This article is written by Seerat Kaur, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from lawsikho.com.

Table of Contents

Introduction

A merger occurs when two companies voluntarily form a fusion on broadly equal terms, resulting in a single legal entity. It is a combination of two companies to create a new company, usually by mutual agreement. While the terms ‘merger’ and acquisition are used together a lot of times, they are not the same. An acquisition deals with a single company buying and subsuming other companies to expand its dominance. At the same time, a merger deals with two companies combining to form a new company, to enhance the financial and operational strength of both the entities. Mergers can happen for several reasons and by a number of ways. The following are the five basic categories of mergers;

- Horizontal Mergers: A merger that takes place between companies that are in linear competition with each other in terms of the product and market both.

- Vertical Merger: A merger between companies that are involved in different stages of a supply chain of a common product or service.

- Market-extension Merger: A merger between companies that are present in a different market, but sell similar goods.

- Product – Extension Merger: A merger between companies that are present in the same market, but sell different, yet related goods

- Conglomerate Merger: A merger between companies in business activities that are unrelated to each other.

The type of merger is chosen based upon the aim of both the companies. A merger often involves a transfer of ownership, either through cash payment, or stock swap. Mergers tend to result in a direct or indirect increase of financial strength or brand value of the entities.

Role of NCLT in a merger

The Companies Act 2013 (New Act) includes the provision of setting up National Company Law Tribunal (NCLT) and gives it the power to assume jurisdiction of High courts for sanctioning M&A deals. The aim of this provision was to ensure fairness and effective overseeing of the deals. All mergers have to be carried out in accordance with the Companies Act, 2013. Section 230, 231 and 232 are the essential sections that provide the role of CLTs in mergers.

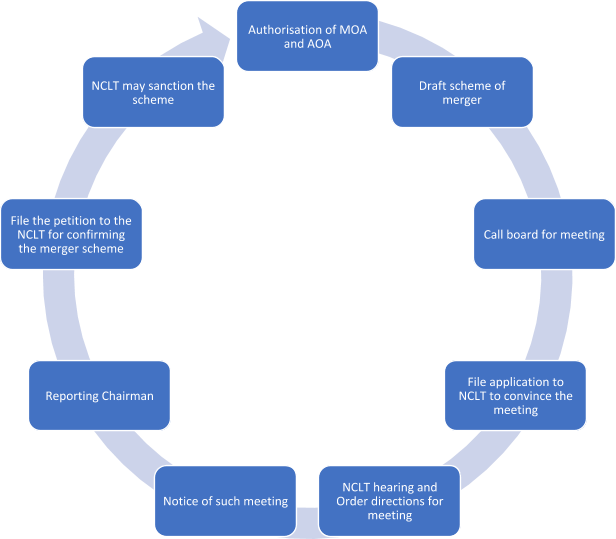

Checklist for NCLT approvals

The checklist for NCLT approvals consists of the following:

Authorisation of MOA and AOA

A Memorandum of Association is a legal document that is prepared during the formation and registration process of a company, it defines the objectives behind the formation of the company and its relationship with the shareholders. Article of Association, on the other hand, is a document which along with the MOA, forms the company’s charter and defines the various responsibilities. This step includes checking if the memorandum and AOA allow the company to have mergers. If it does not, then it would be necessary to amend the object clause to include the same.

Draft scheme of merger

The next step is to formulate and prepare the Draft of the scheme of merger between the transferor company and the transferee company. It would include various clauses containing details about the transferor of Company. For the transferee company, the scheme would include an Introductory part, Operating part and the Prayer/relief. The Introductory part would include the basic details of the transferor and transferee company like date of incorporation, the Corporate Identification Number (CIN), registered office and address for service of notice and the main objects in the MOA and AOA along with the jurisdiction of bench/limitation and definition clauses, ‘facts of the case’ which provides for the reason behind the merger and the nature of business/share capital of the companies involved along with the shareholding relationships. The Operating part would include the appointed date/transfer of undertaking, transfer of assets, debts and liabilities, licenses, company’s staff, workmen and employees, contracts of transferor company along with the enforcement of deeds, bonds legal proceedings and issuance and allotment of shares and the accounting treatment. Last but not the least, the Prayer/Relief part will comprise of the Approval of the scheme along with the particulars of the bank draft evidencing the payment of a fee for the said application.

Call board for meeting

In this step, the notice for a meeting to discuss the merger needs to be sent at least 7 days before the date of meeting as per section 173(3) of the Companies Act, 2013. Once the board meeting of both the transferor and transferee company is held, it is eminent for a resolution consenting the merger to be passed. After this is done, the draft of the scheme will be considered. Besides approving the merger, the resolution should also authorize a director/Company secretary to make an application to the Tribunal. This step will also involve the appointment of an independent registered valuer for valuing the shares to determine the share exchange ratio.

File application to NCLT to convene the meeting

The application for the merger needs to be sent to NCLT as a petition submitted through Form No. NCLT-1, along with an attachment of the notice of admission in Form No. NCLT-2, an affidavit in Form No. NCLT-6, a copy of the scheme of compromise and arrangement will include the required disclosures as per section 230(2) and the fee as prescribed in the schedule of fees. It is important to include the latest financial position, auditors report, the pendency of any legal proceeding, reduction of the share capital of the company and scheme of corporate debt restructuring (CDR) if any.

NCLT hearing and order directions for meeting

Upon hearing the application, the tribunal may, unless it thinks fit for any reason to dismiss the application, give such relevant directions for conducting a meeting of the creditors or class of creditors or of the members or class of members as per rule 5 of Compromise Arrangement and Amalgamations, 2016.

Notice of such meeting

A notice of the meeting is then sent to all the creditors/class of creditors or members/class of members and debenture holders of the company, in Form no. CAA-2 by post or courier or email or hand delivery, or any other method as directed by the Tribunal to their last known address at least one month before the date fixed for the meeting. The notice for the meeting to the creditors and members needs to be accompanied by a copy of the scheme of compromise and arrangements, if the same are not already included in the said scheme under rule 6 of the Compromise, Arrangements and Amalgamations, 2016. The scheme of compromise or arrangement has to be approved by the members of the company or the members of each class, if the company has different classes of shares and the creditors or each class of creditors, if the company has different classes of creditors.

The notice is required to be given in the prescribed form and advertised in Form No. CAA-2 in at least one English newspaper and one vernacular newspaper having a prevalent circulation in the state in which the company’s registered office is present. A copy of the notice shall also be placed at least 30 days before the date fixed for the meeting on the company’s website. This notice, along with the scheme of compromise and arrangement and the explanatory statement, shall also be sent to the Central Government, the income tax authorities, the Reserve Bank of India, the Registrar of Companies, the Official Liquidator, the Competition Commission of India and other such sectoral regulators or authorities which are likely to be affected, as per FORM CAA-3. If any of these mentioned authorities wish to make any representations, then the same needs to be sent to the Tribunal at least 30 days from the date of receipt of the notice and the copy of these representations needs to be simultaneously sent to the concerned companies.

Reporting chairman

The chairman who has been appointed by the Tribunal, for the purpose of the meeting of the company has to file an affidavit before the Tribunal at least seven days before the date fixed for the meeting or the date of the first meeting, stating that the directions regarding the issue of notices and the advertisement have been duly complied with. The scheme is said to be approved in the meeting when a majority of the persons representing three-fourths in value of the creditors, or class of creditors or members or class of members, voting in person, or by proxy or by postal ballot, agree to it. Then it is the duty of the chairman to, within the time fixed by the Tribunal, or where no time has been fixed, within 3 days after the conclusion of the meeting, submit a report to the Tribunal on the result of the meeting in Form no CAA-4.

File the petition to the NCLT for confirming the merger scheme

The company shall, within seven days of the filing of the report by the chairman, present a petition to the Tribunal in Form No CAA-5 for the sanction of the scheme of merger. A notice of this hearing should be published in the same newspapers in which the meeting was advertised, within not less than 10 days before the date fixed for hearing (Rule 16). An order of the Tribunal on summons for directions should also be obtained and will be enclosed in Form No CAA-6 (Rule 17). The notice of hearing shall also be served to the representatives or objectors under section 230(4).

NCLT may sanction the scheme

The Tribunal may then either sanction the arrangement or not. If sanctioned, the order shall include directions in regard to any matter or modification in the merger as the tribunal may think fit to make the proper working of the merger. The order shall be in Form No CAA-6, with any variations as may be necessary. As per the Companies Act, 2013 the order shall direct that a certified copy of the same shall be filed with the Registrar of the Companies along with the INC-28 within 30 days from the date of receipt of a copy of the order, or any such time as fixed by the Tribunal.

Conclusion

The request of a specific tribunal was introduced by the Hon’ble Supreme Court of India in the judgment of S.P. Sampath Kumar v. Union of India where Hon’ble court held that the number of inhabitants in India has been continually expanding and so is the weight on courts to take up the issues. A report exhibited by the Shah Committee in connection with specific tribunals also said that there is a critical need to modify the laws in connection to setting up of an autonomous tribunal in light of over abundance of cases under the steady gaze of the courts. The companies Act, 2013 has ensured provisions that provide for a single consolidated forum in the form of the National Company Law Tribunal (“NCLT”), for all the merger and de-merger schemes. This ensures a smooth and quick mode of executing mergers. Having NCLT look after mergers also guarantees a level of transparency which is important in today’s times where mergers and de-mergers are a sought after panacea for corporate turbulence. Having a proper procedure also gives impetus to foreign companies in exploring business relationships in India, thus opening up a gateway for more foreign investments. NCLT is an important part of the regulatory framework that revolves around these corporate tools. The procedure involved is very simple and to the point, it also upholds the true spirit of rule of law by ensuring that all stakeholders are made aware of the scheme and any rising contentions are given a stage. The formation of these tribunals has marked a positive paradigm shift in the corporate restructuring process.

References

- https://nclat.nic.in/?page_id=113

- https://nclat.nic.in/?page_id=113

- http://www.mca.gov.in/MinistryV2/mergers+and+acquisitions.html

- https://acadpubl.eu/hub/2018-120-5/1/18.pdf

- https://www.mondaq.com/india/corporate-and-company-law/503156/constitution-of-nclt-and-nclat-a-new-era-of-company-law-litigation-in-india

- https://taxguru.in/company-law/procedure-merger-nclt.html

- http://www.singhanialaw.com/mergers_and_acquistion.php

- https://mnacritique.mergersindia.com/nclt-impact-ma-procedure/

- https://www.investopedia.com/terms/v/verticalmerger.asp

- https://corporatefinanceinstitute.com/resources/knowledge/deals/types-of-mergers/

- https://blog.ipleaders.in/role-of-nclt-in-fast-track-merger/

- https://corporatefinanceinstitute.com/resources/knowledge/deals/types-of-mergers/

- https://www.investopedia.com/terms/m/mergersandacquisitions.asp

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications