In this article, Swati Garg, an Advocate and an LL.M. graduate from Gujarat National Law University discusses the commercial reasons for creating a holding and subsidiary company structure, permitted transactions between holding and subsidiary companies and layering of subsidaries.

Understanding what a subsidiary and holding company is

Essentially, if one company holds more than 50% of the shares of another or appoints a majority of the other company’s directors, the second company is a subsidiary of the first. The first company is called the holding company.

If the holding company owns 100% of the shares of the subsidiary, the subsidiary is known as a wholly owned subsidiary (WOS).

A private company requires a minimum of two shareholders, so 100% shareholding is technically impossible. The company may give one share to another shareholder (who is friendly or aligned to the holding company). Typically, it is a relative of the promoters who run the company.

5 Commercial reasons for creation of a holding subsidiary structure

- To segregate the business structure and to create the distinct entities with separate management. For example, FMCG products can be housed under one vertical and consumer durables and electronics can be in another. This enables the value of different businesses to be captured separately. It facilitates buying and selling of an individual business. An investor can directly acquire shares of the company it is interested in. If an investor wants exposure (i.e. stake or benefit) in both segments then it can invest at the parent company level.

- Holding-subsidiary structure can also be used by companies to create different brands and brand categories for different kinds of products. For example, Vivanta is the budget brand of the Taj Group of Hotels. Companies may prefer to house different brands under different verticals. It enables them to bundle a brand and its intellectual property together in the event of a sale. This planning is typically done beforehand or when the company’s operations expand and they need to be ‘organized’ or ‘restructured’ in a new way.

- Companies use subsidiary structures to when they do business internationally, where they incorporate a separate subsidiary company in each country. This enables a company to enter and exit from business with respect to a particular country.

- Sometimes, this form of structuring enables companies to take advantage of lower tax rates in other jurisdictions. For example, many international venture capital funds have structured investments into India through a Mauritius entity to take advantage tax exemptions under India and Mauritius Double Taxation Avoidance Agreements (DTAAs).

- The structure can be expanded and extrapolated further by adding more layers of subsidiaries. For example, a global company may have a South Asia Holding company which has a parent India subsidiary, and further subsidiaries for different industry segments that the company sells products/ services in.

Subsidiary and holding company under Companies Act

Holding company and subsidiary company is defined under the Companies Act, 2013 (herein referred as Act).

Holding Company

Section 2(46) of the Companies Act, 2013 defines Holding Company. The company is said to be the holding company if that particular company holds/owns at least 50% of the other companies and has the authority to make management decisions, influences and controls the company’s board of directors. A holding company may exist for the sole purpose of controlling and managing subsidiary companies.

Subsidiary Company

Section 2(87) of the Companies Act, 2013 defines the Subsidiary Company. The subsidiary company is the company that is controlled by the holding or parent company. It is defined as a company/body corporate where the holding company controls the composition of the Board of Directors. As per the Companies Amendment Act, 2017, Section 2(87)(ii), if the holding company have control over more than one-half of the voting power of another company, that particular company will be identified as the subsidiary company.

Note: If a holding company owns 100% of the stock of other company, then the other company would be known as whole owned subsidiary of the holding company.

Layers of subsidiaries

The word layer as used in the section 2(87) of the act implies subsidiary or subsidiaries of a holding company. The context in which it is used in the section, it implies it means vertical subsidiaries. Section 186 and proviso to Section 2(87) of the Companies Act restricts the number of layers that holding companies can have. It must be read in conjunction with the Companies (Restriction on Number of Layers) Rules, 2017.

Note that wholly owned subsidiaries have now been excluded from being treated as a separate layer as per the rules above.

The restriction on layered structuring also does not apply when a specific law requires a layer to be created. We have discussed this later.

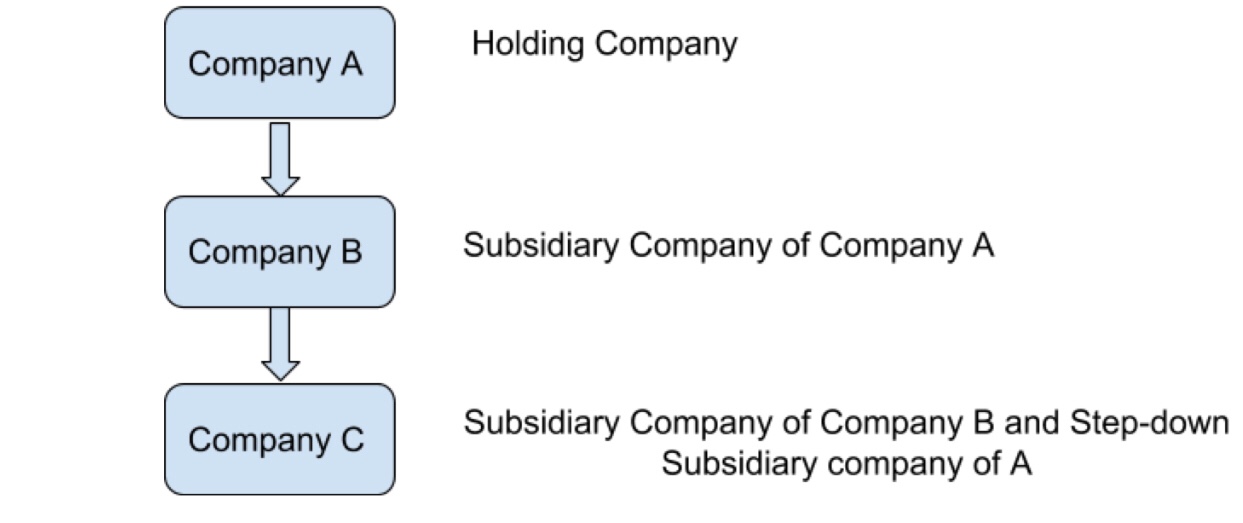

Step-down subsidiary company

This phrase is not defined anywhere in the Companies Act, 2013. In common parlance, it is used to specify a subsidiary of the subsidiary company.

5 Unique features of transactions between holding and subsidiary companies

- All transactions qualify as related party transactions and need to comply with the relevant restrictions on related party transactions. These restrictions are of multiple kinds, depending on the type of transaction. They could range from disclosure of interest, abstention from voting or taking approval of a specific majority of shareholders before entering into the transaction. These principles seek to ensure that the transaction does not get influenced merely by the relationship between the parties and is executed on an arm’s length basis.

- There are certain stamp duty relaxations available on transactions between holding and subsidiary companies, especially if they are wholly owned. Since the holding and subsidiary are different legal entities, their relationship and transactions between them will require various kinds of contracts to be executed, and payment of stamp duty on each contract can be onerous. Hence, stamp duty relaxations are beneficial. These exemptions have been done with a view to facilitate such structuring and organization of a company’s business. These exemptions are made available through separate notifications hence they are not ordinarily visible in the text of the state-level Stamp Act or schedule.

- From an income tax perspective, arm’s length pricing principles may have to apply especially, if the holding-subsidiary relationship is international. In certain cases, arm’s length pricing applies in domestic situations also under Indian law.

- Transferring dividend from a level 2 or level 3 subsidiary (where permitted) to the holding company can be cumbersome and have unintended tax implications if the structuring is not done carefully.

- For loan transactions, one or more holding companies may issue guarantees for the obligations of the subsidiary.

Practical Tip: When you are working on a transaction between a holding and subsidiary company, at the time of checking the stamp duty under the relevant state-level Stamp Act or schedule for the transaction, make sure that you also check whether there is an exemption or relaxation for that transaction if it is undertaken between holding and subsidiary companies.

What are the permitted transactions between subsidiary and holding companies? Are there any transaction which are prohibited? What is the logic behind the prohibition?

Permitted Transactions

- Any loan made by a holding company to its wholly-owned subsidiary company is permitted if the said loan is used for wholly-owned subsidiaries’ principal business. The loan should not be used for any other investment by the subsidiary company.

- Holding company can provide guarantee/security for any loan made to its wholly-owned subsidiary company if the said loan is used for wholly-owned subsidiaries’ principal business. The loan should not be used for any other investment by the subsidiary company.

- Furthermore, holding company can provide guarantee/security for any loan made to its subsidiary company by any bank and financial institution if the said loan is used for wholly-owned subsidiaries’ principal business. The loan should not be used for any other investment by the subsidiary company.

Other than above, transactions between holding companies and subsidiary companies are classified as related-party transactions under section 2(76). For these transactions, consent of Board of directors should be given by a resolution at a Board meeting. Moreover, if these transactions are not entered by the holding or subsidiary company in its ordinary course of business, they have to make sure that they have followed arm’s length principle. Thereafter, holding company and subsidiary company can enter into a contract or an arrangement for the following things:

- Sale, purchase or supply of any goods or materials;

- Selling or otherwise disposing of, or buying, property of any kind;

- Leasing of property of any kind;

- Availing or rendering of any service;

- Appointment of any agent for purchase or sale of goods, materials, service or property;

- Appointment of related party to any office or place of profit in the company, or its subsidiary or associate company;

- underwriting the subscription of any securities or derivatives thereof, of the company.

To further govern these related party transactions, central government came up with The Companies (Meetings of Board and its Powers) Rules, 2014.

Prohibited Transactions

As can be seen above, permitted transactions have been specified in the act. One thing we need to remember is that if the proper procedure has not been followed to conduct permitted transactions, it will be in contravention of the act and will result into penalty for the company.

However other than that, the act also specifies various prohibited transactions between subsidiary and holding company. The rationale behind is that to ensure that the directors are not utilising the companies’ funds for their own benefit. Prohibited transactions are:

- A subsidiary cannot have an shares in its holding company. Thus, cross-holdings are not permitted between holding subsidiary companies. Holding company can not allot or transfer its shares to any of its subsidiary company. If you see the holding structure of the Tata group there are numerous cross-holdings between companies (i.e. Company A will have some shares in Company B and Company B will also have some shares in Company A). That is possible if the two companies are not holding and subsidiary companies (i.e. mutual shareholding in each other should be less than 50%).

- Any loan made by a holding company to the subsidiary company is not permitted under the act.

- Any loan/guarantee/security made by the subsidiary company to the director of the holding company is not permitted.

What kind of layering is permitted under the Companies Act and rules and what layering is not permitted? Is the situation different in the case of foreign holding company or foreign subsidiary company?

As explained above, layering under the act means subsidiary or subsidiaries of the holding companies. As given under the proviso of section 2(87), there is a prohibition on the holding company to not have more layers as prescribed under the act. Section 186(1) of the act specifies that a company should not invest in more than two layers of investment companies. Keeping in mind the proviso of section 2(87) of the act, on 20th September 2017, the Central Government enacted “the Companies (Restriction on Number of Layers) Rules, 2017. These rules specify that no companies shall have more than two layers of subsidiaries. This restriction is for vertical subsidiaries not for horizontal subsidiaries.

Before going into the details of layering, let’s first understand why there is a need for restricting layers of the company which is as follows:

- To reduce the illicit fund flows.

- To curb diversion of funds.

- To keep a check on the multiple layers of subsidiaries.

- To stop companies to reduce shell companies for diversion of funds.

- To prevent the company from money laundering, the illegal way of obtaining money.

- To enable the authorities to identify the beneficiaries of corporate structures.

Restrictions on Layering under the Companies (Restriction on Number of Layers) Rules, 2017

Now, let’s take a look at the provisions of these rules.

- A company shall not have more than two layers of subsidiaries.

- A wholly owned subsidiary company would not be taken in account as a separate layer.

- Following classes of companies are outside the scope of these rules:

-

- A banking company;

-

- A non-banking financial company;

-

- An insurance company;

-

- A government company.

-

- A company acquiring a company incorporated outside India having more than two layers of subsidiaries provided it is in accordance with law of that country.

-

- A subsidiary company who is required to have an investment subsidiary under any law or rules.

- These rules are prospective in nature. Therefore, any company who had more than two layers of subsidiaries on or before these rules came into force, they are required to

-

- file a return in Form CRL-1 to Registrar within 150 days of publication of these rules.

-

- shall not add more layers of subsidiaries.

-

- If the layers are reduced after these rules came into force, shall not increase their number of layers beyond two.

- A maximum fine of Rs. 10,000 will be imposed on the companies and every officer of the company which is in contravention of these rules. If the contravention is a continuing one, then a maximum fine of Rs. 1,000 every day will be imposed.

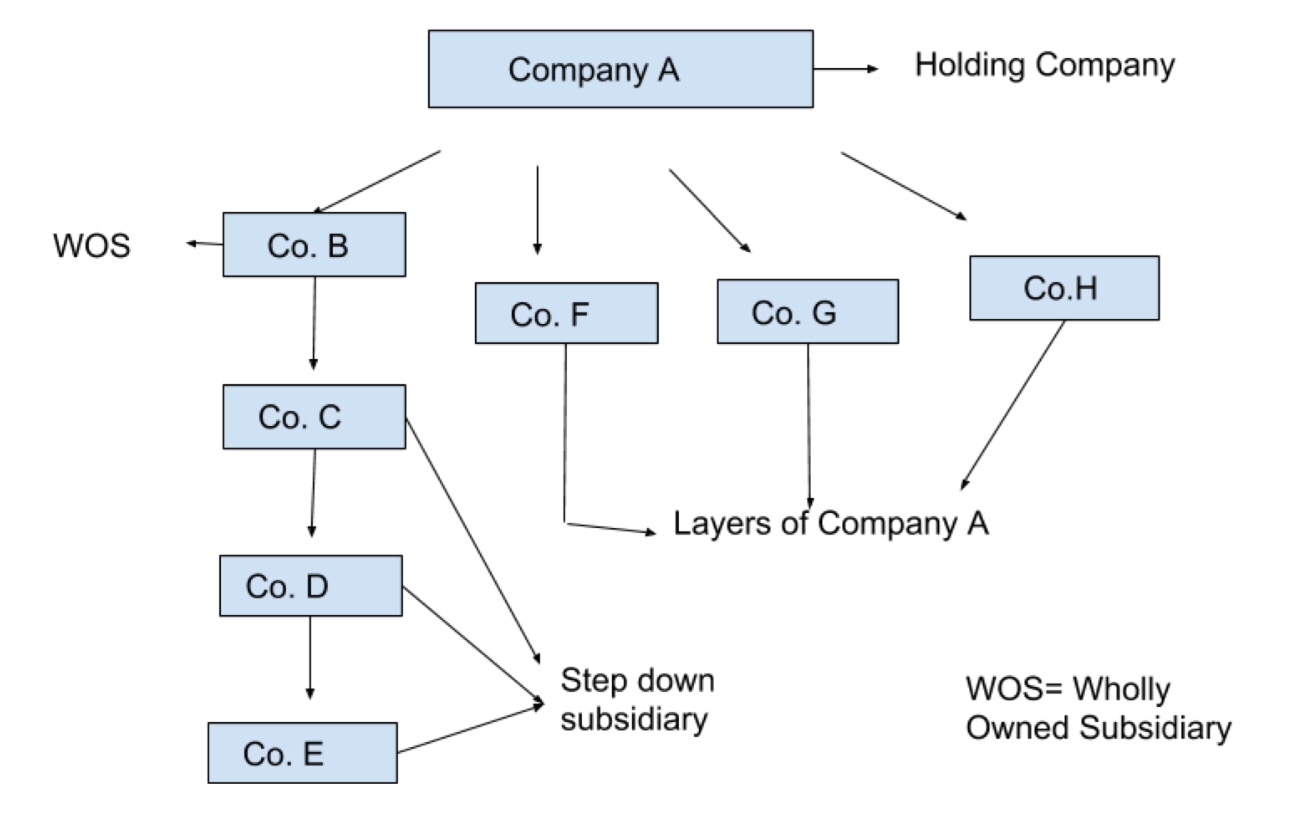

Illustration 1: Layering – Distinction between subsidiary and step-down subsidiary

Here Company A is the holding Company.

- Company B, F, G and H are the horizontal subsidiaries of the holding company where the restrictions are not applicable. They can have as many horizontal subsidiaries.

- Company F, G and H can have step down/layer subsidiaries just like company B.

- Company B, C, D and E as the vertical subsidiaries company of the holding company A. Here, we have to test the restrictions.

- As company B is wholly owned subsidiary of company A, it will not be considered separately as a layer. Therefore, it can be said that in the given illustration, holding company A has 3 step down subsidiaries or layer companies i.e. company C, D and E.

- As the rules specifies, any holding company can have only two layers, therefore company C and D are well within laws. However, company A can’t have company E as its subsidiary.

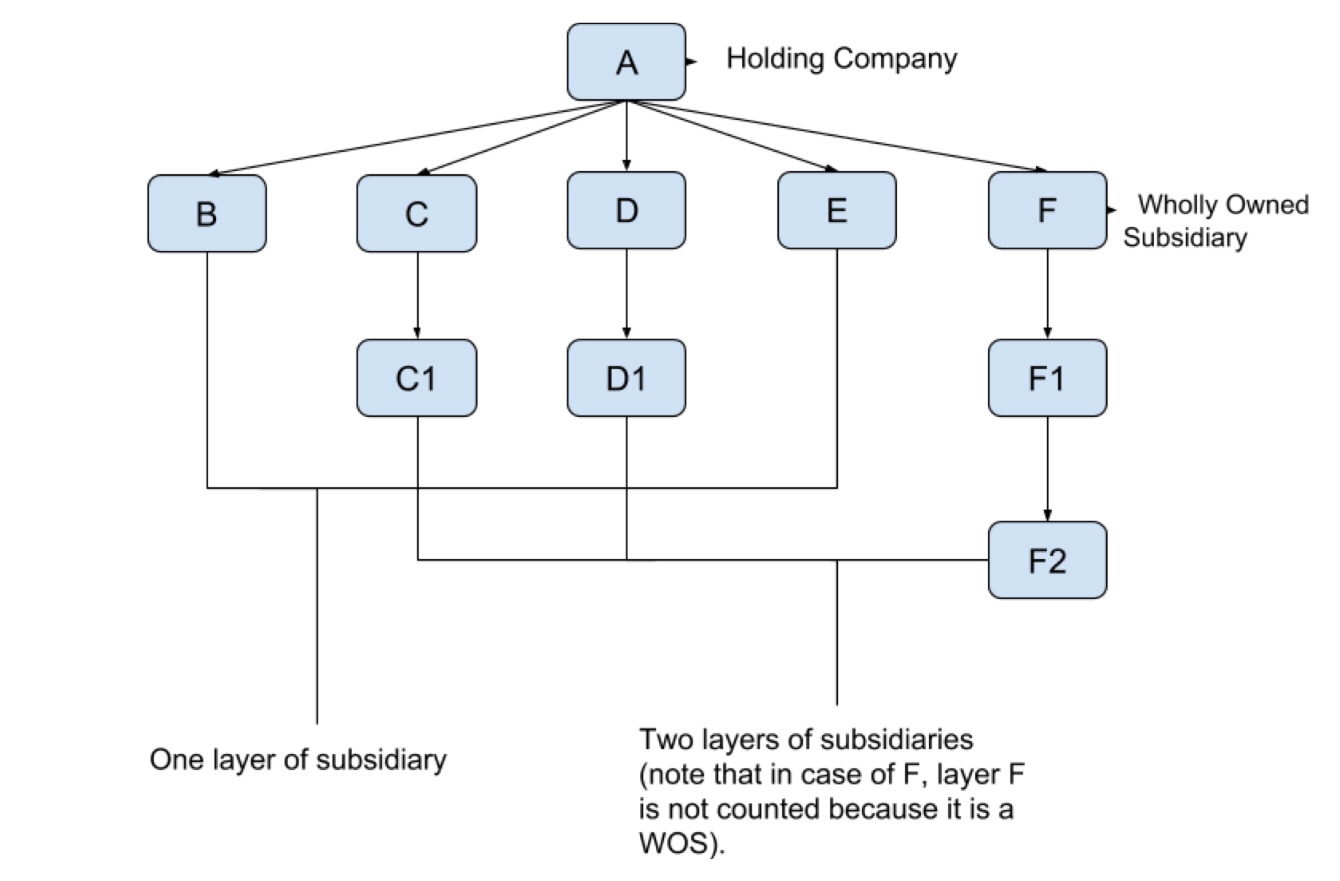

Illustration 2: Layering: Single and Two-Level Subsidiaries (with exceptions)

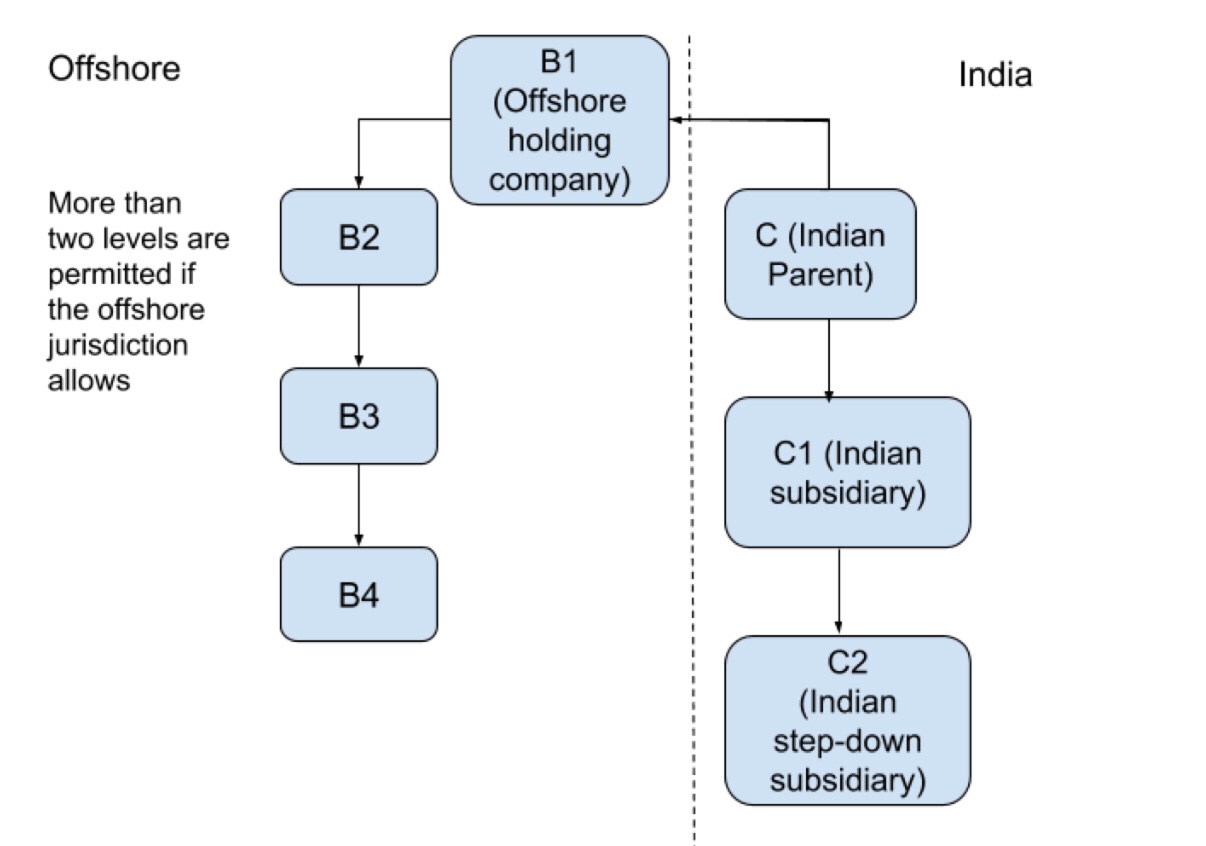

Illustration 3: Layering in International Context

Here in the illustration, in India, a parent company C can have two layers of subsidiary but if it has to acquire an offshore company and the offshore company has more than two layers of subsidiaries which is permitted as per the jurisdiction of the offshore company, it will be exempted under Indian law.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

hi great blog