This article is written by CA. Chetan Monga.

Background

Concept of online selling has always been an attractive avenue and lets people reach beyond a certain boundary. In the recent past, this business trend has seen a huge spike because of the E-Commerce players like Amazon, Flipkart etc. These companies analyzed the potential the concept of online selling has and because of which they are reaping hefty dividends on their investment. Who would have thought in the yesteryears that such a concept could exist and would boom like anything. In the current scenario, this nifty concept of online selling has given stiff competition to the local sellers who are selling in their vicinity. After having analyzed the potential of revenue creation in this system of selling, the Government introduced the very new concept of TCS ( Tax collected at source ) under the very new GST (Goods and Service Tax) Act which was implemented on 01.07.2017 in our country.

Legal Provisions for TCS under GST Act

Section 2(45) of CGST Act defines – “electronic commerce operator” means any person who owns, operates or manages digital or electronic facility or platform for electronic commerce;”. The e-commerce operators need to compulsorily get themselves registered under GST who are required to deduct TCS u/s 52 of GST Act and there is no threshold limit exemption for it.

TCS applies only if the operators collect the consideration from the customers on behalf of vendors or suppliers. In other words, when the e-commerce operators pay the consideration collected to the vendors they have to deduct an amount as TCS and pay the net amount. TCS will be deducted on the net value of taxable supplies. “Net value of taxable supplies” shall mean the aggregate value of taxable supplies of goods or services or both, other than services notified under sub-section (5) of section 9 made during any month by all registered persons through the operator reduced by the aggregate value of taxable supplies returned to the suppliers during the said month.”

According to section 52 (4) of the Act, the Operator shall furnish a statement in form GSTR-8, electronically, containing the details of outward supplies of goods or services or both effected through it, including the supplies of goods or services or both returned through it, and the amount collected during a month, within ten days after the end of such month.

According to section 52 (5) of the Act, the Operator shall furnish an annual statement in form GSTR-9B, electronically, containing the details of outward supplies of goods or services or both effected through it, including the supplies of goods or services or both returned through it, and the amount collected during the financial year, before the thirty first day of December following the end of such financial year.

Section 52 (6) of the Act – If any operator after furnishing a statement in form GSTR-8 discovers any omission or incorrect particulars therein, other than as a result of scrutiny, audit, inspection or enforcement activity by the tax authorities, he shall rectify such omission or incorrect particulars in the statement to be furnished for the month during which such omission or incorrect particulars are noticed, subject to payment of interest, as specified in sub-section (1) of section 50.

Provided that no such rectification of any omission or incorrect particulars shall be allowed after the due date for furnishing of statement for the month of September following the end of the financial year or the actual date of furnishing of the relevant annual statement, whichever is earlier.

Section 52 (8) of the Act – The details of supplies furnished by every operator in the form GSTR-8 shall be matched with the corresponding details of outward supplies furnished by the concerned supplier registered under this Act in form GSTR-1.

Section 52 (9) of the Act – The discrepancies shall be communicated to the both persons i.e. the Operator and the concern Supplier.

Section 52 (10) of the Act – The amount in respect of such discrepancy if had not been rectified earlier, shall be added to the output tax liability of the supplier, where the value of outward supplies furnished by the operator is more than the value of outward supplies furnished by the supplier, in his return for the month succeeding the month in which the discrepancy is communicated.

Section 52 (11) of the Act – The concerned supplier, in whose output tax liability any amount has been added under sub-section (10), shall pay the tax payable in respect of such supply along with interest, at the rate specified under sub-section (1) of section 50 on the amount so added from the date such tax was due till the date of its payment.

All the above stated provisions may sound tough to comprehend and apply but since everything under the GST regime is technology-driven so compliances of above provisions have been inbuilt in the GST system. The same has been explained in a layman’s language and with practical approach under another heading below.

How this Concept works Practically

It was seen that the sales that were executed online were being escaped by the sellers as there was no way to keep a track of the sales executed through the portals like Amazon, Flipkart etc. Under the current regime of GST, it is next to impossible to escape the sales executed online.

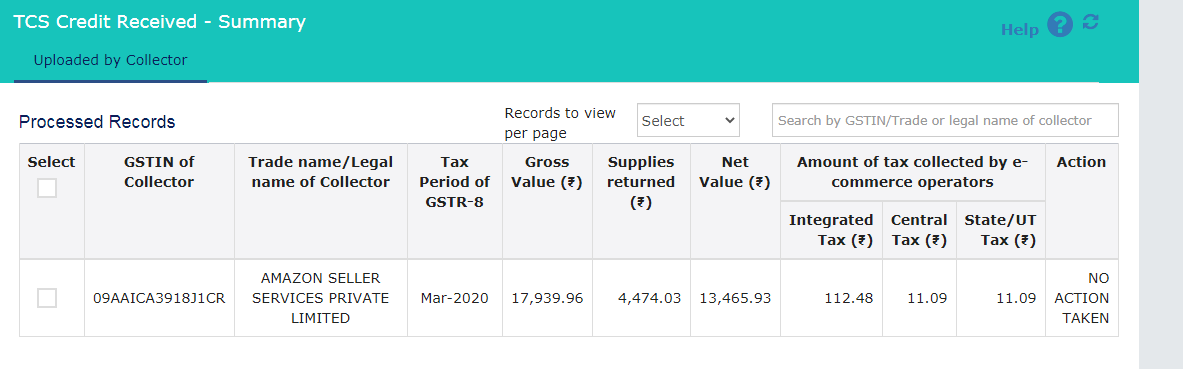

Let us try this concept through a lucid example. Let’s say a company ABC Limited wants to sell taxable goods(taxable @5%) on Amazon. For this, ABC Limited has to create an account as a seller on Amazon. Account creation is as easy as we create an account over Gmail or Facebook. After fulfilling all the requirements as required, the account gets approved by Amazon. Now ABC Limited can start listing its products and executing the sales. Let’s assume that during the month of June 2020 the sales executed is Rs 1,00,000. Amazon will make the payment to ABC Limited after deducting its own commission ( for providing the platform) and TCS @1%. This TCS deducted by Amazon will reflect on ABC Limited’s GST portal under services/Returns/TDS and TCS credit received ( Refer Figure 1(a)).In order to get that TCS reflected on ABC Limited’s portal, Amazon needs to file GSTR-8 by 10th of July 2020. By filing GSTR-8, it declares that ABC Limited has executed sales of Rs 1,00,000 through its portal and TCS of Rs 1,000 has been deducted ( Refer Figure 1(b)). ABC Limited is also given the option to accept or reject it. This option is provided so that in case ABC Limited finds any discrepancies in the sales so declared by the E-Commerce, it may reject the same which will be intimated by the GST portal to the E-Commerce operator. This makes the system even easier for all the parties involved in the transaction.

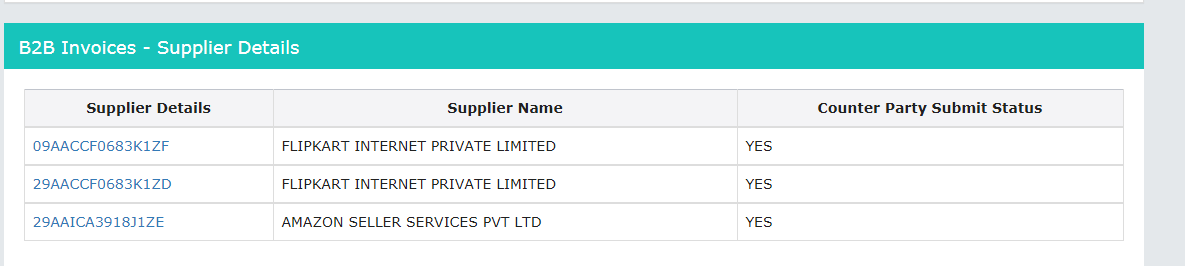

The commission earned by Amazon will be an expense for ABC Limited which will also reflect on ABC Limited’s portal under GSTR-2A section (Refer Figure 2). In order to get this commission reflected under GSTR-2A of ABC Limited, Amazon will need to file GSTR-1/3B(return in which any business declares it’s own sales under GST regime) by 11th of July 2020.

(Figure 1(a): TDS and TCS Credit Received)

(Figure 1(b): Details Sales executed through Amazon and TCS deducted on that sales)

(Figure 2: GSTR-2A Where Commission Invoices by the Amazon can be Checked)

Since the TCS deducted @1% is being reflected at ABC Limited’s GST portal, now it will not be able to escape these sales and it will have to declare these sales in its own GSTR1/3B. However, the TCS so deducted will be available as a credit which can be used to pay off the GST liability. Now ABC Limited will have to pay an additional 4% tax since 1% tax has already been deducted by Amazon(since the product sold by ABC Limited is taxable @ 5%). This TCS deduction is a mere additional step to ensure that the sales executed on Amazon portal does not go unnoticed or is not concealed by the seller.

Had this concept not been in place, ABC Limited would have paid the entire 5% at the time of declaring its own sale in GSTR-1/3B. In that case, the Revenue would have been left at the mercy of the seller and there was no mechanism to track these sales. By bringing the concept of TCS, the Government has been able to keep a check on these types of sales and has been able to increase its tax collection.

Now the question arises how the seller i.e. ABC Limited makes sure that it declares accurate details as declared by Amazon while filing GSTR-8.In a nutshell, the sales declared by ABC Limited should tally with the sales declared by Amazon for ABC Limited. For this, Amazon provides monthly B2C (Business to Consumer) and B2B (Business to Business) report which provides the state wise details of the sales. This helps the seller to file the GST returns (GSTR -1/3B) accurately.

This nifty concept has been one of its kind. This concept was never seen under VAT/Service Tax/Excise regime. There are so many new concepts that have been introduced to make the GST system robust and smooth and this is one of them. It will prove to be a boon for the Revenue as tax evasion will reduce substantially and tax collection will go up as all the transactions can be tracked in no time. However, it will be a challenge for the sellers as TCS so deducted will impact their liquidity flows because they can not claim it until they file their returns. The Government has been making some genuine efforts to make sure that the tax system becomes more compliant and easy to follow. The paperwork has been brought to its bare minimum which has helped businesses at large. This will not help our country to grow but also help us to meet international standards.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications