The article seeks to provide a brief overview of the Central Goods and Services Tax Act, 2017 by analysing some of its major provisions and also discussing judicial precedents in this regard.

Table of Contents

Introduction

For the longest time, indirect taxation of goods and services in India was a subject under the State Legislature. The states had the authority to decide and levy indirect taxes under the heads of cess, VAT, service tax, etc. This resulted in inconsistency among the states on the grounds of what kind of taxes were to be levied and at what rate. Another major problem arose during the inter-state transport of goods, as it allowed double taxation on the same goods by different states. To cater to this problem, there were various recommendations for introducing a unified indirect tax system in India. After various recommendations and discussions, in 2016, the indirect tax regime in India was replaced by a unified system known as the Goods and Services Tax (GST).

Under the GST system, the principle of ‘One Nation, One Tax’ has been adopted by the Legislature. The GST Council has been established to make recommendations on the rates of tax on goods and services in both intra-state as well as inter-state commerce. The tax levied is distributed equally between the Centre and the states. This article focuses on the historical background, structural framework, and crucial jurisprudence revolving around the GST system.

Historical background of Central Goods and Services Tax Act (CGST), 2017

The concept of GST has not been new to India. As early as 2000, it was the Kelkar Task Force on Indirect Taxes that first proposed to bring a unified indirect tax system in India. The recommendation was made with the following objectives:

- Reduce the cascading effects of tax

- Simplify compliance for the common man

- Unify the fragmented indirect taxes

- Cooperative federalism

Thereafter, certain recommendations were given by the Task Force, which included the following:

- Both the Center and states should have a common tax base.

- Both the Center and states should remove the existing taxes that prevailed in their respective jurisdictions.

- Both the Center and states should have independent power to fix tax rates, yet both must come together to coordinate and decide the taxes to be imposed

- Both the Center and states should adopt a mechanism for cooperative revenue sharing.

Pursuant to a lot of deliberation, the Constitution (122nd Amendment) Bill, 2014, was introduced in Parliament. After certain amendments, the GST was finally brought into the Indian tax regime by way of the Constitution (101st Amendment) Act, 2016.

Structural framework surrounding GST law

Pursuant to the passing of the Constitutional Amendment, the Parliament introduced certain laws that cumulatively form part of GST law. These include the Central Goods and Services Tax Act, the Integrated Goods and Services Tax Act, and the Goods and Services Tax (Compensation to States) Act, 2017. Alongside, each of the states and union territories also passed their respective statutes relating to GST.

The Constitutional Amendment also gave way to the formation of a GST Council, which shall be responsible for providing recommendations on various issues surrounding GST laws. As regards the executive wing, the Central Board of Indirect Taxes and Customs (CBIC) replaced the erstwhile Central Board of Excise and Customs (CBEC) and functions under the Ministry of Finance. For adjudication of disputes, recently, the GST Appellate Tribunals (GSTAT) have been formed in various states. Hence, it can be said that CBIC, the GST Council, and the GSTAT function together to give effect to the GST laws.

Key provisions in Central Goods and Services Tax Act (CGST), 2017

Definition clause (Section 2)

Actionable claim

Section 2(1) of the Act defines an actionable claim. It makes reference to Section 3 of the Transfer of Property Act, 1882, and assigns the same meaning. Reference to Section 3 of the Transfer of Property Act reveals that an actionable claim is a claim to a debt that entitles a ground of relief to the beneficiary. Such interest/benefit may be existent, accruing, conditional, or contingent. However, it does not include mortgage/hypothecation. The definition is relevant to understanding some of the recent judgments on the law, which have been discussed in the latter section. In Gurdip Singh Sachar v. Union of India (2019), the Hon’ble Bombay High Court held that the amount pooled in an escrow account for operating an online fantasy game constitutes an actionable claim as the same are to be distributed among the winning. Other examples of actionable claim, as held in H. Anraj v. Government of Tamil Nadu (1985), would include negotiable instruments, a claim to arrears, a right to recover insurance money, etc.

Composite supply

Section 2(30) of the CGST Act defines composite supply as a supply that consists of two or more supplies that are naturally bundled and supplied in conjunction with one another. Here, there is a principal supply and other supplies complement the principal supply. For example, Mr. A from Kolkata supplies certain goods to Ms. B in Delhi. The goods are packed, insured, and transported through a courier. The services of courier, packing, and transportation form part of the composite supply, and the main supply of goods is the principal supply. Another example of a composite supply could be the supply of a mobile phone, wherein the inclusion of a charger, earphones, and other phone accessories forms part of the composite supply.

Exempt supply

Exempt supply, as defined in Section 2(47) of the Act, means the supply of goods or services in the following three categories:

- Goods/services which attract nil or zero rate of tax

- Goods/services that are wholly/partly exempt from the levy of GST

- Exempt supplies under Section 2(72) of the CGST Act, 2017 (covered in latter part)

Goods

Goods have been defined in Section 2(52) of the Act. It states:

“goods means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply;”

Hence, the definition of goods has been kept broad enough under the Act to include all sorts of movable property as well as actionable claims, growing crops, and things attached to the land. Article 366(12) of the Indian Constitution defines goods to include all materials, commodities, and articles. Hence, it makes it clear that goods include both raw materials as well as finished products. This view has also been upheld by the Hon’ble Supreme Court in Ch. Tika Ramji v. State of Uttar Pradesh (1956).

Further, it is also pertinent to mention the ruling of the Hon’ble Supreme Court in the case of Tata Consultancy Services v. State of A.P. (2004), where it was held that a good must be capable of being abstracted, consumed, extracted, transferred, transmitted, delivered, stored, and possessed, irrespective of whether such good is tangible, intangible, corporeal, or incorporeal. Further, in the case of Commissioner of Sales Tax, Madhya Pradesh v. Madhya Pradesh Electricity Board (1968), the Hon’ble Supreme Court held that the term ‘movable property’ to interpret goods should be given a broad purview. As regards the supply of electricity, it cannot be said that the same is immovable merely because it is intangible or cannot be moved or touched.

Mixed supply

Mixed supply has been defined in Section 2(74) of the Act and means a supply where certain goods are supplied together, though they are not naturally bundled. Though a single price is charged for such a combination, they may not always necessarily/naturally be sold together. In a mixed supply, there is no principal supply. For example, a gift hamper containing a mix of chocolates, juices, packed food items, cold drinks, etc. Another example could be a case where a company sells a pencil box along with a pencil, eraser, sharpener, and ruler and charges a single price.

Non-taxable supply

Non-taxable supply has been defined under Section 2(78) of the CGST Act, 2017. At the time of the introduction of GST, certain items were kept outside the purview of GST, as many of the states were reluctant owing to the significant source of revenue from such goods or services. Some of these include petrol, diesel, alcoholic liquor, etc. All such categories of goods and services are non-taxable supplies. GST cannot be levied on these supplies nor can credit be claimed.

Principle supply

Principal supply has been defined in Section 2(90) of the Act and is relevant to the concept of composite supply. Principal supply refers to the supply of goods or services that constitutes the predominant element in the entire bundle.

Services

Services have been defined under Section 2(102) of the CGST Act, 2017 and given a wider connotation than the term ‘goods’. It states:

“services means anything other than goods, money and securities but includes activities relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged.

The term has been given a much wider scope to ensure that the Department can tax anything under the sun, even if such supply does not qualify as goods.

Scope of supply (Section 7)

Section 7 is the charging Section of the Act. It forms the basis for the Government to charge taxes. The provision elaborately provides for the definition of supply and what is excluded and included in the definition of supply. The supply of all forms of goods and services, whether by way of sale, transfer, barter, exchange, licence, rental, lease, or disposal, will be covered under the definition of supply. Such a supply should be made by a person for consideration in the course of business. Six parameters to understand the concept of supply have been enlisted below:

- Involves either goods or services

- Made for a consideration

- Made in the course or furtherance of business

- Must be a taxable supply

- Must be made by a taxable person

- Must be made within the taxable territory

It is crucial that Section 7 is read along with Schedule I, Schedule II, and Schedule III. Schedule I provides for certain activities that must be treated as supply even if made without consideration. Schedule II mentions certain activities and specifies whether they are to be treated as supply of goods or services. Schedule III provides for activities or transactions that are neither treated as supply of goods nor services.

Composite and mixed supply (Section 8)

Section 8 of the Act provides for the taxability of composite and mixed supply. For composite supply, the rate of tax is determined on the basis of principal supply. However, in the case of a mixed supply, it is determined on the basis of the good/service that attracts the highest rate of tax.

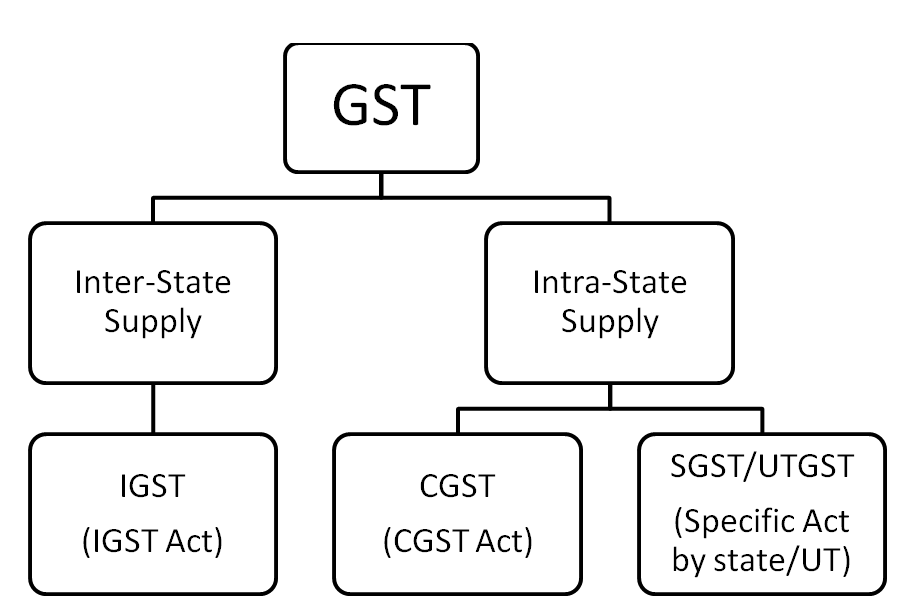

Levy and collection (Section 9)

Section 9 of the Act gives the power of levy and collection of taxes to the Government. It provides for a levy of tax, which shall be known as the central goods and services tax, i.e., CGST. It is important to know that CGST is only levied on intra-state supplies of goods and services, i.e., transactions that take place inside the state. If the supply of goods and services takes place outside the state, then it is considered as inter-state supply of goods and services, and an integrated goods and services tax is levied on such transactions. This can be understood with the help of the following illustration and chart:

Mr. A, residing in Maharashtra, carries on the trade of selling electronic devices. Ms. B buys a mobile phone worth Rs. 20,000, on which GST is levied @18%. The treatment of GST will differ based on the destination of Ms. B since GST is a destination-based tax.

Case 1 – When Ms. B resides in Maharashtra

In such a case, the transaction will be considered an intra-state supply of goods and CGST and SGST will be levied. Here, SGST is Maharashtra Goods and Services Tax (MGST). Hence, 18% GST (Rs. 3,600) will comprise 9% CGST and 9% MGST (i.e., CGST = Rs. 1,800 and MGST = Rs. 1,800).

Case 2 – When Ms. B resides in any state other than Maharashtra

In such a case, the transaction will be considered as an inter-state supply of goods and IGST will be levied. Accordingly, IGST will be levied at 18% (i.e., IGST = Rs. 3,600).

The provision provides that the maximum CGST that can be levied by the Government is 20%, which means the entire GST can be 40%. However, in the current GST regime, the highest tax slab rate has only been 28%. Additionally, certain goods, such as petroleum crude, high speed diesel, motor spirit, natural gas, and aviation turbine fuel, are currently exempt from the levy of GST; the Government can levy tax on these goods pursuant to a notification based on the recommendations of the GST Council.

Lastly, the provision also empowers the Government to notify the categories of taxable persons who shall be responsible for payment of tax on a reverse charge basis and also those electronic commerce operators who may be deemed suppliers if goods or services are supplied through them.

Composition levy (Section 10)

Section 10 of the Act provides for the option of a composition levy. It is an alternative scheme, especially designed to cater to the small taxpayers in the country. For a small-scale business, compliances under GST might become cumbersome and complicated, thereby defeating the objective of GST to simplify the taxes. Hence, a business with an aggregate turnover of less than one crore fifty lakhs in the previous financial year can opt for the composition scheme. For certain special category states, which include the seven north-eastern states and Uttarakhand, the aggregate turnover is considered to be seventy-five lakhs.

The rate of tax prescribed for persons opting for the composition scheme is as follows:

| S. No. | Category of Person | Rate of GST |

| 1. | Manufacturers | 2% |

| 2. | Supplier of food/drink other than alcohol | 5% |

| 3. | Traders or any other supplier eligible for composition levy | 1% |

The following conditions are required to be met by a person opting for the composition scheme:

- They cannot raise any tax invoices.

- They are not eligible to collect tax on any supply of goods/services.

- The recipients of supply made by composite dealers cannot claim input tax credit.

- Entities opting for composition levy cannot claim input tax credit.

- Such entities must clearly state on invoices that they have opted for composition levy.

- Such entities must mention ‘composition taxable person’ at their place of business.

Additionally, the following categories of entities are not eligible for the composition scheme:

- Casual taxable person or non-resident taxable person

- Persons making inter-state outward supply of goods/services

- Person making supply of goods not covered under GST law

- Suppliers of services other than restaurant services

- Manufacturers of ice-cream, pan masala, tobacco or aerated water

- Suppliers whose aggregate turnover exceed the stipulated limit

- Suppliers making any supply of goods through any e-commerce operator covered under Section 52 of the Act

Time of supply of goods and services (Section 12-14)

Time of supply of goods (Section 12)

The time of supply of goods, in accordance with Section 12, can be understood with the help of the following table:

| S. No. | Type of supply | Time of supply of goods |

| 1. | Supply of goods on forward charge basis | Earlier of two dates:Date of issue of invoice or the last date on which the invoice was ought to be issuedEarlier of the date on which the payment is credited in the bank of supplier or the date on which amount is credited in the books of accounts of the supplier |

| 2. | Supply of goods on reverse charge basis | Earlier of three dates:Date of receipt of goodsEarlier of the date on which the payment is credited in the bank of supplier or the date on which amount is credited in the books of accounts of the supplierDate immediately following thirty days from the date of issue of invoice |

| 3. | Supply of voucher | Identifiable supply of voucher (i.e. the supplier is aware for what category of goods such a voucher will be used, such as a voucher by Pizza Hut) – Date of issue of voucherIn all other cases (such as an Amazon voucher), – Date of redemption of voucher |

| 4. | Other miscellaneous cases | Where periodical return is filed – Date on which such return is filedIn all other cases – Date on which the tax is paid |

Time of supply of services (Section 13)

Time of supply of services, in accordance with Section 13, can be understood with the help of the following table:

| S. No. | Type of supply | Time of supply of goods |

| 1. | Supply of goods on forward charge basis | Earlier of three dates:Earlier of the date of issue of invoice or the date of receipt of paymentEarlier of date of provision of service or the date of receipt of payment, if invoice is not issued in the stipulated timeThe date on which the recipient shows the receipt of services in his books of account, if the above conditions are not applicable |

| 2. | Supply of goods on reverse charge basis | Earlier of two dates:Earlier of the date on which the payment is credited in the bank of supplier or the date on which amount is credited in the books of accounts of the supplierDate immediately following sixty days from the date of issue of invoiceIf the above conditions are not applicable, then the date on which the recipient shows the receipt of services in his books of account |

| 3. | Supply of voucher | Identifiable supply of voucher (i.e. the supplier is aware for what category of services such voucher will be used, such as a voucher by a restaurant service provider) – Date of issue of voucherIn all other cases – Date of redemption of voucher |

| 4. | Other miscellaneous cases | Where periodical return is filed – Date on which such return is filedIn all other cases – Date on which the tax is paid |

Change in rate of tax in respect of supply of goods or services (Section 14)

The general practice is to identify the time of supply in accordance with Section 12 or Section 13, depending on whether the supply is of goods or services. However, there might be situations where the Department has changed the rate of tax prevailing on certain particular goods or services. In such a case, it becomes difficult for taxpayers to understand whether the old or new tax rate will be applicable.

To resolve this issue, Section 14 comes into play. It is important to remember that in all instances, there will be three factors – time of supply, date of issue of the invoice and date of payment. If two of these factors fall before the change in tax rate, the old rate will be applicable, and vice-versa. The same can be understood with the help of the table below:

| Change of tax rate before the supply | Change of tax rate after the supply |

| When the invoice is issued and payment is received subsequent to the change, then the time of supply will be earlier of the date of payment or the date of issue of the invoice.Accordingly, the new rate will be applicable. | When the invoice is issued and payment is received before the change in tax rate, then the time of supply will be earlier of the date of payment or date of issue of invoiceAccordingly, the old rate will be applicable. |

| When the invoice is issued prior to the change in tax rate and payment is received after the change of rate of tax, then the time of supply will be the date of issue of invoice.Accordingly, the old rate will be applicable. | When the invoice is issued is prior to change in rate and payment is received after the change in tax rate, then the time of supply will be the date of payment.Accordingly, the new rate will be applicable. |

| When the invoice is issued after the change in tax rate and payment is received prior to the change in tax rate, then the time of supply will be the date of receipt of payment.Accordingly, the old rate will be applicable. | When the invoice is issued after the change and payment is received prior to the change in tax rate, then the time of supply will be the date of issue of invoice.Accordingly, the new rate will be applicable. |

Value of supply (Section 15)

Section 15 provides that the value of supply shall be transactional value, which means the actual price paid by the buyer to the supplier. This condition is applicable only to those situations where the buyer and supplier are not related and price is the sole consideration for the supply. Where such a prerequisite is not fulfilled, reference must be made to Rules 27 to 35 of the CGST Rules, 2017.

Further, an explanation to Section 15 defines related persons and includes officer/director/partner in one another’s business, employer and employee, members of the same family, directly/indirectly control a third person or are controlled by a third person, or if a person holds more than 25% of the stock.

Input tax credit (Sections 16 and 17)

Eligibility and conditions for input tax credit (Section 16)

Section 16 is one of the most important provisions in the entire CGST Act, as it provides for the concept of input tax credit (ITC). GST was aimed with the object of removing cascading effect of taxes. This object is fulfilled through the mechanism of the ITC itself. In simple terms, a taxpayer receives credit of the amount of its inward supplies, which can be adjusted against the amount of its outward supplies. This ensures that the burden of taxes charged at multiple levels of the supply chain is not entirely on the end customer.

Section 16(1) provides that a registered person shall be eligible for ITC for all those good/services that are used in the course or furtherance of their business. Hence, it is imperative to note that goods or services that are used for personal consumption cannot be taken into account. Yet, we may observe that people tend to show their personal expenses in their business accounts to gain deductions from taxes. In order to curb this situation, Section 17 was imbibed into the Act to disallow credit on certain supply of goods and services. The same has been discussed in the latter part.

As regards Section 16(2), it provides conditions for availment of credit. It provides for five basic conditions, which are as follows:

- The recipient possesses tax invoice, debit note, or any other tax-paying document issued by the supplier of goods/services.

- Details of invoice/debit note have been furnished by the supplier in its outward supplies in GSTRR-2B.

- The recipient has received the goods or services.

- Tax has actually been paid to the Government in respect of such goods and services.

- Return has been furnished by the recipient under Section 39 of the Act.

Lastly, Section 16(4) also culls out one condition for the eligibility of the ITC. It provides that, in respect of any invoice or debit note for the supply of goods or services or both, credit must be claimed:

- Prior to 30th November following the end of financial year to which such invoice or debit note pertains, or;

- Furnishing of the relevant annual return, whichever is earlier.

Apportionment of credit and blocked credit (Section 17)

As Section 16 provides for conditions for the eligibility of credit, Section 17 stipulates the conditions by virtue of which credit cannot be taken. As has been previously mentioned, credit can be taken for only those transactions carried out in the course or furtherance of business. This has been provided under Section 17(1) of the Act. Further, credit cannot be taken in those instances where the supply of goods or services are exempt supplies. Clauses (a) to (i) of Section 17(5) provide specific instances where credit cannot be availed. Some of these instances include motor vehicles with capacity of less than 13 people, membership of a club or fitness/health centre, works contract for construction of an immovable property, goods for personal consumption, etc. The object of specifically excluding these supplies is that the Revenue assumes that such supplies are mostly used as end consumption; providing credit on these supplies would create a means to escape the taxes.

Registration (Sections 22 to 24)

Chapter VI of the Act provides for the eligibility and procedure of registration. It states the conditions under which registration shall be required by a person or entity and cases where registration is not mandatory. It also provides for amendment, cancellation, and revocation of registration. Some of these pertinent provisions have been discussed hereafter.

Persons liable for registration (Section 22)

Section 22 provides that any supplier who crosses the aggregate turnover in a particular financial year is required to be registered under the Act. Aggregate turnover means the total amount of supplies made by a supplier, whether on his own account or that on behalf of his principals. The limits for aggregate turnovers for goods and services are as follows:

| Normal category states | Special category states | |

| Goods | Forty lakh rupees | Twenty lakh rupees |

| Services | Twenty lakh rupees | Ten lakh rupees |

If any entity is engaged in the supply of both goods and services, the turnover relating to services, i.e., twenty lakh rupees and ten lakh rupees, will apply, depending on the category of states.

Special category states are those states that have been accorded special status owing to their socio-economic and geographical conditions. These include Assam, Nagaland, Himachal Pradesh, Manipur, Meghalaya, Sikkim, Tripura, Arunachal Pradesh, Mizoram, Uttarakhand, and Telangana. All other states are considered to be in the normal category.

As regards cases where the business is transferred as a going concern or the business is merged or amalgamated, the aggregate turnover will be calculated from the date such transfer is actually effected or the date when the new entity receives the certificate of incorporation pursuant to an order of a court or tribunal.

Persons not liable for registration (Section 23)

As per Section 23, a person shall not be required to register under the Act if satisfying any of the two below-mentioned conditions:

- A person is exclusively engaged in the supply of goods and services which are non-taxable or wholly exempt under the Act

- A person is an agriculturist only engaged in supply of produce cultivated from the land

Further, on the recommendations of the GST Council, the Government may specify other instances where registration may not be mandatory. To exemplify, vide Notification No. 05/2017 (Central Tax) dated June 19, 2017, the Government notified that suppliers who are exclusively engaged in supply of goods or services taxable under the reverse charge basis, shall not be mandatorily required to register under the Act.

Compulsory Registration (Section 24)

Section 24 carves out cases where a person is mandatorily required to be registered under the Act even if such supplier does not cross the specified aggregate turnover. These cases are as follows:

- Person engaged in inter-state supply of goods and services

- Casual taxable persons who make taxable supplies

- Persons who are required to pay tax under reverse charge mechanism

- Persons who are considered deemed suppliers as per Section 9(5) of the Act

- Non-resident taxable persons making taxable supplies

- Persons required to deduct tax in accordance with Section 51 of the Act

- Persons making supply on behalf of other persons as agent etc.

- Input Service Distributor

- Electronic commerce operator required to collect tax at source in accordance with Section 52 of the Act

- Person engaged in supply of OIDAR (online information and database access or retrieval) services from outside India to a non-registered person in India

- Such other class of persons as notified by the Government

Returns (Chapter IX)

Since GST follows the mechanism of self-assessment, taxpayers are required to file a return providing all the requisite information relating to their outward and inward supplies, input tax credit, etc. Unlike the erstwhile regime, returns are to be mandatorily filed online by the taxpayer. This helps the Government with proper record keeping and easy identification of any irregularities through technological assistance. Some of the most relevant provisions in this regard are discussed hereafter.

Furnishing details of outward supplies (Section 37)

Section 37 provides for furnishing details related to outward supplies. Outward supply refers to the sale/supply of goods or services by the supplier. All the details related to outward supplies is required to be furnished in Form GSTR-1 and must be filed on or before the 10th day of the immediately succeeding month. This means that such a return is required to be filed on a monthly basis. Only the following categories of persons are exempt from filing this return:

- Input service distributor

- Non-resident taxable person

- Composite dealer

- Person deducting tax at source

- Person collecting tax at source

- Supplier of OIDAR services located in non-taxable territory providing services to a non-taxable online recipient

Furnishing details of inward supplies (Section 38)

Section 38 provides for furnishing details related to inward supplies. Inward supplies refer to those supplies purchased by the supplier and used in the course or furtherance of business. Details related to inward supplies are provided in Form GSTR-2A and Form GSTR-2B.

GSTR-2A is a system-generated statement of inward supplies based on the information furnished by the outward supplier of such goods or services in GSTR-1 (normal supplier) or GSTR-4A (composite dealer). For example, Mr. A bought certain raw materials for his business from Ms. B. Ms. B will furnish GSTR-1 as part of her outward supplies. From this data, the GST portal will automatically recognize the transaction with Mr. A and the same will be reflected in GSTR-2A of Mr. A. The information is updated on a real-time basis and is considered an auto-generated return on every 12th day of the immediately succeeding month.

GSTR-2B is also an auto-generated statement and it provides information relating to the eligible input tax credit of the assessee. It is a static statement and is available only once a month.

Furnishing of returns (Section 39)

Section 39 further stipulates a monthly return required to be filed by all taxpayers except the categories as already specified in Section 37. It provides for filing of a summary return as per Form GSTR-3B which is to be filed on or before the 20th of the month succeeding the month for which the return is furnished. GSTR-3B contains a summary statement of all the outward supplies, inward supplies, eligible ITC, liability under reverse charge, etc.

Refund (Section 54)

We have already discussed that the GST law provides for the facility of input tax credit to prevent the cascading effect of taxes and make goods and services more economical for the common man. However, in certain situations, it may happen that excess credit is accumulated in the electronic credit ledger of the taxpayer and cannot be utilized. Resultantly, Section 54 of the Act provides for a refund of tax. It mentions two situations in which tax can be refunded.

- Firstly, the goods/services are zero-rated supplies and no payment of tax has been made. This means that the taxpayer has accumulated credit due to the payment of tax on input supplies but the output supplies are zero-rated, as a result of which excess credit gets accumulated.

- Secondly, the rate of tax of input supplies is higher than rate of tax of output supplies, resulting in an inverted duty structure. This may be understood with the help of an example. Supposedly, the input supplies are taxed at 18% but output supplies are taxed at 5%. Resultantly, there will always be a situation of excess accumulated credit.

It is only under these two conditions that the provision permits for refund of tax. Additionally, the Department may notify other cases where refunds may be given pursuant to the recommendations of the GST Council.

Inspection, Search, Seizure and Arrest

Power of inspection, search and seizure (Section 67)

In order to protect the legitimate dues of the Government, Section 67 of the Act provides for mechanisms of inspection, search, seizure, and arrest. However, it must be remembered that these mechanisms must be used sparingly by the Department only to recover the taxes and not as a mode to harass them. Hence, for all these actions, it is mandatory that the officer must be at least of the rank of Joint Commissioner and he must have a reason to believe the existence of the following circumstances:

- Suppression of information related to stock of goods or services

- Claimed excess input tax credit

- Contravention of provisions of Act or related rules with an intention to evade taxes

- Transporting/keeping goods which have not been duly taxed or manipulation in stocks/accounts to evade tax

Power of arrest (Section 69)

Arrest under Section 69 is considered to be among the harshest modes of recovery under the GST law. It is only to be used in extraordinary circumstances and as a last resort. An order for arrest can be made only on the commission of offences mentioned under Section 132 of the Act. Hence, arrest can be done only when the tax escaped involves huge amounts, i.e., two hundred lakhs rupees or such taxpayer is a repeated offender. The Commissioner is empowered to order for arrest and may authorize any central tax officer in this regard.

Demands and Recovery of Tax

In case any taxable person fails to discharge the tax obligations within the prescribed period, the Department may demand initiate proceedings for recovery of such tax. GST follows the mechanism of self-assessment i.e. it is the responsibility of the taxpayer to assess its tax obligations and accordingly deposit the same to the Government. However, if it comes to the notice of the Department at a later point of time that tax has not been adequately or appropriately paid, it may demand and recover such taxes. Chapter XV of the Act deals with the same.

Demand of tax in cases other than fraud, willful mis-statement or suppression of facts (Section 73)

Section 73 states that the Department may send a show-cause notice to the taxable person to prove why it should not be liable under the Act to pay any additional amount where it appears to the officer that there is non-payment of tax, short payment of tax or wrongful availment or utilization of input tax. It is imperative to note that this provision is applicable only in cases of a bonafide error and not in cases involving fraud, willful mis-statement or suppression of facts. Such notice must be issued at least three months before the expiry of three years from the date of furnishing of annual return relating to the financial year for which the tax has not been paid.

Pursuant to the show-cause notice, the taxpayer can either pay the tax within thirty days along with interest. In such a case, no penalty shall be levied on the taxpayer and no further proceedings would be conducted on the same matter by the Department. Secondly, the taxpayer may dispute the amount and reply to the show-cause notice. Based on the representation, the officer can finally issue an order determining the final tax liability of the person along with interest and penalty (not exceeding 10%). The order must be passed before the expiry of three years from the date of furnishing of annual return relating to the financial year for which the tax has not been paid.

Demand of tax in cases of fraud, willful mis-statement or suppression of facts (Section 74)

As opposed to Section 73, Section 74 is applicable in cases involving an element of evasion of tax by the taxpayer, i.e., fraud, willful mis-statement or suppression of facts. The notice must be issued at least six months before the expiry of five years from the date of furnishing of annual return relating to the financial year for which the tax has not been paid. Here as well, similar procedure applies i.e. the taxpayer can either pay the amount within thirty days or dispute the amount by replying to the show-cause notice.

If the taxpayer decides to pay the taxes, interest and penalty (upto 25%) will be applicable. In case of dispute, representation will be made by the taxpayer and consequently, an order will be passed by the proper officer. The order must be passed before the expiry of five years from the date of furnishing of annual return relating to the financial year for which the tax has not been paid.

In both of these provisions, the time limits (three and five years) hold much relevance, as the law deems it fit that, pursuant to the expiry of such time, a taxpayer cannot be harassed and be made liable for tax obligations (if any) which existed years ago.

Section 78

Section 78 provides that where an order is passed by the officer under Section 73 or Section 74, the taxpayer must pay the amount within three months from the date of service of such order, failing which, the Department can initiate recovery proceedings against the person. Different modes of recovery have been provided in Section 79, as discussed hereafter.

Section 79

As per Section 79, the Department may initiate recovery proceedings against the taxpayer in the following ways:

- Deducting the amount from owed money under the control of officer (Rule 143)

- Detaining or selling the goods (i.e. auctioning) of the taxpayer which are under the control of officer (Rule 144)

- Recovering it from a third person (Rule 145)

- Executing the decree by the civil court (Rule 146)

- Attaching the movable or immovable property of the taxable person (Rule 147)

- Recovery with assistance from Collector, Deputy Commissioner or other authorities (Rule 155)

Reference may be made to this article for further information on different modes of tax recovery by the GST Department.

Liability to pay in certain cases (Chapter XVI)

Chapter XVI of the Act provides for certain special instances where the person or entity liable to pay GST has been specified. This is to ensure that, in the event of happening of these special cases (such as liquidation of a company or transfer of business, etc.), the Government does not face any loss of revenue.

Transfer of business (Section 85)

The Section provides for the determination of liability for payment of tax where any taxable person transfers the business by the following modes:

- Sale

- Gift

- Lease and license

- Hire

- Any other mode

Where the transfer is made in any of the aforementioned modes, whether wholly or in part, both the seller of the business as well as the recipient of the business shall be jointly and severally liable for tax obligation upto the date of transfer. The tax obligations include the payment of tax, interest, penalty or any other amount arising therefrom. Moreover, it becomes irrelevant whether such tax was determined prior or subsequent to the transfer.

Principal-agent relationship (Section 86)

Section 86 provides for cases where the agent either receives or supplies the taxable goods on behalf of the principal. In such a case, the agent is primarily responsible for the payment of taxes. However, since the agent is acting on behalf of the principal, both the principal and agent will be jointly and severally liable for the payment of tax on such goods.

Amalgamation or merger of companies (Section 87)

Section 87 deals with instances where two or more companies have entered into a scheme of merger or amalgamation and have engaged in the supply of goods and services with one another. If, by virtue of an order of court or tribunal or otherwise, the arrangement takes effect from a date prior to the date of passing of the order, even then, the transactions between the two entities upto the date of order will be included in the turnover of supply or receipt. This means that irrespective of the date of effect of arrangement, the date of passing of order shall be relevant to determining whether the transactions between the entities are considered to be distinct (in order to make them taxable). Further, their status as distinct companies shall be valid till the date of passing of the order, pursuant to which, their registration certificates will be cancelled by the Department.

Liquidation of a company (Section 88)

Section 88 aims to protect the revenue of the Government in cases where the taxable person, being a company, goes into liquidation. Section 88 aims to protect the revenue of the Government in cases where the taxable person, being a company, goes into liquidation. It provides that the where the court or Tribunal passes an order of liquidation for the company, then the person appointed as receiver or liquidator of the company is required to intimate its appointment to the Commissioner within thirty days of appointment. Pursuant to such intimation, it is the duty of the Commissioner to ascertain the amount of tax, interest, and penalty that is required to be paid or likely to be paid by the company. After ascertaining the tax obligation, the Commissioner must intimate the same to the receiver or liquidator within three months from the date of intimation of appointment of receiver.

In a case where such liquidation is that of a private company, and tax obligation determined becomes impossible to be recovered, whether before or after the liquidation, then all the persons of the company who were directors at the time when tax was due, shall be jointly and severally liable for the tax obligation. The only exception to the liability is if the director is able to prove that “such non-recovery cannot be attributed to any gross neglect, misfeasance or breach of duty on his part in relation to the affairs of the company”.

Directors in a private company (Section 89)

Section 89 is somewhat similar to Section 88 in application but it concerns private companies in general and is not only limited to instances involving liquidation. In a case where any payment of tax, interest, or penalty is due from a private company, and such tax obligation becomes impossible to be recovered, then all the persons of the company who were directors at the time when tax was due, shall be jointly and severally liable for the tax obligation. The only exception to the liability is if the director is able to prove that “such non-recovery cannot be attributed to any gross neglect, misfeasance, or breach of duty on his part in relation to the affairs of the company”. Further, if a private company is converted into a public company and tax, interest or penalty is not recovered before the conversion, then the directors cannot be made liable at a latter point post conversion. However, personal penalty could still be imposed on such director.

Partners in a firm (Section 90)

Section 90 burdens the partners of a firm where a firm fails to discharge any tax obligation under the Act. The firm as well as each of the partners are jointly and severally liable for paying such tax, interest, or penalty, unless any contract or law provides for the contrary. In case a partner seeks retirement, such retiring partner or the firm must intimate the Commissioner about the date of retirement by a notice. Moreover, it is the responsibility of the partner to ensure that all the tax obligation, whether determined or not, must be discharged as on his date of retirement. The failure of the same would cast a liability on the partner for payment of tax. Lastly, if the firm or partner fails to intimate about the retirement within one month, the liability of the partner towards the tax obligations of the firm would continue till such intimation is actually received by the Commissioner.

Additionally, the Act also provides for special instances relating to the liability of guardian and trustees (Section 91), court of wards (Section 92) etc.

Advance ruling (Chapter VII)

The Act provides for a new level of grievance redressal mechanism, as was previously provided under various erstwhile indirect tax laws. Chapter XVII of the Act deals with advance ruling. An advance ruling is a decision passed by an Authority for Advance Ruling or Appellate Authority for Advance Ruling on certain specified issues. Such decision-making authorities are part of the executive wing itself. Some of the important provisions in this regard are discussed hereafter.

Application for advance ruling (Section 97)

An assessee has the option to make an application for an advance ruling in accordance with Section 97 of the Act read with Rule 107A of the CGST Rules. It is important to note here that an application for advance ruling can be made with regards to only that supply of goods or services that are being undertaken or proposed to be undertaken by the applicant. It cannot be made for transactions that have already happened in the past. Section 97(2) provides that an advance ruling can be sought on the following matters:

- Classification of goods or services

- Applicability of any notification on the applicant

- Determination of time and value of supply of goods or services

- Admissibility of credit

- Determination of liability to pay GST on any supply

- Requirement of registration for applicant

- Identification of a transaction as a taxable supply under the law

Appellate Authority for Advance Ruling (Sections 99 and 100)

Section 99 provides for the constitution of an appellate body. Section 100 entitles an assessee or applicant with the right to appeal before the Appellate Authority for Advance Ruling. Such appeal is required to be filed within thirty days from the date of original ruling in accordance with Rule 106 of CGST Rules.

Applicability of advance ruling (Section 103)

Section 103 mentions two aspects of applicability of an advance ruling. Firstly, it provides that an advance ruling shall be binding on the applicant, i.e., the assessee, and the concerned revenue officer. This means that such advance ruling cannot be used as precedent in other cases and it only has persuasive value for other assessees. Secondly, the advance ruling shall be applicable only if the law, facts, and circumstances in the original case remain the same. For example, if an assessee significantly modifies its goods, which might result in difference in classification of such goods, then it may again apply for an advance ruling and the previous rulings shall cease to apply.

Mechanism for appeal and revision

Under GST, where the Revenue is of the view that there has been short payment of tax or credit wrongly availed, tax paid is inadequate or there is any such circumstance, a demand-cum-show cause notice is issued by the Commissioner. Pursuant to representation by the assessee, an order is passed by the concerned Commissioner (adjudicating authority). Section 107 provides that an appeal can be made against such order before the Commissioner (Appeals) who is considered to be the Appellate Authority.

Constitution of Appellate Tribunal and qualification of members (Sections 109 and 110)

Section 109 of the CGST Act, 2017 provides for the constitution of the Appellate Tribunal and its benches. Further, the qualifications and conditions for service of the judicial and technical members of the Tribunal have been prescribed in Section 110 of the CGST Act, 2017. However, both of these provisions posed various constitutional challenges. One of the most important of these challenges relates to the composition of benches, where two technical members and one judicial member were prescribed. Further, there were various difficulties caused by the qualifications prescribed for technical and judicial members, such as members of the Indian Legal Service being eligible for appointment as judicial members.

Owing to these difficulties, the constitutionality of these provisions was challenged on the basis of Article 14 and Article 50 before various judicial forums. The Hon’ble Madras High Court, in Revenue Bar Association v. Union of India (2019), struck down various clauses of Section 109 and Section 110. Accordingly, the Finance Act, 2023, substituted both Sections 109 and 110. The amended provisions now provide that a Bench will comprise of four members – two technical members (one from state and one from Centre) and two judicial members. Further, qualifications for both technical and judicial members have also been amended to bring it in consonance with the Indian Constitution.

Offences and Penalties (Chapter XIX)

Section 122 provides for twenty-one different offences. These offences can be categorised and understood with the help of the table below.

| S. No. | Category of offence | Particulars |

| 1. | Fake or wrong invoice | Supply of goods or services without issuing any invoice or issues a false invoiceIssue of invoice or bill without actual supply of any goods or servicesIssues invoices using GST number of another taxable person |

| 2. | Fraud | Submission of fake financial records with an intention to evade taxFailure in providing adequate information or providing false information during proceedings |

| 3. | Tax evasion | Collection of GST from recipients but failure of submitting the same to the government within three monthsObtains a fraudulent refund of CGST/SGSTAvailment/utilization of input tax credit without actual receipt of goods or servicesWillful suppression of sales to evade GST |

| 4. | Supply or transport of goods | Transportation of goods without proper documentsSupply or transportation of goods despite having knowledge that they are bound to be confiscatedDestruction or tampering of seized goods |

| 5. | Other offences | Failure to register under GST if requiredFailure to deduct TDS or deducts less amount than stipulatedFailure to collect TCS or collects less amount than stipulatedTakes or distributes ITC being an input service distributorFailure to maintain proper books of accounts |

For all such offences, penalty is imposed at the rate of 100% of the total tax evaded or at least ten thousand rupees, whatever is higher.

Transitional provisions (Sections 139 and 140)

We have already discussed how a number of taxes were subsumed into GST at the time of its introduction. Accordingly, the rights and liabilities of the assessees under these taxation laws were also required to be transferred into GST. For instance, CENVAT credit accumulated in a taxpayer’s VAT account must be carried forward along with the tax obligations in the GST regime. In furtherance of the same, Section 139 and Section 140 of the Act read with Rule 117 of CGST Rules was introduced.

Section 139 of the Act provides for provisional registration of taxpayers who were already registered under the erstwhile tax laws. This provision is now redundant as such registrations have already taken place. Section 140 relates to transitional credit of the CENVAT amount which was pending in a taxpayer’s account at the time of introduction of GST. The aim of the provision was to ensure a smooth transition of the taxpayers to the GST regime. However, the provision has been in dispute on multiple occasions.

Rule 117 of the CGST Rules provided for furnishing GST TRAN-1 Form and GST TRAN-2 Form within ninety days from introduction of GST. Nevertheless, for the longest time, the GST portal had multiple technical glitches and the forms were regularized only a couple of months. Resultantly, the deadline for filing of both the forms was revised multiple times. Directions were also given by different High Court on various occasions where the taxpayer could not file the form due to technical faults on part of the Government. Finally, the Hon’ble Supreme Court, in Union of India v. Filco Trade Centre Pvt. Ltd. (2022), directed the Central Government to open the portal for one last time and also issue guidelines in such regard. Consequently, Ministry of Finance laid down the guidelines vide Circular No.180/12/2022-GST dated September 09, 2022.

Yet, it is imperative to note that issues regarding transitional credit continue to arise. Taxpayers still knock the doors of the courts as taxpayers still struggle to get their credit while others have accumulated transitional credit which can no longer be utilized by them.

Recent landmark judgments on GST law

Gameskraft Technologies Private Limited v. Directorate General of Goods Services Tax Intelligence (2023)

Gameskraft is one of the recent judgments of the Hon’ble Karnataka High Court which held rummy to be a game of skill. The case gained importance as this was the highest-ever demand made by Revenue in the last six years of GST implementation. The Department issued a show-cause notice on the contention that rummy, being a game of chance, amounted to ‘gambling or betting’ as per Entry 6 of Schedule III of the CGST Act. The Court negated this contention and held that GST could be levied only on the platform fee charged by Gameskraft and not on the entire betting amount.

Yet, it is pertinent to note here that pursuant to this judgment, an amendment was made by the Legislature in the CGST Act which overrided the judgment. In the current scenario, GST is levied on the pooled amount at the rate of 28%. To exemplify this, supposedly, two players put Rs. 1000 each at stake and the gaming company charges 10% platform fee, which in this case would be Rs. 200. Prior to the amendment, GST would be levied at 18% on platform fee i.e. GST would be Rs 36. However, as a consequence of the amendment, now GST would be charged at 28% on Rs. 2000 i.e., 560.

Munjaal Manishbhai Bhat v. Union of India (2022)

In this case, the question pertained to the levy of GST on the sale of land. Entry 5 of Schedule III of CGST Act, 2017 provides that sale of land shall not be considered as a supply of goods or services, thereby no GST could be levied on such a transaction. However, subsequently, Paragraph 2 of Notification No. 11/2017-Central Tax provided that in case of a construction contract where supply involves both sale of land as well as supply of construction services, the value of land shall be mandatorily deemed as one-third of the total value of the total value of supply. Accordingly, the said Notification was challenged based on Entry 5 of Schedule III.

The Hon’ble Gujarat High Court held that such mandatory deeming fiction would be bad in law. There might be cases where the value of land may be more than one-third of the total value of supply and vice-versa as well. Such a situation results in arbitrariness causing violation of Article 14. It goes beyond the purpose of the provision that was meant to be served. Further, the Notification, being a delegated legislation, surpasses the supreme legislation, by levying GST on supply which has been exempted by law itself.

Lastly, the Court held that as regards the cases where the value of both supplies is not distinguishable, the Revenue must resort to the valuation rules (discussed above in Section 15) rather than arbitrarily fixing a particular ratio.

Safari Retreats (P) Ltd. v. Chief Commissioner of Goods & Service Tax (2019)

In this case, the Petitioners were engaged in the construction of shopping malls. In the process, they acquired large supplies of various raw materials and input supplies involving enormous amount. However, by virtue of Section 17(5)(d) of the CGST Act, the Revenue denied input tax credit on these supplies as Section 17(5)(d) provides that no credit shall be given for construction of immovable property. The contention of the Petitioner was that in case of denial of credit, the entire project would be futile and they would run into losses, thereby violating their right to carry on their business under Article 19(1)(g).

Reading down the provision, the Hon’ble Odisha High Court held that credit should be disentitled only if there would not be any further tax incidence to serve the purpose of Section 17(5). The provision intends to cover only those cases “where the immovable property is sold after grant of completion certificate.” However, in the present case, the property would be retained by the Petitioner for letting out the shops on rent and hence, the Petitioner must be entitled to the credit. It is pertinent to note here that the Department has appealed against the decision and the case (SLP No. 26696/2019) is currently pending before the Hon’ble Supreme Court for final adjudication.

Conclusion

The system of taxation of goods and services under GST regime has proven to be a successful step in eradicating the challenges of indirect taxation in India. One of these major challenges was the cascading effect of taxes which was solved by the introduction of the input tax credit. The role of the judiciary has also been commendable in giving effect and deriving proper interpretation to the provisions of the Act. The law gave birth to a beautiful structure namely the GST Council, where both the Centre and states collectively discuss issues pertaining to GST. Lastly, it is hopeful that soon, the GST Appellate Tribunal will also be effective so that the burden of higher courts is reduced and taxpayers are able to adopt a definite tax position.

Frequently Asked Questions (FAQs)

Is registration mandatory under the CGST Act?

Yes, registration is mandatory if any person crosses the prescribed limits as discussed above. However, one may choose for composition levy which is a simple form of registration and is preferable for small-scale businesses.

What is the difference between output GST and input GST?

Output GST is the tax that the taxpayer is required to pay to the government based on his sales. On the other hand, input GST refers to the tax owing to the purchases made by a taxable person which are used in the course or furtherance of the business.

Is CGST levied on all kinds of transactions?

No, CGST is only applicable on intra-state supplies i.e. where the recipient of supply is in the same state. It is levied along with the specific SGST.

Can advance rulings be cited before authorities?

Though there is no prohibition on citing advance rulings of other persons. However, it must be remembered that they are binding only on the taxpayer and officer. Hence, they only have a persuasive value and not binding value before courts and other judicial authorities.

References

- https://gstcouncil.gov.in/brief-history-gst

- https://old.cbic.gov.in/resources//htdocs-cbec/gst/51_GST_Flyer_Chapter4.pdf

- https://blog.saginfotech.com/gst-section-15-value-taxable-supply

- https://www.indiacode.nic.in/bitstream/123456789/15689/1/A2017-12.pdf

- https://cbic-gst.gov.in/pdf/01062021-CGST-Rules-2017-Part-A-Rules.pdf

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications