")

This article is written by Hanumant Rambihari Chauhan, pursuing a Diploma in Advanced Contract Drafting, Negotiation, and Dispute Resolution from LawSikho.

Table of Contents

Introduction

Since the very beginning of the 21st century, over 800,000 transactions have taken place worldwide with a known value of over 57 trillion USD. Since 2018, the quantity of deals in M&A has declined by 8 per cent to 49,000 transactions, while their worth has increased by 4 per cent to 3.8 trillion USD. The reason behind this can be attributed to mergers and acquisitions with other business entities in order to gain augmentation in a province or market, increased access to the customer base, obliterating a competitor or an anchorage economy of scale. While entering into agreements of merger and acquisition, sellers inevitably are going to make mistakes. Through this article, the author seeks to highlight the common mistakes made by sellers in M&A.

Mentioned in the ensuing paragraphs are the common mistakes that sellers end up committing while making M&A deals.

Not having an appropriate NDA

The M&A process requires extensive disclosure, so a well-drafted non-disclosure agreement (NDA) is crucial to protect the seller’s proprietary company information and a ‘well-drafted’ NDA means that it includes specific M&A-related protections for the seller.

It is of importance to include clauses needed around potential buyers not being able to contact the seller’s customers, suppliers and employees. Incredibly good NDAs, as essential as they are, are often not thought about much in a rush to sell. A well-developed offer contains several barriers for the buyer. In particular, a restriction in the form of a ban on poaching or hiring the seller’s employees for a certain time period, non-disclosure of essential data, amongst others.

Not having an entire online data room

An “online data room” is a warehouse of key documents about a company. Online data rooms are used in merger and acquisition transactions, to facilitate the extensive due diligence process typically undertaken by buyers.

This data room is crammed with the company’s important documents: contracts, intellectual property information, employee information, financial statements, capitalization tables, and much more, basically anything that the buyer might need to access. It allows the selling company to furnish valuable information in a systematic manner, which aids in preserving confidentiality and promotes efficiency. Such data rooms avoid the use of a physical data room where documents are kept and helps quicken M&A procedures. Thus, the preparation of an online data room is extremely important for an M&A transaction.

Even though creating an online data room is very time consuming as one has to put all the information and financials in it, it is of utmost importance to set up early on in M&A transactions. It is one of the key factors behind M&A success.

Not negotiating the terms of the financial advisor or factor engagement letter

Companies usually take on financial advisors or investment bankers for capital fund-raising and M&A activities, and these investment bankers or financial advisors are valuable partners for companies.

An investment banker or financial advisor strives to start the negotiation with their purported ‘standard form’ letter, this letter is mostly one-sided in favour of the investment banker or financial advisor. It is valuable to see a particular description of the services to be furnished in the engagement letter. The companies that just sign this engagement letter or hardly negotiate such a letter are making a huge mistake. This letter is negotiable and legal counsel/deal professionals negotiate it.

- Negotiate the percentage payable as compensation to the advisor generally as “success fees” based on the ultimate sale price percentage. (The amount of the fees will ordinarily range from 1% to 3% of the net consideration received from the sale.)

- Many engagement letters will have a tail obligation by the company. Under what situation and how long a ‘tail’ applies, companies try to limit this tail between 6 to 9 months and only for potential buyers who have signed an NDA with the company while signing the engagement letter.

- Representation and warranty regarding any quarrel of interest by the investment banker or financial advisor.

Having incomplete books, records and contracts

Usually, companies have incomplete files with contracts, minutes, stock option information, corporate records, etc. Acquirer insists on checking all the record books and contracts of selling the company for due diligence purposes. The acquirer spends a great deal of time and due diligence on the company’s projections. So, those projections must be equitable and sensible with realistic assumptions. Preferably, an updated online data room should be kept by the company in advance. Preparation of such records at the eleventh hour is difficult and tedious and can lead to mistakes, and therefore, it should be started at the earliest in the process as it can lead to delays in the transaction of M&A.

Not having a whole disclosure schedule

As a prevailing party of any M&A transaction, the seller should prepare an all-inclusive disclosure schedule that labels many of the key diligences and recognizes any exceptions to the seller’s representations and warranties in the acquisition agreement. This disclosure schedule must be carefully prepared as it is immensely important and time-consuming for the seller. The seller’s management team needs to be sharply involved in the drafting of the disclosure schedule. The buyers and their legal and financial advisors negotiate the wording of the disclosure agreement. Also, the seller has no right to update the disclosure schedule after signing and before closing.

Not negotiating the key terms of the deal in a letter of intent

One of the significant mistakes made by the seller is not negotiating the terms of the letter of intent. There should be a clear consensus on the principal terms and conditions in the letter of intent (LOI). Considering that the LOI is not signed, the seller can expedite the bargain and dictate his terms. Once it is signed, the ball is in the investor’s court where he can demand oneness; restricting the buyer from negotiating with other investors for a certain time period. The LOI should include the price and payment method and the apparatus for price correction; also, the scope and duration are of utmost importance alongside the remedies for breach of the agreement, etc.

A bewildering letter of intent (LOI) notably speeds up the duration of the transaction and increases the likelihood of its successful completion.

Not having a decent legal advisor for M&A transaction

As preparations commence in anticipation of a sale, it is critical to bring in the right professionals to help facilitate the deal. Trying to navigate the intricacies of this kind of sale without the requisite skills, knowledge, and expertise on board might affect the sale adversely and therefore, it is vital to hire experts wisely. It is essential for the selling of the company to hire an advisor who specializes in M&A transactions for the success of the M&A process. It is vitally important to have an experienced M&A negotiator leading the negotiation to avoid acrimonious negotiation, as this could kill the deal.

The legal team is obliged to have experts in the relevant areas, such as fiscal, real estate, intellectual property, jurisdiction, administrative etc. Also, an M&A lawyer must be amicable with the company’s business and with the operations of an M&A deal. The legal advisor helps the seller’s team to upload the information of company’s business information to the data room “also, assists” in price negotiation and other terms of the transaction.

Dispute resolution provisions in M&A deals

The M&A agreement must set out how and where dispute resolution will take place. Although most of the acquisition agreements backtrack to the court system, numerous sellers and buyers, especially those who have been through dispute processes, usually prefer to resort to an absolute confidential binding arbitration provision. which allows for quicker and more cost-effective resolution compared to litigation. Litigation lasts for many years throughout the appeal process and is extremely costly, and it is, therefore, preferable to find an alternate dispute resolution mechanism like arbitration, for example.

Amidst the issues to be considered for arbitration, the following things have to be decided prior to finalisation of the deal:

- Number of arbitrators.

- Location of arbitration.

- The time period for issuance of a decision.

- How parties will hold up the fees and arbitration expenses.

Conditions to the closing of the M&A deal

If a delay occurs between signing and closing, the acquisition agreement will need to chart the conditions for closing, both concerning the buyer and the seller. Some of these conditions are akin, but most of them are incomparable to one party or the other.

The common closing conditions that run in favour of the buyer are

- Accuracy in the material respects of the seller’s representations and warranties in the agreement.

- The obedience by the seller with the seller’s covenants in the acquisition agreement.

- To get the approval of all the necessary government consent.

Representations and warranties regarding contracts in M&A deals

The representations and warranties clause of the acquisition includes a key section concerning the seller’s contracts, and especially, the subject matter of the contracts with the sellers as mentioned in the agreement. Before signing the acquisition agreement, the contract will be made available to the buyer and their counsel in the “online data room”. This section generally requires a listing of all the material contracts of the seller which are:

- Completion bond,

- Joint venture and partnership agreement,

- Intellectual property related-agreement,

- NDA or confidentiality agreement,

- Guarantees of third-party agreement,

- Other material agreements.

Failure to list the essential contracts in the schedule could allow the buyer to walk away from the deal before closing which would lead to possible post-closing liability for the seller’s stakeholders.

Current samples of where M&A transactions failed

It’s gripping how many unfavourable M&A transactions fail all the time for various reasons. Let us focus on a couple of examples to gain an insight into the same.

1. HDFC and Max Life

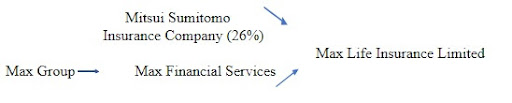

Shareholding patterns

Max life Limited being India’s Fourth largest private insurance underwriter, a Venture between Max Financial Services and Mitsui Sumitomo Insurance Company (26%), a Japanese Insurance Company.

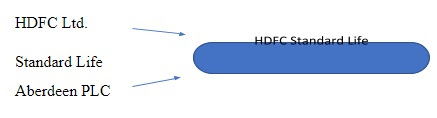

HDFC Standard Life Insurance within the past unlisted company and a joint venture between (HDFC) Housing Development Financial Corporation Limited holding 61.5% shares and Standard Life Aberdeen PLC, holding 35% merger of Standard Life and Aberdeen Asset Management rest by others.

Merger structure and advantage

HDFC was a Private Company and ought to get listed. The merger would list it automatically without going through the route of unwieldy Initial Public Offering. The merger was not the only advantage with regards to avoiding the intricacies of an IPO but would cut down the cost significantly. It was a reverse merger as a listed company was to be merged with non-listed, (HDFC Standard Life was going to merge in Max life Limited).

As per the plan, Max Life Limited would first merge with its parent company Max Financial Services, and later, the life insurance business would de-merge from Max Financial and get merged into HDFC Life. The majority stake in the combined entity was to be held by HDFC Life.

Reason for failure

The proposed merger was not approved by the sectoral authorities, Insurance Regulatory and Development Board (IRDB). Section 35 of the Insurance Act bars the merger of the insurance company with non-insurance companies.

2. eBay and Skype (2005)

Another such example of failure in M&A transactions was eBay’s acquisition of Skype. The concept was that this merger would allow communication between buyers and sellers on eBay, bring about gentle transaction flow and generate more revenue.

But eBay didn’t bargain with the people who didn’t want to talk to a stranger about the transaction if they could just email them. Soon, eBay came to know that there was no real need for the acquisition and ended up selling 2/3rd of Skype for the US $1.9 billion four years later.

Conclusion

The procedure of selling a company or acquisition requires much more than assent on a price. There are numerous aspects to negotiating different clauses in the acquisition agreement. Advice is not to let things take their own course and endow the sales process with the adeptness to account the supposition and make transactions well organized and tight.

An M&A transaction ordinarily requires counsel, advisors, and accountants of the buyer and seller to take on a notable amount of due diligence. The seller, by being duly prepared for due diligence activities, can ensure that the procedure goes smoothly and swiftly, helping the best interests of all parties to the transaction.

Reference

- https://www.allbusiness.com/a-comprehensive-guide-to-due-diligence-issues-in-mergers-and-acquisitions-120837-1.html

- https://www.allbusiness.com/9-key-ways-to-prepare-for-an-ma-transaction-5363-1.html

- https://www.forbes.com/sites/allbusiness/2016/06/24/negotiating-investment-banker-engagement-letters/?sh=2088d3d66120

- https://www.forbes.com/sites/allbusiness/2020/07/03/negotiating-merger-and-acquisition-agreements-for-technology-companies/?sh=7129d8a3ad1d

- https://imaa-institute.org/mergers-and-acquisitions-statistics/

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications