In this article, Debarati S Tripathi pursuing M.A, in Business Law from NUJS, Kolkata discusses the valuation of copyright.

Introduction

Valuation is a term used to ascertain the worth of an asset. An asset is a resource from which future economic benefit can be expected. Assets can be fixed or tangible like property, machinery movable like jewelry, and intangible like goodwill in a business, intellectual property or IP. Valuation is a common and everyday practice and not all valuations require a formal analysis. Valuation is an art and has a science behind the value ascertained.

IP assets include patents, industrial designs, trademarks, copyright and trade secrets. IP assets are a subset of intangible assets and distinguished from other intangible assets by the fact that these are created by law – legally protected and can be legally enforced. These can be independently identified, are transferable and have an economic life (in contrast to their legal life, which is generally longer than their economic life). While an IP asset can be defined in terms of particular qualitative features or standards like novelty, originality, it may not directly be linked to market value, e.g. there are patent filed that do not contribute to production of protection of income but are aimed at technical and scientific aspects which indirectly may create a value or block competition.

The objective of this write-up is to give an overview of the ever evolving and changing legal framework in India in the domain of IPRs, with a mention on the current context.

Value of an IP Asset

IPRs have very little intrinsic value. Successful exploitation of the asset creates value, like an IP asset which is able to exclude competitors from a particular market is value to the user/owner.

The legal right grants exclusivity or the right to exclude and the economic right is based on the ability to control the use of an IP asset thus creating exclusivity of use. For an IP asset to have a quantifiable value, it should generate measurable amount of economic benefit to its owner/user and /or enhance the value of other assets with which it is associated.

Value may be derived from an IP asset by,

- Direct exploitation of the IP

- Through sale or licensing of the IP

- Even by not exploiting an IP asset (i.e., by merely owning it), it may be possible to add value, e.g. by raising barriers to entry by competitors, reducing the negotiating power of customers, balancing out supplier power, mitigating rivalry, and lowering the threat of substitutes.

IP Valuation is a Process to Determine the Monetary Value or Worth of Subject IP

Valuation often combines objective and subjective considerations. It is an opinion about the result of a virtual transaction. IP Valuation is dependent on various factors, such as:

- Use of the IP assets

- Market position of the company

- Openness of economy (in the country or region of operation)

- Legal protection of IP

- Enforcement cost

- Overall economic growth and profile of economy

Copyright

The subject of this write-up is Copyright, as the representative of IP.

A Copyright provides for a bundle of exclusive rights to authors of original literary, musical, dramatic and artistic works, the sole right to authorize (or prohibit) the following uses of their copyrighted works:

- To reproduce all or part of the work.

- To make new (derivative) versions.

- To distribute copies by selling, renting, leasing, or lending them.

- To perform (that is, to recite, dance, or act) the work publicly.

- To display the work publicly, directly, or by means of film, TV, slides, or other device or process.

The first three rights are violated when anyone copies, excerpts, adapts, or publishes a copyrighted work without permission. Thus, a copyright legally protects the original expression of ideas, NOT the ideas themselves, that means an idea cannot be copyrighted. It is the expression of the idea — the way it is presented — that is copyrighted. The value derived from a copyright is by virtue of using the copyright.

As is true with all intellectual property, a copyright has a special set of legal rights and protections that is afforded to the copyright owner. These legal rights are the basis for the value of a copyright. A copyright can confer monopoly to the owner by creating a barrier to entry and thereby translate to buying power and greater profit margins for the owner.

It brings about a domain of permissibility – where the owner permits a party to use the IP in return for compensation which can be a license or has a sale value. A copyright can be enforced and is often subject of litigation – where the benefits are the litigation award or the owner can sue for damages.

On the face of it, a copyright signals creativity, innovation and uniqueness which may result in additional sales and incremental margins with reduced promotion and marketing efforts. For a copyright to command value it requires other resources like natural resources/tangible resources or people resources or capital when combined by way of a Copyright and exploited in terms of products or services has the capability of yielding profit.

The Value of a Copyright can be broken down to Two Step Process

- Determine the profits.

- And then apportion the profits to the Copyright.

This in turn determines the Value of the Copyright. The value of a copyright that is most commonly enjoyed is the Royalty earnings by licensing the Copyright. The rate of this Royalty is often driven by the earnings of the business of the licensee from the Copyrighted material.

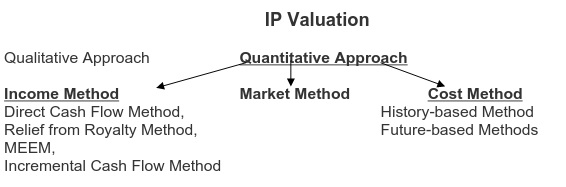

IP Valuation

Qualitative Approach

- Income Method

-

- History – based Method

- Relief from Royalty Method

- MEEM

- Incremental Cash Flow Method

Quantitative Approach

- Market Method

- Cost Method

- Direct Cash Flow Method

- Future – based Methods

The 3 generally accepted methods of IP valuation may be applicable to the analysis of copyrights. The Cost method is less commonly used than the Income method or the Market method. Because the copyright grants monopolistic rights to the owner, the Cost approach is not always applicable to a copyright valuation analysis.

1. Cost Method

This method is based on the intention of establishing the value of an IP asset by calculating the cost of developing same or identical IP asset either internally or externally. The method aims to determine the value of an IP asset at a particular point of time by aggregating the direct expenditures and opportunity costs involved in its development and considering obsolescence of an IP asset. The Cost Method is generally the least used method as, in most cases, it is considered suitable only as a supplement to the income method.

Both creation cost and re-creation cost methods may be used with regard to copyright valuation analysis. In all cost approach valuation analyses of copyrights, the analyst should consider as cost components both, the developer’s profit and the entrepreneurial incentive – both of which often represent the largest components of value. The cost approach has certain limitations when analyzing of a corporation-owned copyright and is often considered to provide a minimum estimate of value — as opposed to a maximum estimate of value.

The Cost Approach is based on the economic principle of substitution. This principle suggests that an investor will typically pay no more for a fungible intellectual property asset than the cost to purchase or construct a substitute asset. However, it is not legally possible to purchase or reconstruct a substitute intellectual property with regard to copyrights. Because by definition of Copyrights – they are unique and original work. Therefore, the hypothetical investor who attempts to purchase or construct a substitute intellectual property will be guilty of copyright infringement. Therefore, the “willing buyer” in a copyright market value transaction cannot legally re-create the subject and similarly a willing seller will not sell for less than his cost, which mostly would mean his investment. Hence the cost method is not the most accurate approach to arrive at a ceiling or maximum copyright valuation.

Reproduction Cost method and Replacement Cost method are the two alternatives of the cost method.

2. Market Method

The Market Method is based on comparison with the actual price paid for a similar IP asset under comparable circumstances. Market approach methods are commonly used in a copyright valuation analysis. The free and simple sale of copyrights is usual practice in the market and is true with regard to all of the types of copyrighted materials like musical, artistic, literary. However, the pricing details related to these copyright sales are not publicly disclosed. Also, it is often difficult for analysts to develop metrics in order to extract market-derived pricing multiples from these transactional data, e.g. it is not easy to convert pricing data regarding the actual sale of a copyright into a logical “per picture”, “per lyric” or “per word” pricing multiple.

Licensing of all types of copyrighted materials is on the other hand a thriving option. Thus, the most common market approach methods involve some form of royalty rate or similar license analysis. Analysts sometimes have the problem of developing units of comparison if the selected empirical license agreements call for fixed periodic dollar payments — for example, $100,000 per year.

Many copyright license agreements employ either a royalty rate formula or a per-use formula. In the royalty rate formula, the license agreement typically compensates the author by a percentage of the total revenues generated through the use of the copyrighted materials. In the per-use formula, the license agreement typically compensates the author as a dollar amount for each time the copyrighted material is performed, displayed, or otherwise used.

3. Income Methods

They are very commonly used in the valuation and economic analysis of copyright intellectual properties. It focuses on the income generating capability of the property. The Income method values the IP asset based on the amount of economic income that the IP asset – Copyright is expected to generate, adjusted to its present day value.

To determine the Economic Income

- Project the revenue flow or cost savings generated by the Copyright over the remaining useful life (RUL) of the asset.

- Offset those revenues/savings by costs related directly to the Copyright. Here, Costs could comprise labor, materials, required capital investment and any appropriate economic rents or capital charges.

- Take account of the risk to discount the amount of income to a present day value by using the discount rate or the capitalization rate.

The Various Income Approach Methods typically involve some form of the following types of Analysis

1. Incremental Income Analysis

This is the estimation of the difference between the amount of income that the owner/operator would generate with the use of the subject copyright and the amount of income the same owner/operator would generate without the use of the subject copyright.

2. Profit Split Income Analysis

The estimation of the total income that the owner/operator would generate from the use of the copyright where the total income estimate is split between the copyright and all of the other tangible and intangible assets that contribute to the generation of the owner/operator total income estimate.

3. Residual (or Excess) Income Analysis

The estimation of the residual owner/operator income with the ownership/operation of the copyright. This residual income analysis is accomplished by first estimating the total owner/operator income.

The analyst then identifies and values all of the owner/operator tangible and intangible assets. A fair rate of return, which represents a capital charge or an economic rent, is then assigned to each category of the tangible and intangible assets. The analyst would then subtract the capital charge on contributory assets from the total owner/operator income estimate. Finally, the residual or excess income is assigned to the copyright.

For analysis based on an income approach, the copyright income is projected over an estimate of the Remaining Useful Life (RUL) of the copyright income stream. The maximum amount of time that may be considered is the very long legal life remaining in the copyright – typically, the author’s life plus 50 years. However, the more practical time span to consider is the expected period of popular acceptance and commercial viability for the copyrighted work. Some computer games, for example, have a limited lifetime of trendiness and popularity before they are overtaken by the “next big thing”. The determination of remaining useful life of earning potential obviously has a significant effect on the calculation of today’s net present value. The present value of the owner/operator income (defined as excess, incremental or residual income) over this expected RUL is an indication of the value of the copyright.

Case Study Examples

A. Market Method

Assume for example that a valuation expert must find the fair market value for a Rembrandt portrait from 1642. The expert will have to toil hard and collect probative information from market transactions of other Rembrandts of the same subject matter (same person, similar pose, similar social position, etc.), year painted and other characteristics. However, if the particular subject Art is copyrightable – it would be original and hence there would be room for differences from those available and such differences can attribute disproportionate value. In the end, the appraiser will need to account for differences as well as similarities with the market-based transactions found to come up with a value.

B. The Relief from Royalty Approach

It provides one estimate of the fair market value of the Subject Assets as shown below. This estimate can be used in negotiating a transaction price with the Acquirer.

| YEAR- | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Royalty Base (million €) | 3.0 | 6.0 | 12.0 | 24.0 | 48.0 | 52.8 | 58.1 | 63.9 | 70.3 | 77.3 |

| Royalty Rate | 4.0% | 4.0% | 4.0% | 4.0% | 4.0% | 4.0% | 4.0% | 4.0% | 4.0% | 4.0% |

| Pretax royalty stream (million €) | 0.12 | 0.24 | 0.48 | 0.96 | 1.92 | 2.11 | 2.32 | 2.56 | 2.81 | 3.1 |

| Tax rate | 20% | 20% | 20% | 20% | 20% | 20% | 20% | 20% | 20% | 20% |

| After tax royalty stream (million €) | 0.096 | 0.192 | 0.384 | 0.768 | 1.536 | 1.688 | 1.856 | 2.048 | 2.248 | 2.48 |

| Present value factor | 0.878 | 0.675 | 0.519 | 0.399 | 0.307 | 0.236 | 0.182 | 0.140 | 0.107 | 0.083 |

| Present value of Royalty stream (million €) | 0.084 | 0.13 | 0.199 | 0.306 | 0.472 | 0.398 | 0.338 | 0.287 | 0.241 | 0.206 |

| Total present value of Royalty streams (million €) | 2.66 |

The University could negotiate a range of terms with the prospective acquirer – from a running royalty rate of 4% of revenue for products incorporating the intellectual asset to a fully paid up license fee of 2.66 million Euro. The University could also set terms that included a one-time payment plus a running royalty or set terms that included a one-time payment plus a running royalty should cumulative product sales exceed a certain level.

C. Income Method

Roses N Thorn (“Thorn”) is a composer of rock and roll music and lyrics. Last year, Thorn composed the words and music to “Blue Valley” (“Valley”), a classic rock and roll number. Thorn is a contract employee of music producer RocknRoll Corporation (TV1). Valley was a work for hire and therefore the copyright is owned by TV1. The local taxing authority assesses the TV1 on a unit valuation basis. The local taxing authority assessor estimated the total unit value of TV1, as of January 1, 2009. In the taxing jurisdiction in which TV1 is located, intangible personal property is exempt from tax. In this case, a copyright intellectual property clearly qualifies as an exempt intangible asset. Accordingly, TV1 management will use this valuation to contest its tax assessment.

Fact Set and Illustrative Valuation Variables

The date of the copyright valuation is January 1, 2009. TV1 management prepared a projection of the income it expects to earn from the recording and distribution of the “Valley” work. For popular rock and roll songs like ‘Valley,” it is the TV1 historical experience that the average life of consumer popularity is five years.

Also, according to TV1 historical experience, consumer demand of such a successful popular musical composition approximates an exponential decay curve function. Therefore, starting with the January 1, 2009, valuation date, the percent surviving in the consumer demand curve will be less than 10 percent (i.e., immaterial) after the year 2019.

This expected decay curve for consumer demand is based on,

- A Five-year Average life

- An Exponential Decay function

Based on the analyst’s cost of capital analysis, the analyst concluded that the appropriate present value discount rate is 16 percent. The analyst performed a comprehensive search for musical composition license agreements. Such license agreements are very common in the music recording industry. The analyst identified several guideline copyright license agreements with regard to commercially popular rock and roll musical compositions that had already been released. Based on this research, the analyst concluded that the most applicable license royalty rate for “Valley” would be a 50 percent profit split. That is, in such copyright license agreements, the copyright licensor receives 50 percent of the composition-related net income, the copyright licensee also receives 50 percent. In such license arrangements, the licensor is typically the copyright author or an owner/operator corporation copyright holder.

Also in such arrangements, the licensee is the recording artists and/or recording producers that actually record and distribute the recordings. In this case, TV1 corresponds to the typical copyright licensor in these musical composition license agreements. In the case of the TV1 license agreement, let’s assume that net income subject to the “profit split” royalty rate is defined as:

Total revenue Less: Cost of goods sold Less: Selling, general, and administrative expenses Equals: Net income.

Application of the Copyright Valuation Approaches and Methods

The income approach is the most applicable analysis, based on:

- The Information available to the analyst (including the TV1 business plan)

- The Objective of the analysis (i.e., to estimate the value of the subject copyright for taxation appeal), the income approach is the most applicable analysis.

Exhibit 2

Exhibit 2 summarizes the TV1 management-prepared business plan with regard to its recording and distribution of the “Valley” song.

- The projection of total revenue generation

- The Gross Profit (i.e., total revenues less cost of goods sold)

- The Net income (i.e., gross profit less selling, general, and administrative expense)

Based on the TV1 projection of net income over the expected life cycle of the production and distribution of the “Valley” recordings, the analyst estimated the expected copyright license payments to the subject owner/operator corporation copyright holder.

Using a present value discount rate of 16 percent, Exhibit 2 presents the present value of the expected license payments to the subject owner/operator corporation of the “Valley” copyright.

Based on the income approach valuation analysis summarized in Exhibit 2, the value of the TV1 owner’s intellectual property of the “Valley” copyright, as of January 1, 2009, is (rounded) $110,000,000. This amount represents the value of the subject corporation owner’s intellectual property of the copyright on the subject musical composition. This value is based on an income approach valuation method — the profit split method.

IP Valuation is Useful

- For commercial transactions

- For pricing the product, work or service

- For evaluating potential merger or acquisition candidates

- For identifying and prioritizing assets that drive value

- For strengthening positions in commercial negotiations

- For making informed financial decisions on IP maintenance, commercialization and donation

- For evaluating the commercial prospects for early stage R&D projects

- For evaluating R&D efforts and prioritizing research projects

- For financing or securitization

- For litigation

- For tax planning

Benefits of Copyright Valuation

The value of copyrights can be a significant factor in determining reasonable royalty rates for licensing agreements. Further, the value of copyrights can be an important factor in determining damages in cases of copyright infringement. They are of value when selling a business.

Copyright generate the following benefits for,

- Increases the pricing power

- Greater Profit Margins

- Litigation award (PV of award less cost)

- Protect from threat of litigation

- Additional Sales

- Reduced Marketing

- Incremental margin

References

http://www.willamette.com/insights_journal/09/autumn_2009_1.pdf

http://www.wipo.int/edocs/mdocs/mdocs/en/cdip_17/cdip_17_inf_2.pdf

http://corbinpartners.com/wp-content/uploads/2012/12/vue1108.pdf

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

It was a good experience while reading your blogs. Thanks for sharing this with us.