This article is written by Prabhat Shetty, pursuing a Certificate Course in Advanced Corporate Taxation from LawSikho.com.

Table of Contents

Introduction

A few months back, before the COVID-19 pandemic, the business community and specifically the MSMEs in India were cautiously optimistic about its growth prospects.

The global economic slowdown was imminent because of various factors like Trade war between economic giants – U.S and China, growing unrest in the Middle-east and the South China Sea, BREXIT and various other factors.

India too was heading towards an economic slouch but still, the business environment was positive, because the government, as well as businesses, were taking corrective measures to face the potential recession. Various opportunities were identified and various programmes and plans were formulated to navigate through slow-down of businesses. The various schemes laid down by the government focused mainly on 9 key aspects revolving around employment generation and credit support schemes, reviving the Khadi, Village and Coir industry, qualitative technological up-gradation, promoting ‘Make In India’ products, Entrepreneurship and skill development and conducting various programmes and training institutes for the same, Infrastructure Development, helping new entrepreneurs understand the importance of R&D for the growth, development and diversification of business, Promotions and encouragement of backward areas and lastly Improvement in Information, Education and Communication.

These schemes focused mainly on growth in specific sectors, but due to the outbreak of novel coronavirus, many businesses found themselves in a very uncomfortable situation of having to choose between life and livelihood.

No one predicted an ECONOMIC HALT in the form of lockdowns in different phases. Now that the lockdowns are relaxed, businesses are trying to get accustomed to the new normal in the Covid-19 Era. There was a need for new schemes to be formulated so as to push for-

- Innovation in the smooth functioning of businesses in the new COVID-19 era.

- Guarantees to Investors, Banks and Non-Banking Financial Company (NBFCs) regarding their return on investment.

- Working Capital support to ailing businesses.

This was made possible and in accordance with the aims and objectives put forth by the Micro, Small, and Medium Enterprises Development (MSMED) Act, 2006. In this article, I have tried to explain the various policies formulated by the government and the objectives behind the same, which can be a crucial saving grace for the MSME sector during these testing times.

Problems faced by MSMEs due to COVID-19

MSMEs are always projected as the backbone of the Indian economy having enormous growth potential. If this is true, then why is it that the MSME sector has suffered the most due to COVID-19? It is mainly due to factors like credit deficit (i.e. shortage of Loans), shortage of working capital, and a decrease in demand for non-essential goods which fall under the domain of MSMEs.

According to the latest available (2018-19) Annual Report of Department of MSMEs (click here for the PDF) the following chart is extracted:

- Distribution of Enterprises Category Wise (Numbers in lakh)

|

Sector |

Micro |

Small |

Medium |

Total |

Share (%) |

|

Rural

|

324.09 |

0.78 |

0.01 |

324.88 |

51.25 |

|

Urban |

306.43 |

2.53 |

0.04 |

309.00 |

48.75 |

|

All |

630.52 |

3.31 |

0.05 |

633.88 |

100 |

From this chart, we can also infer that Micro enterprises (630.52 lakhs), when divided by the total number of MSMEs (633.88 Lakhs), amounts to a whopping 99.47% of all MSMEs in India.

Out of these Micro Enterprises, most of them may be just too small an enterprise to be registered as MSME because the total number of MSMEs is calculated according to the Economic census and not by actual registration of such MSMEs.

This is primarily because most micro-enterprises may be just too small in size for-

- Filing an Income Tax Return as they do not qualify the threshold limit specified under GST.

- Maintaining proper Books of Accounts.

- Complying and adhering to various Laws and regulatory norms.

Therefore, they are by-default pushed out of formal networks thereby creating a blind spot for all the schemes and benefits provided by the government.

- This invisibility from formal networks can be an advantage for short-sighted businessmen as non-compliance of it brings down the production cost but, in times of crises like the Covid-19, it becomes difficult for the government to help them.

- Due to lockdowns, many micro-enterprises are finding it difficult to maintain their workforce and sometimes also their business.

- If such micro-enterprises are adequately mapped, the government could provide wage subsidies and direct bank transfer to help out the small businesses with their working capital requirements to sustain their business during the Covid-19 lockdowns which are a common practice in many developed countries of the world.

- In close connection to this, the single biggest hurdle facing the MSMEs is – lack of financing. According to a report by the International Finance Corporation (part of the World Bank) (see here), the formal banking system supplies less than one-third of the total loans required by the MSMEs which means the informal sectors are providing more than two-thirds of loans.

- Due to this pandemic, a big issue plaguing the sector is the delays in payments to MSMEs — be it from their buyers (which includes the government – as it is a big purchaser of MSME goods) or recovering finances by way of GST refunds etc.

In order to address the above-mentioned problems, the government has formulated new schemes to help the businesses navigate through these difficult times.

Various government schemes launched for MSMEs due to COVID-19 and their objectives

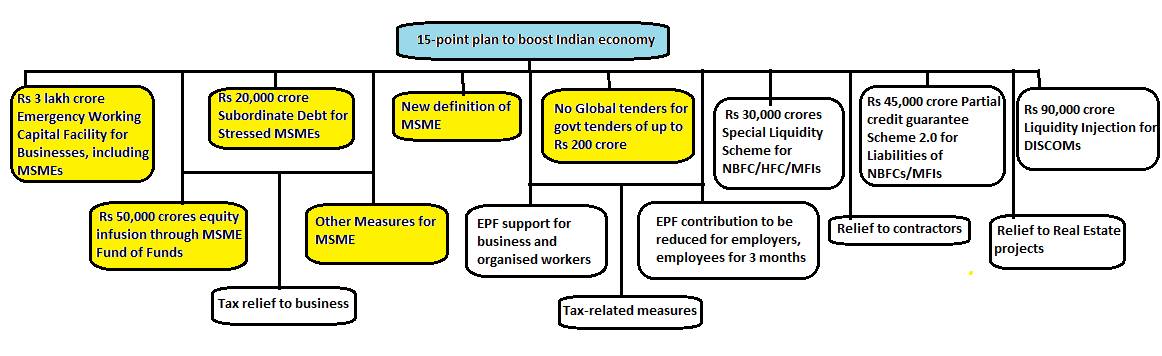

The Prime Minister of India, Narendra Modi, announced a special economic package amounting to Rs 20 lakh crore to deal with the Covid-19 crisis, soon after this announcement the Union Finance Minister Nirmala Sitharaman introduced a 15 Point Plan to boost the Indian economy out of which 6 directly affected the MSME sector.

This Scheme is aimed at providing emergency Working Capital Facility, buying raw materials and support to restart businesses for MSMEs and interested MUDRA borrowers (Pradhan Mantri Mudra Yojana is a Government of India scheme, which enables a small borrower to borrow from banks, Microfinance Institutions (MFIs), NBFCs for loans up to 10 lakh for non-farming income-generating activities. Generally, loans up to 10 lakh issued by banks under Micro Small Enterprises are given without collaterals). The Union Cabinet has approved funding of Rs. 3 lakh Crore for this Scheme.

Eligibility

All MSME borrowers with an outstanding credit of up to 25 Crore and Annual Turnover of up to 100 Crore would be eligible for 20% of their outstanding credit in the form of loans from banks and NBFCs.

Tenure

The loans have tenure of 4 years;

|

Initial 12 months |

Subsequent 36 months |

|

Moratorium period for Principal repayment i.e. The amount of Principal need not be repaid for the initial 12 months whereas Interest @ 9.25% must be paid |

Principal and Interest must be repaid in the remaining months |

Availability

- The facility is available from,

- The date of announcement to 31st of October, 2020; or

- Till the amount of Rs. 3 lakh crore is sanctioned; or

- Whichever is Earlier.

Objective

The main objective is to provide incentives to Banks, NBFCs and other Financial Institutions to increase access and availability of funds to MSMEs in view of economic distress caused by Covid-19 by providing 100% guarantee for any losses suffered by them due to non-repayment by borrowers.

-

Rs 20,000 crores subordinate debt for stressed MSMEs

Subordinate Debts are collateral-free debt that has secondary priority in repayment if the company files for bankruptcy or liquidation.

Eligibility

MSMEs which are facing financial difficulties because of the pandemic and as a result not able to pay the loans taken from banks are eligible.

Objective

The main objective is to provide incentives to Banks, NBFCs and other Financial Institutions by providing partial credit guarantee support to give loans to MSMEs that are financially stressed and are NPAs.

-

Rs 50,000 cr. equity infusion for MSMEs through fund of funds

New businesses have always found it difficult to get sufficient funding for their ideas and the current situation has decreased the risk-taking capacity of investors to a minimum.

So, in order to help the new businesses or the existing businesses with high growth prospects, the government has introduced a concept of Fund of Funds (FoF). This concept is borrowed from the FoF concept of Mutual Funds. Here, the government is the investor who establishes a Mother fund along with few daughter funds having a total corpus of around 10,000 Crores. These funds will be invested in MSMEs having high growth potential by buying up to 15% of their equity. The money tactfully invested in such businesses will give dividends, and the amount earned will be further invested in another business having high potential. The government aims at growing the fund up to 50,000 Crores to help more MSMEs.

Objective

The main objective is to help expand the size and capacity of the business and encourage the MSMEs to get listed on the main board of the Stock Exchange.

-

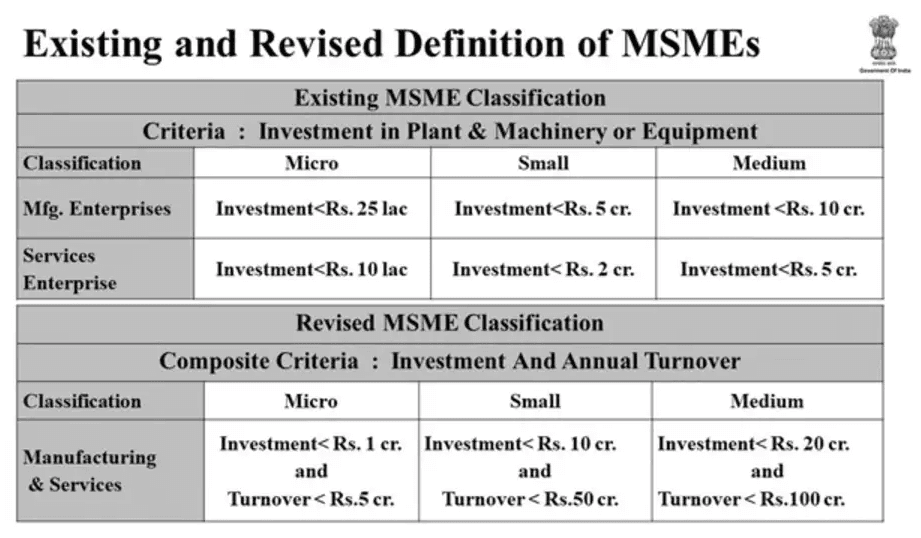

New definition of MSMEs

Objective

As per the new definition of MSMEs which was announced in May 2020, the limit for investments has been increased and an additional criterion of turnover is introduced. The proposed revised definition for the MSME sector based on turnover is progressive in nature and is in perfect sync with the GST framework – as GST is also based on annual turnover. Further, the distinction between manufacturing and services has been done away with, as now under the revised definition both manufacturing and service sectors of a business can be bifurcated as Micro, Small or Medium enterprise on the basis of investment and turnover.

-

Global tenders to be disallowed up to Rs 200 Crores

Competition is ruthless everywhere, in the International arena Indian MSMEs are just too small to compete with their highly advanced and well-funded international counterparts, but in the domestic arena, the Government of India extends a helping hand by prioritising tenders from Indian MSMEs by disallowing global tenders up to Rs. 200 Crores.

Objective

This will give opportunities to MSMEs to grow and prosper and also the government will become less dependent on international companies to do their domestic work. This might just be the first step to make India self-reliant and with this step, the government of India intends to lead by example.

-

Other measures are taken for MSMEs

- E-Market places are promoted by the government in order to conduct Trade fairs and exhibitions through virtual means.

- Fintech companies are promoted to enhance and secure financial transactions through electronic mode. These companies will also be used to boost transaction-based lending.

- The Finance Minister has said that the government is monitoring pending settlement of dues to MSMEs and also issued an ultimatum to Government Central Public Sectors Undertakings to settle the dues within 45 days.

Objective

The main objective is to promote Marketing and Liquidity of funds to MSMEs and help out the MSMEs with settlement disputes as these areas have been significant pain points augmented by COVID-19.

The impact of these schemes in addressing the current concerns on the ground can be analysed only in the upcoming months and years to come.

Conclusion

The government is fully aware that rebooting the Indian economy is a herculean task but policy-driven plans & strategies and meticulous execution of it might just do the trick. MSME sector plays an important role in bringing the economy back on track and thus the government has prioritised this sector and formulated schemes to find appropriate solutions to problems like Lack of infrastructure, Inadequate market linkage and poor marketing strategies, financial struggles, Managerial difficulties, use of obsolete technology, Low production capacity to name a few.

The plans and strategies have been laid out to support the MSME sector, various schemes have been launched but will the initiatives like MAKE IN INDIA and ATMANIRBHAR BHARAT or SELF-RELIANT INDIA become a success?

Time will be the judge of that but as of today, the Government of India has shown the way forward and tried to bring back “Cautious Optimism” among its investors, businessmen and people in general.

References

- A PowerPoint presentation was given by Finance Minister

- Annual Report of Department of MSMEs

https://msme.gov.in/sites/default/files/Annualrprt.pdf

- Report by the International Finance Corporation

- 6 COVID relief measures announced by FM Nirmala Sitharaman to make MSMEs ‘Atma-nirbhar’

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications