")

In this blog post, Salang Ishan Sharma, an Advocate in Punjab And Haryana High Court, Chandigarh who is currently pursuing a Diploma in Entrepreneurship Administration and Business Laws from NUJS, Kolkata, discusses how the founders of a trust earn money.

Definition of trust

According to Section 3 of the Indian Trusts Act, 1882, a trust is defined as “an obligation annexed to the ownership of property, and arising out of a confidence reposed in and accepted by the owner, or declared and accepted by him, for the benefit of another, or of another and the owner”.

In general terms it is an equitable and beneficial right or title to land or other property, held for the beneficiary by another person, in who resides the legal title or ownership, recognized and enforced by the Court of Chancery. An obligation arising out of the confidence reposed in the trustee or representative, who has the legal title to property conveyed to him, that he will faithfully apply the property according to the confidence reposed or, in other words wishes or guarantor of the trust.[1]

Nature of trusts

It is a duty which binds the person to deal with the property over which he has control, for the benefit of persons, of whom he may himself be one, and anyone of whom may enforce the obligation.

Constitution of trusts[2]

A trust is completely constituted by the settlor either:

- Effectively transferring certain property to trustees and declaring the trusts on which the trustees are to hold such property, or

- Declaring that certain property vested in them is to be held henceforth by them

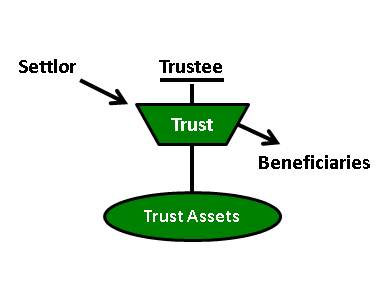

The essential requirements of a trust[3]

A trust must have the following essential elements:

- a settlor (the person who creates the trust)

- the assets to put into the trust

- a trust deed (the legal document setting up the trust)

- one or more trustees (those in charge of administering the trust)

- beneficiaries

The law requires that the settlor must intend to create a trust in order for a trust to exist. Therefore a valid trust cannot come into being by accident.

Issues to consider for trusts

- The property to be subject to the trust must be certain

- The precise extent of the beneficial interests must be certain

For certainty as to the objects or persons to be benefited by a trust, these must be:

- Expressly designated or

- So defined that they are capable of being ascertained

Purpose

There are various situations in which a trust may be set up, and not all of them are related to making a Will. For the purposes of making a Will, trusts are usually set up for one of the following reasons:

- To hold assets on behalf of a child until they reach the age of 18. Doing so allows for the property or money to be properly managed until the children are old enough legally to take possession of it. Some types of trust allow the beneficiary to receive an income from the property.

- To reduce the Inheritance Tax liability. Putting assets into trusts can, in some cases, reduce or even eliminate the inheritance tax liability for that asset; it can also help to keep the value of the estate within the nil-rate band.

- To provide for your spouse while keeping the estate intact to be passed to your children.

- To protect the family home from being sold in order to pay for residential care.

For advice on how a trust could work in your specific circumstances, you should speak to a legal or financial professional.

Classification of Trusts[4]

-

Express trust

It is created by a settlor, who transfers property to a trustee for a valid trust purpose. The trustee then distributes the trust property to a beneficiary pursuant to the terms of the trust. This could be under a will or by way of a trust deed or even under a document not under seal or orally. What matters is that there is intention and conduct creating the trust. An express trust is also referred to as a declared trust.

-

Implied trust

An implied trust arises from the presumed as opposed to the expressed intention of the owner of the property. So, for example, if property is transferred to A to be held on certain trust which fail there is a presumption that A hold the property in trust for the owner’s estate. Sometimes these are also called presumptive trusts or resulting trusts.

-

Private trusts

A trust is said to be private if it is for the benefit of an individual or a class of individuals which the law refers to as a defined but limited group of beneficiaries. By its nature it can be enforced by the individual or individuals. It is private even though there may be some benefit conferred thereby to the public at large. It is for the benefit for certain private individuals and for general public.

-

Public or charitable Trust

On the other hand, a public trust promotes the public welfare as an object and is public even if it incidentally confers a benefit on an individual or class of individuals. The public trust is only enforceable by the Attorney-General or an officer appointed by him for that purpose or by two or more persons who can show that they have interest in the trust with the express consent of the Attorney-General. So, it is an organization that manages money for a particular charity or group of people who are poor or in need of help. Also Public trusts, on the other hand, are governed by central legislations such as the Religious Endowments, 1863, the Charitable Endowments Act, 1890, the Charitable and Religious Trusts Act, 1920, the Registration Act, 1908 and by state legislations such as the Bombay Public Trust Act, 1950.

Modes of earning money for founders of a trust

As Trust is formed for a welfare purpose and the mode of earning can either be in the form of:

- Donations- It shall be in the form of pubic donations or private donations which are made voluntarily to the trusts without any force or forgery ;

- By giving on lease, rent, Mortgage, license to the said Trust property for generation of income;

- For the service of maintaining Beneficiaries property which is being given to the trustee for taking care of the beneficiaries property;

- A trustee has no right to remuneration unless a provision for such remuneration has been laid down in the instrument of the trust. Thus, if the founder of a private trust wishes to earn money through a trust as its trustee, he or she must lay down express provisions for the same in the trust’s instrument.

- In case of any commercialization then in that case income generated from such commercialization.

- Contracting with a client in relation to interest earned on client monies.[5]

- Dividends received in lieu of investments which are made by the founders or the owners of the trusts.

Benefits of setting up a trust[6]

Here are some common benefits and objectives of using trusts:

- Avoiding taxes: A common tax-saving trust is an irrevocable life insurance trust. After you die, the proceeds from your life insurance policy (the death benefit amount) are added back into your estate, often turning an estate that isn’t subject to federal estate taxes into an estate that needs to write a substantial check to the IRS!

However, an irrevocable life insurance trust shelters life insurance death benefit proceeds from estate taxes. After setting up the trust, you still have life insurance, and your beneficiary or beneficiaries still receive the proceeds from your policy upon your death. But now, estate taxes may not be a problem.

- Avoiding probate: By keeping certain property out of your probate estate, you may be able to avoid many of the hassles, costs, and lack of privacy concerns related to probate.

- Protecting your estate (and your beneficiary’s or beneficiaries’ estate): One of the primary uses of trusts is to protect your property even after it becomes someone else’s estate.

For example, suppose that you want to leave $500,000 to your only son, but you’re concerned that before you can say, “sail around the world,” he will have spent the entire half million.

You can use a trust to parcel out the money to your son as you see fit. The trust can give him a little bit each year for some duration, and then a final lump sum at some age when you think he’ll be mature enough to protect the money as if he had actually earned it himself.

Or you can add conditions to how the money in the trust is dispersed, such as your son receives a little bit of money until a certain age, and then he gets the rest only if he graduates college or meets some other criteria you determine when you set up the trust.

- Providing funds for educational purposes: Trusts can make money available to your children, grandchildren, other relatives, or even non-relatives (your employees’ children, for example) for educational purposes, such as college tuition and living expenses.

You can set up and fund trusts that parcel out money for educational purposes with a no-school, no-money restriction.

- Benefiting charities and institutions: You can help out charities by setting up some type of charitable trust that may, for example, annually give money to the charity while you’re still alive, give a larger amount upon your death, and then continue to make regular payments out of the remainder.

You can even set up a charitable trust to make regular payments to the charity for some amount of time but eventually “give back” whatever is left to you or, if you’ve died, to someone else in your family. Alternatively, you can set up a charitable trust to work the other way — pay you while you’re still alive, and upon your death, the remaining amount in the trust goes to the charity.

Winding up of a trust

When the primary beneficiary of the trust dies, any remaining trust assets can be distributed to other named beneficiaries, or to charity if preferred, according to the instructions given in your Will.

Footnotes:

[1] http://thelawdictionary.org/trust/

[2] https://www.lexisnexis.com/uk/lexispsl/privateclient/document/393819/5FN9-GY41-F18D-H32K-00000-00/Nature%20and%20classification%20of%20trusts%E2%80%94overview

[3] http://www.howtolaw.co/understand-trusts-392075

[4] http://www.kenyalawresourcecenter.org/2011/07/classifications-of-trust.html

[5] https://www.charteredaccountants.com.au/secure/myCommunity/blogs/PaulM/professional-standards-blogs/106/interest-earned-on-client-money-held-in-a-trust-account

[6] http://www.dummies.com/how-to/content/benefits-of-setting-up-a-trust.html

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

Can a trust earn money through businesses?