This article is written by Shreya S.K Pandey, a student of Law College Dehradun Faculty of Uttaranchal University. In this article, she discussed the Demand and Recovery under Goods and Services Tax (GST), how the Government recovers the tax and how the proceeding is initiated in case of no/short payment of tax.

Table of Contents

Introduction

Goods and Services Tax (GST) is a system where one person determines the tax and pay the tax by self-assessment. When the tax is paid by doing self-assessment, there is likely to be a chance that the tax may be short paid without any malice intention or there may be also a chance that the assessees may pay the tax short intentionally or knowingly. Under such circumstances, there are some provisions which are followed by the authority to recover those taxes which are short paid by assessees intentionally or without intention.

Under Chapter XV from Section 73 to Section 84 of the Central Goods and Services Tax Act, 2017, The provisions relating to Demand and Recovery under Goods and Services Tax (GST) has been discussed. The process of recovery of GST starts with the issuance of the show-cause notice and end up in the Adjudication proceedings.

Central Goods and Services Tax (GST) Act, 2017, authorizes the proper offices to demand and determine the amounts:

- A tax which is not paid (Section 73 and Section 74)

- A tax which is short paid (Section 73 and Section 74)

- A tax which is erroneously refunded (Section 73 and Section 74)

- Wrongly availed Input Tax Credit (Section 73 and Section 74)

- Wrongly utilized Input Tax Credit (Section 73 and Section 74)

- A tax which is collected but not paid (Section 76)

- A tax which is collected beneath the wrong head (Section 77)

What is Demand and Recovery under GST?

Demand means the wish or desire of a consumer to get or acquire goods or services. When there will be more demands, the market will flourish. It is an action that leads to the growth of the economy. The government imposes a tax on every goods and service. Every person is liable to pay the tax to the Government when they purchase the goods. When a person fails to oblige with his duty, the Government has to recover the tax from the defaulter. Tax is the basic source for the Government to run the economy of the country failing in which causes the economic imbalances. The government adopts strict measures to recover the tax from the defaulters.

Issuance of Demand Notice

Demand notice is a notice which is sent by the authority under Goods and Service Tax (GST) to communicate its taxpayers.

Section 73:- Determining the tax which is Short or Not Paid or Refunded Erroneously

Section 73 of Central Goods and Services Tax (CGST) Act, 2017, deals with the determination of those taxes which are short paid or not paid or which is erroneously refunded

When any tax has been short paid by the assessee or has not been paid or refunded erroneously and where Input Tax Credit has been wrongly utilized or availed for any of the reason which does not include reason of any wilful-misstatement or fraud or any suppression of tax due to its evasion and it comes to the notice of the proper officer, he will send him a notice to show cause why he should not pay the amount of tax mentioned in the notice along with the interest. He will also state the assessee to pay the penalty which is levy upon him.

Time Period: The notice served by the proper officer shall be served three months before the issuance of an order under sub-section (10) of Section 73.

Service of Statement: When the notice to be issued by the proper officer under sub-section (1), he will serve a statement to the person who is liable to pay the tax. The statement will include all the details relating to the taxes which are either short paid, or not paid, or erroneously refunded or where the input tax credit is utilized or availed for a period which does not include those as mentioned in sub-section (1).

Service of the statement shall be deemed to be the service of notice when the grounds upon which the tax period has relied shall be the same as in the previous notice to the assessee.

If the person to whom notice has been served pays the tax including the interest on that tax within a period of thirty days from the date of issue of the notice, the penalty shall not be imposed and all the proceedings against that person relating to the notice shall be considered as complete.

After representation by a person who is liable to pay the tax, the proper officer shall take this into account and determines the interest, taxes, and a penalty equal to 10% of the tax or Rs.10,000 (whichever shall be higher) which is due from the person liable to pay the tax. After this, the proper officer shall issue an order.

Adjudication and limitation for the recovery of tax

- If the case is related to the non-fraud, the case shall be adjudicated within a period of three years. The limitation shall be counted from the date of filing of the annual returns for the prevailing financial year.

- If the case is related to the erroneous refund that is received by the assessee, in such circumstances the case shall be adjudicated within a period of three years. The limitation for the three years shall begin from the date when the erroneous refund was credited in the account of an assessee.

- The issuance of notice for the recovery of tax shall be made by the proper officer three months before the time limit for the verdict of the issue of order or case.

- The order of decision shall be issued within three years from the date of furnishing the annual return for the financial year by the proper officer.

Section 74:- Determining the Tax which is Short or Not Paid or Refunded Erroneously and Input Tax Credit has been availed due to Fraud, Wilful-misstatement or Suppression of Facts

Section 74 of Central Goods and Services Tax (CGST) Act, 2017, deal with the determination of those taxes which are short paid or not paid or which is erroneously refunded and Input Tax Credit has been wrongly utilized or availed for any of the reasons which include wilful-misstatement or fraud, etc.

When any tax has been short paid by the assessee or has not been paid or refunded erroneously and where Input Tax Credit has been wrongly utilized or availed for any of the reasons which include wilful-misstatement or fraud or any suppression of tax due to its evasion and it comes to the notice of the proper officer, he will send a notice to the person has wrongly utilised or availed the Input Tax Credit to show cause why he should not pay the amount of tax mentioned in the notice along with the interest. He will also state the assessee to pay a penalty equal to the tax which is levy upon him in the notice.

Time Period: The notice served by the proper officer shall be served six months before the issuance of an order under sub-section (10) of Section 73.

Service of the Statement: When the notice to be issued by the proper officer under sub-section (1), he will serve a statement to the person who is liable to pay the tax. The statement will include all the details relating to the taxes which are either short paid, or not paid, or erroneously refunded or where the Input Tax Credit is utilized or availed for a period which does not include those as mentioned in sub-section (1).

Service of the statement shall be deemed to be the service of notice when the grounds upon which the tax period has relied shall be the same as in the previous notice to the assessee.

Person to whom tax is chargeable may pay the sum of the tax including the interest which is equal to 15% of the tax, after determining the tax on his own or by the proper officer. After this, he has to inform the proper officer in writing about that payment.

Adjudication and limitation for recovery of tax

- When the case deals with the suppression of facts or fraud, the case shall be adjudicated within a period of five years. The limitation shall be counted from the date of filing of the annual returns for the prevailing financial year.

- If the case is related to the erroneous refund that is received by the assessee, in such circumstances the case shall be adjudicated within the period of five years. The limitation for the three years shall begin from the date when the erroneous refund was credited in the account of an assessee.

- The issuance of notice for the recovery of tax shall be made by the proper officer three months before the time limit for the verdict of the issue of order or case.

- The order of decision shall be issued within five years from the date of furnishing the annual return for the financial year by the proper officer.

Penalty and Interest under Goods and Services Tax

|

Sr. No. |

Situations |

Section 73 of the Central Goods and Services Tax, 2017. |

Section 74 of the Central Goods and Services Act, 2017. (Case of suppression or fraud or misstatement) |

|

1. |

Before show cause notice is issued |

There shall be no-issuance of penalty or notice and the taxpayer pays the due tax including the interest which is applicable. |

There shall be no-issuance of notice and the taxpayer pays the due tax including the penalty and interest @15% of the amount due on a tax |

|

2. |

Aftershow cause notice is issued |

A taxpayer is required to pay the due tax within the period of 30 days from the issue of show cause notice along with the interest which is applicable and there shall be no penalty after the payment of due tax. |

A taxpayer is required to pay the due tax along with the interest and penalty @25 |

|

3. |

After an order is issued |

A taxpayer may avoid the prosecution even after the issuance of the order if he will pay the interest, tax or penalty on time. |

A taxpayer pays tax including the penalty and interest @50% of the due amount of tax. After the payment of due tax, the proceeding shall be deemed to be completed. |

|

4. |

Other Cases |

A taxpayer is required to pay the due amount of tax along with penalty and interest equal to of @10% of the due amount tax or Rs. 10,000 (whichever is higher) within 30 days from the communication of the decision. |

A taxpayer is required to pay the due tax along with the penalty and interest @100% of the due amount of tax. |

Note:-

- When any tax which is self-assessed is paid or any amount which is collected as a tax is paid along with the interest within 30 days from the due date, the penalty shall not be charged.

- The amount of interest, penalty, and tax which is demanded in the decision shall not exceed the amount mentioned in the notice. And, the demand shall have the same ground as mentioned in the notice.

Section 76:- Tax which is collected but not paid to the Government

Section 76 of the Central Goods and Services Tax (CGST) Act, 2017, deals with the taxes which are collected by a person but not paid to the Government.

If a person collects from any other person the amount of tax and has not paid it to the Government have to pay the amount of tax to the Government irrespective of the fact that the goods or services upon which the tax was collected are taxable or not.

If any person, who is liable to pay the tax to the Government fails to do so, then the proper officer may serve a notice to that person asking him to show cause why he should not pay the amount as mentioned in the notice and why he should not pay a penalty equal to the amount mentioned in the notice.

The person will pay the amount after the due amount shall be determined by the proper officer after his representation. Following the principle of Natural Justice, the opportunity of being heard shall be provided to the person by the proper officer on his requests in writing.

Adjudication and limitation for recovery of tax

- The order shall be issued by the public officer within one year from the date of issuance of the notice.

- When the appellate court had put a stay on the issuance of an order by the public office, then the limitation period shall exclude the period of stay for the purpose of computing the time period of one year.

Rule 142:- Order and Notice of Demand

Rule 142 of Central Goods and Services Tax (CGST) Rules, 2017 deals with the issuance of order and notice of demand which is required to be paid by the person upon whom the liability has been imposed to pay the tax.

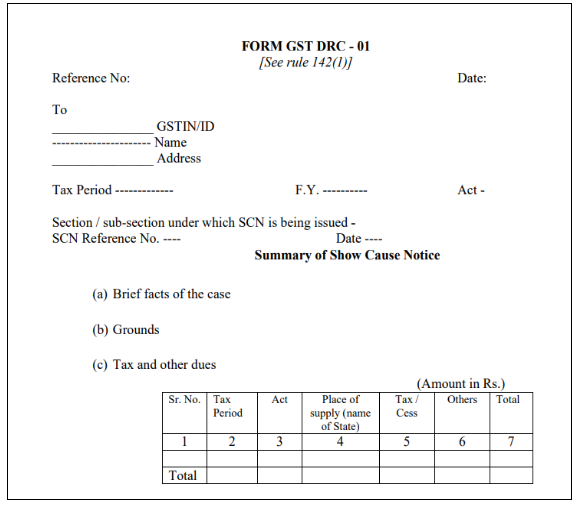

A proper officer is required to serve a summary in an electronic manner along with the notice under Section 73(1) or Section 74(1) or Section 76(2) in FORM GST DRC-01, stating the details a payable sum.

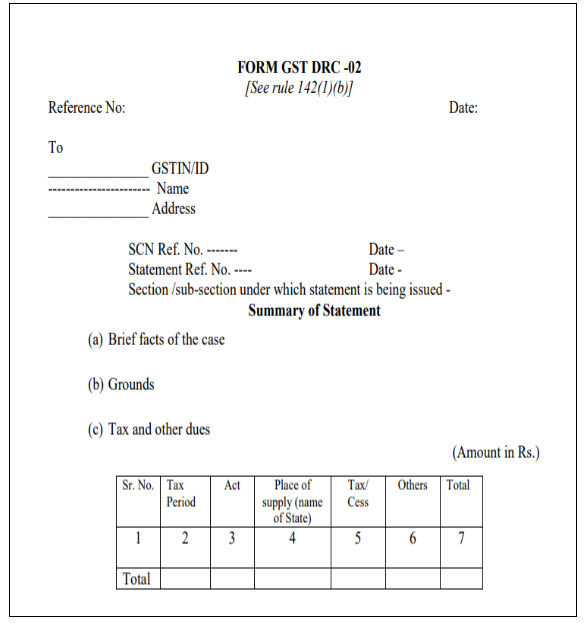

A proper officer is also required to serve a summary in an electronic manner along with the statement under Section 73(3) or Section 74(3) in FORM GST DRC-02, stating the details of the payable sum.

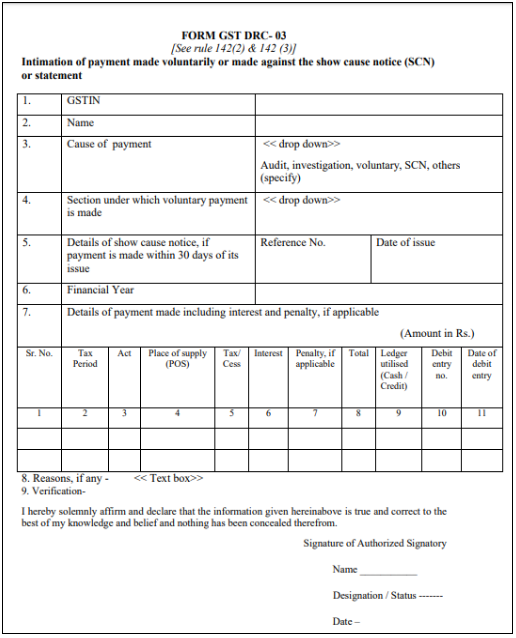

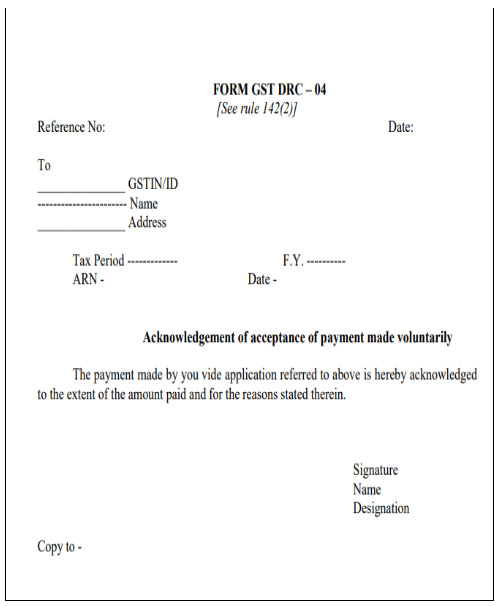

If a person who is liable to pay the tax makes the payment of interest and tax in compliance with Section 73(5) or tax, interest or penalty in compliance with Section 74(5) before the statement or notice may be served to him, he is required to inform about such clearance of dues to the proper officer in FORM GST DRC-03. When a proper officer receives such information, he will accept the payment made by the defaulter taxpayer and he may issue an acknowledgment stating that he had accepted the payment given by the taxpayer in FORM GST DRC-04.

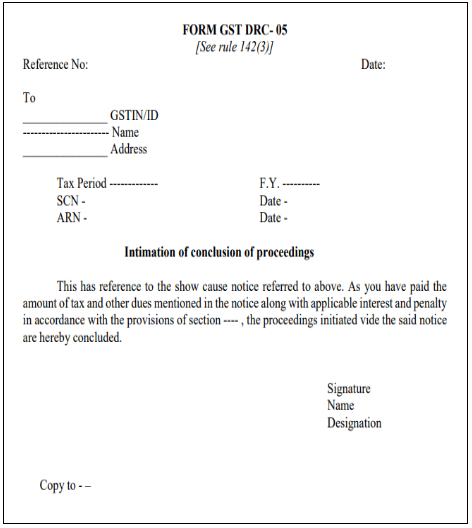

When a person upon whom the liability to pay the tax has been imposed pays the tax under Section 73(8) of interest, penalty or tax under Section 74(8) within the period of 30 days from the date when notice was served, the person is required to inform about this to the proper officer in FORM GST DRC-03 and after the issuance of the order in FORM GST DRC-05, the proper officer shall conclude the proceedings.

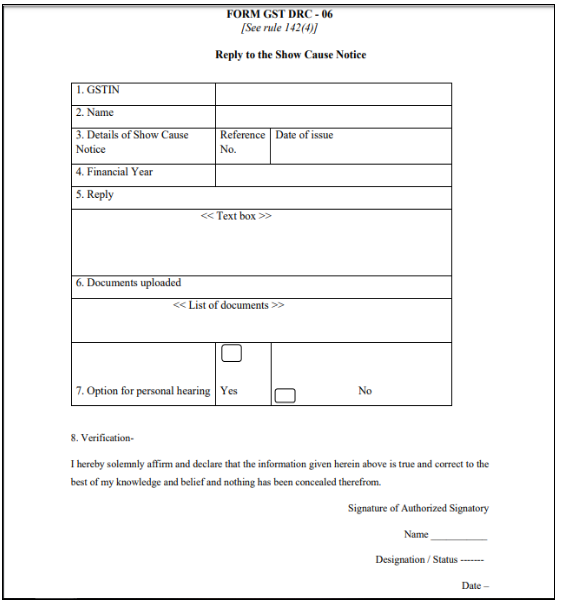

When a person who is liable to pay the tax represents himself under Section 73(9) or Section 74(6) or Section 76(3), that representation made by such person may be in FORM GST DRC-06.

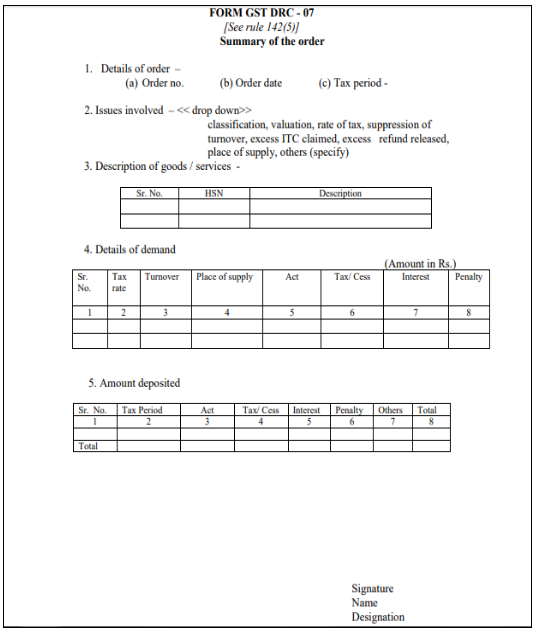

When the issuance of order is done in summary under Section 73(9) or Section 74(9) or Section 76(3), it is required that it shall in FORM GST DRC-07. It shall state the sum of interest, penalty or tax that a person is liable to pay. Issuance of the order shall be a recovery notice.

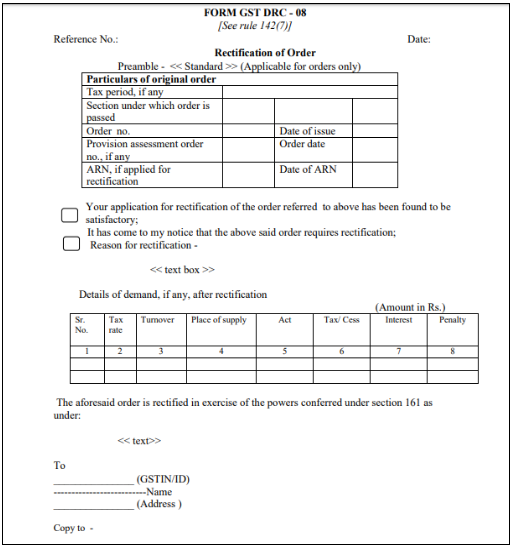

When a proper officer may correct the order in compliance with Section 161 of the Central Goods and Services Tax Act, 2017, it shall be done by the proper officer in FORM GST DRC-08.

Section 75: General Provisions regarding Determination of Tax

Section 75 of the Central Goods and Services Tax Act, 2017, deals with the provisions regarding the determination of tax.

When Appellate Court stays the issuance of the notice or order by the public officer, for computing the limitation period under Section 73(2) and Section 73(10) or Section 74(2) and Section 74(10), the period till the issuance of notice or order are under stay shall be excluded.

When the charges under Section 74(1) relating to the willful misstatement or fraud or suppression of facts to escape the tax did not establish against the person to whom notice has been issued by the public officer in the Appellate Court or Tribunal and the court will remove those charges, the notice shall be treated as a notice under Section 73(1).

When Appellant Court or Tribunal passes any direction and an order is required to pass in relation to that direction then such order shall be passed within two years from the date when the direction was one communicated.

When any adverse decision is pronounced against the person liable for tax or penalty or where he gives in writing, an authority may provide him with an opportunity of being heard. And if he shows sufficient cause to satisfy the proper officer, his hearing may be adjourned or time may granted to him.

When the amount of the tax, penalty, and interest is outlined in the order it shall not exceed the amount that was mentioned in the prior notice. Moreover, the grounds in the decision or order and the grounds in the notice must be the same.

If the order does not talk about any interest in the short/not paid tax, the taxpayer is still liable to pay the interest on taxes. If the court does not come up with a judicial decision in the three years under Section 73(10) or five years under Section 74(10) then the proceeding shall be deemed to be concluded.

If a court has imposed a penalty upon a person under Section 73 or Section 74, then no subsequent penalty shall be imposed upon that person under any provision of Central Goods and Services Act,2017, for the same act or omission.

Section 78: How Recovery Proceedings are Initiated

Section 78 of Central Goods and Services Tax, 2017, talks about the consequences of not paying the tax after the order has been made by the court.

If a notice has been issued to a person to pay tax and subsequently an order has been issued by the court against that person to pay the tax then that person is required to pay the tax within three months from the date when the first service of an order has been made. If that person fails to pay the tax within three months, recovery proceedings will be started against that person.

The proviso of Section 78 deals with a situation where it is desirable to the proper officer in the sale of revenue that the person should pay tax before the three months prescribed to him, then he may direct the person to pay the tax before the time period after recording his reasons in writing.

Section 79: Tax Recovery

Section 79 of Goods and Services Tax Act, 2017, deals with the provisions relating to the recovery of tax when the person fails to pay tax to the Government.

- If a person does not pay the tax to the Government which he is required to pay under the Central Goods and Services Tax Act, 2017, then it shall be recovered by the proper officer by any of the modes as prescribed:-

- If the proper officer or any other specified officers are holding the money which is unpaid to the defaulter or overdue against such person, then the proper officer or any other specified officer by the proper officer will deduct the amount of tax from that money.

- If the proper officer or any other specified officer is in control of any goods which belong to the person who is required to pay the tax, then that goods may be sold or detained by the proper officer or any other specified officer.

- If some person holds due money of the person who is liable to pay the tax under this Act, than the proper officer may require that person holding due to the taxpayer to pay the tax to the Government equivalent to the money due irrespective of the fact that whether it is equal to the due tax or equal to it. A person to whom the notice has been issued in the previous clause is bound to obey the notice. If the person to whom notice has been issued fails to pay the due tax to the Government, he will be considered as a defaulter in relation to the amount specified in the notice and he has to follow the consequence prescribed in the Act or Central Goods and Services Tax Rule, 2017. The proper officer who is issuing the notice may revoke it or amend the notice or even he may extend the time for the payment of tax in respect of notice.If a person, who has due money of the taxpayer pays the tax on behalf of defaulter taxpayers, it shall be regarded as a sufficient and valid discharge from the liability by that person in relation to the money due to the extent mentioned in the receipt by the Government. Now, as money has been credited to the Government account, he is not required to pay his due money to the taxpayer. This clause makes the person, to whom notice has been issued, personally liable to the extent he has due money of the defaulter taxpayer. If the person to whom notice has been issued under this clause proves to the proper officer and if proper officer is satisfied that the money is not due or he does not hold any money against the person who is defaulter taxpayer, then nothing shall make that person liable to pay the tax on behalf of that person to the Government.

- The proper officer has power under this Section to detain any property, whether movable or immovable, forcefully belonging to the defaulter taxpayer until he pays the amount which is due. Even after the detention of property, if the payment is not made within a period of thirty days, then the property may be a sale by the authority. Tax due will be paid from the money received after the sale of the property and any surplus money will be provided back to the taxpayer.

- The proper officer may even prepare a certificate under his signature and send it to the collector of the district where the property of the defaulting taxpayer lies specifying the amount due from that person and the collector will move to collect the amount from that person as if the amount as arrears of land revenue.

- If in case, the defaulter lives in a jurisdiction other than that of the proper officer, then the proper officer may file an application and send it to the magistrate appropriate in this behalf. And that magistrate will recover the amount specified as if the amount is imposed as fine by fine.

2. If the tax, penalty or interest which is required to be paid under the Central Goods and Services Tax, 2017, or Central Goods and Services Tax Rule, 2017, to the Government remains unpaid then the proper officer of the Union territory tax or State tax may recover those arrears from the taxpayer as if those arrears belongs to the Union territory tax or State tax and then credit it to the Government’s account.

Click Here

Rule 143:- When tax is recovered by deducting the amount from owed money

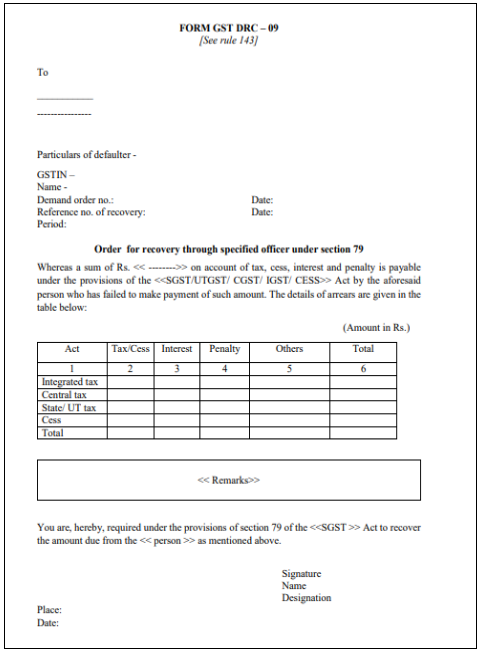

Rule 143 of the Central Goods and Services Tax Act, 2017, deals with the recovery process when tax is recovered by the Government from the defaulter taxpayer by making a deduction from the money owed.

When a defaulter taxpayer, who is liable to pay the tax to the Government, does not pay the tax then, the proper officer will ask the specified officer, in FORM GST DRC-09, to deduct the sum from the money which is unpaid or due against such defaulter person in compliance to Section 79(1)(a).

Specified Officer:- Specified Officer is an officer of the Government belonging to the UnionTerritory or the Central Government or the State Government or the local body (authority). Specified Officer may be an officer of the Corporation or a Board or a Company controlled or owned by the State Government or the Central Government or the local authority or the Government belonging to the Union Government whether wholly or partly.

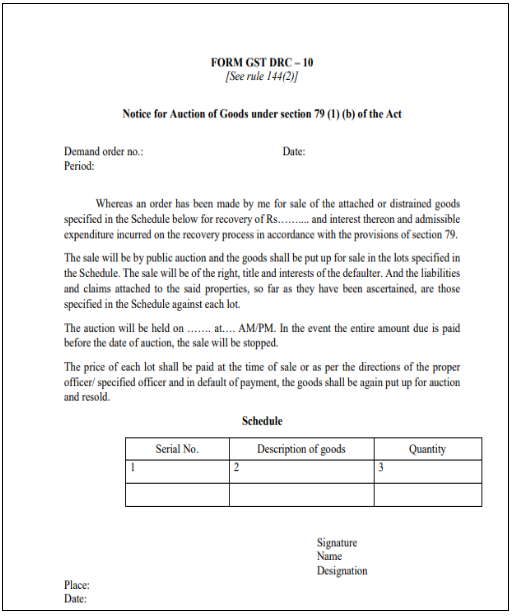

Rule 144. Recovery of tax by auction

Rule 144 of the Central Goods and Services Tax Act, 2017, deals with the situation where the proper officer may sell the goods by auction to recover the tax from the defaulter person.

When a person liable to pay the tax fails to do so, then the amount of tax will be recovered from the goods owned by that person. The goods shall be sold in compliance with Section 79(1)(b). It is the duty of the proper officer to estimate the market value and make an inventory of the goods required to be sold and begin with the procedure of to sell that much of goods through which the tax amount may be recovered along with the expenditure incurred by them in selling the goods.

The goods belonging to the defaulter taxpayer shall be sold by auction or by e-auction. When the method of e-auction is adopted, a notice in FORM GST DRC-10 is issued which will show the property and the purpose behind making a sale. In no case, the last date of auction or submission of a bid shall be prior to fifteen days from the date when the notice was issued for the auction.

If goods from which the amount of tax is required to be recovered is of perishable and hazardous nature and the expense to maintain that goods exceed its actual value then the proper officer may sell it without any delay.

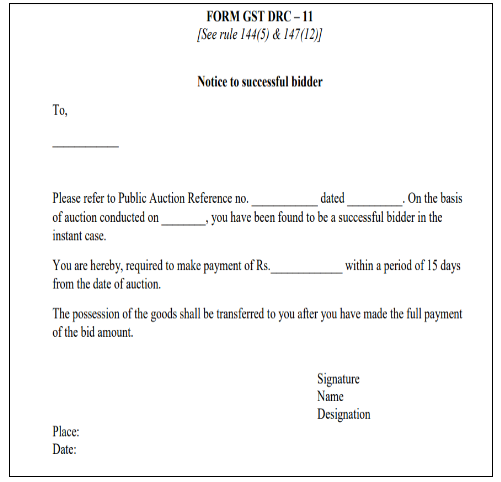

All the bidders have to make a mandatory deposit of amount (pre-bid) to get eligible for the purpose of participating in the auction. If bidders fail to get the goods, the pre-bid deposit shall be refunded to them. Where a successful bidder who is liable to pay the whole amount of goods after auction fails to do so, then he will lose the pre-bid deposit as a penalty.

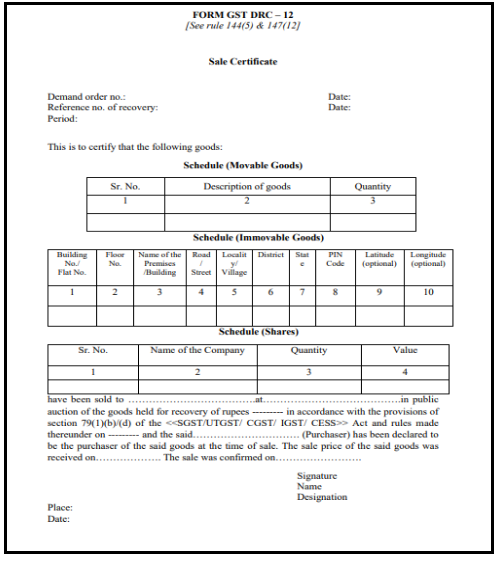

When a person is successful in getting the goods through auction then it is liability of proper officer to supply notice in FORM GST DRC-11 to that successful bidder. He will ask him to make full payment of the goods in fifteen days from the day when the auction was conducted. When the amount is fully paid by the successful bidder, the proper officer will transfer the property to him and a certificate will be issued in FORM GST DRC-12.

Where the defaulter pays all the recovery amount of the tax including the amount which is incurred during the recovery of tax, then the proper officer will order to release the goods and he will not conduct the auction.

If the proper officer will receive no-bid, he will conduct the auction again or may cancel it where the auction is considered to be non-competitive due to less bid or less participation.

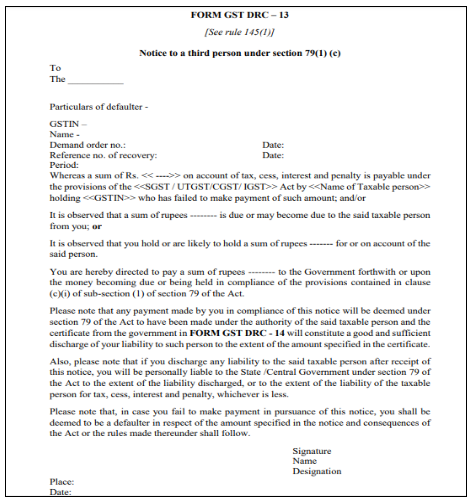

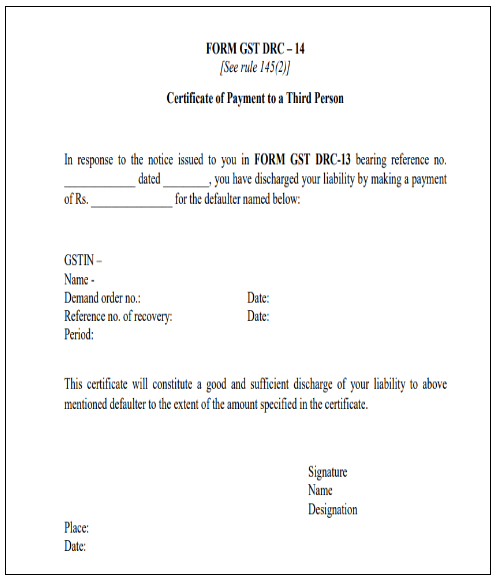

Rule 145:- Tax recovery from the third person

Rule 145 of the Central Goods and Services Tax Rule, 2017 deals with the situation where proper officers recover the tax from the third person. The third person will pay the tax on behalf of the defaulter.

A notice in FORM GST DRC-13 will be served by the proper officer to the third person under Section 79(1)(c) directing him to pay the sum which is mentioned in the notice.

After the payment of the amount mentioned in the notice by the third person which is served to him by the proper officer, a certificate will be issued to him by the proper officer in FORM GST DRC-14 which will state the description of the responsibility so discharged by him.

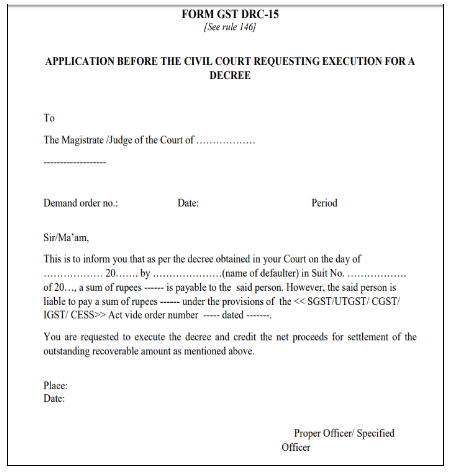

Rule 146:- Execution of Decree for the recovery of tax

Rule 146 of the Central Goods and Services Tax Rule, 2017, deals with the execution of the decree by the civil court to recover the tax.

While the execution of the decree for sale or payment of money for enforcing the charge or mortgage if the defaulter is receiving money through this then a request in FORM GST DRC-15 will be sent by the proper officer to the court. Court will execute the decree and tax money will be recovered by them through the net proceeds of the decree.

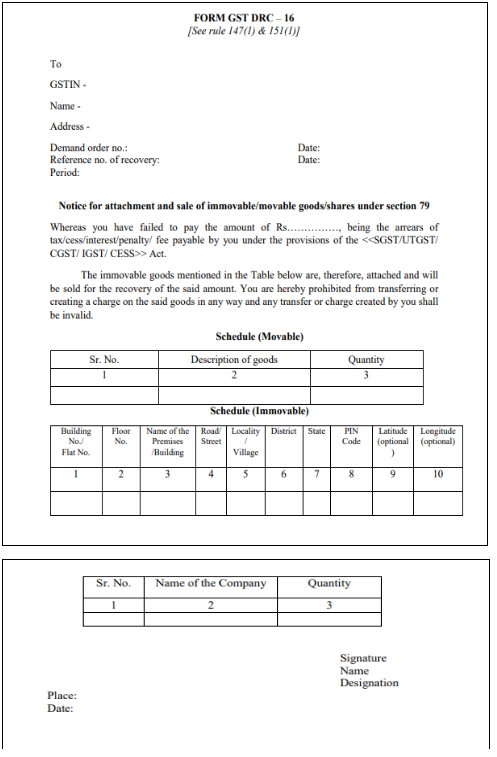

Rule 147:- Attachment of movable or immovable property for recovery of tax

Rule 147 of the Central Goods and Services Tax Act, 2017, deals with the recovery of the tax from the defaulter by attaching the immovable and movable property belonging to him.

There shall be attachment or seizure of the property belonging to the defaulter after the proper officer makes a list stating defaulter’s immovable and movable property. A proper officer will estimate the market value of the property and order to seize or attach it. He will pass a notice in FORM GST DRC-16. The notice of sale will prohibit any kind of transaction in relation to that immovable and movable property which is necessary for the recovery of the due amount.

Rule 151 of the Central Goods and Services Tax Rule, 2017, describes the manner of attachment of those property which is a share in any corporation, any debt which is not secured by any kind of negotiable instruments or the movable property which is not in the defaulter’s possession excluding the property which is in the court’s custody.

A copy of the decision of seizure or attachment of property will be delivered to the Transport Authority or Authority of Revenue or other Authorities which will impose restrictions or incumbrance on the attached property of the defaulter whether immovable or movable. Restrictions and incumbrance shall be set aside only when the proper officer will give written directions.

When the property which is attached or seized under this Section is-

- An immovable property, then the order or decision of the court shall be affixed in the immovable property till the sale is confirmed;

- A movable property, then the property will be seized by the proper officer according to the provisions of Chapter XIV of Central Goods and Services Tax Act, 2017, and the proper officer or other officer authorized by him will take custody of that movable property.

The goods belonging to the defaulter taxpayer shall be sold by auction or by e-auction. When the method of e-auction is adopted, a notice in FORM GST DRC-17 is issued which will show the property and the purpose behind making a sale.

If the property which is required to be sold for the purpose of generating the recovery amount is negotiable instrument or corporation share then the public officer gives it to the broker for selling it instead of selling it through public auction. The broker will sell it and pay the amount generated through such sale to the Government to extend the amount of tax after taking his commission. After recovering the tax and reducing his commission from the amount, the broker will hand over to the remaining amount to the instrument’s owner.

All the bidders have to make a mandatory deposit of amount (pre-bid) to get eligible for the purpose of participating in the auction. If bidders fail to get the goods, the pre-bid deposit shall be refunded to them. Where a successful bidder who is liable to pay the whole amount of goods after auction fails to do so, then he will lose the pre-bid deposit as a penalty.

In no case, the last date of auction or submission of a bid shall be prior to fifteen days from the date when the notice was issued for the purpose of the auction. If goods from which the amount of tax is required to be recovered is of perishable and hazardous nature and the expense to maintain that goods exceed its actual value then the proper officer may sell it without any delay.

When a person is successful in getting the goods through an auction then it is liability of proper officer to supply notice in FORM GST DRC-11 to that successful bidder. He will ask him to make full payment of the goods in fifteen days from the day when the auction was conducted. When the amount is fully paid by the successful bidder, the proper officer will transfer the property to him and a certificate will be issued in FORM GST DRC-12. The certificate will contain the details about the property, details about the bidder, the date on which the property is transferred, an amount which is paid and after the certificate is issued the right, interest, and title which is transferred in property to the bidder.

If in case, there are two highest bidders among which one is the co-owner of the property, then the property will be transferred to him.

The person to whom property is transferred will pay the Government an amount which will include the tax, stamp duty, and fees relating to the property transfer.

Where the defaulter pays all the recovery amount of the tax including the amount which is incurred during the recovery of tax, then the proper officer will order to release the goods and he will not conduct the auction.

If the proper officer will receive no-bid, he will conduct the auction again or may cancel it where the auction is considered to be non-competitive due to less bid or less participation.

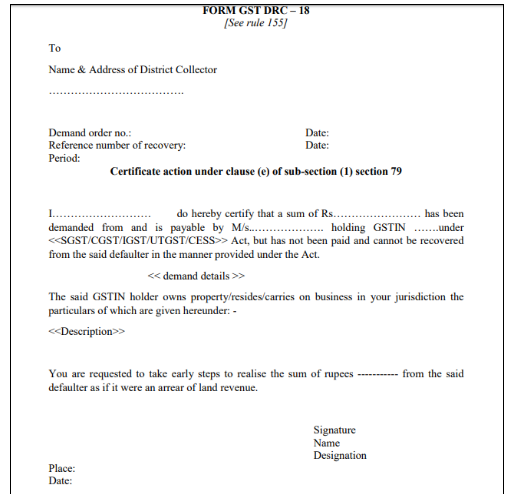

Rule 155:- Recovery of tax by the Collector, etc.

Rule 155 of the Central Goods and Services Tax Rule, 2017, deals with the process of recovery of the tax from the defaulter by the Collector, Deputy Commissioner or other officers.

Collector or Deputy Commissioner of a district or other officers will recover the tax amount from the taxpayer when the proper officer will authorize him by issuing a certificate in FORM GST DRC-18. This rule is invoked when the amount of tax is required to be recovered according to Section 79(1)(e). Collector or Deputy Commissioner will recover the amount mentioned in a certificate from the defaulter as if the amount as arrears of land revenue.

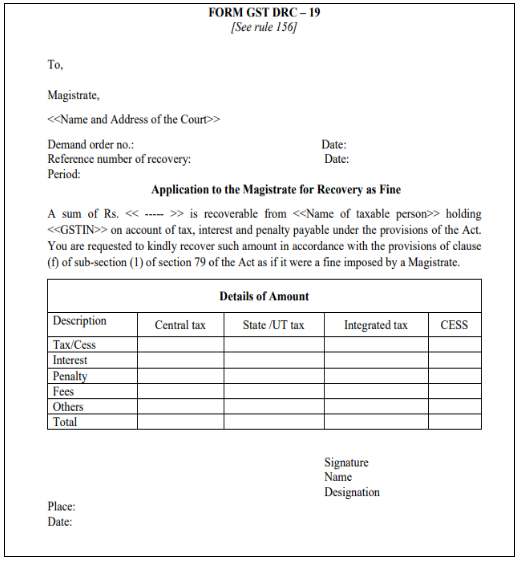

Rule 156:- Recovery by a criminal court

Rule 156 of the Central Goods and Services Tax Act, 2017 deals with the scenario where a proper officer will impose the liability upon magistrates to recover tax through the provisions of the Code of Criminal Procedure, 1973.

When it is considered that the due tax must be collected as a penalty or fine imposed through the Code of Criminal Procedure, 1973, then the magistrate will work in compliance with the application given to him by the proper officer. An application made on this behalf by the proper officer will be in FORM GST DRC- 19. After receiving an application the magistrate will recover the amount as if it was a fine instituted by him upon the defaulter.

Rule 157:- Recovery from the surety

Rule 157 of Central Goods and Services Tax Rule, 2017, deals with when another person will be liable for defaulter’s act.

If a person has been made a surety for the defaulter’s due amount, then all proceedings under this Chapter shall be initiated against him as if he had not paid the tax.

Section 77: Tax Which are Wrongfully Collected and which is paid to Central or State Government

Section 77 of Central Goods and Services Tax, 2017, deals with the taxes which are collected wrongfully and credited in the account of the Central Government or State Government.

If a registered person pays a Central tax and State tax or if he pays Central Tax and Union Territory tax considering it to be an intra-state transaction, but it is an inter-state transaction than the amount of tax paid by him shall be refunded to him in a manner prescribed.

Now, if a registered person pays the integrated tax considering it to be an inter-state transaction, but which is an Intra-state transaction than that person is not liable to pay the interest on the State tax and the amount of Central tax or Union Territory tax and Central tax.

|

Payment of tax by Registered Person |

Actual Transaction |

What is Refunded? |

If any interest? |

|

Payment of State tax and Central tax or Payment of Union Territory tax and Central tax, considering the transaction to be intra-state supply |

Where an actual transaction is an Inter-state supply |

Refund of State tax and Central tax or Union tax or Central Territory tax under Section 77(1) of the Central Goods and Services Tax Act, 2017. |

There shall be no interest in the Integrated Tax payment under Section 19(2) of the Integrated Goods and Services Tax Act, 2017. |

|

Payment of Integrated Tax, considering the transaction to be Inter-state supply |

Where an actual transaction is an Intra-state supply |

Refund of Integrated Tax under Section 19(1) of the Integrated Goods and Services Tax Act, 2017. |

There shall be no interest on the Central/State Tax and Union/Central Tax under Section 77(2) of Central Goods and Services Tax Act, 2017. |

Section 54: Tax Refund

Section 54 of Central Goods and Services Tax Act, 2017, deals with the process of the Refund of Taxes.

If a person claims a refund of any interest and tax from the Government, then he may write an application to the authority within the two years from the date prescribed under that form.

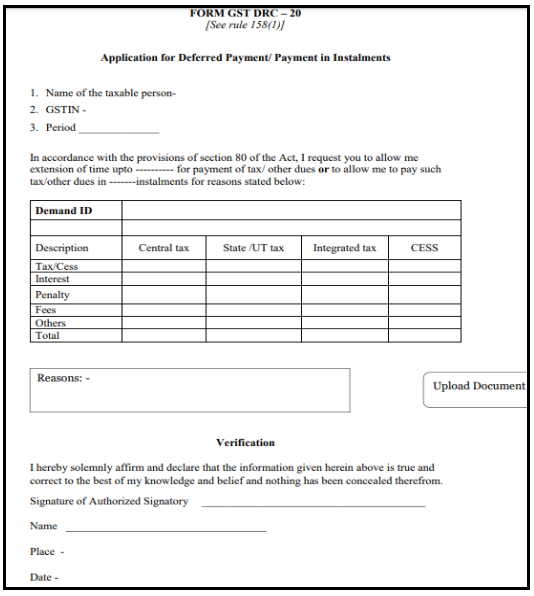

Section 80: Tax Payment and Payment of Other Amount in Monthly Instalments

Section 80 of the Central Goods and Services Tax Act, 2017, deals with the payment of tax by using the mode of monthly installments.

If a person, who is liable to pay the tax, files an application to the commissioner to extend the time for paying off the tax or to allow him to pay the tax or any due amount under this Act in monthly installments, the Commissioner may allow him to pay the tax in installments not exceeding twenty-four after recording his reasons in writing.

Section 121(d) of the Central Goods and Services Tax Act, 2017, deals with the decisions and orders which are not appealable. There lies no appeal against the decision or order of the Commission where he does not allow the payment of tax in installments or where he is allowing the payment of tax in the lesser installments.

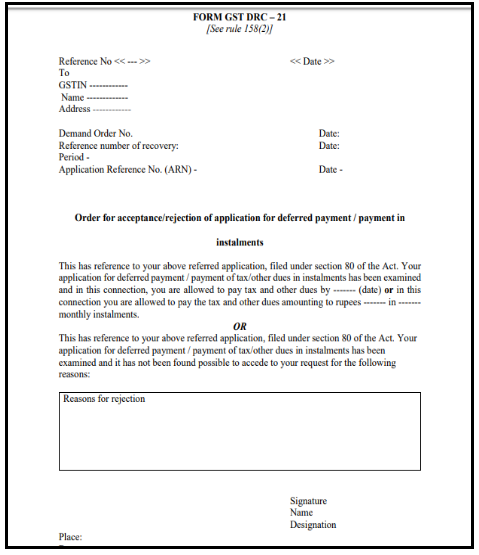

Rule 158:- Tax Payment and Payment of Other Amount in Monthly Instalments

Rule 158 of Central Goods and Services Tax Rule, 2017, deals with the request for making the late tax payment or for making the payment through installments in FORM GST DRC- 20.

When the person who wants to pay the tax in installments file this form using electronic means for the purpose of paying the taxes in monthly installments or for extension of the period to pay the tax, the commissioner will ask the jurisdictional officer to submit a report about the financial ability of the person who is liable to pay the tax.

When commissioner will consider the request of the person who is liable to pay the tax after taking the report from the jurisdictional officer, the commissioner may allow the taxpayer to pay the tax in monthly installments and exceeding the twenty-four installments or may provide him further time to make the payment of the tax. The commissioner may allow this by issuing an order in FORM GST DRC- 21:

When late payment or payment through installments is not accepted-

- When the taxpayer had already made default in paying the amount under this Act or Union Territory Goods and Services Act, 2017 or Integrated Goods and Services Tax Act, 2017 or State Goods and Services Tax Act, 2017, and the proceedings under this is going on.

- When his request to pay the tax in installments has been rejected in the previous financial year under this Act or Union Territory Goods and Services Act, 2017 or Integrated Goods and Services Tax Act, 2017 or State Goods and Services Tax Act, 2017.

- The request for the amount to pay in installments in less than rupees twenty-five thousand.

Section 81: When Transfer of Property is considered to be Void

Section 81 of Central Goods and Services Tax Act, 2017, deals with-

If a person with an intention to defraud the Government revenue transfers his property by means of sale, exchange, mortgage or by any other way or creates charge upon the property, such transfer of property by any mode or creation of charge shall be considered as a void against the claim in relation to the tax payable by that person.

Exception: when the transfer of property and creation of charge is done due to the reason as follows, it shall not be considered as void –

- Good Faith

- Without knowledge of the pendency of proceedings.

- When previous permission has been taken from the proper officer.

- Without any knowledge that a liability has been imposed upon him to pay the tax.

Section 82: Tax to be Charge on Property

Section 82 of Central Goods and Services Tax Act, 2017, says that-

When a person is required to pay the tax, penalty or interest to the Government, it shall be the first charge on the property of the person liable to pay the tax. Nothing in this Section shall affect the provisions given in Insolvency and Bankruptcy Code, 2016.

Section 83: Provisional Attachment to the Property

Section 83 of the Central Goods and Services Tax Act, 2017, deals with the attachment of property provisionally.

If the commissioner is of the opinion that the property of the taxpayer must be attached provisionally including bank accounts to protect the interests of the Government revenue, he may order in writing to attach the property provisionally. This order shall be given by the Commissioner when the proceeding under Section 62 or Section 63 or Section 64 or Section 67 or Section 73 or Section 74 is pending

Rule 159: Attachment of property provisionally

Rule 159 of Central Goods and Services Tax Rules, 2017, is read along with Section 83 of Central Goods and Services Tax Act, 2017.

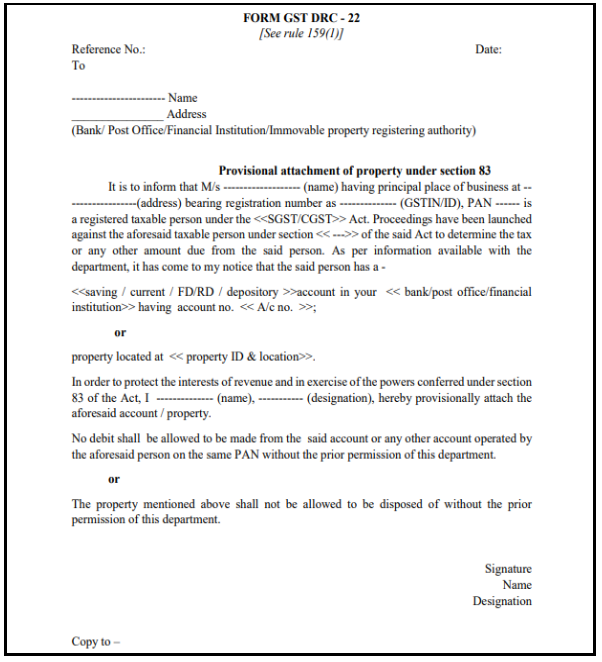

When Commissioner attaches the property of the taxpayer provisionally, including the bank account under Section 83 of Central Goods and Services Tax Act, 2017, he shall mention all the details of the property and pass a decision in FORM GST DRC- 22:

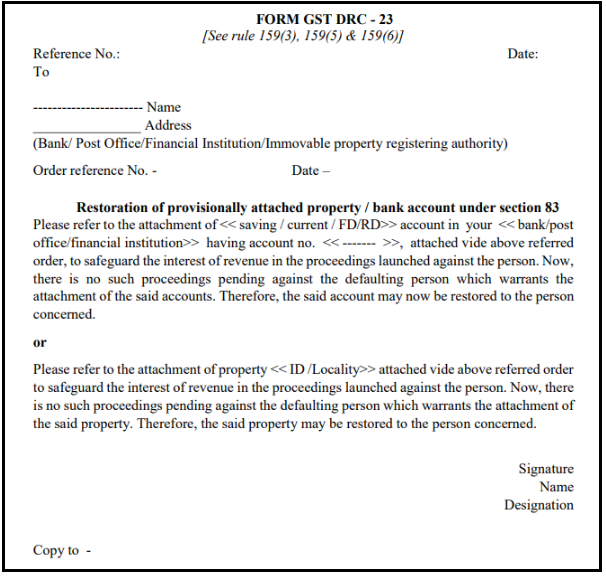

When the person liable to pay the tax pays the amount of equal to the market value of the attached property or the amount which he is required to pay and the nature of property which is attached is of hazardous or perishable nature, then the order will be passed to release the property when the proof of the payment will be shown. Order will be in FORM GST DRC- 23.

If the property attached is of hazardous or perishable nature and the person fails to pay the tax, penalty, and interest then, the commissioner will order to dispose of the property and the amount so recovered will be adjusted in the tax, penalty, and interest.

If a person is dissatisfied by the order of attachment may file his objection that the property is not subjected to attach. Commissioner after providing him with an opportunity of being heard may release such property. The order of such release may be in FORM GST DRC- 23.

If the commissioner is satisfied that the property must be released from the attachment than he will order this in FORM GST DRC- 23.

Section 84:- Enhancement and Reduction of Tax in Appeal, Revision, etc.

Section 84 of Central Goods and Services Tax Act, 2017, deals with the cases where the dues upon the Government has been

When a demand notice is served to the person who is liable to pay the tax, interest, penalty or Government dues under the Central Goods and Services Tax Act, 2017, and the order is filed in revision or appeal, etc, then in such case:

- When, in revision, appeal, etc. dues by Government has been increased, the Commissioner shall serve another notice of demand to the person who is required to pay the tax. Such notice of demand shall state the increased Government dues or recovery proceedings will resume from the stage where it was halted before the disposal of revision, appeal, and other proceedings. And no new notice of demand shall be issued in relation to the enhanced amount.

- If in any revision, appeal or other proceedings, dues upon Government is reduced, then-

- Commissioner will not serve any new notice of demand to the taxpayer.

- Commissioner is duty-bound to inform the taxpayer and other authorities that the amount is reduced in the proceeding.

- If any recovery proceedings have been initiated due to the notice of demand which has been served to the taxpayer before the proceedings in revision, appeal or any others have been disposed of, then such recovery proceedings may be carried on against the amount which is so reduced.

Conclusion

Demand and Recovery under Goods and Services Tax (GST) talks in whole about the recuperation of tax amount by the Government when any person defaults in paying the Goods and Services Tax (GST) for the supply of goods and services either intentionally or without intention. The government gives time to every defaulter to pay in case of short paid or not paid. If a person fails to pay the tax within the time limit as prescribed by the Act, proceedings will be initiated against that defaulter.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

Can recovery proceedings be initiated for late filling of GSTR-10 with a late fine of Rs. 10,000/- who is a NIL Return filler for the F.Y. 2017-18. Doesn’t it unfair to levy such huge amount just for the delay and that too for a case where no transactions were carried out in the books of accounts for the whole year.

After reading this article, now I understand how the Government recovers the tax and how the proceeding is initiated in case of no/short payment of tax. Thanks for sharing this valuable post about GST.