This article is written by Dreamy Jain, pursuing a Certificate Course in Capital Markets, Securities Laws, Insider Trading and SEBI Litigation from LawSikho.

Introduction

Have you ever thought about having a uniform Know Your Customer (KYC) repository every time you submit your KYC details to banks and financial institutions? A centralized storehouse which can eliminate the process of submitting your KYC documents and in return saving your energy and time, every time you are asked for KYC documents. Well, your thoughts have been turned into reality and if you are still not aware of it, this article will apprise you about Central Know your Customer (CKYC) registry. In this article, I shall be first apprising you with the concept of KYC and why is KYC provided. Then we are going to look at who are reporting entities and what is Central KYC registry. We shall be also discussing types of CKYC account and working of KYC registry.

Central KYC (CKYC) registry acts as a centralized KYC repository which stores information/documents pertaining to a customer who is undertaking a financial transaction or availing a financial service. The Central Registry of Securitization Asset Reconstruction and Security Interest (CERSAI) was incorporated under Section 8 of the Companies Act, 2013 by the Government and later it was given the responsibility of managing the CKYC registry as well. With the objective to promote ease of doing business, the Government formed a CKYC registry which will in turn reduce the cost and burden of maintaining KYC documents by each financial institution or intermediary. Simply stating, when I first started investing in Mutual funds through Systematic Investment Plan (SIPs), I created a dematerialized account with one broking firm and at the time of creating such account, I submitted my KYC documents and till today I can invest in as many mutual funds as I wish (and of course afford) without going through the cumbersome process of submitting my KYC documents to every mutual fund company. This was one of the examples of how CKYC registry works.

What is KYC and need for furnishing KYC documents

Submission of KYC documents for Proof of Identity (POI) and Proof of Address (POA) is mandatory for customers and clients who want to initiate opening of a bank account or undertaking a financial service like opening a dematerialized account or an insurance policy. The main purpose of implementing stringent KYC policies by Government, Reserve Bank of India, regulatory bodies namely Securities & Exchange Board of India (SEBI) and Insurance Regulatory and Development Authority (IRDA) is to prevent money laundering, terrorist financing, financial fraud, evasion of taxes and identification of the customer/client. The following are the KYC documents which are accepted “Officially Valid Document” (OVD) as per RBI circular:

- passport,

- driving license,

- proof of possession of Aadhaar number,

- voter’s Identity Card issued by the Election Commission of India,

- job card issued by NREGA duly signed by an officer of the State Government, and

- letter issued by the National Population Register containing details of name and address.

Apart from the above listed documents, proprietorship firm/partnership firms/Hindu undivided family (HUF) and companies are required to give additional documents but not limited to the following:

- Trade License,

- Shop & Establishment registration certificate,

- Pan card of HUF, partnership firm, Company,

- Partnership Deed,

- Memorandum of Association,

- Articles of Association,

- Board Resolution/Power of Attorney authorizing the employees to sign documents,

- Identification of Ultimate Beneficial Owner (UBO).

Who are reporting entities and their role in Central KYC registry

The reporting entity is defined in Section (wa) of Prevention of Money Laundering Act, 2002 means a banking company, financial institution, intermediary or a person carrying on a designated business or profession.

An intermediary means a stock-broker, sub-broker, share transfer agent, banker to an issue, trustee to a trust deed, registrar to an issue, merchant banker, underwriter, portfolio manager, investment adviser or any other intermediary associated with the securities market.

The reporting entities are required to be registered with CKYC registry and after obtaining a registration, they shall undertake customer verification and initial due diligence while creating an account based relationship. They are also obligated with the responsibility of updating the details of clients if there is a change in the existing records of the clients.

A client can check the status of their KYC status by visiting the website of https://www.cvlkra.com/ and providing a PAN number.

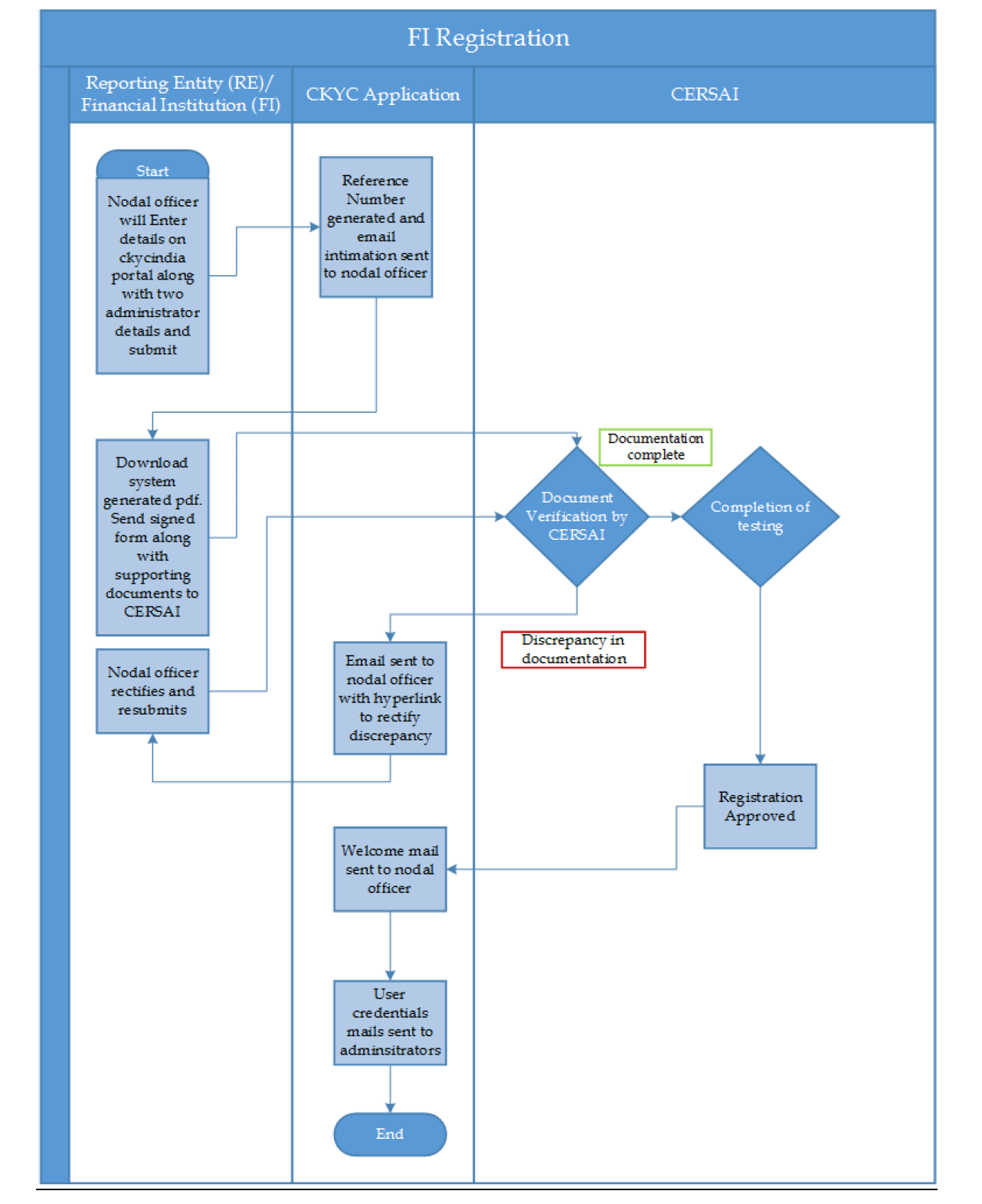

The following is the process of reporting entity registration with CERSAI:

Source: Central KYC Registry Operating Guidelines 2016

What is Central KYC (CKYC) registry and how does it work

As stated earlier CKYC registry has been formed to maintain the records of KYCs in the form of a central repository and eluding the burden of resubmitting KYC documents repeatedly for undertaking financial transactions. Once KYCs are submitted to the reporting entity registered with CERSAI, the reporting entity will upload the details along with supporting documents on the CKYC portal. A CKYC identifier which is a 14-digit unique number, will be provided to the registered customer/client which can be quoted by them to other financial institutions. Since it is a centralized repository, financial institutions have access to the KYC records and one need not be asked to submit their KYC documents for initiating a financial transaction if they are registered. The reporting entity can search and download KYC details using the CKYC identifier if quoted or by entering a valid ID type and number. Thus with the help of the reporting entities, the CKYC registry is being operated and fostering its objective of minimum burden of documentations and ease of doing financial transactions.

The form for registration with the Central KYC registry can be found on various reporting entities and a sample form can be assessed from this link http://portal.amfiindia.com/spages/CKYC-KRA-KYC-FormforIndividuals.pdf

Different types of CKYC accounts

The CKYC accounts are classified into the following types of accounts which are as mentioned below:

- Normal KYC account- In this type of account, the KYC submitted are among the 6 Officially Valid Documents (OVD) as per RBI which are also mentioned above.

- Simplified or Low-Risk KYC Account- Here, the customer cannot provide any document out of the 6 OVDs mentioned and are marked ‘low risk’ by the reporting entities. However, they have to provide any of the following:

- A proof of identity with photos issued by state/central government departments, public sector undertakings (PSUs), statutory/regulatory authority, public financial institutions and scheduled commercial banks.

- Letter with a duly attested photo of the person issued by a gazetted officer. Such types of accounts will have a prefix ‘L’ to it.

- Small accounts- In these types of accounts, the customer is not holding any valid identity proof but can open the account by providing a self attested photograph and signed application with the condition that they shall provide a valid proof of identity and address within a year or a proof of their application for a valid document. These accounts are prefixed with ‘S’ and can be operated with several restrictions on their withdrawals, account balance and credits.

Recent amendments in law

Prevention of Money-laundering (Maintenance of Records) Rules, 2005 were amended on 19th August, 2019 and are called the Prevention of Money-laundering (Maintenance of Records) Third Amendment Rules, 2019. In this amendment, Digital KYC has been introduced and its process has been provided which shall be part of the Prevention of Money Laundering Act, 2002. As per the Act, “digital KYC” means the capturing live photo of the client and officially valid document or the proof of possession of Aadhaar, where offline verification cannot be carried out, along with the latitude and longitude of the location where such live photo is being taken by an authorised officer of the reporting entity as per the provisions contained in the Act. It has also mentioned digital signatures but it has not yet allowed digitally signing of documents instead, physical signatures are still in place.

Conclusion

The above amendment and having CKYC in place are positive beginnings through major reforms are needed of the hour in our legislature, to promote digitalization and having a Centralized KYC registry can be termed as a stepping stone for those reforms. We are hopeful that more such reforms will take place in our near future as we all witnessed the repercussions faced due to a pandemic and how digitalization made banking/financial transactions easier, which was under a pile of paperwork for even carrying out small monetary transactions!

References

Central KYC Registry Operating Guidelines 2016, Version 1.1.

Prevention of Money-Laundering (Maintenance of Records) Third Amendment Rules, 2019.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications