This article has been written by Joe Mathew, pursuing the Diploma Programme in Business Laws for In-House Counsels from LawSikho.

Table of Contents

Introduction

COVID-19 pandemic has seen a surge in the number of digital users. We saw a dramatic rise of over the Top platforms in India. People, particularly youth, were inclined to web series and movies in different languages. Recently I happened to hear an interesting plot.

Well, here is the storyline:

“Where a giant company with huge debts is conceded into the bankruptcy procedures, tt thus turns out to be somewhat the biggest insolvency in the country and in the end prompts an outcome of twists and turns “

Sorry, my dear colleagues, It is not a premise about class action films. This is a milestone case in the Insolvency and Bankruptcy Code 2016, a pronouncement made by the honourable Supreme Court of India on November 15, 2019, and which is called the Essar Steel Judgment.

I went through the landmark ruling and it felt like an important chapter in the history of IBC. In a way, it has tried to delve into every aspect of the Act. It would be an ardent task to write about it in one article. So here I have attempted to learn and analyse the verdict in layers.

First, I would like to introduce the very important aspects in the Act. Part 1 draws attention to the role of Insolvency and Bankruptcy Code, creditors, interim resolution professional, resolution plan and adjudication authority.

In order to comprehend a case, it is quite appropriate to investigate the facts and circumstances. Second part captures it in a profound way like background, arguments and notable observations by the court. These insights help readers to draw inferences and associate with the factors that lead to decision.

The analysis is all about your takeaways. At the end of the day, the final question would be how you make sense of the ruling. I believe this is something fundamentally relevant which also augments our critical skills. Final part reviews my understanding and assumptions focusing on insolvency and recent developments in the Act.

IBC, 2016

Huge pile of debts and non-performing assets has caused misfortunes to the banking system and creditors. Despite the fact that there are laws on different facets of insolvency somewhere around it was in dire straits. This inspired authorities to address the concerns and comprehensively redefine existing pictures. Under the authority of TK Vishwanathan, former Union Law secretary and Secretary-General of Lok Sabha, the Bankruptcy Law Reforms Committee was formed. Upon the recommendations of the committee and a clarion call for reforms, the Insolvency and Bankruptcy Code was passed by Parliament in the year 2016.

Some people often misunderstood the Act as a mere recovery mechanism. It is quintessential to perceive various objectives to comprehend why it was implemented:

- Applicable on companies, limited liability entities, partnership firms and individuals.

- Eradication of the complicated process of Insolvency.

- Revival and Redemption of the Corporate Debtor.

- Reconsider the relation between Creditors and Debtors

- Distribution of assets in a systematic order.

- Established deadlines for Insolvency Cases.

Financial creditors and operational creditors

Both parties fall under the domain of creditors yet they stand on different pedestals. The primary difference between them is the relation with debtors. In the case of financial creditors, it is the financial dimension that encompasses the definition and operational creditors it may be in the form of an unpaid supplier who has supplied goods or services or outstanding dues of employees, etc.

What IBC says about financial creditors?

Section 5(7)- “A person to whom a financial debt is owed and includes a person to whom such debt has been legally assigned or transferred to“.

Financial creditors are the entities like banks or financial institutions that lend money to the corporate enterprises. In various decisions, the court has cited the supremacy of financial creditors over operational creditors. The rationale basis of financial creditors is found in the presumption of financial debt. However, the definition calls two crucial aspects for notice:

Financial Debt

To lay it out simply, payment of money against the consideration of time value of money is called financial debt. Moreover, financial instruments recommended in Section 5(8) of the Act are also included in the definition and most importantly it is not merely the amount advanced that matters but the time value connected with the debt. Court has shed light on the concept of “time value of money” on various occasions. It involves time identified with the conveyance of money which may be the interest rate, market rate and so forth.

Supreme Court in its judgment of Anuj Jain Interim Resolution Professional For Jaypee Infratech Limited v. Axis Bank Ltd etc. specifically laid down that the basic ingredient of financial debt is debt along with interest distributed against time value of money or debt should be under any modes or events in Section 5(8) of the Act. Only if the required elements subsist the creditors could be called financial creditors and debt as financial debt.

Assignment

The word assignment appears to be a familiar one. Yet in financial understanding, it is quite different. Under the legal framework according to a contract, the debts and obligations are transferred to a third party. Thus assignee steps into the shoes of the assignor who is the creditor and fully entitled to recover the debts. It is one of the significant aspects of business transactions.

However, recently, there has been a growing trend where debt is assigned to a non-related party to dilute the rights of other creditors. The decision of National Company Law Appellate Tribunal (New Delhi) Bench in the case of Pankaj Yadav and Branex Impex Ltd v. State Bank of India and Fortune pharma Ltd. (2018) held disqualification that existed for related parties at the beginning of Corporate Insolvency Resolution Process could not be denied by assignment where related parties suddenly become a non-related party.

Operational creditors

Another group of individuals whose interests are at stake with the corporate debtor.

Section 5 (20)- “A person to whom an operational debt is owed and includes any person to whom such debt has been legally assigned or transferred “.

Now, what about the operations of a company. The scope of operations is huge and multi-dimensional in a business. Sometimes the company may not be in a position to pay back the money which is the debt arisen within the operations of a company called operational debt. Debt may be in the form of supply of goods and services, employee’s payment of any dues under any law or authorities. This is where operational creditors come into the picture. In fact, they are on the other side who provide the services.

Let me give a context for better understanding. Suppose you are a big steel manufacturing unit. For business functions, the steel enterprise requires power. Electricity Company supplies electricity and there is a claim in respect of the service disbursed. If the default exceeds the threshold limit under the Act, then the company as an operational creditor can initiate the insolvency proceedings. In other cases, if as a company you owe any taxes or fees to statutory authorities then the government is the operational creditor i.e. with respect to goods or services or debt in payment of outstanding tax or dues. Another important aspect is that the debt should arise with the business activities or operation of the company. Unlike Financial creditors it is not about direct financial relation that governs operational creditors it would be how you claim in respect of goods or services.

What differentiates financial and operational creditors?

The most significant distinction between financial and operational creditors was laid down by the Supreme Court in Swiss Ribbons case (25th January 2019). Court held that financial creditors can better assess the financial feasibility and value of the corporate debtor. They have the ability to recognize their business and ensure a free path of survival. This isn’t something operational creditors could undertake. Thus, it is a difference which can reinstall the corporate debtor on a sound financial avenue.

Committee of Creditors

In the movie 12 Angry Men, we saw 12 jurors retire to the jury room to decide the fate of a teenage boy accused in a crime. Eventually, they were left in a position to introspect their own prejudices.

Here, we have a committee who possess certain powers and duties with the objective of survival and restoration of corporate debtors. Could you imagine a situation where people or institutions who have advanced money or services come pouring in one day? Thus, IBC has introduced a committee called a Committee of Creditors (CoC) to consider their grievances and comprehend the commercial viability of debtors.

After the collision of all claims of corporate debtors, Interim resolution professionals shall constitute the committee. They conduct meetings where they are entrusted with certain voting rights and possess the right to accept or reject resolution plans proposed by resolution applicants. The bottom-line is the committee decides about the strategies to recover the debt.

A substantial part of the committee is financial creditors. All decisions pertaining to revival and implementation of the corporate debtor are taken by CoC by the majority of the vote not less than 66 % of voting share of creditors. Nevertheless, operational creditors are allowed only when there are no financial creditors pertaining to the corporate debtor and the former should meet prescribed criteria under the Act. As per Section 24(2), (3) and (4) of the Act, Operational creditors can be part of the committee when there is no financial debt claimed. Such people will have limited rights to receive notice of the meeting and to attend such meetings provided their aggregate dues are at least 10 % of total debt.

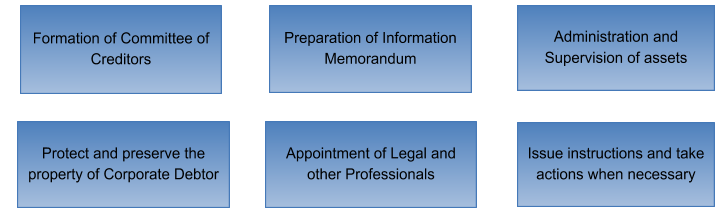

Interim Resolution Professional

There should be someone who shall form CoC and safeguard the corporate insolvency resolution process. For this purpose, the Adjudicating Authority shall appoint an Interim Resolution Professional (“IRP”) after fourteen days from the commencement of insolvency. IRP acts like a CEO for the company. Enrolled under Section 206 of the Act with an insolvency professional agency, duration of IRP continues until a resolution professional is appointed and in most times IRP is appointed as the same.

Some of the functions and duties of IRP are:

Secured and Unsecured Creditors

Other classes of creditors who have defined rights and obligations are secured and unsecured creditors. Secured are those who advance payment by creating security in favour of the creditor in the transaction. A security interest may be in the form of right, title charge, mortgage, etc. Court has laid down the principle that financial creditors can be secured or unsecured and operational creditors are normally unsecured creditors. Apex court has absolutely examined the equality principle of secured and unsecured creditors in the Essar steel judgement.

Secured creditors cannot exercise the right of enforcing security because of the moratorium during CIRP. Further, in the liquidation proceeding where they can renounce security interest in the asset and receive its gains from the sale of the assets or can realize security interest in the procedure mentioned in pursuant to Section 52 of the Act. In the case of unsecured creditors, the procedure to recover dues is somewhat similar to the insolvency resolution by operation creditor in Section 8 of the Act.

Corporate Insolvency Resolution Process

The fundamental object of the Act is to restore the corporate debtor from its sickness. So as to cure its sickness and to recover the money of creditors there is a mechanism called Corporate Insolvency Resolution Process (CIRP). On an application of a Financial or operational creditor or a corporate debtor himself, NCLT can initiate the proceedings. Usually, there is a misconception among people that insolvency resolution is liquidation.

According to data released by IBBI in 2019:

“56.17 percent of CIRPs ended in liquidation and only 14.93 percent ended with a resolution plan”. (https://www.ibbi.gov.in/uploads/whatsnew/cff2db5cfaa42ed5aad9544b04bfac8b.pdf)

Section 33 of the Act prescribes conditions when a resolution plan of a company ends and begins liquidation proceedings. As per the recent amendment to Section 12 of the Act, the CIRP shall be completed within a period of 330 days and if not concluded then to a final extension of 90 days.

Resolution plan

It is tantamount under the Act to have a resolution plan. More or less for a corporate debtor, it is like an exit plan. Here you will have the resolution applicants who may submit the plan to CoC. Then the committee will have to approve the plan by not less than sixty-six percent of votes.Prospective resolution applicants shall be corporate entities, investors, employees or defined under section 5 (25) of the Act. However, the person shall be subject to disqualifications under Section 29A of the Act. In the matter of Essar steel, the initial resolution plan submitted by Arcelor Mittal and Numetal Limited was rejected because there were non-performing assets of their corporate debtors and it attracted ineligibility under the Act.

As or perhaps, more importantly, one has to recognize different dimensions of contents in the resolution plan. Whether the proposed plan is feasible or viable, duration and deadlines, interests of all stakeholders which includes financial and operational creditors, and amount due to creditors are some of the few things that the resolution plan aims for.

Adjudicating Authorities

In the insolvency resolution and liquidation related matters, the adjudicating authority shall be National Company Law Tribunal (‘NCLT”). The authority is also vested with the powers of Debt Recovery Tribunal in Part 3 of the Act where the default of individuals and partnership firms is not less than one thousand rupees. The appeal process falls under the purview of Section 62 of the Act. If a person is aggrieved by the order of NCLT, it can be challenged before National Company Law Appellate tribunal and secondly an appeal to the Supreme Court of India. Thus the Adjudicating authority is a three-tier mechanism which includes NCLT-NCLAT & Supreme Court.

Conclusion

To conclude the basic idea here was to highlight some of the important concepts in the Act. I don’t think that I have emphasized each and every objective. There are a lot more elements where to an extent which I tried to introduce their key roles and responsibilities So from creditors to the committee of creditors the process journeys through Interim resolution professionals and finally ends in a resolution plan. In the event that it doesn’t work out how about we forget what has happened and proceed into Liquidation?

References

- Standard Chartered Bank and State Bank of India Vs. Essar Steel India Limited (NCLT Ahmedabad)

- Swiss Ribbons Pvt. Ltd. vs. Union of India on 25 January, 2019

- Pankaj Yadav & Brainer Impex Ltd. Vs. State Bank of India. Ltd. & Fortune Pharma Pvt.Ltd (Company Appeal (AT) (Insolvency) No. 28 of 2018) .

- https://www.ibbi.gov.in/webadmin/pdf/whatsnew/2019/Jul/Essar%20Steel_2019-07-04%2016:25:31.pdf – (NCLAT decision)

- https://www.ibbi.gov.in/uploads/order/d46a64719856fa6a2805d731a0edaaa7.pdf

- https://www.mca.gov.in/Ministry/pdf/TheInsolvencyandBankruptcyofIndia.pdf

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications