLT – Biggers loans which cannot be resolved through any of these strategies will be transferred to the NCLT for resolution under the Insolvency & Bankruptcy Code (“IBC”).

Conclusion

The gross NPA ratio of scheduled commercial banks could rise to 12.2 per cent by March 2019 from 11.6 per cent in March 2018, as stated by the RBI. Without a doubt, a technologically advanced system which is transparent and highly efficient can lead to a financially healthier banking system of the country. In my opinion, to achieve the goal of a faster yet inclusive growth, in the banking sector, the government and the banking sector should undertake a comprehensive relook into the existing policies and structures. They should be open to more ideas that have been implemented around the world. Only the time will tell as to how the government and the banking industry sector get together the current NPA problem plaguing the loan portfolios of various banks.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications