This article is written by Tejas Geetey who is pursuing a Diploma in Business Laws for In-House Counsels from LawSikho.

Table of Contents

Introduction

The aftermath of COVID-19 has led to a stoppage of normal day-to-day functioning of business and industries. The lockdown has led to restriction of movements for various licencing purposes including stamping which has forced the government to adopt digital and technological advancements. Many state governments including Karnataka have proposed to end the physical franking of documents and introduce the e-stamping method as a mandatory process for the legal approval of the documents.

Franking signifies the process of paying the stamp duty. It has become necessary for the government authorities to alter the current mechanism of getting the documents franked. The purpose of this article is to inform and educate the reader about the current system in place for stamping the documents and how important it has become to alter the whole mechanism.

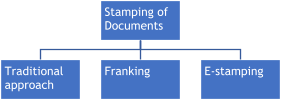

Stamping of Documents

Any document or instrument signed shall have a legal value assigned to it. This legal value and admissibility of these instruments shall be approved by the governments through the process of stamping. Stamping of the documents implies that the applicable tax/fees for making the document legally valid has been duly fulfilled by the payor. The stamping of the documents can be paid through many ways and mechanisms out of which one is franking. Franking is the process which signifies that stamp duty has been paid thereby making the document legally valid. For the stamping of documents, three procedures are followed which includes:

- Traditional approach – This traditional approach of stamping of the documents is also known as non-judicial stamps through which the payor purchases the stamp paper from the authorised institution or agent. The terms of the arrangement is signed by the payor and the agent to execute a written agreement signifying that the tax levied has been duly paid. As per this approach, the payor can pay the stamp duties before or after the execution of agreement. But the problem with this approach is that the scrutinizing of documents at every stage has led to inefficiency. This has made the traditional approach a slow and time-consuming process. Such inefficiency has made the system ineffective thereby making a breeding ground for many fraudulent acts.

- Franking – Franking is another mechanism to get the documents stamped. For the stamping of documents, a franking machine is used which is designed to stamp the documents thereby giving an approval to the payor that the taxes have been duly paid to the government. For the franking of documents, the payor has to approach the authorised bank or postal agency which affixes the stamp thereby giving legal validity to the documents. Additionally, the payor can also buy printed stamps. These stamps have already completed the franking process and are ready to be affixed at the time of signing or execution of the agreement.

- E-stamping – E-stamping is the digital approach to pay the taxes whereby an e-application is submitted for payment of taxes. Stock Holding Corporation of India Limited (SHCIL) has been designated by the Central Government as the central record keeping agency for the governance of e-stamps in India. For e-stamping of the documents, the payee has to follow a proper procedure as given on its official website. The payment and transfer of the stamp charges can be made through many states including Delhi, Gujarat, Karnataka, Rajasthan, Assam, Chhattisgarh and any other neighbouring states which have implemented the e-stamping portal [1].

Process of franking of documents

Stamp Duty is the tax levied by the government for the approval and implementation of documents and instruments. Article 246 of the Indian Constitution read with 7th Schedule gives the power to central and state governments to charge fees or taxes on providing legal value to instruments or documents [2]. The instruments to be taxed include documents pertaining to land properties, investments and other related transactions included under the Indian Stamp Act, 1899 [3].

For getting any document stamped, the person or organisation paying the taxes (hereinafter referred to as the payor) can do so through three different ways which includes franking, non-judicial stamp papers and e-stamping. For franking of documents, the following steps have to be followed:

- The payor has to submit an application to an authorized bank, postal institution or any other franking agency to get the document stamped.

- The internal procedure for the franking might vary from state to state. For illustration, maximum denomination against which a document is signed might change depending on that particular state stamp rules and regulations.

- Stamping of the documents is done through a franking machine whereby the document is stamped against a particular denomination. For example, the agency Indian Post franks the documents with a maximum denomination of Re 999. Thereafter, the payor has to inform the agency in advance for franking of the documents exceeding that denomination.

- After the approval of the document by the authorised institution or bank, the document is stamped through a franking machine. In this process, the stamp is affixed upon the document indicating that the stamp duty is duly paid by the payor.

- The stamped document or instrument thereby acts as a legally valid document which can be admissible as evidence in the court of law.

Importance and Usage of Franking

Franking is part of stamping of the documents. Any document to get legal validity has to pay stamp duty to the respective state or central government. The process of paying this stamp duty is done through franking which implies that the payment of stamp duty has been paid thereby making the document legally valid.

Stamp duty is one of the major sources of revenue for the government. Any document whether relating to home loan or for any other related purposes has to go through the process of stamping or franking. The government levies or taxes some amount for the stamping or franking of the documents. Only when the document is franked or stamped by the designated authority it gets approved and given legal validity. Franking charges differ from one state to another. For franking, each state has its own prescribed amount that is required to be charged. Although some states and authorised organisations do not charge any amount, there are other states that charge a percentage of the purchase value of the land its major source of revenue depends on the stamp duty collection.

Franking fees are normally just a fraction of stamp duty fees and are often adjusted in the stamp duty fees only. For instance, the franking price for any property to get stamped in Karnataka is calculated at a minimum 0.1% to a maximum of 5% of the sales value. For illustration, If a person purchases/mortgages a land for Rs. One (1) crore, then the franking charges for the document might vary from paying Rs. 10,000 to Rs. 50,0000 as franking charges which will be adjusted in the stamp duty.

Why does the current mechanism need to change?

The mechanism for the stamping of documents needs a complete overhaul. The traditional approach of stamping is exploited by the intermediaries and agents at every stage leading to interference and red-tapism thereby making the stamping process more complex and tiresome. Due to the lockdown, various restrictions were imposed on business and movement of people which lead to unavailability of agents or intermediaries. Additionally, most of the states are not equipped with franking machines and even among the states which are equipped, their licenses are generally expired. Thus, the availability and renewal of licenses is an important consideration. The denomination for franking of the documents is also generally fixed at a certain amount.

Moreover, the printed stamps which are already franked can also be used in only limited situations. It is reasonable to interpret from this that the current mechanism whether paper-based or through franking is not flexible. Many of these limitations have come to the fore due to the lockdown. It is palpably visible that a more flexible and dynamic system for franking/stamping of documents is needed.

The Way forward

Many businesses as well as major industries have been affected due to COVID. The government at the centre has been taking various measures for bringing the business cycle to a normal pace. It was observed in the landmark case of Kul Bhushan vs Chief Controlling Authority Chandigarh and Ors that the franking/stamping of documents was not executed as the agent was not available. The court therefore ordered that the collector should exempt the party from paying duties and not impose any penalties for the same considering the conditions and unavailability of any agent at that time [4].

It is therefore recommended that the government follow the reasoning adopted by the landmark case and provide reliefs to the payors from stamp duty and exempt them from penalties for non-payment of stamp duties in cases where such stamping and franking become impossible tasks to be performed. Stamping of documents is one of the major sources of revenue for the government which is exploited by intermediaries at every stage of stamping. It has become the need of the hour for the government to either overhaul the traditional and franking approach for the stamping of documents by providing better regulatory framework such as implementing the e-stamping process as mandatory.

References

[1] BV Shiva Shanker, ‘E-stamping may fully replace franking mode in Karnataka’(TOI, 5th Jan 2021) <https://timesofindia.indiatimes.com/city/bengaluru/e-stamping-may-fully-replace-franking-mode-in-karnataka/articleshow/80107763.cms> as accessed on 12th February 2021.

[2] The Constitution of India, 1950

[3] The Indian Stamp Act, 1899

[4] Kul Bhushan v. The Chief Controlling Authority, Chandigarh and Ors. (1991) MANU/PH/1608.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications