This article is written by Nikita Sangal.

Table of Contents

Introduction

Whenever a platform of technology is used by the Government for governance, it not only exhibits its vision towards public administration but also reflects its perspective towards shifting its existing paradigms to the new ones. However, governance through an electronic medium is not just simple online information provision. It calls for analysing & filling the gaps in the current processes, improving & integrating various activities which are working in different directions and thereafter building a comprehensive architecture. Of late, an initiative of this kind was taken in India where through the mechanism of e-way bills through which transparency in relation to tax compliance, logistics, accountancy and governance is sought. E-way bill is one of the electronic documents generated on the Goods and Services Tax Portal, evidencing movement of goods. Five states namely Karnataka, Madhya Pradesh, Kerala, Rajasthan, Nagaland and Uttarakhand voluntarily implemented e-way bills in the month of December 2017. A 15 days nation-wide trial of e-way bill was conducted from 16th January 2018 till 31st January 2018 and after that trial, e-ways bills were made compulsory nation-wide the instance of inter-state movement of goods from 1st of February 2018 onwards. Thus, in case of movement of goods where the value of the consignment is more than Rs. 50000, every person who takes charge of movement of goods is required to generate e-way bills. For instance, Mr. A is in Uttar Pradesh and wants to transport goods value of more than Rs. 50000 to Mr. B in Delhi, since here movement of goods is involved where value of goods is more than Rs.50,000, Mr. A(in this case) is required to generate an e-way Bill. However, in certain cases even Mr. B or the transporter may have to generate E-way bills.

The literature in relation to e-way bills specifically is very limited. E-way bill is a broader concept which includes e-governance, e-taxation and streamlining of transportation and logistics. Thus, review of literature in relation to e-governance and e-invoices have been made. Mechanism of E-way bills has been implemented in a narrow sense in countries across the world. In European Countries e-taxation was implemented in the early twenty first century and in the same era e–invoice system was adopted by countries like Denmark and Taiwan. It was clearly stated by (Sheng-Chi Chen, 2015) that the adoption of an e-invoice system can enhance business transactions and reduce operating costs. The research conducted by Cheng-Chieh Wu, Sheng-Chi Chen, and Scott, entitled Constructing an Integrated e-Invoice System: The Taiwan Experience argued that a united effort is still wanted to promote the adoption of the e-invoice system, and in depth analysis is still needed to determine how the new e-invoice platform will empower the government to become smarter. E-invoicing has the potential to substantially reduce transaction costs in the corporate and public sector. In the year 2005, Denmark’s e-invoice system already accounted for roughly 90 per cent of all invoices in the public sector. (Brun, 2007). (Al-Hashmi, 2014) in his paper ‘Understanding Phases of e-Government Project’ stated that a ‘smart government’ attributes to an administration which appropriates ICT to handle planning, management, and operations within a single tier (city, state or federal) or across tiers (across state and local governments) to cause sustainable public value. In a similar way, the mechanism of e –way bills ICT in planning and administration to refine the levels of governance. (Janja Nograšek, 2014) in its paper ‘E-government and organisational transformation of government: Black box revisited?’ explains that the impact of ICT on the development of processes and administrative structures i.e. organisational transformation are still relatively poorly appreciated and there exist sometimes conflicting views about ICT’s role. (John Carlo Bertot, 2012) in its research paper ‘Promoting accountability and transparency through ICTs, social media, and collective e‐government’ identified potential impacts key initiatives and future challenges for collaborative e‐government as a measure of transparency. (Pashev, 2007) in its research paper ‘Countering cross- border VAT fraud: the Bulgarian experience’ explained, that in the case of fake exports, the exporter carries the transaction on paper, applying the zero VAT rate on exports as well as claiming the tax credit on the inputs, actually while selling the products on the domestic market without the sales invoices, i.e. it amounts to without paying VAT. Confronted with the drastic increase of carousel fraud, the European Commission analysed the critical need of a consistent strategy to combat it. Earlier, neither the literature nor the practices of tax and law enforcement have labelled the threat appropriately. Tax evasion literature is focused on the deterrents of individual evasion, while studies of VAT network crime rarely consider the preventive instruments’ extra compliance costs for taxpayers. Here again in the situations of tax-fraud, mechanisms like e-way bills may come to the rescue to avoid such tax evasions. (Vivek Soni, 2017) , an IITian in his paper named ‘Digitizing grey portions of e-governance’ explained that implementation of ICT applications to support e-governance varies from one sector to another. This type of governance involves different high degrees of complexity in driving the operations for development of respective sectors. Therefore, policymakers and the government need more flexibility to conquer present barriers of sector development.

Purpose

The purpose of this paper is to understand the mechanism of e-way bills which have been recently introduced in India, analyse the gaps/ weaknesses in the policy formulation, analyse the possible impediments/apprehensions that may arise during implementation of e-way bills mechanism and to provide possible solutions for various practical challenges and issues that businesses may air in the implementation of e-way bills mechanism under Goods and Services Tax Act 2017.

Understanding the mechanism of e-way bill

A Way- Bill is a document issued by the carrier of the goods depicting the name of consignor, consignee, origin, destination and instructions related to shipment of consignment of the goods. E-Way Bill is a compliance mechanism in which if the value of goods exceeds Rs. 50,000, a document has to be generated electronically before the commencement of movement of goods from one place to another, if the movement is beyond 10 kilometres. This movement of the goods can be either interstate or intrastate. E-way bills can be generated after following few steps:

- Registration must be made by logging on the E-Way Bill portal.

- The Invoice or Bill or Delivery Challan related to the consignment of goods should have been generated.

- By logging on to the GSTN Portal, FORM GST EWB -01 can be demanded.

- Fill the details given in PART-A consisting of FORM GST EWB -01.

- If the transportation of the goods is undertaken by road, then the Transporter ID or the Vehicle number has to be mentioned under Part –B of the FORM GST EWB-01.

- If the transportation of the goods are undertaken by air, rail or ship then the Transport document number, Transporter ID and date on the document needs to be mentioned under Part –B of the FORM GST EWB-01.

Once the e-way bill is generated by following steps mentioned above, a copy of the e-way bill number or e-way bill has to be kept by the transporter either physically or mapped to a RFID (Radio Frequency Identification Device). RFID will be fixed on the vehicle to track the location of the vehicle and goods, the details mentioned in e-way bill can be tracked with the help of RFID embedded on the vehicle.

An e-way bill once produced it will be valid for a specific time period. The validity of an e-way bill is determined on the foundation of the distance to be travelled by the goods. For a distance of less than and equal to 100 km, the e-way bill will be valid for a day from the date of generation of e-way bill. For every 100 km thereafter, the validity will be additional one day from the date of generation of e-way bill.

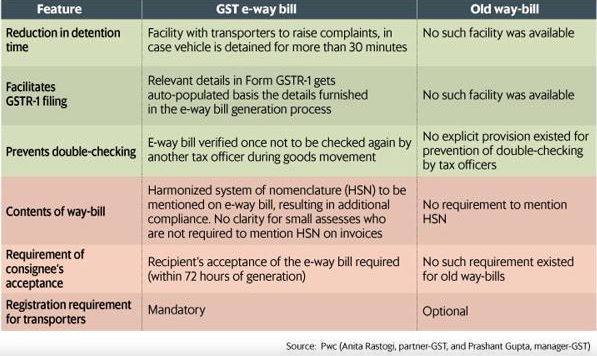

The E-way bill is one of the major reforms in Goods and Services Tax (GST) regime and would bring about a revolutionary change in the way movement of goods will be governed in the country. The E-way bill has replaced the way bills were physically made in the pre-GST regime. The contrast between the two mechanisms has been made in Figure 1 below:

Figure 1: Contrast between E-way Bill and Way Bill

Source: PWC (Anita Rastogi, partner GST, and Prashant Gupta, manager-GST)

In e-way mechanism under the GST regime, if in case the goods of the person or vehicle or transporter, is detained for more than 30 minutes by the tax officers without any proper reason, then the transporter can generate ‘Report of Detention’ in Form GST EWB-04 giving details of office in-charge. This provision will rule out the possibility of transporter’s harassment in the hands of field officers. In the pre-GST regime, absence of such provision paved the way for manipulations by the field officials. It was also analysed that the transporter had to go for verification of the same Way bill several times in pre-GST scenario whereas under e-way bill mechanism, if the e-way bill has been once verified by an official, it will not be checked again by the officials during its entire journey. Such provisions will help streamlining the system of transportation of goods across nations.

The Harmonised System of Nomenclature was introduced by the World Customs Organisation to bring uniformity in the coding of the traded goods across the world. Harmonised System of Nomenclature (HSN) is an internationally standardized system of assigning the names and numbers to classify traded products. HSN is adopted under e-way bills mechanism, which will help to keep a check on types of goods transported.

Moreover, when an e-way bill will be generated either by consignor or the transporter, such e–way bill has to be accepted by the consignee by logging-in to Goods and Services Tax Network Portal within 72 hours from generation of such e-way bill, else, the said e-way bill will deemed to be accepted by the consignee.

Another feature of the mechanism of e-way bill is that the details furnished while generating an e–way bill will be auto populated while filing returns under GST. These all provisions will help in tax compliance, automated validation, vendor self-service, enhanced account reconciliation and enhanced governance.

Gaps/weaknesses in the policy formulation and their possible solutions

The E-way bill mechanism has its in-built advantages. However, the benefits of such mechanisms will percolate down only when the gaps in the policy formulation are bridged. Following are the gaps /weaknesses of the system which are explored through thorough analysis of the provisions of Central Goods and Services Tax (CGST) Act 2017:

- It is mandatory to generate an e-way bill when the value of the goods exceeds Rs. 50,000. The threshold limit of Rs. 50,000 is quite low in which the majority of small businesses operate. These vendors are generally small traders and manufacturers who now have to comply with an additional plethora of formalities. These vendors usually cannot afford the technical help of an expert for filing e-way bills. Thus, the threshold limit of Rs. 50,000 should be increased to keep small dealers out of the ambit of generation of e-way bills.

- As a corollary of the point discussed above, if the value of the single consignment of the goods by a vendor doesn’t exceeds the threshold limit of Rs. 50,000 but if the total value of the all the consignments of goods intended to be transported by the transporter exceeds Rs. 50,000, in that case the transporter has to generate a consolidated e-way bill, mentioning all details pertaining to each consignment. This provision expects a lot from transporters, who in majority are uneducated. A possible solution to such a case could be, that the liability to generate an e-way bill should be made on the last consignor who should also be made liable to update the information pertaining to the rest of the consignments.

- Practical difficulties which a person causing movement of goods may face is the case where the e-way bill has to be generated even when the goods are to be moved from factory to a weighbridge situated outside the factory. A possible solution to such a case could be that an e-way bill will be generated in void of an invoice, as invoice cannot be issued until and unless goods are weighed. Once the goods are weighed and goods are received back in the factory, then invoice can be generated and another e-way bill needs to be generated for movement of goods for sale to the customer. Even such a solution is too tedious to perform. Thus, a relaxation in generation of e-way bills in case of weighing the goods should be given.

- In the scenarios where multiple vehicles have to be used for ease of transportation, the details in Part-B of FORM GST EWB-01 can be entered only by the transporter assigned in the EWB or generator himself. The assigned transporter cannot further re-assign the authority to update the details in Part-B to the subsequent transporter. Whereas, in reality the assigned transporter becomes out of picture when goods are loaded to another vehicle under another transporter. In the light of above circumstances, the provision of re-assigning the transporter by previous transporter must be incorporated in EWB forms.

- The validity of e-way bills is dependent upon the distance to be travelled by the goods. For a distance of less than and equal to 100 Kms, the e-way bill will be valid for a day from the date of generation of e-way bill. For every 100 Kms thereafter, the validity will be additional one day from the date of generation of e-way bill. Now, in case of break-down of the vehicle, how the validity of e-way bills can be extended is not defined. Thus, clarity should be made in this regard under the CGST Rules 2017 related to e-way bills.

- In case of ‘Bill to’ ‘Ship to’ transactions, two transactions take place resulting in one transaction. If a certain invoice is raised in the name of one person (here ‘Bill to’), whereas the goods are to be delivered to another person (here ‘Ship to’) and if the legal addresses of both the parties are different. In this case, two e-ways bills have to be generated by the transporter to show the short-cut movement of goods, whereas the goods are moving directly from the person generating invoice to the person whom goods are to be shipped.

This system would have a lot of practical challenges and implementation issues. A lot of real-time coordination is sought prior to the movement of goods.

- There is no recourse available in CGST Rules 2017 pertaining to e-way bills regarding the situation, where if the other party wrongly rejects the E-Way Bill after the goods have commenced movement. The solution to this problem could be to stop the transportation of the goods then and there, as the e-way bill is wrongly cancelled. And to generate a new e-way bill in relation to the goods in transportation. However, guidelines in relation to this problem are expected from the Central Board of Excise and Customs. Delay in the same will cause serious hardships to all the parties involved in the transaction and transportation.

- Ideally, Part-A of an e –way bill has to be filled before movement of goods from the place of origin. Part –A asks for details related to the transporter document number. But in cases where the goods are transported through railways or air or ship i.e. where mode of transportation is otherwise than by road, transportation document number is generated only when the goods are submitted to the concerned authority. The e-way bill generator will definitely face problems in resolving this issue. The solution to this problem is not provided in the law. People generating e-way bills must find the probable suitable answers in the frequently asked questions issued by the Central Board of Excise and Customs for this.

- Some goods are still kept out of the preview of Goods and Services Tax Act 2017. These goods are namely petrol, diesel, alcohol for human consumption, turbine fuel etc. No clarity is given in the rules that whether an e-way bill has to be generated in the transportation of the said goods which are out of the purview of GST.

Rule 138(14) of CGST Rules, 2017 provides the list of the goods for which no e-way bill is required to be generated. In the said list the goods mentioned above are not mentioned. Thereby bringing a state of confusion as the two provisions of the GST Act 2017 are in contradiction. An immediate action is requested from the Central Board of Excise and Customs in this regard.

- When a job worker completes his job work and returns the goods back to the Principal, in that case he is required to generate an e-Way Bill on the basis of delivery challan. The basic concept of GST gets violated here as in e-way bills when the job worker will fill Part-A of the e-way bill, he will show the value of goods returned. Whereas, there must be a provision in e-way bill to show the value of the job work services in e-way bill on which GST is chargeable by the Job worker. Another probable solution to this problem could be that the value of goods could be shown inclusive of job work charges.

Possible impediments/apprehensions that may arise during implementation of E-way bills mechanism

- The mechanism may face the bottlenecks during its practical implementation. Industry and trade, along with a section of analysts have the opinion that this mechanism is a ‘cumbersome’ process that could lead to supply chain bottlenecks. In the opinion of the trade analysts, small businesses such as small transporters may find the entire process difficult to comply with because e-way bills add another layer of compliances for GST payers.

- The biggest hurdle in implementing e-way bills is the lack of reliability of the Information Technology Infrastructure. E-Way Bill portal has been developed by National Informatics Centre (NIC) which is one of the country’s premier informatics services organisations, but the kind of magnitude of transactions that take place in an hour, in a day, in India is huge. The experts believe that the portal will not be able to handle the traffic once e-way bills will be made compulsory in case of both intra-state and inter-state movement of goods.

- Small transporters are wary that the e-way bill system would encourage harassment of the small transporters and will help big transporters create a monopoly at the cost of small ones. As small transporters cannot afford the technical expert help to generate e-way bills, they will end up losing big clients. The big transporters on other hand will be able to entertain all the consignments which are of the value above Rs. 50,000.

- Trade and industry have raised concerns about the system being a possible route of giving discretionary power to tax officials leading to undue harassment of the traders, as the tax officials can keep a track of the location of the vehicle/ goods in the movement. Inspectors have the right to unload the entire consignment to check compliance. Since, there are no guidelines provided for genuine randomness as against “targeted” checks, the transporters may become victims in the hands of the officials.

- The transporters are of the view that Inspector Raj will return as the RTO and sales tax check posts are still there.

- Transporters who do transportation of heavy cargos argue that heavy cargos take a long time to transport because it takes a lot of time to lift these heavy cargos, such cargos even have other related logistics issues and there is requirement of multiple permissions while in transit of heavy cargos. In such scenarios if, for some reason, the validity of e-way bills expires, it would invite penalties for these transporters.

- Low literacy levels and poor technology awareness among a majority of truck owners could also create a stumbling block in the implementation of e-way bill mechanism.

- If the transporter is a small transporter who hasn’t crossed the threshold limit of turnover prescribed for having registration under Goods and Services Tax Act, 2017, is also supposed to have registration under e-way bill mechanism if he wants to generate an e-way bill. This may call for adding woes to a small transporter who may not be technology equipped.

- Installation of a radio frequency identification device (RFID) in a transporter’s vehicle to map the soft copy of an e-way bill will be an additional cost burden to be faced by the transporter.

- Trade analysts and experts are of the view that since under the VAT regime the rates of VAT were different for different states and hence the vendors used to charge lower VAT instead of higher VAT for the same goods. But since, in the GST regime, there is uniformity in the rates of taxes levied across nations, there is no need to implement an out-dated mechanism of e-way bills.

- Basic Infrastructure to implement the mechanism of e-way bills includes electricity and internet connectivity. The internet connectivity across nations is not the same as in the case of remote areas and hilly areas. Thus, a major impediment in implementation of e-way bills is the lack of availability of electricity and internet at the time of movement of goods. Without this basic infrastructure, goods cannot be moved unless an e-way bill is not generated.

These possible impediments and apprehensions raised by the trade experts and IT experts should be taken into consideration for the smooth implementation of the e-way bills mechanism.

Conclusion

The adoption of an e-way bill mechanism has the potential of changing the ways of governance, tax compliance and streamlining the logistics and transportation operations, in the long run. The movement of the goods will be unobstructed as there will be no physical checks- points at the entry of each state. At present, as the mechanism is new to the nation, it will definitely face some teething issues. However, the government will start reaping the benefits of the e-way bill from the moment the e-way bills are made mandatory in the case of both inter-state supply of goods as well as intra-state supply of goods. For reaping the benefits and to percolate those benefits to the public at large, the gaps in the provisions framed under the Act, have to be filled and bridged. The resentment and the apprehensions raised by the trade representatives have to be dealt with extensive care. The basic IT infrastructure has to be made in place and tested beforehand for handling larger magnitudes of online traffic. Above all, cooperation from all the players in the mechanism of e-way bills is required to have collaborative governance.

References

- Al-Hashmi, A. (2014). Understanding Phases of E-government Project. Emerging Technologies in e-governance.

- Anita Rastogi, partner GST, and Prashant Gupta, manager-GST. (n.d.). Way Bill and E-way bill.

- Brun, M. H. (2007, February). Electronic invoicing to the public sector in Denmark (EID). Retrieved from https://joinup.ec.europa.eu.

- Janja Nograšek, M. V. (2014). E-government and organisational transformation of government: Black box revisited? Government Information Quarterly, 31(1), 108-118.

- John Carlo Bertot, P. T. (2012). Promoting transparency and accountability through ICTs, social media, and collaborative e‐government. Transforming Government: People, Process and Policy, 6(1), 78-91.

- Pashev, K. V. (2007). Countering cross‐border VAT fraud: the Bulgarian experience. Journal of Financial Crime, 14(4), 490-501.

- Sheng-Chi Chen, C.-C. W. (2015). Constructing an integrated e-invoice system: The Taiwan experience. Transforming Government: People, Process and Policy, 9(3), 370-383.

- Vivek Soni, P. K. (2017). Digitizing grey portions of e-governance. Transforming Government: People, Process and Policy, 11(3), 419-455.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications