This article is written by Prachi Gupta, pursuing a Diploma in M&A, Institutional Finance, and Investment Laws (PE and VC transactions) from LawSikho.com.

Table of Contents

Introduction

Economists may refer to this era as the age of mergers and acquisitions. Globalisation has become an essential feature of the economy. This has resulted in tougher competition, an increase in cost pressure and has necessitated the adoption of the processes adapted at the multinational level. This has not been restricted to multinational companies but also the medium-sized companies.

In the past two decades, the M&A world has gone global. It is no more restricted just to the local or domestic market. Nowadays, companies prefer to seek targets in more far-flung areas. The exponential development of countries in Asia, the Middle East, and Latin America has created a plethora of opportunities for acquirers in these areas. Acquirers in these regions, while at the same time turning local companies into acquirers in their own right. M&A is a mechanism to foster growth and increase the shareholder value of a company. Thus, it plays a crucial role in a company’s armoury. When a company seeks targets in a foreign land it is referred to as a cross-border M&A. Cross-border M&A, in particular, can act as a springboard for a company aiming at expansion and prosperity in the long run.

During a cross-border transaction, various complex and often mystifying issues come up. Thus, for a cross-border transaction to be successful, these challenges have to be navigated. Some elite U.S. players in this area reckon that successful transactions are possible because of prior preparation, rational strategies, and deal structures that foresee the probable issues and concerns. For an inbound or outbound transaction to be successful, it is important to identify and address the legal issues (and other issues) in the initial stage or in some cases even overcome them. This article put forth the understanding of the issues (legal issues, in particular) in the cross border mergers and acquisitions, and indeed understanding the concept of cross border mergers and acquisitions.

Cross border M&A

Cross-border M&A refers to a transaction between two or more companies of different countries. It can also be referred to as an overseas merger and acquisition. In such a transaction, the assets and operations of two (or more) companies belonging to different nations combine to establish a new legal entity. This results in a transfer of the control of assets and operations from a local company to a foreign company; the former becoming an affiliate of the latter. On the basis of the flow of transactions, cross-border M&A can be categorised as Inbound (foreign businesses investing in India) or Outbound (Indian business making an investment abroad). Cross-border M&A aided by technological advancements, low-cost financing arrangements, and robust market conditions have made deal-makers confident and consider better growth strategies.

Risks and challenges posed by cross border merger and acquisitions

Substantial corporate earnings and company cash balance have motivated companies to mull over the springboard of global growth (cross-border M&A) and various development opportunities in business ventures. There are various advantages of cross-border transactions like expediting time to market, gaining access, scale, brand recognition, and mitigating competitive moves.

But like with every strategic decision, rewards come with certain risks. All jurisdictions do not offer stringent legal protections as various businesses have found to their costs as they might have expected in their homelands. Some businesses, despite knowing the potential rewards in cross-border transactions remain cautious in expanding their footprints: protecting moderate fortune at home rather than losing a larger part overseas.

The principal challenges which arise due to the general issues during such transactions are in terms of market assessment, regulatory evaluation, cultural fit, and deal structure evaluation. The specific challenges that arise during such transactions are:

- Imposition caps on foreign investments in the country where the target company is situated.

- Fetching relevant information about the target company might be an issue.

- There may be disclosure and reporting requests to be untangled and complied with.

- Complex tax structures

- The legal processes in the foreign land may be complex and not similar to those in the home country.

- The other country might have stringent labour laws and might have considerable obligations of consulting with unions and work councils.

- Costlier and complex due diligence process.

- Cultural differences and a difference in approach might lead to more nuanced negotiations.

- The probable requirement of regulatory clearance to further proceed with the deal as in, due to competition law and/or antitrust concerns.

- A possible conflict in the regulatory and/or taxation regimes of the countries.

- The expenses and length of complying with the target’s regulatory regime.

- Political challenges and government interference in the target’s company’s jurisdiction.

- There might be implicit challenges from politicians if the target provides a vital public service or a considerable number of jobs.

- A substantial increase in the operating costs due to the difference in the legal landscape might make the acquisition less profitable in the long run.

Advantages of cross border M&A

Despite the various challenges that crop up in a cross-border transaction, it is a mechanism that fosters the growth of the company and increases its shareholder value. Cross-border M&A provides easy access to new markets and customers. Following are the various benefits of a cross border transaction:

- Quicker and easy access to new markets.

- Enables companies to scale through acquisition.

- Provides for an expansion of brand recognition in various territories.

- Helps in absorbing a competitor.

There are various drivers of cross-border M&A. Such drivers mainly include saturation or slowdown in core markets and a need for diversification. Other important drivers include regulatory uncertainty in home markets and high repatriation costs of overseas earnings, technology, and productivity enhancement synergies.

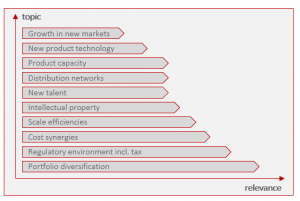

Considering the following factors, companies take the extra efforts of cross-border M&A transactions. But companies also consider the substantial rewards they can achieve from the particular target. Looking back in time, the most important reward was the diversification of the revenue streams of the companies; either in product diversification or geographic diversification (portfolio diversification). Apart from this, a regulatory environment that provides for investment protection or produces substantial tax benefits is another reward that can be considered (favourable regulatory environment).

An acquisition in a new market can help companies in becoming more cost-efficient by increasing sales (cost synergies). Apart from this, new markets provide for a new customer base and aid in scaling faster (scale efficiencies). Companies can also realise other rewards like access to new talents, adding new distribution networks, or securing new product technologies.

Legal risks involved in cross border transactions

Companies aiming at mergers and acquisitions cannot neglect the challenge of meeting the various legal and regulatory issues that they will probably face. Legislations pertaining to security, corporate, and competition are certain to diverge from each other. Legal Risk refers to the losses incurred due to unexpected control and sanctions. This happens mainly because the company did not comprehend the relevant laws of the host country after the success of mergers and acquisitions. This means that the legal risk has been running through the process of cross-border transactions right from the time of the foreign capital merger and acquisition of the host country.

When two entities from different countries merge they are obligated to abide by the legislation, rules, and regulations which differ considerably from one country to another, turning the entire process into a more complex and risky one. There may be instances of a company finding itself incompatible resulting in a deadlock as it so happened in the case of the merger of Sony and Columbia Pictures.

Therefore, before considering a deal it is necessary to go through the employment regulations, antitrust statutes and other contractual requirements to be dealt with. These laws play a crucial role while the deal is in process and also when the deal has been closed. While reviewing these concerns it might turn out that the potential merger and acquisition would not be compatible and hence it would be recommended to not go forward with the deal.

Considerations to mitigate risks in cross-border M&A

Cross-border M&A provides for considerable financial, market, and competitive value. Legal, political and regulatory challenges often have crucial impacts on cross-border M&A, so engaging a specialist team of corporate solicitors in the early stage would be a prudent step.

A successful cross-border transaction requires the executives to plan ahead, conduct thorough due diligence, and scrupulously operate the pre and post-deal execution. Following are the points which the executives and deal members must consider during the cross border M&A:

- Make sure that the whole M&A cycle is based on the deal thesis and deal objectives.

- To prevent the global challenges, adapt the deal methodology and playbook whenever needed.

- Combining pre-deal due diligence with pre-close planning activities to pre-empt handoff misses.

- The deal structure should be such as to meet the main objectives.

- Mention explicitly the overall integration scope, approach, and plan for achieving both initial and end-state goals.

- Curate a global integration program that has representation from both the target and acquirer pertinent to key workstreams and regions/countries.

- Pay attention to efficiently planning pre and post-close integration in detail, with dependencies, and critical path explicitly defined.

Conclusion

For a company to expand its footprints into a foreign market requires it to identify a suitable target, an effective execution of the transaction, and successful integration of the converging legal entities. However, as simple as it may seem, it presents a number of challenges and pitfalls. Quoting Andrew Sherman, a partner of Seyfarth Shaw LLP, “The current cross-border M&A landscape is robust, but with a few hints of caution. Most growing companies understand that being acquisitive in a wide variety of markets has become the new normal in strategic growth planning.”

This springboard of global growth has often exposed companies to numerous complex and mystifying challenges which require scrupulous navigation. These challenges may include: (i) political considerations and their implications;

(ii) legal and regulatory compliance challenges;

(iii) cultural and communication obstacles;

(iv) labour and employment problems;

(v) tax and accounting difficulties;

(vi) post-closing integration hurdles; and

(vii) antitrust and anti-competition concerns.

References

- “Cross-Border M&A: Rewards, Risks, and Integrated Transaction Management,” Finance Monthly | Monthly Finance News Magazine, n.d., accessed May 24, 2021, https://www.finance-monthly.com/2020/01/cross-border-ma-rewards-risks-and-integrated-transaction-management/.

- “M&A Beyond Borders: Opportunities And Risks,” Institute for Mergers, Acquisitions and Alliances (IMAA), March 8, 2008, accessed May 24, 2021, https://imaa-institute.org/ma-beyond-borders-opportunities-risks/.

- “Cross-Border M&A: Opportunities and Challenges,” Financier Worldwide, accessed May 24, 2021, https://www.financierworldwide.com/cross-border-ma-opportunities-and-challenges.

- “Top 10 Issues for Cross-Border M&A and Strategic Investments in 2013,” accessed May 24, 2021, https://www.dykema.com/resources-alerts-Top-10-Issues-for-Cross-Border-M-and-A-and-Strategic-Investments-in-2013_4-2013.html.

- “A Critical Analysis of Cross-Border Mergers and Acquisitions in a Global and Regional Perspective,” TaxGuru, accessed May 24, 2021, https://taxguru.in/corporate-law/critical-analysis-cross-border-mergers-acquisitions-global-regional-perspective.html.

- “Mergers and Acquisitions in the New Era of Companies … – EY / Mergers-and-Acquisitions-in-the-New-Era-of-Companies-Ey.Pdf / PDF4PRO,” PDF4PRO, last modified September 9, 2018, accessed May 24, 2021, https://pdf4pro.com/view/mergers-and-acquisitions-in-the-new-era-of-companies-ey-537099.html.

- Legal Aspects of Cross Border Transactions: Trends, Challenges and Opportunities (Thomson Reuters, 2016), accessed May 24, 2021, https://www.legalexecutiveinstitute.com/wp-content/uploads/2016/09/Trends-in-cross-border_Report.pdf.

Students of LawSikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications