This article is written by Mokshiv Malla and Dhruv Singhal, students of Rajiv Gandhi National University of Law, Patiala, Punjab. In this article, the authors have analysed the composition scheme under the Goods and Services Tax with all the advantages and disadvantages.

Table of Contents

Introduction

One of the quintessential elements for working of an economy is the tax structure of the nation. Tax is collected from general public by the government to provide basic facilities like Infrastructure, Transportation, Shelter, Education, Food and other goods and services for the common good of all. Tax can be said to be a compulsory transfer of money from “Persons” to government. Taxation system is important for an economy because it is fundamental equipment which helps in removing poverty of the country and a strategic taxation system will lead to holistic growth of the economy. In India we follow Progressive Taxation System. It means rich people will be charged more tax and poor people will be charged with very less tax or no tax, depending on their income. Person aforementioned is the person registered under the Act.

Two types of taxes are levied in India:

- Direct Tax;

- Indirect Tax.

There are various distinctions between these two taxes. However, both are directly or indirectly collected from general public. Some of the important distinctions are:

- Direct tax is paid by the person himself to the government on the basis of their income. Indirect taxes are transferable where liability to pay has been shifted to others in the course of transaction.

- Direct Taxes are completely dependent on the individual income of the person. More Income – High Tax. Indirect tax is not dependent on individual income.

- Direct Taxes are imposed on income or profits. Indirect Taxes are imposed on goods and services.

So, Indirect Taxes are those taxes levied by the Government on goods and services and not on the income and profit of the person and can be shifted from one taxpayer to another. Some of the examples of Indirect taxes are Customs Duty, Central Excise Duty, Service Tax, Sales Tax, Value Added Tax etc.

With the objective of “One Nation, One Tax, One Market” Goods and Service Tax were introduced and implemented by the Government with effect from 1st July 2017. Goods and Service Tax (hereinafter referred to as GST) subsumed almost all indirect taxes into one tax called GST. The quintessential benefit of GST is the removal of cascading effect (tax on tax) by providing input tax credit after each stage of production nationwide. GST is a “destination based consumption tax” collected on value-added at each stage of supply chain. Input Tax Credit will be provided to all registered purchaser until it reaches to the unregistered purchaser, composition dealer or ultimate consumer.

To empower the Central and States government to impose tax under GST regime five legislations were passed by the Government, which includes:

- The Central Goods and Service Tax Act, 2017;

- The Integrated Goods and Service Tax Act, 2017;

- The State Goods and Service Tax Act, 2017;

- The Union Territory Goods and Service Tax Act, 2017;

- The Goods and Service Tax (Compensation to States) Act, 2017.

India has adopted and implemented, dual model GST whereby both Centre and States concurrently imposed and collect tax equally on any transaction, where the transaction occurs only in a specific state. However, if the transaction occurs between or among two or more than two states tax is collected by the Central Government and half of the tax will be distributed to that State Government where that Goods or Services have been ultimately consumed. If the transaction occurs in a specific or between or among two or more Union Territories then UTGST will be charged and whole tax will be imposed, collected and used by the Central Government alone.

Complying with the provisions of GST is too complex and costly. However for the holistic development of the economy and to remove cascading effect on goods and services, introduction of GST is utmost important. Small Businesses finds it very difficult to comply with complex formalities under the Act and for this reason Section 10 has been added in the Act with the objective to provide simplicity and reduced compliance cost for small businesses. This project analyze provisions relating to the Composition Scheme, Advantages and Disadvantages attached with the scheme and try to analyze difference between normal scheme and composition scheme. However, for proper understanding of Composition Scheme in GST two definitions are very important to understand.

Input Tax Credit

Arrival of GST streamlines the process of claiming Input Tax Credit. Input Tax Credit or ITC means the tax that a business pays on a purchase and that it can use to reduce its tax liability when it makes a sale. In simple words it means Businesses can reduce their tax liability by claiming credit to the extent of GST paid on purchases.

Reverse Charge Mechanism

To avail the benefits of GST, the supplier is compulsory required to be registered. However there are circumstances where supplier is not registered but the recipient is registered. Since supplier cannot issue tax invoice, the recipient pays GST on supply on behalf of the supplier, directly to the Government. This concept is reverse charge mechanism.

Detailed Analysis of Composition Scheme Under GST

As discussed above, GST though helpful for the holistic development of the economy and beneficial in the long run, it brings some disadvantages for the registered businesses. One such disadvantage is to comply with various provisions of the GST Act and to file 3 returns every month which will lead to heavy increase in the operational cost. If the threshold limit which is 20 Lakh or Rs. 10 Lakh (in special category States) is crossed, businesses are required to be compulsory registered. Small businesses (if turnover is more than 20 Lakh) are compulsory required to be registered and this will lead to increase in there operational cost as the compliance in GST is too complex and costly. To avoid the unnecessary hardship for small businesses GST Act has introduced Section 10 in the Act which provides for Composition Scheme. Composition comes from a Latin term “Componere” meaning “put together”. It provides a gateway to small businesses in order to provide comfort to registered taxable person from maintaining details of input and output and by charging very small percentage of tax which range from 1% to 6% depending on the commodity. So, composition scheme has been inserted in the Act with the objective to provide simplicity and reduced compliance costs for small businesses. Act provides that composition scheme is optional and for this reason business that opt for the scheme can pay tax at a prescribed percentage of his turnover without being involved in the compliance of normal scheme.

Prescribed threshold limit to opt for Composition Scheme

Section 10 of the CGST Act, along with the rules and notification published by the government from time to time, provides for levy of composition scheme. It provides threshold limit for those businesses that can opt for composition scheme. Section 10 provides:

a registered person, whose aggregate turnover in the preceding financial year did not exceed fifty Lakh rupees, may opt to pay, in lieu of the tax payable by him at composition rate.

However Government by exercising its power under Section 10 and considering the needs of the business community issued 3 important notifications regarding the threshold limit. These are:

- Notification No. 8/2017 dated 27th June 2017

Central Government via this notification has increased the threshold limit from 50 Lakh to 75 Lakh considering the needs and demand of the business community.

- Notification No. 46/2017 dated 13th October 2017

Central Government further increases the threshold limit from 75 Lakh to 1 crore considering the demands and needs of the business community. For special category states, except State of Jammu and Kashmir, specified in Article 279A (4) (g) [Arunachal Pradesh, Assam. Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand] threshold limit has been increased from 50 Lakh to 75 Lakh.

- Notification No. 14/2019 dated 7th March 2019

Central Government further increase the limits from 1 crore to 1.5 crore. However for special category states specified above limits are not changed. This notification came into force from 1st April 2019.

So for registration under the scheme, aggregate turnover must not be more than Rs. 1.5 Crore in all States except special category States. For special category States this limit is Rs. 75 Lakh.

Since the person registered under Composition Scheme cannot issue Tax Invoice, he can neither permitted to collect any tax nor can he avail any input tax credit. Also the person registered under the composition scheme has to pay specified percentage of tax on their aggregate turnover. Aggregate turnover has been defined in Section 2(6) of the CGST Act. It provides:

Aggregate turnover is the sum of:

- Taxable Supplies;

- Exempt Supplies;

- Zero-rated Supplies;

- Inter-state Supplies.

Supplies on which tax is paid through Reverse Charge basis are excluded from the definition as this would lead to an increase in the turnover of the supplier without even making any sale.

Rate of Tax in Composition Scheme

The prescribed category of persons who are eligible to opt for composition scheme has to pay tax on the basis of their aggregate turnover of a fixed percentage amount. Section 10 of the CGST Act prescribed percentage of aggregate turnover that is required to be paid in lieu of payment of tax. Act prescribes:

“(a) one per cent. of the turnover in State or turnover in Union territory in case of a manufacturer, (b) two and a half per cent. of the turnover in State or turnover in Union territory in case of persons engaged in making supplies referred to in clause (b) of paragraph 6 of Schedule II, and (c) half per cent. of the turnover in State or turnover in Union territory in case of other suppliers”

However vide Notification No. 01/2018 dated 1st January 2018, CBEC reduced GST rates for manufacture from 1% to 0.5% on its aggregate turnover.

Since we have adopted dual model GST, both Centre and State can collect equal amount of tax from registered person. This means that equal percentage of tax as aforementioned has to be paid both to the Central Government and the State Government. Below mentioned table will be helpful to understand this concept.

|

S. No. |

Composition Dealer |

CGST Rate |

SGST Rate |

Total Tax Rate |

|

Manufacturers |

0.5% |

0.5% |

1% |

|

Restaurant Services (Suppliers for food or drink for human consumption other that alcoholic liquor) |

2.5% |

2.5% |

5% |

|

Traders |

0.5% |

0.5% |

1% |

Persons who are involved in the supply of services are not eligible to opt for composition scheme. This creates a problem for those businesses whose principal business is to supply goods but involved in some kind of supply of services as well. To safeguard the interest of these kinds of businesses a Proviso was added in Section 10(1) by Amendment Act 31 of 2018. The said proviso provides:

“Provided further that a person who opts to pay tax under clause (a) or clause (b) or clause © may supply services (other than those referred to in clause (b) of paragraph 6 of Schedule II) of value not exceeding ten percent of turnover in a State of Union Territory in the preceding financial year or five Lakh rupees, whichever is higher”

This means that if the person is involved in the supply of services of value not exceeding 10% of turnover in the preceding financial year or Rs. 5 Lakh in the preceding financial year, whichever is higher, can opt for composition scheme notwithstanding he is involved in the supply of services.

Eligible Person to avail Composition Scheme

Section 10(2) of the CGST Act provides for those categories of persons who are eligible and can opt for Composition Scheme. This section provides a negative list of persons who are not eligible to opt for composition scheme. List includes:

- Person engaged in supply of service except as provided in sub-section 1 of section 10 or proviso of section 10. That means if registered person is involved in supply of services of more than Rs. 5 Lakh or in any business other than Restaurant Business, he is not eligible to opt for composition scheme.

- Persons who are engaged in supply of goods which are not subject to tax under this Act for example petroleum products.

- Person engaged in making inter-state outward supplies of goods. That means businesses [if engaged in supplying goods in different states (other than their registered state)] are not eligible to opt for composition scheme.

- Person is engaged in making any supply of goods through an electronic commerce operator who is required to collect tax at source under Section 52 of CGST Act.

- Person is either a casual taxable person or a non-resident taxable person. These persons are not permanently registered in that particular State.

- Person is engaged in manufacturing of those goods as may be notified by the Central Government on the recommendation of the council.

Central Government via Notification No. 8/2017 dated 27th June 2017 has specified goods manufacturers of which are not eligible for composition scheme. These products are:

- Ice cream and other edible ice products;

- Pan Masala;

- Tobacco and manufactured tobacco substitutes.

All these persons are not eligible to opt for composition scheme. Other than this rule 5 of the Central Goods and Service Tax Rules, 2017 also provides that to be eligible to opt for composition scheme Goods held in stock on the appointed date must not be

- Purchased in the course of Inter-state trade or commerce.

- Imported from the place outside India.

- Received from its branch outside India.

- Received from his agent or principle outside India.

Proviso to Section 10(2)(f) further provides that to avail the benefits of composition scheme all entities registered under Single PAN must opt for the scheme.

By the Amendment Act 23 of 2019 Sub-section (2-A) was added in the CGST Act to cover all those cases where a person is not covered under Section 10(1) or Section 10(2). This Sub-section is added in the Act with the objective to cover the cases which are not covered earlier and to provide benefits to all those businesses whose turnover is more than Rs. 20 Lakh but less than Rs. 50 Lakh, as the case may be. Now because of this provision all those persons whose turnover are less than aforementioned limit but not covered by Section 10(1) or Section 10(2) can opt for composition scheme. Registered person will be charged fixed amount of 3% CGST + 3% SGST/UTGST on their aggregate turnover. The section provides:

“(2-A) Notwithstanding anything to the contrary contained in this Act, but subject to the provisions of sub-sections (3) and (4) of Section 9, a registered person, not eligible to opt to pay tax under sub-section (1) and sub-section (2), whose aggregate turnover in the preceding financial year did not exceed fifty lakh rupees, may opt to pay, in lieu of the tax payable by him under sub-section (1) of Section 9, an amount of tax calculated at such rate as may be prescribed, but not exceeding three per cent. of the turnover in State or turnover in Union territory.”

However, this sub-section also provides negative list of persons who are not eligible to opt for composition scheme. List includes:

“(a) engaged in making any supply of goods or services which are not leviable to tax under this Act;

(b) engaged in making any inter-State outward supplies of goods or services;

(c) engaged in making any supply of goods or services through an electronic commerce operator who is required to collect tax at source under Section 52;

(d) a manufacturer of such goods or supplier of such services as may be notified by the Government on the recommendations of the Council; and

(e) a casual taxable person or a non-resident taxable person.”

These all are the conditions required to fulfill in order to be eligible to opt for the composition scheme.

Ways to opt Composition Scheme

As discussed above Composition Scheme can be opted by businesses that are eligible for the scheme under Section 10. When any registered person opts for Composition Scheme he must intimate the authorities about the same. Various forms have been prescribed by the authorities that can be used in intimating the authorities about the same. The option to opt for a Composition Scheme can be exercised in the below mentioned possible manner.

|

S. No. |

Scenarios of opting the scheme |

Form No. |

How to opt |

Effective date for Composition |

| 1. |

Taxable Person in the previous regime shifted to the GST regime |

GST CMP – 01 |

Taxable Person can opt for Composition Scheme by filing this form with the authorities not later than 30 days from the appointed date. |

Effective from the Appointed date |

| 2. |

Person became Taxable Person after arrival of GST regime and has applied for new registration under the Act. |

GST REG – 01 |

Can opt for Composition Scheme directly when the Taxable Person has applied for registration under the Act |

Effective from the date of Registration. |

| 3. |

When a taxable person under the GST regime has opted to shift to the Composition Scheme |

GST CMP – 02 |

By filing the intimation in the prescribed form prior to the commencement of the Financial Year for which the option is exercised. |

Effective from the beginning of the financial year |

Any Taxable Person who has availed input tax credit and in the meantime also applied for composition scheme and opts to pay tax under composition scheme, then, such a person has to pay an amount equal to the input tax credit he has availed on the:

- Inputs held in Stock;

- Inputs contained in semi-finished or finished goods;

- On capital goods, earlier.

Returns

Registered Persons who opts to pay tax under Composition Scheme required filing GSTR – 4 form on a quarterly basis. Unlike a normal return which needs to be filed every month, composition dealer required to file only one return quarterly. The due date for filing GSTR – 4 is 18th of the month after the end of the quarter.

Due Date

|

Period |

Due Date |

|

April – June 2019 |

18th July 2019 |

|

July – September 2019 |

18th October 2019 |

|

October – December 2019 |

18th January 2020 |

|

January – March 2020 |

18th April 2020 |

Apart from the quarterly return a registered person opting for the composition scheme is required to file Annual Return in Form GSTR – 9A.

Invoice

As the composition dealer cannot charge tax on supplies, he is barred from issuing tax invoice on any supply. Instead of Tax Invoice, Composition Dealer is compulsory required to issue Bill of Supply. Rule 5 – Chapter II of the CGST rules prescribed some mandatory requirements which must be mentioned on the bill of supply issued by the Composition Dealer. These requirements are:

- Bill of supply should not contain a separate column for tax or tax amount should not be shown separately in the bill.

- Bill of Supply should specifically mention that the registered person is a composition dealer and he is not eligible to charge tax on any supply.

- Following particulars are specifically required to be mentioned in the Bill of Supply:

- Date of issue of bill of supply;

- GSTIN no. of the recipient if the recipient is a registered party;

- Name and address of the Recipient;

- HSN Code of Goods;

- SAC code of Services;

- Description of the Goods or Services ;

- Value of Goods or Services;

- Discount if any;

- Signature of the Supplier.

In cases where the value of supply is less than 100, a consolidated bill can be issued for the whole day.

Contravention of any provision of the Composition Levy

Two possibilities are there when provisions relating to composition scheme can be contravened. These two situations are:

- When a registered person has become ineligible to opt for composition scheme because he does not fall within the definition of section 10 of the CGST Act.

- When he voluntary contravened the provision of the Act.

In both the situation proper officer may issue a notice to composition dealer in Form GST CMP – 05 to show cause within 15 days as to why the option to pay as a composition dealer has not been denied to the person.

Registered Person has to give reply of the said notice within 15 days in Form GST CMP – 06. In reply registered person will show how he is either eligible or ineligible to be a composition dealer. After the said reply proper officer will issue an order in Form GST CMP – 07, either accepting the said reply or denying the reply filed by the registered person.

Section 12(5) of the CGST Act also provides than if any contravention occurs by the registered person then proper officer may also impose a penalty on the registered person.

Opting out of the Composition Scheme

Registered person who has opted for composition scheme has to file a declaration every year intimating that he is eligible to be composition dealer. In simple words Registered person has to decide in the beginning of the financial year whether he wants to opt for composition scheme or not. He cannot opt for composition scheme any time during the year. Also registered person can be a composition dealer so long as he satisfies all the conditions to be the same. However if he crossed prescribed threshold limit or in any way violated section 10 of the CGST Act he will be treated as a normal tax payer.

Since to opt for composition scheme is not compulsory, registered person can opt out of the composition scheme in the beginning of the financial year. In order to opt out the composition scheme, registered person is required to file intimation for withdrawal from the composition scheme in Form GST CMP – 04. Registered person can opt out of the composition scheme only at the beginning of the financial year. Once the registered person opts out of the composition scheme he will be charged as a normal tax payer.

Comparison of Composition Scheme from Normal Scheme

As discussed earlier, to get registered under the Composition Scheme is not compulsory. CGST Act provides that a person whose aggregate turnover crossed Rs. 20 Lakh is compulsory required to be registered as a taxable registered person. Section 10 of the Act provides that if the turnover of the Taxable Person does not exceed Rs. 1.5 Crore and Rs. 75 Lakh (in special category states) can opt for composition scheme. Under the scheme Taxable Person has to pay a fixed percentage of tax on their aggregate turnover which may range from 1% to 6%. Taxable person may opt for the scheme or may not opt for the scheme considering the advantages and disadvantages of the scheme. This scheme is very beneficial for small businesses and micro and small enterprise. However various registered persons not opt for the scheme considering its restrictive provisions. Let us discuss and compare the Normal Scheme from Composition Scheme.

Comparison of Registration Process

Section 22 of the CGST Act makes it mandatory for the businesses to get the registration once the Aggregate Turnover in a particular year crosses prescribed limit of Rs. 20 Lakh or Rs 10 Lakh (for Special Category States). After registration Taxable Person will have to pay tax as a normal taxable person and normal scheme is applicable on that person. However if after registration Aggregate Turnover of the Taxable Person does not exceed Rs. 1.5 Crore or Rs. 75 Lakh (for Special Category States) and that person is not in Contravention of Section 10 of the CGST Act, he may opt for the scheme. However if any time later Aggregate Turnover of the person exceed Rs. 1.5 crore or Rs. 75 Lakh as the case may be, he has to pay tax under the normal scheme.

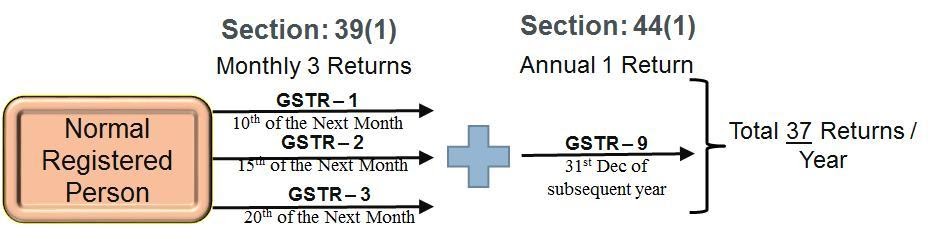

Difference in Procedural Compliance

One of the significant advantages of opting the Composition Scheme by the Taxable Person is its easy compliance. Under Normal Scheme the procedure to follow by the Taxable Person is very complex and burdensome. They have to maintain thorough accounting of all its expenditure, income, sale, purchases and even of small petty expenses. Also under normal scheme taxable person needs to file minimum 3 returns monthly and one return annually, totaling 37 returns over a year. Normal Taxable person has to file GSTR – 1 by 10th of the next month, GSTR – 2 by 15th of the next month and GSTR – 3 by 20th of the next month to claim Input Tax Credit for the goods or services purchased. Apart from this Normal Taxable Person is required to file 1 Annual Return under Section 44(1) of the CGST Act in the prescribed form GSTR – 9 by 31st December of the subsequent year. Diagrammatic representation will be more helpful in understanding the compliances under normal scheme.

Under Composition Scheme procedural compliances are easy as the complexities of filing as many as 37 returns as in the Normal Scheme are not there. Also under Composition Scheme Taxable Person has to pay tax on the basis of their aggregate turnover, so to maintain thorough accounting records are not as such a compulsion for the composition dealer. Composition dealer is required to file only five returns over the year which makes the procedural compliances for the composition dealer very easy. Under Section 39(2) of the Act, Composition Dealer is required to file quarterly return in Form GSTR – 4 by the 18th of the next month and under Section 44(1) of the Act, an annual return in Form GSTR – 9A by 31st December of the subsequent year. So Composition Dealer is required to file only five returns over the year. Diagrammatic representation will be more helpful in understanding the compliances under Composition Scheme.

Comparative Cost Advantage under Composition Scheme

One of the major benefits attached with the Composition Scheme is its simplicity and easy compliances. The complex formalities as are required to be followed by the Normal Taxable Person are not required to be followed by the Composition Dealer. It is seen that the operational cost to comply with the procedure of Normal Scheme is way too high then in Composition Scheme. This difference is mainly because under Normal Scheme businesses are required to file 37 Annual Returns while under Composition Scheme only 5 Returns are required to be filed annually. One of the major drawbacks faced by the Composition Dealer is non claiming of Input Tax Credit. However, non-claiming of ITC is beneficial in transactions where Composition Dealer will supply goods directly to the consumer. That means in Business to Consumer transaction non claiming of ITC in fact increases the profits of the Composition Dealer in comparison to the normal taxable person. Below mentioned table will be helpful in understanding the fact. It is assumed in this table that Normal Taxable Person and composition dealer both are dealing with final consumer.

|

S.No |

Description |

Registered as a Normal Taxable Person |

Description |

Composition Dealer |

|

A. |

Value of Total Sale |

224000 |

Value of Total Sale |

224000 |

|

B. |

GST@ 12% on sales value |

24000 |

GST@ 2% on sales value |

4392 |

|

C. |

Sales Value Exclusive of Taxes |

200000 |

Sales Value Exclusive of Taxes |

219608 |

|

D. |

Input Purchases |

140000 |

Input Purchases |

140000 |

|

E. |

GST @ 12% on input purchases |

16800 |

GST @ 12% on input purchases |

16800 |

|

F. |

Total Purchases Value ( D + E ) |

156800 |

Total Purchases Value ( D + E ) |

156800 |

|

G. |

Net GST liability ( B-E ) |

7200 |

Net GST liability ( only B ) |

4392 |

|

H. |

Net Profit { A- (F+G)} |

60000 |

Net Profit { A- (F+G)} |

62808 |

This table clearly illustrates the fact that in cases when normal taxable person and composition dealer are dealing with the final consumer, Composition dealer will fetch more profits out of the transaction. However, this table and this fact is based on the general presumption that both the persons are dealing with the final consumer. In cases when they are dealing with another taxable registered person i.e. business to business transaction, then Normal taxable person will fetch more profits out of the transaction because while doing the last transaction he can claim input tax credit and reduce the cost of goods. In this example if both the respective persons are involved in Business to Business transaction i.e if these persons are selling their goods to other taxable person then net GST liability (G Point) will be 0 for the registered taxable person because he will claim input tax credit of that amount. However it will be same i.e 4392 for composition dealer because he is barred from claiming input tax credit. So for registered taxable person net profit will be (A- F) that is 67200 and for the Composition dealer it will be {A–(F+G)} that is 62808.

So, for Business to Consumer transaction composition scheme is advisable. However for Business to Business transaction Composition Scheme is not advisable.

Limitation of the Scheme

There are so many demerits attached with the scheme. Person opts for the scheme considering its advantages of being less complex and easy complaint. However, there are so many conditions which need to fulfill even to be eligible for the scheme and if one opts the scheme there are so many limitations attached which the composition dealer must comply all the time. These limitations are:

- Composition dealer cannot raise tax invoice. He has to issue bill of supply after every sale.

- Composition dealer cannot claim input tax credit.

- Composition dealer cannot charge or collect tax on supply.

- Composition dealer has to specify on its bill of supply that he is a composition dealer.

- Composition dealer has to file a declaration every year intimating that he is eligible to be a composition dealer.

Section 10 of the CGST Act and Rule 5(1) (a) of the CGST Rules 2017 also mentions those persons who are not eligible to opt for the scheme. Below mentioned picture will show those who are not eligible to opt for the composition scheme. If any composition dealer makes any transaction which is prohibited under Section 10 of the Act or any transaction prohibited by Rule 5 (1) (a) of the CGST rules 2017 he will be treated as a normal taxable person.

Tabled Comparison of Normal Scheme and Composition Scheme

|

S. No. |

Particulars |

Normal Scheme |

Composition Scheme |

|

1. |

Registration |

Compulsory required to be registered under Section 22 of the Act, if the prescribed threshold limit of Rs. 20 Lakh or Rs. 10 Lakh (for special category States) is crossed. |

A registered taxable person can opt for Composition Scheme if his aggregate turnover is below the threshold limit of Rs. 1.5 Crore or Rs. 75 Lakh (for special category states) as provided under Section 10 of the Act. |

|

2. |

Restriction on Manufacturing of Goods |

No restriction for any manufacturing activity |

Vide Notification no. 8/2017 dated 27.06.2017; Central Government has prohibited ice-cream, pan masala and tobacco manufacturers from being Composition Dealer. |

|

3. |

Restriction on Supply of Services |

No restriction on supply of services. |

Supply of Services as provided under Section 10(1) (b) [Restaurant Services] is allowed. However vide Amendment Act of 31 2018, Central Government has allowed supply of services of value not exceeding 10% of the turnover (in the preceding financial year) or Rs 5 Lakh (in preceding financial year), whichever is higher, by the composition dealer for any purpose mentioned in clause (a) and (c) under Section 10(1) of the Act. |

|

4. |

Restriction on Outward Supply |

No restriction on Inter-State or Intra-State sale. |

Under Section 10(2) (c) Interstate outward supply of goods by the Composition Dealer is prohibited. |

|

5. |

Restriction on E-Commerce operator |

No restriction to supply goods or services to E-Commerce operator. |

Prohibited to supply goods to E-Commerce operator who is liable to collect tax at source under Section 52. |

|

6. |

Restrictions on Export or Supply to SEZ |

No restrictions for the normal registered taxable person. |

Since under Section 7(5) of the IGST Act, Export or supply to SEZ are considered Interstate supply. Composition Dealer cannot make any such supply. |

|

7. |

Casual taxable person or nonresident taxable person. |

Casual Taxable Person or Non – Resident taxable person can opt for normal scheme after taking registration under Section 24 of the CGST Act. |

Casual Taxable Person or Non – Resident Taxable person shall not opt composition scheme as they are prohibited by Rule 5(1)(a) of the CGST Rules, 2017. |

|

8. |

Restriction on Imports |

No restriction under Normal Scheme. |

No restriction under Composition Scheme. |

|

9. |

Filing of Returns |

As discussed earlier Normal Taxable Person is required to file 3 returns monthly and 1 return annually, totaling to 37 returns over the year. |

Composition Dealer is required to file 1 return quarterly and 1 return annually, totaling to only 5 returns over the year. |

|

10. |

Keeping of Records |

Vide Section 35(1) of the Act and Rule 56 of the CGST rules. Every registered taxable person is required to maintain following records.

|

Rule 56 of the CGST Rules provides, Composition Dealer is not required to maintain any such particular as are required to be maintained by the Normal Taxable Person. |

|

11. |

Applicable rate of Tax |

Notified rate of CGST and SGST/UTGST in case of Intrastate supply or notified rate of IGST in case of Interstate supply. |

Section 10 of the Act prescribes the Rate of Tax payable by the Composition Dealer. It is:

|

|

12. |

Tax Invoice |

Normal registered taxable person shall issue tax invoice under Section 31(1) (2) of the CGST Act and Rule 46 of CGST Rules. |

Instead to issuing tax invoice Composition Dealer is required to issue Bill of Supply under Section 31(3) (c) of the CGST Act and Rule 49 of the CGST rules. |

|

13. |

Tax Collection |

Allowed to collect tax under Section 9 of the CGST Act. |

Section 10(4) of the CGST Act prohibits Composition Dealer from collecting tax. |

Advantages and Disadvantages of Composititon Scheme

Discussed all over the project, Composition Scheme has been introduced with the objective to benefit small businesses from being involved into the complex GST compliance procedure. The main criteria for being eligible for Composition Scheme are the aggregate turnover. To opt for the Composition Scheme is optional and registered taxable person should analysis all its advantages and disadvantages before opting the scheme. Some of its advantages and disadvantages are discussed below:

Advantages of opting Composition Scheme

- Less Compliance

One of the biggest and most attracting advantages of Composition Scheme is its less compliant nature. Under the scheme composition dealer has various major benefits. Two of such major benefits are:

– Not required to maintain hefty records of various transactions. Rule 56 of the CGST rules provides leverage to the Composition dealer from maintaining hefty records and recording various transactions. This has been discussed comprehensively in the comparison table.

– Required to file only 5 returns. Composition Dealer unlike normal taxable person is required to file only 1 return in each quarter and 1 return annually. Normal taxable person is required to file 3 returns monthly and 1 return annually, totaling 37 returns over the year. This reduced the compliance cost of the composition dealer significantly.

- Lower tax payable under the Scheme

Section 10 of the CGST Act prescribed fixed percentage of tax payable on the aggregate turnover by the Composition Dealer. The percentage prescribe in the Act are significantly lower than the tax payable by the registered person under the normal scheme which may exceed to 20% CGST + 20% SGST/UTGST or 40% IGST

- High Liquidity

Composition Dealers are not eligible for input tax credit. They have to pay fixed percentage of tax on their aggregate turnover. Input tax credit is paid by the Government later in the year. This leads to the problem of blocked working capital for the normal taxable person. Since Composition Dealers are not eligible for any credit and have to pay very less amount tax, they have high liquidity available all the time.

Disadvantages of Composition Scheme

- Non-availability of Input Tax Credit

Composition Dealer cannot avail input tax credit. Concept of input tax credit has been incorporated in GST with the objective to remove cascading effect and double taxation. However, Composition Scheme is incorporated in the Act with the objective to benefit small businesses. Benefit of Input tax credit is available only to the normal taxable person because he has to pay huge percentage of taxes in comparison to the composition dealer. In composition scheme small percentage of cascading takes place because input tax credit is not available to dealer and this will increase the cost of his customer.

- Collection of tax is prohibited.

Composition Dealer is not allowed to raise tax invoice and instead of tax invoice he has to raise bill of supply. Since Composition Dealer cannot issue tax invoice he is prohibited from collecting tax for the supply.

- Registered person do not prefer to trade with Composition Dealer.

Since composition dealer are prohibited to claim input tax credit, Registered Person do not prefer to trade with the composition dealer because in that case burden of tax paid by the composition dealer has to bear by the registered person which will increase the cost of goods to the registered person.

Conclusion

Composition Scheme provides a gateway to those person who are below the prescribed threshold limit. This scheme is beneficial to all those persons who are unable or don’t want to indulge in the complex compliance procedure attached with the normal scheme. However it has also been seen in the project that there are so many restrictions attached while opting to be the composition dealer. The restrictions under section 10 of the Act in a way bar the person from expanding the business because person cannot make any interstate sale. Also limits regarding turnover makes it clear that this scheme is only available for small businesses and once the business crosses that particular limit, opting of the normal scheme is mandatory. Non-availability of input tax credit attached with the scheme also makes the scheme unattractive because it increases the burden on the purchaser.

However it is seen in the study that composition scheme is beneficial for the registered person in many aspect. It helps in reduction of huge amount of compliance cost attached with the normal scheme. Also problem of blocked credit is always attached with the normal scheme resulting in less liquidity and less working capital in the hands of normal taxable person. Since the composition dealer is not eligible for input tax credit, problem of blocked credit never take place in case of composition dealer and because of this composition dealer manage to have high working capital and high liquidity.

It is also seen in the study that in Business to Consumer transaction, Composition Dealer will be benefitted out of the transaction in comparison to the Normal taxable person. However if the transaction is business to business then Composition Dealer will be in loss in comparison to the normal taxable person. In the end it is advisable to opt for the scheme after considering all its advantages and disadvantages.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications