This article has been written by Anubhav Garg, who is pursuing BBA LL.B. from Delhi Metropolitan Education. In this article, he has discussed how to lodge a complaint to the Banking Ombudsman, what are the grounds of complaint, grounds of rejection of complaint along with all the important documents list and other important intel.

Table of Contents

Who is a Banking Ombudsman?

Banking Ombudsman is appointed by the Reserve Bank of India. As defined in Clause 3(Definition clause), The Chief General Manager or General Manager of the RBI are appointed as Banking Ombudsman for the fulfilment of the duties entrusted to the said designation under The Banking Ombudsman Scheme, 2006.

The maximum tenure of a Banking Ombudsman can’t exceed three years as per Clause 4 of the Banking Ombudsman Scheme, 2006.

Powers, Jurisdiction and Duties of Ombudsman

The powers, jurisdiction, and duties of Banking Ombudsman have been laid down in Clause 7 of the Banking Ombudsman Scheme, 2006. The duties defined in the scheme are as follows: –

-

Receiving Complaints

The Banking Ombudsman receives and considers complaints pertaining to the deficiencies in banking or other services filed on certain grounds like non-payment or inordinate delay in the payment or collection of bills, cheques, and drafts. These complaints are admitted regardless of the pecuniary value of the deficiency in service complained.

-

Settlement by Agreement:

Banking Ombudsman also facilitates the satisfaction of the complaints filed and endeavors to settle the quarrel by an agreement between the bank and the complainant by way of conciliation and mediation. If the bank or the complainant fails to agree on the same terms and conditions then the complaint is resolved by adjudicating the matter and awarding the damages per the provisions of the scheme.

-

Command over office

The Banking Ombudsman also exercises general powers of superintendence and has full command over his office and he is also in charge of the conduct of business thereat.

-

Furnishing Annual Budget

The Banking Ombudsman is also responsible for preparing up a yearly budget for his office in consultation with the Reserve Bank of India and he has the authority to exercise the powers of expenditure in accordance with the budget approved under the provisions of the Reserve Bank of India Expenditure Rules, 2005.

-

Review Report

The Banking Ombudsman has the duty to send the Governor of the Reserve Bank, an annual report, as on 30th June of consistently, containing a general review of the of his Office’s activities during the previous financial year and shall also provide such other information which the Reserve Bank may direct him to. If reserve bank deems fit, it can publish the reviews, reports and other documents received by Banking Ombudsman in public interest in such consolidated form or otherwise as it deems fit.

What can be the grounds of complaint?

There are certain grounds on which a complaint can be lodged to a Banking Ombudsman laid down in Clause 8 of the scheme. These grounds are: –

-

Collection of Instruments

Non-payment or unnecessary deferral in the payment or collection of cheques, drafts, bills, etc;

-

Rejection of Deposit

Rejection without adequate reason, of coins or small-denomination notes offered for any purpose, and for charging of commission in regards thereof;

-

Remittances

Non-payment or delay in payment of inward remittances;

-

Instruments Issuance

Failure to issue or delay in issue of drafts, pay orders or bankers’ cheques;

-

Working Hours

Violation of RBI’s prescribed working hours guidelines;

-

Banking Facility Default

Failure to provide or delay in providing a banking facility (except advances and loans) promised by a bank or its immediate selling agents in writing;

-

Monies’ Proceeding Default

Defer, non-transfer of proceeds in parties’ accounts, non-payment of deposit or non-adherence of the Reserve Bank directives, if any, applicable to rate of interest on deposits in any savings, current or other account maintained with the bank;

-

Foreign Remittance

Complaints pertaining to remittances from abroad, deposits and other bank- related matters by Non-Resident Indians having accounts in India;

-

Opening or Closing of Account

Refusal to open deposit accounts without any sufficient reason for denial or forced the closure of deposit accounts without due notice or without satisfactory reason(s) or refusal to close or late closing of the account.

-

Unjustified Charges

The imposition of charges without sufficient prior notice to the customers are also the grounds to file a complaint to ombudsman;

-

ATM and Debit Card Default

Non-adherence of Reserve Bank’s instruction pertaining to ATM /Debit Card and Prepaid Card operations in India by the bank or its subsidiaries on any of the following: –

- Account debited but cash not dispensed by ATMs

- Account debited more than one time for a single withdrawal from ATMs or POS transaction

- Less/Excess amount of cash dispensed by ATMs that what was being entered

- Balance debited in the account without the use of the card or details of the card

- Use of stolen cards or cloned cards

- Others

-

Credit Card’s Default

Non-adherence by the bank or bank’s subsidiaries to the instructions of the Reserve Bank on credit card operations pertaining to any of the following:

- Unsolicited calls for Add-on Cards, insurance for cards, etc.

- Charging of yearly fees on Cards issued on the term of free for lifetime

- Wrong debits or wrong billing of your credit card

- Threatening calls or inappropriate approach of recovery by recovery agents including non-observance/violation of the Reserve Bank’s guidelines on engagement of recovery agents

- Reporting of wrong credit information to Credit Information Bureau

- Delay or failure to review and correct the credit status on account of wrongly reported credit information to the Credit Information Bureau.

- Others.

-

Online Banking Default

Non-adherence to the Reserve Bank’s guidelines pertaining to Mobile Banking, Electronic Banking service in India by the bank on any of the things given below:

- delay or failure to proceed online payment or fund Transfer,

- unauthorized or fraudulent electronic payment / Fund Transfer.

-

Pension

Non-disbursement or late disbursement of pension (to the extent the complaint can be ascribed to the activity with respect to the bank concerned, but not with respect to its employees);

-

Accepting of Payment

Denial to accept or late acceptance of payments with regard to taxes, as required by Reserve Bank/Government;

-

Government Securities

Denial in issuing or late issuance, or failure to service or late servicing or redemption of Government securities;

-

Unfair Practise

Non-adherence of the fair operation practices code as adopted by the bank or of the provisions of the Bank’s Code of commitment towards Customers issued by Banking Codes and Standards Board of India and as the same adopted by the bank or any matter relating to the non-adherence of the directives issued by the Reserve Bank in relation relating to banking or other services;

-

Para-Banking Activities

Non-adherence of the Reserve Bank’s guidelines on para-banking activities like sale of mutual fund/ insurance /or banks’s other third party investment products pertaining to the following:

- Ingenuine, unsuitable sale of third-party financial products,

- non-transparency/ absence of proper transparency in the sale,

- Concealment or Non-divulgence, of complaint redressal mechanism of the bank,

- Denial or late in facilitating after-sales service by banks.

Click Here

Click Here-

Grievances Pertaining to Loans

A grievance relating to any one of the following grounds accusing deficiencies in banking service pertaining to loans and advances can be filed to the Banking Ombudsman with jurisdiction:

- Violation of the Reserve Bank’s guidelines on interest rates;

- Late sanction, disbursement or non-adherence of the prescribed time schedule for disposal of loan applications;

- Rejection of an application for loans without providing sufficient reasons to the applicant; and

- Violation of the provisions of the fair practices code for lenders as adopted by the bank or Bank’s Code of Commitment to Customers, as the case may be;

- Violation of Reserve Bank’s directives by the bank on the engagement of recovery agents; and

- Violation of any such direction or instruction of the Reserve Bank specified by the Reserve Bank from time to time.

What is the procedure to lodge a complaint?

Step 1, Reporting to Bank

When you have any grievance from a bank, don’t straight file a complaint to the Banking Ombudsman, it is not maintainable. First Report the complaint to the bank. You can approach the Banking Ombudsman only if the bank has rejected your complaint or you don’t receive any reply from the bank within a period of one month from the date bank received your complaint, or if you are not satisfied with the reply given by the bank;

Step 2, Ascertaining Jurisdiction

A person having any grievance against a bank on any one or more of the grounds as discussed above can either himself or through his authorized representative (except an advocate), can make a complaint to the Banking Ombudsman within whose jurisdiction the branch or office of the bank against whom the complaint has been filed is located.

Jurisdiction for Credit Card Grievances: A complaint pertaining to the operations of credit cards and other types of services with centralized operations, shall be filed before the Banking Ombudsman within whose territorial jurisdiction the billing address of the complainant is located. Here is the link for Address and Areas of operation of all the Banking Ombudsmans in India.

Step 3, Complaint Drafting

1.Complaint’s Format

The written complaint shall be duly signed by the complainant or his authorized representative. The format for the complaint is pre-specified in the scheme. Here is the link to the Complaint Form. Prefer to draft the complaint in this format or only with the slight modifications as the circumstances admit, clearly stating:

- The name and the address of the complainant,

- The name and address of the branch or office of the bank against which the complaint has been filed,

- All the requisite facts pertaining to the rise of the issue,

- The extent and nature of the loss suffered by the complainant due to the bank’s default, and

- The relief sought for.

Once you have drafted the complaint according to the above instructions, by simply posting to the complaint to the Banking Ombudsman within who has jurisdiction over your matter or you can simply email the complaint to the Banking Ombudsman. The details of all the Banking Ombudsmen of various areas, along with their mailing address, email address and contact no. is given in this link. You can also file a complaint online on this link.

2. Maintainability of complaint

The complainant has to ensure that the complaint is accompanied by the copies of the documents, if any, which he will count upon and annex declaration that the complaint is maintainable on one or more of the following grounds as laid down in Clause 3 of the Banking Ombudsman Scheme: –

(a) before knocking the door of Banking Ombudsman, the complainant has made a complaint to the bank and the bank didn’t reply within one month, rejected or didn’t give a satisfactory reply to the aggrieved person (step one has been followed).

(b) the complaint has not been made in regards to the same cause of action which was already settled or dealt with on merits by the Banking Ombudsman in any previous proceedings whether or not received from the same complainant or along with one or more complainants or one or more of the parties concerned with the cause of action ;

(c) the same complaint shall not be pending before any other court, tribunal or arbitrator or any other forum is pending or an award or decree or order has already been passed by any such tribunal, court, forum or arbitrator;

(d) the grievance shall not be vexatious or frivolous in nature; and

(e) the complaint has to be filed within the expiry of the stipulated time period of limitation as prescribed under the Indian Limitation Act, 1963 for such claims.

Step 4.1, Settlement by Agreement

As we have already mentioned previously, Banking Ombudsman also facilitates the satisfaction of the complaints filed and endeavors to settle the quarrel by an agreement between the bank and the complainant by way of conciliation and mediation. The procedure of the settlement by the agreement is as follows: –

- Notice to Nodal’s Officer: When the Banking Ombudsman receives the complaint, he sends a copy of the same to the branch or office of the bank against whom the complaint has been filed, to the Nodal Officer(representative of Bank), and endeavour to settle the whole quarrel by an agreement between the bank and the complainant through conciliation or mediation.

- Applicable Rules and Opportunity to the complainant: For settling the matter with the agreement, Banking Ombudsman has no obligation to adhere to the rules of evidence. But Banking Ombudsman does have the obligation to grant an opportunity to the aggrieved party to furnish his/her submissions in writing along with documentary evidence within a stipulated period of time after the written submissions by the bank.

Further, if the Banking Ombudsman has the opinion that the documentary evidence annexed and written submissions by each of the parties are not enough to reach the decision, he calls for a meeting of the complainant and the bank or the concerned subsidiary together to promote a friendly resolution.

If such a meeting takes place and a mutually acceptable resolution of the grievance is fetched out of it, the proceedings of such meeting is documented and signed by each of the party stating that they have agreed to the resolution. Thereafter, the Banking Ombudsman then passes an order recording down the particulars of settlement and annex the terms of the settlement.

- Situations in which matter is considered settled: The Banking Ombudsman has the power to consider the grievance as settled, in any of the accompanying conditions:-

3.1 Issue settled by Bank itself: Where the complaint raised by the complainant has been settled by the bank or by its concerned subsidiary with the mediation of the Banking Ombudsman; or

3.2 Complainant Settles the case: The complainant concurs, either in writing or otherwise, to the manner and extent of the resolution of the complaint provided by Banking Ombudsman depending on the conciliation and mediation efforts; or

3.3 Not Bank’s Fault: If Banking Ombudsman is of the opinion, the bank has clung to the banking standards and practices in effect for the time being and the complainant has been informed to this effect by way of appropriate methods and no objection, if any, has been received by complainant for the same by the Banking Ombudsman within the stipulated time period.

Step 4.2, Rewards imparted by Banking Ombudsman

What if the complaint is not settled by agreement?

If Banking Ombudsman is unable to settle the quarrel by the means of agreement within a period of one month from the receiving date of the complaint or for such further time period as the Banking Ombudsman grants the parties, he after giving the parties a reasonable chance to present their case, grants an Award or turn-down the complaint.

What are the factors for determining the Award?

For imparting an award, the Banking Ombudsman considers the evidence presented before him by each of the parties, the principles of banking law, lawful practices, Reserve Bank’s instructions, guidelines and directions from time-to-time and all the other factors which he thinks are relevant to the complaint.

What does an Award consist of?

The Banking Ombudsman do mention the reasons and the factors which guided him to grant that particular Award. In an award, Ombudsman mentions the amount, if any, to be paid by the bank to the complainant as compensation for the loss suffered him, arising directly because of the bank’s acts or omissions. In addition to that, the Award also contains the direction(s), if any, for the bank, for specific performance of its duties.

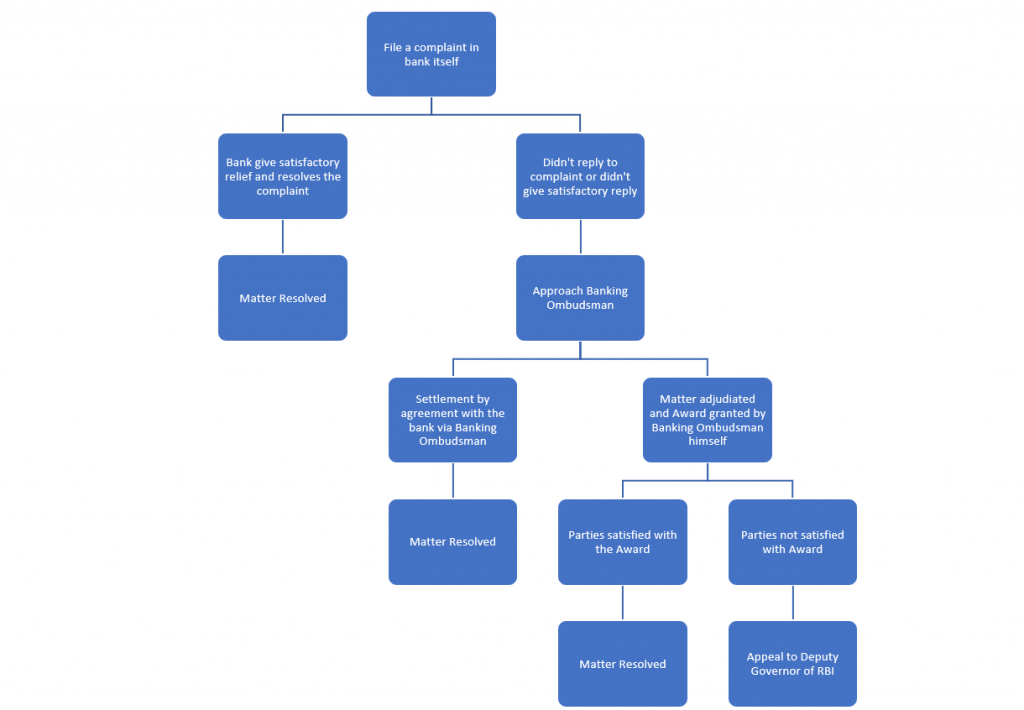

Pictorial representation of dispute redressal procedure against banks:

What is maximum Award Banking Ombudsman can impart?

Irrespective of anything mentioned in the scheme, the Banking Ombudsman doesn’t have the authority, to grant an Award which directs a payment of the amount as compensation which is higher than the actual material loss incurred by the complainant as a direct consequence of the bank’s acts of omission or commission of INR twenty lakhs, whichever is lower. The Banking Ombudsman jurisdiction is exclusive of the amount involved in the dispute. In addition to that, Banking Ombudsman sometimes also grants further compensation considering the complainant’s loss of time, expenses incurred by the complainant, mental agony and harassment the complainant has gone through. But even that award can’t exceed INR one lakh. The complainant and the bank are entitled to receive a copy of the Award granted by Ombudsman.

Do you get money immediately after the order?

Do you get money immediately after you have got an award from Ombudsman? Is it bank’s responsibility now to credit the amount of compensation in your account after the award?

The complainant has the responsibility to furnish a letter of acceptance in writing of Award as full and final settlement of all his claims, within a period of 30 days from the date of receipt of copy of the Award. If the complainant doesn’t do so, the order will be considered as lapsed and will have no effect. Further, the complainant doesn’t have to furnish any such acceptance given that he has filed an Appeal against the Ombudsman’s award.

The bank also has an obligation, to give effect to the Award and intimate compliance to the Banking Ombudsman, within a month from the date of receiving the written acceptance of the Award from the complainant, if there is no

What are the grounds of rejection of the complaint?

The Banking Ombudsman has the authority to reject a complaint at any stage of the proceeding, if it appears to him any of the following things: –

- Complaint made to him is not on the grounds as laid down in Clause 8 we discussed hereinbefore;

- If the complaint is not made in accordance with the procedure laid down in with sub-Clause (3) of clause 9 which we have discussed earlier under the head of “Maintainability of Complaint”;

- If the amount involved in the matter is beyond the pecuniary jurisdiction of Banking Ombudsman as laid down under clause 12 (5) and 12 (6) of the scheme;

- Requisite consideration of verbal evidences and elaborate documentary and the proceedings before the Banking Ombudsman are not adequate for adjudication of such complaint; without any sufficient cause;

- That the complaint has not been pursued with reasonable diligence by the complainant;

- If the Banking Ombudsman is of the opinion that no damage or loss or inconvenience has been suffered by the complainant.

- If the Banking Ombudsman discovers, at any stage of the proceedings, that the complaint before him relates to the same cause of action, for which any proceedings before any court, tribunal or arbitrator or any other forum is pending or a decree or Award or order has already been passed by any such judicial body, he passes an order to reject the complaint, providing the same as the reason.

What if you are not satisfied with the Award?

The complainant party, who is aggrieved by the Award or rejection of a complaint for the reasons laid down in sub clauses (d) to (g) of Clause 13 as discussed in previously, should within thirty days from the date of communication of Award or rejection of complaint, can file an appeal before the Deputy Governor of the Reserve Bank of India (the Appellate Authority). If Appellate Authority thinks that complainant has sufficient cause for not making an appeal within the said time limit, then it can further allow a period of maximum 30 days to the complainant to appeal.

If bank is the party to file the appeal, thirty days period for filing an appeal will commence from the date on which the bank receives letter of acceptance of Award by complainant under Sub-Clause (8) of Clause 12. The bank can only file an appeal with the previous sanction of the Chairman or if he is not present, the Managing Director or the Executive Director or the Chief Executive Officer or any other official of equivalent rank.

What to expect from Appellate Authority?

The Appellate Authority hears the case, after providing each of the parties a reasonable opportunity of presenting their case, there are the following possible outcomes: –

- The Appellate Authority will dismiss the appeal,

- The Appellate Authority will allow the appeal and set aside the Award,

- The Appellate Authority resend the case to the Banking Ombudsman for rehearing, this time in accordance with such instructions and directions as the Appellate Authority deems to be necessary or proper,

- The Appellate Authority will make the necessary modifications in the Award and give such instructions as it may deem necessary to give effect to the Award so modified;

- The Appellate Authority can grant any other award as it deems fit.

Duties of Banks covered under Banking Ombudsman Scheme 2006:

- Display Banking Ombudsman Details in its branches and offices: All the banks covered under the Scheme have the duty to make sure that the purpose of the Scheme and the contact details of the Banking Ombudsman to whom the complaints are to be made are displayed prominently in all of its offices and branches in such a way that it is noticeable to the person visiting the branch or office and he can get all the information including the contact details of the banking ombudsman and information pertaining to the scheme.

- Make available Scheme’s copy: All the banks under the said scheme have to make sure that a copy of the Scheme is available with the designated officer of the bank for reference purposes in the workplace premises of the bank, so that if anyone wishes to file a complaint, the information is available to him on the spot.

References

Name & Address of the Office of Banking Ombudsman

https://rbi.org.in/Scripts/AboutUsDisplay.aspx?pg=BankingOmbudsmen.htm

FAQs

https://www.rbi.org.in/Scripts/FAQView.aspx?Id=24

ANNUAL REPORT ON BANKING OMBUDSMAN SCHEME

CONSUMER CASES ON BANKING

https://www.rbi.org.in/Scripts/bs_viewcontent.aspx?Id=171

Compendium of Cases Handled by the Banking Ombudsman Offices:

https://rbidocs.rbi.org.in/rdocs/Content/PDFs/71337.pdf

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications