This article has been written by Riya Dubey, pursuing a Diploma in M&A, Institutional Finance, and Investment Laws (PE and VC transactions) from LawSikho.

Table of Contents

Introduction

In the context of M&A transactions, how to choose an optimal structure plays an important role. The structure you choose for an M&A transaction could either make or break the deal. The choice made by the buyer and the seller for choosing the mode of an acquisition depends on the taxation, successor liability, employee transfer, stamp duty, time, and effort for implementation besides the commercial considerations involved. Thus choosing the structure that works best for the buyer and the seller is the first step in making the M&A deal transaction.

In general, companies choose corporate restructuring due to an increase in losses, general market or economic forces and trends, change in corporate strategy, change in ownership. It is done for maximizing the company’s strength by reducing costs, increasing profits, and removing inefficiency.

The reasons may differ but successful restructuring is a complex process and needs exhaustive efforts. The corporate restructuring for the company is based on the reason for restructuring and the unique circumstances and characteristics of the company.

Five common ways to transfer a business undertaking

Asset sale

An asset sale is the itemized sale of the asset of an entity in a bit-by-bit manner. In this individual values are assigned to each asset. This is generally used to clean up the balance sheet which is saddled with bad loans. In an asset, the sale acquirer gets an opportunity to cherry-pick the assets and liabilities he wants to undertake.

Asset sale transaction

The asset sale transaction takes place between the shareholder and the company. Further, the company is involved in selling those assets to the buyers, in return for which it receives cash.

Advantages of Asset sale

- Buyers can cherry-pick the assets and liabilities.

- There are lesser chances that the buyer will pick unforeseen liabilities that may be lurking in the target company.

- Sometimes, not always, the buyer can receive better tax treatment in comparison with stock purchases.

Disadvantages of Asset sale

- An asset sale may lead to high-impact tax costs for both the buyer and the seller.

- An asset sale also takes more time to close the deal as compared to other structures.

How can the taxability of capital gains be determined?

For determining the taxability of capital gains, a difference should be made between depreciable and non-depreciable assets.

|

Non-depreciable Assets |

Depreciable Assets |

|

For example vehicles, buildings, plants, furniture, equipment, etc.

|

Share sale

Shares represent the complete underlying value of the assets and liabilities of the company. Share acquisition is the common manner of acquiring a company. In a share sale, the acquirer looks to secure the entity which houses the business as well as the setup. When the target has made a name for itself in the market and has established a loyal customer base, acquirers will be looking to acquire the company as well as the business

The tax implications of share acquisitions are:

- Liability to tax on capital gain, if there is any,

- Liability under Section 56(2)(x) of the Income Tax Act, if any.

The existing shareholders may get a profit or suffer a loss on a share transfer. This depends on whether such shares are held as capital assets or as stock-in-trade.

In case shares are held as capital assets, profits and gains arising from the transfer of the shares will get charged to tax under Section 45 of the Income Tax Act as ‘capital asset’. And in case of shares are held as stock in trade, profits and gains from transfer of share will be charged to tax as ‘profits and gains from business and profession’.

Advantages of the Share sale

- Taxes on the share sale are less, especially for the seller.

- The share sale deal is less time-consuming since negotiations are less complicated.

Disadvantages of the Share sale

- In a share sale, legal or financial liabilities may accompany a share sale.

- In a share sale, an uncooperative minority shareholder can create the problem.

Slump sale

In slump sale business undertaking is transferred as a whole, on a “going concern” basis. It is defined under Section 2(42c) of the Income Tax Act, 1961, which says “ slump sale to be the transfer of one or more undertakings, in lump sum consideration without assigning any specific value to any assets and liabilities.”

Explanation 2 of the section says that the value of assets and liabilities is determined for the sole purpose of stamp duty, registration fees, or any other taxes or any kind of fees. It shall not be considered as the value assigned to individual assets and liabilities. Thus, for better understanding, slump sale has been explained point-wise;

- Sale of Undertaking;

- Consideration to be in a lump sum amount;

- Capital gains to be computed for undertaking as per the formula;

- No GST.

When slump sale is an effective strategy to undertake a business?

- When the purchaser wants to expand its already existing business or when the purchaser wants to diversify its existing business;

- When a company segregates one too is divisions to get some private equity into that division and not the other divisions owned by the group;

- When the seller wants to separate its core operation from non-core operations;

- When the transfer is not possible through merger or demerger then slump sale can be considered to transfer the business undertaking.

Why is slump sale effective?

It is effective by the Business Transfer Agreement. In this, the list of assets, liabilities, contracts, employees, etc. which would be transferred from the seller to the buyer is prepared. It also includes the clause like condition precedent, representations, and warranties from the seller and buyer and lump sum consideration at which such undertaking would be transferred. Business Transfer Agreements can be negotiated and can be executed within 1-2 months of conceiving the slump sale. Section 230-232 of the Companies Act, 2013 also deals with how the slump sale can be done.

Amalgamation

In an amalgamation, there is a combination of two or more entities forming a new entity. In this neither of the entities involved survives as a legal entity, there is the formation of an entirely new entity. The assets and liabilities of the entities involved are also combined into the new entity formed. Section 2(1B) of Income Tax Act, 1961 defines amalgamation as the merger of one or more companies with another company or merger of two or more companies to form a new company in a way that-

- All property of the amalgamated company becomes the property of the amalgamated company.

- All liabilities of amalgamated companies become the liabilities of the amalgamated company.

- Shareholders holding not less than 3/4th of shares in the amalgamating company become the shareholders in the amalgamated company.

In amalgamation, two or more companies combine to form a new entity. X and Y both will wound up and Z will be the new entity.

What are the purposes of amalgamation?

It is done for:

- Gaining synergy;

- Avoiding completion in the market;

- Increasing efficiency of the business;

- Expanding business;

- Building up of goodwill;

- Reducing the degree of risk by the way of diversification;

- Saving of taxes;

- Increasing shareholder’s value.

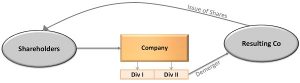

Demerger

The demerger is splitting up a company into a new entity. It occurs either to function independently or to be liquidated. The demerging company doesn’t need to be a subsidiary of the parent company. It is done for splitting up for specialization and to expand the entities. The splitting up of an entity can also be called “spin-off”, “spin-out” or a “starburst”. It generally means that the company gets divided into a separate entity. After the demerger, the spin-off company gets the assets, intellectual properties, technologies from the parent company. Demerger according to Section 2(19AA) of the Income Tax Act 1961 in relation to companies, means the transfer, pursuant to a scheme of the arrangement under Sections 392-394 of the Companies Act, 1956, by a demerged company of its one or more undertakings to any resulting company in such a manner that:

- all the property of the undertaking, being transferred by the demerged company, immediately before the demerger, becomes the property of the resulting company by virtue of the demerger;

- all the liabilities relatable to the undertaking, being transferred by the demerged company, immediately before the demerger, become the liabilities of the resulting company by virtue of the demerger. The image below explains the concept of demerger clearly.

Advantages of demerger

- It helps to concentrate on core competency;

- After the demerger, each company will have its balance sheet and will raise its funds. And this will lead the demerged company accountable for its account.

- It helps in increasing capitalization.

How did the demerger take place?

Section 232 of the Companies Act, 2013 covers the process of merger and acquisition which also covers the concept of the demerger. Demerger can be affected by the following:

-

- By the virtue of agreement entered between promoters: Here the agreement is entered between the promoters, which results in the principal company transferring its property, liabilities, and issues to the resultant company before the demerger.

- By the schemes of arrangement with the court’s approval: this is based on the powers provided to a company in its Memorandum. This requires approval from the Tribunal. The scheme of arrangement is an important document in the demerger it binds all the stakeholders of the company.

- Demerger and voluntary winding up: the company which has demerged itself into several companies after splitting can wound up voluntarily under section 484 to 498 of the Companies Act, 1956.

Comparative analysis

The table provides a comparison between various methods of undertaking M&A transactions.

|

S. No. |

Type of Transfer |

Stamp Duty Implication |

Tax Implications |

Carry forward of losses |

|

1. |

Asset sale |

The Rate of stamp duty that is to be paid on the asset purchase agreement is specified by the state. |

When it’s a case of depreciable assets, the capital gains computed on a block of asset basis and the value over and above the aggregate of the written down value of the block of the assets and expenditure incurred in relation to the transfer will be treated as the capital gains and subject to tax as short term capital gains. Whereas in other cases, capital gain payable by the seller will depend on the period that the seller has held each of the assets that are transferred. |

Not allowed |

|

2. |

Slump sale |

The Rate of stamp duty that is to be on the slump sale is specified by the state. |

When capital gain realized on the transfer of the undertaking, if held for more than 36 months, are taxed as long-term capital gains. If the assets are held for less than 36 months are taxed as short-term capital gains. |

Not allowed |

|

3. |

Share sale |

The Rate of stamp duty that is to be paid on state transfer is specified by the state and maybe on the value of the shares sold. |

When capital gains realized on the transfer of listed shares, held for more than 12 months is taxed as long-term capital gains. Capital gains are realized on the transfer of the shares, held for 12 months or less is taxed as short-term capital gains. |

Is permissible if a change in shareholding does not exceed 49 percent. |

|

4. |

Demerger |

The Rate of stamp duty that is to be paid on demerger is specified by the state. |

When there is a tax neutral demerger then there is no capital gains tax liability and if the transaction is covered under Section 47 of The Income Tax Act. Usually undertaken for restructuring of group companies. |

Is allowed if conditions under Section 72 A of the Income-tax Act are satisfied. |

|

5. |

Amalgamation |

The Rate of stamp duty that is to be paid on amalgamation is specified by the state. |

If it is a tax-neutral amalgamation then there is no capital gains tax liability. And if it is covered under section 47 of the Income Tax Act. Usually undertaken for restructuring of group companies. |

Is allowed if conditions under Section 72 A of the Income-tax Act are satisfied. |

Conclusion

The decision to opt for the structure for M&A transactions differs from case to case. Each structure has its own merits and demerits. The buyer and the seller had to choose wisely which structure they wanted to opt for. Acquisition of business is crucial as it helps a business to expand in size or territory and to assist a business in diversifying risk. Ensuring the smooth and cost-effective transfer of the transferee company is important to the purchase of the undertaking. There are various routes of business transfer, each route has different cost implications and one has to choose the structure which will be most beneficial to it.

References

- https://nishithdesai.com/fileadmin/user_upload/pdfs/Research%20Papers/Tax_Issues_in_M_A.pdf

- http://www.nishithdesai.com/fileadmin/user_upload/pdfs/Research_Papers/Deal-Destination-Business-Transfer.pdf

- https://www.wikiaccounting.com/depreciation-accounting/

- https://www.genesislawfirm.com/asset-acquisition-stock-purchase-and-merger-structures

- https://image.slidesharecdn.com/1-160315120829/95/accounting-and-income-tax-aspects-demerger-3-638.jpg?cb=1458044602

- https://www.valentiam.com/newsandinsights/corporate-restructuring-strategies

- https://www.taxdose.com/demerger-section-219aa-income-tax/

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications