")

This article is written by Vaibhav Sachde, pursuing Legal Writing For Blogging, Paid Internships, Knowledge Management, Research and Editing Jobs from LawSikho.

Table of Contents

Introduction

In the technological era, the twenty-first century has improved the techniques of work all over the globe. Technology is increasingly being utilised in all sectors and at all levels. The legal industry makes extensive use of technology for legal research and data storage. And now, the most recent technological advancement is the application of artificial intelligence which is also being used in various areas of the legal field as well. Of the various fields, the rise in the use of AI-powered smart contracts is the talk of the town. This is one of the most sophisticated contract law practices in online commerce protocols for strangers. These are programming codes that are saved and duplicated on the system and are monitored by the blockchain’s computer network. Blockchain technology is also used for these AI-powered smart contracts. In the following sections, we will attempt to comprehend the future of AI-powered smart contracts in the Indian legal system.

AI and blockchain : how they function

Artificial intelligence is the practice of replicating human intellectual processes by computers, most notably computer systems. AI applications include expert systems, natural language processing, voice recognition, and machine vision. Artificial intelligence systems operate by ingesting massive amounts of labelled training data, analysing it for correlations and patterns, and then using these patterns to predict future states. A chatbot-given set of examples of text conversations may learn to create realistic dialogues with people via analysis of millions of cases, while an image recognition software may learn to recognise and describe objects in pictures through analysis of millions of instances. The three cognitive skills on which AI programming focuses are learning, reasoning, and self-correction.

As the name implies, the blockchain technology system is built on a blockchain. This method stems all the way back to 1991 when an idea was discovered to create cryptography to encrypt data in small digital chunks. These blocks are codes that not only encrypt the data but also serve as a timestamp for future reference. A blockchain is a digital ledger of transactions that is replicated and distributed throughout the whole network of computer systems that comprise the blockchain. Each block on the chain contains a number of transactions, and whenever a new transaction occurs on the blockchain, a record of it is added to each participant’s ledger. As a consequence, the data is not only protected, but can also be cross-checked for length, date, and temporal components.

The relation : smart contracts and advanced technology

As previously stated, AI enables the processing of large amounts of data, while blockchain provides security, immutability, and decentralised data storage. Such sophisticated technology with multifaceted capacities may be channelled for many purposes in our daily lives, and in the legal area, we utilise it in the form of smart contracts. These sophisticated technologies cover a wide range of applications, with smart contracts being only one of them. Now we realise how sophisticated technology has aided in the development of smart contracts.

The AI technology that can be used for smart contracts ranges from rule-based systems, such as expert systems that make choices based on input and rules, to more adaptable systems like logic, neural graphs, and neural networks. Artificial intelligence creates and executes complex smart contracts by using crucial analysis, making them more functional. And the more data AI has, the better its forecasts will be. To that end, when it comes to contract negotiation and determining the best route to reach an agreement, Artificial Intelligence may analyse prior discussions to determine how parties negotiated in the past. As a consequence, AI can recommend the kinds of clauses and wording that will be most effective in obtaining an agreement. Furthermore, its analysis of past contracts enables it to identify factors that were previously unconsidered and subsequently included in future contracts. Because a smart contract is a self-executing document that guides workflow, artificial intelligence may utilise previous smart contracts to analyse the strength of previous workflows and identify potential enhancements that can be employed in the future.

Artificial intelligence systems will be critical for interpreting data from a wide range of sensors and providing it in precise terms on which smart contracts may operate. Contracts that result in actual activities (for example, goods delivery) must, on the other hand, interact with robotic agents and humans. For example, operators and owners of vital energy infrastructure may need insurance contracts against damaging weather conditions and cyber-attacks. Thus, a smart contract would need to determine when the payment event will occur.

These AI-powered smart contracts are not specified in any Indian legislation as of yet, but for a basic concept, they may be derived from one of the notifications issued by the Telecom Regulatory Authority of India (TRAI) in 2018.

According to the notification, smart contracts are digitally encrypted agreements that are formalised using cryptography. Smart contracts are intelligent because they operate on the execution of pre-set instructions while also ensuring regulatory compliance. They also explicitly eliminate any possibility of human involvement or mistake. All of these processes and procedures are documented and handled on all of the systems at the same time. As a result, each party may verify the stage at which the agreement is now operating and whether it has been fully respected or not. The contractual party benefits from such contracts for a variety of reasons, the most important of which is that even if the party wants to modify or alter the agreement to his advantage, he cannot do so after it has been codified.

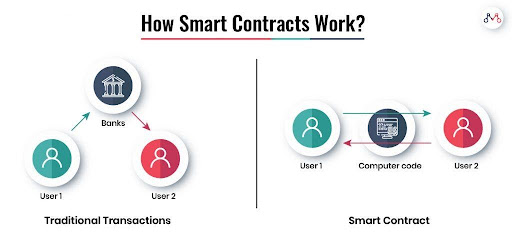

The difference : smart contracts vs traditional contracts

To get a better understanding of smart contracts, it is necessary to first grasp the distinction between them and traditional contracts. Traditional contracts simply refer to the most fundamental kind of contract. In which the parties agree on the terms of a contract while keeping in mind the transaction’s purpose and ultimate goal. These contracts provide the parties with a very flexible approach to contract amendments. This is definitely not true with Smart Contracts. As a basic comparison, smart contracts provide better security than conventional contracts, as well as fraud protection, cost savings, and immutability.

A brief overview of fundamental differences would be as follows:

|

Traditional contracts |

Smart contracts |

|

Contracts use orthodox methods.

|

Contracts are made with the help of the latest technologies. |

|

Function in accordance with agreed-upon legal conditions. |

The computer program that runs on its own. |

|

It is amendable at any moment with both parties’ agreement making it flexible. |

They are exhaustive and cannot be changed at the parties’ discretion. |

|

These contracts are susceptible to manipulation and tampering due to offline methodologies. |

These contracts are irreversible as they are secured by blockchain systems. |

|

These contracts are designed to be executed with human involvement. |

These contracts aim to keep human involvement to a minimum. |

|

This needed to be written or brought into existence each time for new cases. |

Have been designed to lessen the burden and the complexity of writing a new contract each time. |

Advantages of smart contracts

After understanding the distinction between smart contracts and traditional contracts, we can see that smart contracts outperform traditional contracts due to technological advantages. So, in summary, the benefits are as follows:

1. Cost

The operational and administrative expenses connected with the execution of smart contracts are minimal, since there is virtually no human interaction during the execution stage, the cost of the internet is quite low as compared.

2. Reliability

There is no question of clarity because smart contracts are implemented using computer codes. They do not need the use of confusing conversational language as traditional contracts do.

3. Quick and direct contact with customers

Smart contracts do away with the need for middlemen and enable clear, transparent, and direct interactions with customers.

4. Fraud prevention and records management

Smart contracts are stored chronologically on a properly distributed blockchain network, where their outcomes are verified by everyone on the network, ensuring that no one may broadcast or steal other people’s data.

5. Immutable

Because smart contracts’ security and coded structures are unalterable, they become impermeable and unbreakable.

Examining the Indian scenario for smart contracts

The extent of acceptance of AI technology

India, as a developing country, has to stand at par with technological developments around the world to have a good growth rate. As the trend is of such advanced technologies, various government agencies have begun to incorporate blockchain and artificial intelligence into their research and development programs, like the National Policy on Software Products (2019), Framework for Regulatory Sandbox, the Coffee Board’s Blockchain-Based Marketplace in India, and a few more.

Along with the aforementioned programs, there are a few other instances that recognize the importance of blockchain technology, like the indirect relevance mentioned in some of the court decisions. In the High Court of Delhi, a writ petition was filed and allowed for the registration of a patent. The patent claim was previously rejected by the Patent Office on the grounds that it falls under the category of non-inventions. As software is not patentable per se under Section 3 (k) 8 of the 1970 Patents Act, and as we know, artificial intelligence and blockchain are types of software. Thus, this petition emphasizes that simply because an invention is a form of software does not preclude it from being patentable. Rather, we live in a modern era of technology, where the majority of our daily tasks are automated through software advancements over the years. It is extremely orthodox and detrimental to ignore technological advancements such as blockchain and artificial Intelligence. All of these boost a bright future for such advanced technologies.

Though it is true that if a country has a favourable attitude toward such advanced technology, this does not imply that it will embrace smart contracts, but it still creates a brighter opportunity by promoting such technologies.

Indian statutes and the applicability of AI-powered smart contracts

As we have understood the Indian acceptance of the technical requirements of smart contracts. We would look at the acceptance of smart contracts as a concept under the Indian statutes and applicable laws.

Firstly, looking at the basic statute governing all contracts within India, i.e. the Indian Contract Act of 1872 This provides basic regulations for a contract being enforceable. According to Section 10 of this Act, “all agreements are contracts if they hold the free consent of parties willing to contract, for a lawfully accepted consideration and with an object.”

Now relating this to AI-powered smart contracts, we can establish that, as far as the Indian Contract Act of 1872 is concerned, smart contracts seem to be permitted by definition. Because a smart contract entails an offer, acceptance, and compensation in a valid form.

Secondly, looking at the Information Technology Act of 2000 (IT Act), which deals with cyber law relating to all technologies. The IT Act of 2000 has many sections, like Sections 5 and 10 addressing the significance, use, authentication, and production of Digital Signatures. The IT Act clarifies that if a document or information is required to be validated via the affixation of signatures, the need is considered satisfied if the information is authenticated using a digital signature. As a result, digital signatures serve as authentication mechanisms. Then comes the authority of certifying authorities, the process for granting licenses, and the responsibilities of such certifying authorities. Additionally, regulations governing the granting, suspension, and revocation of such licenses and digital signatures are included. The importance of knowing different types of digital signature procedures is to convey the impression that the government is inferring via these laws that self-generated digital signatures are uncertified and therefore invalid.

Now relating this to smart contracts, we can establish that, as stated before, smart contracts incorporate encryption into the ledger-based architecture. Additionally, smart contracts make use of digital signatures to provide authentication and secure restricted access. The sole exception is that digital signatures generated using blockchain and AI technology are not those allowed by the Information Technology Act of 2000. Self-generated digital signatures are used in blockchain and AI technology. This implies that any purposes for which documents, information, or forms must be authenticated via the affixation of signatures may be accomplished using smart contracts but are not certified under the governing law.

But to this, we have Section 65B of the Indian Evidence Act 1872, which states that contracts digitally signed shall be admissible in the courts. The government is therefore enabled to take legal action to settle the conflicts between the parties. So, it does not make the existence of smart contracts void.

Lastly, looking at the validity of cryptocurrencies in India. In March 2020, the Supreme Court under Mobile Association of India vs. RBI reversed the RBI’s 2018 circular which strictly prohibited all regulated entities from dealing in or providing services for the facilitation of virtual currencies on the internet. The Supreme Court said that in the absence of a legal prohibition on the purchase or sale of cryptocurrencies, the RBI cannot impose excessive limitations on their trading. This was also accepted by RBI, making the circular invalid. Thus, there is no issue with cryptocurrencies in India.

The importance of this to the smart contract is that, as seen above, any contract to be a valid contract needs a valid and lawful consideration. As with any other contract, including smart contracts, if you provide a service or sell a product, you expect to be compensated. One of the primary characteristics of smart contracts is that they enable rapid payment across the world in the form of cryptocurrency (which is a form of virtual currency). Thus, the 2018 circular would cause certain barriers, but the judgment has made a more hopeful pathway for the enforceability of smart contracts. Hence, the consideration of virtual currency is valid too in India.

The legal perspective of AI-powered smart contracts in India

Essentially, smart contracts offer a framework for negotiating with parties that may or may not know one another and may also become responsible for risks. While smart contracts are binding under Indian law, if care is not taken while contracting with another party, the penalties of a failed transaction must be borne alone, since the legal system lacks an elaborate framework for regulating smart contracts.

A smart contract may be unenforceable under Indian law in certain circumstances if the consideration for the contract is not reciprocal. This is possible if the contract is unilateral. However, smart contracts that lack mutual consideration are still enforced via code. However, a breach of such a contract would not be considered a breach in Indian courts, as the court would conclude that there was never a contract in the first place due to a lack of mutual consideration, a critical component of a contract.

While the legality of smart contracts in India permits their use, it does not provide legal protection to parties involved in the smart contract who become liable or incur damages. Because there is no regulatory framework in place to govern smart contracts, the law will assist to the extent that the smart contract falls within the bounds of contract law.

Successful instances of smart contracts in the present create future opportunities

In the Bajaj Group, Bajaj Electronics is a major electrical equipment manufacturer. As one of the most important actors in the Indian economy, its commercial operations have an impact on a wide range of industries and suppliers, both inside the firm and beyond. This was due to the fact that Bajaj works with a variety of suppliers and had to verify that each vendor’s transaction had been completed properly before the payment could be made. For its ‘Bajaj Electricals’ verification of delivery’ required a physical bill-of-exchange, and an invoice and further transport papers had to be submitted to Yes Bank to obtain payment.

Because of this, the company decided to look for a quick and secure alternative to replace its manual invoicing system. They settled on blockchain and AI as the answer. In the year 2017, Yes Bank also announced that they have implemented a multi-nodal blockchain transaction to completely digitalize vendor financing for Bajaj Electricals.

In a very recent development, i.e. in June, 2021, Gujarat-based ArcelorMittal Nippon Steel (AMNS) executed a paperless bill discounting transaction in partnership with ICICI bank. This was referred to as the country’s first domestic paperless bill discounting transaction.

Detailed analysis for future of smart contracts in India

Pestle analysis of smart contracts in India

PESTEL is for Political, Economic, Social, Technological, Environmental, and Legal – these are the elements that influence the operations and performance of any business idea. It is a straightforward framework that is simple to comprehend and use, allowing for a deeper and wider knowledge of the many facets of AI-powered smart contracts. Additionally, it enables us to predict future risks and devise strategies to mitigate or eliminate them. Finally, it will assist in identifying future opportunities.

Political

To begin, one of the primary benefits, when applied to politics, is security, and one of the primary drivers of change is increased transparency in government contracts. The government enters into contracts with a wide variety of parties on a daily basis. It deals with everything from small businesses to agreements with developed countries. Thus, using artificial intelligence and blockchain technology can be an extremely smooth, secure, and transparent process. As a result, its use is extremely beneficial. However, while there has been little progress, there is hope for the future because the banking industry, which is regulated by the RBI, has been adopting such contracts and is in the early stages, which is great hope for its success in the near future.

Moving forward to its political ability, we see that, with analysts forecasting rapid growth worldwide, the use of smart contracts is still relatively new to the market and faces numerous obstacles, most notably government regulations. Government support or opposition has a significant impact on the future of AI-powered smart contracts, both in terms of regulation and public sector adoption. The government can either support or oppose the adoption of such smart contracts in the market, and thus regulations can have a positive or negative effect on their development and widespread acceptance. Though we have seen some progress in support and research for AI technologies, there are no steps taken upfront to widen the scope of AI-powered smart contracts in India. RBI’s willingness to give full assent to cryptocurrencies is lacking. Though there is no ban on it, there is no proper structure for it yet and cryptocurrencies play a large role as considerations in smart contracts, as we have seen before.

Additionally, due to a lack of global coordination among authorities and diverse legal cultures, there are divergent views on how to best regulate this space. As a result, rules vary by country, depending on the level of technology and economic development in each country, which may affect the rate of adoption of such advanced technologies. Considering this in the Indian scenario, India is still a developing country with less developed technology than other first-world countries, so its ability to adapt or invest in such advanced technologies will take longer.

As a result, we can conclude that additional political efforts are required to ensure a bright future for the use of smart contracts in India. There is a possibility of a realistic approach to smart contracts in the future with multiple research efforts and government support.

Economical

The most significant benefit of smart contracts is the possible decrease in transaction costs as a consequence of the untamperable and self-executing nature of blockchain-based smart contracts. Smart contracts may be signed automatically if specific agreed-upon criteria are fulfilled, and the contents of the contract cannot be changed. Smart contracts have many important features, including improved transactional efficiency, cheaper enforcement, and monitoring costs, and reduced risk. These advantages may lead to reduced operational expenses, which can be passed on to customers, as well as more time to seek new clients or opportunities. Because smart contracts reduce counterparty risk, institutions may be able to conduct business with a broader variety of customers. The potential of using smart contracts not just between financial institutions and customers, but also directly between consumers, which may substantially reduce the expenses of attorneys, advisers, and other middlemen.

Smart contracts have a natural and successful use in supply chain finance, insurance, and consumer credit. Smart contracts can help close the large gap in the availability of financing for small businesses, particularly in developing countries and regions such as India, by lowering the cost of doing business with large commercial or governmental entities and lowering the risk for institutions. Insurance plans are well-suited to take advantage of smart contract automation by scripting certain outcomes to occur if certain criteria are fulfilled. Insurance policies may be made more broadly available by lowering the cost of issuing them and increasing confidence among parties. Similarly, the potential advantages of utilising smart contracts to automate portions of the consumer credit process, such as credit applications, thus increasing customer access to lines of credit.

But certain smart contract characteristics, such as the parties’ potential anonymity may create complications for customer verification and anti-money laundering regulations that require verifying the parties to an agreement. These problems may certainly be resolved by mandating precise technological requirements for the smart contract or the underlying blockchain.

There is considerable worry about the adoption of smart contracts, owing to the breadth of their use in a variety of diverse areas of employment. It immediately jeopardises millions of jobs. As seen before, smart contracts were developed in order to discover a more efficient and cost-effective method of conducting transactions and storing data. There would be no need for bureaucracy. Numerous unlawful practitioners will face significant changes, and there may be a strong reaction to the high rate of redundancy, as well as many individuals being forced to go on an entirely new profession and understand how such technology works in their area. In India, attorneys’ practices are still traditional, which makes it difficult for them to adapt. However, there is one positive side: individuals working in the technology industry will experience an increase in employment.

Thus, we may conclude that it offers significant economic advantages, but it does have certain drawbacks, as anything does. They seem to be solvable in some way.

Social

Today, it is necessary to upgrade old processing systems for contracting. As a step forward toward this, we are witnessing an increase in demand for smart contracts in sectors such as banking in order to get quicker and more effective outcomes. Efficient banking systems will facilitate access to financing and will enable banks to operate more efficiently. As a result of the rise in demand, investment and adoption are unavoidable. Additionally, the government is placing a greater emphasis on resolving the problem of excessive influence in contracting. Smart contracts open up new possibilities for India by establishing ‘digital identities for people who are not already recorded in the system. And the public is primarily concerned with privacy, data storage, and a new degree of security. There have been significant issues with exposed data, including the biggest data breaches in history.

The public is demanding action and reform on their right to privacy and information data management. Essentially, smart contracts establish confidence via transparency, since users may see previous participants, whose hashes are included in the blockchain. These sophisticated technologies have been designed in such a manner that the need for a middleman/party to handle data and information has been eliminated. This accomplishes the primary objective of protecting data privacy and gives people complete access and control over their data. The fact that smart contracts can address privacy concerns will boost public demand for this system. Also, in the situation of a pandemic and such health threats, paperless online transactions would always be preferred.

Additionally, once a smart contract transaction is completed and recorded, it becomes irreversible and is connected to the remainder of the transactions on that chain. Individuals in positions of power who were previously able to conceal or cover up unlawful activities will now be exposed due to the inherent transparency of such technology. It will be a significant benefit to society, but there will be resistance and reaction from those who have been exploiting individuals as a result of their use of immoral contract conditions.

The lack of public awareness of smart contracts at the district level or among small customers may have a major impact on their degree of acceptance. At the moment, such technology is in the early adoption stage of development. However, for mass consumerism to reach its zenith, it must first be recognised by the populace. Many members of the public are unaware of what it is or the various services it offers. Knowledge must be disseminated in order for such technology to develop. India may also encounter difficulties since we lack the technical advances enjoyed by other nations, and, as a result, it may take longer for us to completely integrate smart contracts into our legal system. It may take years for us to completely upgrade their systems and bring them up to par with first-world nations in terms of technology. This may impede the adoption process and lengthen the time required for adoption.

Despite the difficulties associated with implementing smart contracts in India, they will have a significant effect on the country’s culture and legal system. It provides a reliable means of establishing identification for all parties and identifying corruption and fraud, which are persistent issues in these transactions.

Technology

Due to the flexibility of smart contracts to adapt and alter the level of technology, they serve as a development platform for the legal sector. With the rapid development of technology, there is a great deal of interest and desire for it to pave the way for the next stage of technological innovation. The speed and ease with which contracts may be filed and the quality and validity it offers is the reason why businesses and governments are seeking to embrace it. It has the following characteristics: privacy, security, immutability, transparency, dependability, and process integrity.

The public sector and private sector have shown a growing need for a systematic approach to data dependability and security. The technology that underpins it allows for the modification of data kept on a node only after it has been approved by all parties connected to the blockchain. This ‘Proof of Work’ system provides businesses with dependable methods for ensuring that all information saved is secure and traceable in the event of future issues. All blockchain ledgers are validated using cryptography, which is a digital signature in layman’s words. This enables the traceability of any account or data that has been changed or generated. Additionally, permission ledgers were established to increase the secrecy of specific chains. This enables businesses to implement access-only systems, which restrict access to specific data to those with permission. However, as is the case with the majority of technology, AI and blockchain are always in danger of hacking and fraud.

Eclipse attacks occur when a hacker attempts to exploit a system’s vulnerability and targets a particular node/user. Additional research is being conducted in order to create a way of avoiding these hackings, but it will be required only if more businesses opt to invest in it. Security is a significant factor in the reluctance to invest in such technologies: although keeping all legal information has a number of advantages, there is a significant danger of critical and sensitive data being acquired via hacking. Thus, we can show that smart contracts have a significant technical advantage over paper transactions in this area, as the data is never lost. However, certain small issues must be considered to avoid them from becoming major ones.

Legality

Recently, there has been an increase in demand for security in contract formation and signing for paper waste systems for recording and safeguarding transactions and contracts. The new smart contracts streamline, automate, and standardise contracting. Blockchain technology securely saves all legal papers, ensuring that confidential documents are not tampered with and that all legal information is unalterable. It provides security by allowing for the traceability of all papers. As a result, it has become a source of truth for detecting and contesting contract violations. We can ensure the validity of a contract by implementing the consensus process, which ensures that no modifications, revisions, or interference are made after the contract is signed.

Additionally, smart contracts adhere to the consensus protocols’ proof of work mechanism, obviating any possibility of contract destruction. While the decentralised aspect of the blockchain is a benefit, it has generated an atmosphere of anxiety about the meaning of a lack of authority. This has resulted in a rise in global demand for the security and privacy of legal papers.

To be executed safely and effectively requires suitable controlling legislation. However, there is an issue in India; as we saw before, there is not much legal backing for smart contracts, and further, there are no well-established legal frameworks to govern cryptocurrency transactions, whether in India or elsewhere in the globe.

A government-designated certifying authority may acquire an electronic signature only according to Section 35 of the Information Act. This creates concerns, since it is the blockchain technology that produces the hash key that will be used to authenticate the smart contract, and there is currently no legal authority that sanctions electronic signatures. Section 88A of the Indian Evidence Act provides that the court presumes the authenticity of an electronic record presented in court but makes no assumptions regarding the contract’s sender. Thus, if a signature acquired through blockchain technology is utilised, it will only complicate the acceptability of a smart contract, since the signature was not collected in accordance with the Information Act. This not only invalidates the blockchain technology’s encryption mechanism for smart contracts but also precludes the filing of smart contracts as evidence before a tribunal.

Additionally, regulating the use of smart contracts would need a sophisticated approach to specifying the kinds of contracts and technology that may be utilised, rather than blanket legality. Apart from these minor technological details, the law will need to address several fundamental legal issues relating to smart contracts.

The pertinent legal question is whether jurisdictions will consider smart contracts to be legally binding contracts that adhere to the traditional contract pillars of offer, acceptance, and consideration, or whether certain smart contracts will be defined as general terms and conditions or accorded similar legal status. These decisions will be made based on basic legal principles, such as whether an offer, or a conditional offer, has been made, or if particular criteria of fairness and clarity relevant to general terms and conditions have been satisfied. Additionally, if smart contracts become extensively utilised, there will be a greater number of post-execution conflicts, since parties may argue whether a smart contract should have been executed, raising legal problems such as whether the code underpinning a smart contract is admissible as evidence in court. Additionally, for smart contracts to be broadly accessible and solve the problem of financial inclusion, they will need to connect with data sources and government organisations, which introduces a slew of third-party legal concerns.

The applications and advantages of smart contracts are gaining traction in economic and financial organisations on a daily basis. However, the success of smart contracts will ultimately be determined by the legal and regulatory problems that must be handled correctly to achieve full economic advantages. As smart contracts gain traction, we will almost certainly witness a flood of new legal problems arising from innovative uses, necessitating more complex, and continuously changing, policy and case law to enjoy the advantages of smart contracts.

Environmental

As we can see, there is little environmental concern. Some fundamental elements, such as paperless transactions, are a significant step toward environmental stewardship. While this helps to decrease paper use, it also presents an issue with excessive power and energy consumption. This goes against the trend toward more energy-efficient resources. This may act as a disincentive to investment in such technology, as global warming and environmental pollution continue to be a growing concern. Businesses are investigating new energy-efficient technologies.

SWOT analysis of smart contracts in India

SWOT analysis is a critical technique that assists in evaluating a business idea’s strengths, weaknesses, opportunities, and threats. It will assist us in building on the results of smart contracts and in understanding how to formulate kick-off strategies informally or more sophisticatedly as a real strategy instrument. Additionally, in identifying and resolving issues.

Findings for the future of AI and blockchain-based smart contracts

After conducting a SWOT and pestle analysis on the future of AI-based smart contracts in India, we determined that, despite the numerous advantages and benefits of smart contracts and their application in certain sectors, blockchain technology is still in its infancy and will take time to reach mainstream adoption. And, before embracing the technology, it is necessary to examine the legal and regulatory implications of the technology and smart contracts before they are accepted as a legitimate replacement for conventional contracts.

Additionally, we know that smart contract system are meant to be more autonomous, self-governing, precise, and transparent.

The advantages of digitizing one’s company are many, and the fraud protection, cost savings, and immutability of smart contracts are undoubtedly enormous. Smart contracts may be utilised in a variety of contexts, ranging from payment gateways to utility bills. This almost ensures that smart contracts will form the bedrock of the future global economy and will pervade every aspect of human existence. This cannot be accomplished until all issues have been addressed and a more structured legal strategy has been created.

An approach to a realistic future of AI and blockchain-powered smart contracts

Artificial intelligence is transforming how we live our lives, and many sectors are using AI. Using blockchain without AI requires businesses to take a step backwards. This is the true cause of smart contracts’ lack of success so far a lack of connectivity between AI and blockchain. The AI smart contract is a much-needed functionality that is currently absent from all major blockchains.

There is little doubt that the adoption and growth of smart contracts is the next step in innovation since they have the potential to immediately save billions of dollars in overhead expenses while increasing overall system efficiency.

However, regulatory concerns remain, particularly in India, where the finer intricacies of a smart contract are not regulated. Without explicit restrictions, widespread use of the technology would require changes to the Indian Evidence Act, 1872, and the Information Technology Act.

Thus, although there has been some progress in terms of legislation and business sector adoption of the smart contract idea, the law is still operating in a grey area. Vigorous commitment is needed to create an elaborate structure to govern the operation of smart contracts in India.

We need to understand that humans are creatures of habit, and we are innately resistant to change. However, given the advantages, adoption seems inevitable. On the other hand, rushing the creation of legislation may not be the best course of action until policymakers have a thorough understanding of the technology.

Conclusion

A deep glance through all the factors affecting AI-powered smart contracts is carried out. And a detailed analysis is done to understand the issue and its solution.

Regardless of the disruptive consequences of AI and blockchain-powered smart contracts, no one can dispute that the prospect of a system without central control is frightening. While blockchain-based technology has been dubbed the “next big thing” after the internet, it still lacks the data localisation and border control that the internet is subject to in one way or another. While we may anticipate the widespread use of smart contracts and Blockchain-based technologies in the future, it is critical to promote a broad understanding of the technology today.

References

- https://www.mondaq.com/india/fin-tech/889458/blockchain-and-smart-contracts-indian-legal-status

- https://hackernoon.com/ai-smart-contracts-the-past-present-and-future-625d3416807b

- https://www.mondaq.com/india/contracts-and-commercial-law/874892/the-enforceability-of-smart-contracts-in-india

- https://blog.ipleaders.in/how-is-ai-changing-contracts/

- file:///C:/Users/VAIBHAV/Downloads/Blockchain_and_Smart_Contracts_for_Insurance_Is_th.pdf

- https://www.hindawi.com/journals/scn/2021/9991535/

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications