")

This article is written by Hritika Jannawar, who is pursuing a Diploma in Companies Act, Corporate Governance & SEBI Regulations from LawSikho.

Table of Contents

Introduction

Companies have always sought to discover new ways to compensate their employees and instill the feeling of belongingness towards the organisation they work for. The inculcation of this idea of being a part of the company has helped various industries to retain the talent in their company and prevent poaching. Software industries were first to recognise the value of such compensatory schemes and adopted the Employee Stock Option Plan (ESOP) which enabled them to recruit and retain the best talents. In India, ESOPs came in trend in the early 90s and since then it has become a great tool to provide incentives to the employees, especially in start-ups, wherein the initial days the start-ups struggled to provide lucrative packages to employees. But surely can offer ESOP to share future benefits in the growth of the company, which makes it worth a while for the employee to remain in that job.

This article discusses the different provisions made for the ESOP for the listed companies by SEBI under Securities and Exchange Board of India (share-based employee benefits) Regulations, 2014 and unlisted companies under Companies Act, 2013 ( hereinafter referred as Act) and The Companies (Share Capital and debenture) Rules, 2014. Furthermore, the article dives into the discussion about how the ESOPs work from both company and employee perspective.

What is an Employee Stock Option Plan?

‘Employee stock option’ is defined in Section 2(37) of the Act as follows, “the option given to the directors, officers or employees of a company or of its holding company or subsidiary company or companies, if any, which gives such directors, officers or employees, the benefit or right to purchase, or to subscribe for, the shares of the company at a future date at a predetermined price.”

From the aforementioned definition, it can be concluded that ESOP is a type of compensation that the companies grant to their employees and use as a human resource development tool as it helps to recruit and retain the talent for a longer period. The core incentive that ESOP provides is that the plan has a predetermined price fixed at which the employee will be able to purchase shares at the future date and in case the company flourishes, that would result in profitability to the employee. ESOP also plays a vital function for an employee to feel like a part of the organisation he works for and is yet another means for an employee to acquire ownership in the company and that also at a concessional rate. Furthermore, ESOP is granted by a company to the employees as a matter of right and not an obligation meaning if the employee does not wish to buy equity under this plan he is not mandated to.

Important concepts related to ESOP

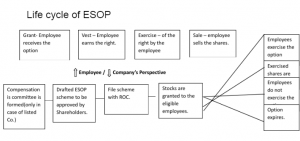

- Grant of option: The company decides the eligibility criteria for the employees to which ESOP will be offered.

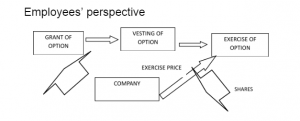

- Vesting of option: Occurs after the lapse of the prescribed minimum period after the grant of option and fulfillment of any performance-based criteria placed by the company (i.e. cliff period generally is minimum 1 year), after this period option gets vested, then only the employees can exercise their right. The options granted can be vested in the employee at one single stroke or in a phased manner; this is determined by the vesting period in the scheme.

- E.g. If 300 options are granted to an employee under the ESOP by the company, the company has within its power to stipulate the vesting of this option in a phased manner such as after one year of grant of option 100 options are vested and then after another year other 100 and so on, basically it stipulates the vesting of interest of 300 options over the period of 3 years. Hence the vesting period in this example is 3 years.

3. Exercise of option: It means once the option gets vested, the employee can exercise its right under ESOP.

4. Exercise period: The ESOP provides for the period within which the option has to be exercised after it gets vested.

How do ESOPs work : company perspective

Rules and regulations regarding the ESOP are different for both unlisted and listed companies. Unlisted companies are governed in regards to ESOP by Companies Act, 2013 and The Companies (Share capital and debenture) Rules, 2014 (hereinafter referred to as rules); whereas provisions for ESOP for listed companies have been made by SEBI in Securities and Exchange Board of India (share-based employee benefits) Regulations, 2014 (hereinafter referred as Regulations).

Which employees are eligible for ESOP?

Permanent employee of the company who has been working in India or outside India; director (not excluding independent director) or a permanent employee or a director of a subsidiary, in India or outside India, or of a holding company of the company.

Excluded from the ambit of ESOP

- The employee, who is a promoter or a person belonging to the promoter group.

- A director who either himself or through his relative or through anybody corporate, directly or indirectly, holds more than ten percent of the outstanding equity shares of the company.

In the case of an unlisted company, a start-up company, as defined in a notification issued by the Department for Promotion of Industry and Internal Trade aforementioned exclusions will not apply for ten years from the date of incorporation or registration.

Rules governing ESOP

Shareholders’ approval in the general meeting by special resolution to approve the ESOP. Separate resolution is required in cases of:

- Secondary acquisition for implementation of the scheme.

- Grant of option/any other benefit to the employees of the subsidiary, or the holding company.

- Grant of option/any other benefit to the employees in any one year, equal to or exceeding one percent of the issued capital (excluding outstanding warrants and conversions) of the company at the time of the grant of an option.

- In accordance with Regulation 6 by SEBI for listed companies, variation in the ESOP is subject to the approval of the shareholder in general meeting by special resolution, not being prejudicial to the interest of the employee. The Schemes can be varied to conform to the regulatory framework and can be varied before the employees exercise their option, whether they have been vested or not is an irrelevant fact.

- For unlisted companies: Section 62 (1) b provides for the grant of ESOP to the employees the rules governing it are provided under Rule 12 of The Companies (Share Capital and Debenture) Rules, 2014 (hereinafter referred as rules). Few important points have been enumerated below–

- Rule 12 (2) also provides the list of disclosures required to be annexed to the explanatory statement of the notice to pass the said resolution.

- In accordance with the said rules, the companies granting ESOP have the freedom to determine the exercise price in conformity with the applicable accounting policies.

- There shall be a minimum period of one year between the grant of option and vesting of option subject to the proviso under Rule12 (6)(a).

- The amount if any payable by the employees during the grant of the option will be forfeited by the company if the option has not been exercised within the exercise period.

- This amount can be refunded if the options are not vested in the employees due to non-fulfillment of conditions relating to vesting of options as per ESOP.

- The employees do not enjoy the rights of dividend or voting on the grant of option till such shares are issued by the company in the exercise of the option by the employee.

- The company specifies the lock-in period for the shares issued pursuant to such a scheme.

- The options granted to the employees are not transferable to any other person. The options cannot be pledged, hypothecated, mortgaged, or otherwise encumbered or alienated in any other manner. No other person other than to whom such options were granted shall be entitled to exercise such option.”

3. Listed companies:

- The provisions under the Regulation 5 states that the ‘Compensation committee’ has to be incorporated by the company for the administration and superintendence of the schemes under this regulation.

- It has to comply with the necessary compliances in Regulation 10 and the disclosures in accordance with Regulation 14.

Types of Employee Stock Option Plans

The Regulations provides for the following types of ESOP-

ESOS (Employee stock option scheme), ESPS (Employee Stock Purchase Plan), SAR (Stock Appreciation Rights).

- ESOS: Regulation 2 (g) defines it as a scheme under which a company grants employee stock options directly or through a trust. Regulation 16 to 20 deals with the ESOS.

The company has the freedom to determine the exercise price. The minimum vesting period is one year subject to the proviso under Regulation 18 (1). The company also has the liberty to specify the lock-in period. The Employee will have rights of voting or dividend only after the option is exercised by the employee and shares are issued in his name pursuant to it by the company.

Failure to exercise the option leads to;

- “Forfeited by the company if not exercised within the exercise period, or

- Maybe refunded to the employee if the options are not vested due to non-fulfillment of conditions relating to vesting of option as per the ESOS.”

- ESPS: Regulation 2 (h) defines it as a scheme under which a company grants employees shares, as a part of a public issue or otherwise, or through a trust where the trust undertakes secondary acquisition for the purposes of the scheme. Regulation 20 and 21 deal with ESPS.

Here the employee purchases the shares of the company at a discounted rate provided at the time of the grant which is lower than the fair market value and after the purchase of the shares the employee immediately becomes the shareholder of the company. Shares issued under this scheme are locked in for a minimum period of one year subject to conditions under Regulation 22 (2). If the ESPS is part of a public issue and is issued to employees at a rate similar to the public issues then the ESPS would not be subject to a lock-in period.

2. SAR: Regulation (2) zf and (2)ze defines it as a scheme that grants stock appreciation rights to the employees. Where the grantee is entitled to receive appreciation for a specified number of shares of the company. The settlement of the appreciation can be made in cash or shares. Regulation 23 to 25 deals with SAR.

In this scheme, the employees do not become the shareholder of the company nor the cap table of the company change. Notional units of shares are allotted under this scheme to the employees at the predetermined price called as exercise price to exercise the option of SAR after the vesting period. The base price is the price that is considered from the date of the grant for computing the appreciation. The minimum vesting period is of one year and no voting rights or dividend rights are acquired under this scheme.

What happens in the event of death, permanent incapacitation, or termination of employees in both listed and unlisted companies?

|

Regulation (listed Company) and Rules (unlisted Company) |

Event |

Interest |

Entitlement |

|

Death of the employee. |

All options granted/ any other benefit (Vested or not) till the event is happening. |

Vest in legal heirs and nominees of the deceased employee. |

|

|

9(5)and 12 (8) e |

Permanent incapacity while in employment. (Permanent disability) |

All the options granted (vested or not)/ any other benefit till the event happening. |

Immediately vest on the date of permanent incapacitation. |

|

9(6) and 12 (8) f |

Termination/ Resignation. |

Vested option/ any other benefit granted but not- vested option yet/ any other benefit. |

Subject to rules formulated by the compensation committee under Regulation 5(3) will be entitled to retain vested options. Expire/lapse. |

ESOP is designed to benefit employees who remain with the employer the longest and contribute most to the employer’s success. Companies Act, 2013 and the SEBI guidelines do provide the rules in regard to such aforementioned events happening, but other than this it also depends a lot on company policies which subject these to certain conditions.

Employees’ perspective

Once the shareholder approves the scheme, files with ROC then the eligible employees’ will be granted options. The detailed ESOP scheme will provide answers to questions like how much vesting period is stipulated. What is the vesting schedule? What is exercise price, exercise period, etc?

Once the shareholder approves the scheme, files with ROC then the eligible employees’ will be granted options. The detailed ESOP scheme will provide answers to questions like how much vesting period is stipulated. What is the vesting schedule? What is exercise price, exercise period, etc?

Understanding with the help of an example

- On 1st January 2021, a company granted its employees 300 options. The scheme of the ESOP stipulates three years the vesting period, vesting of 33.33% options occurs each year, the exercise price would be 10 per share and the exercise period is 5 years.

- Under the Companies Rules, there is a one-year cliff period between grant and vesting of option, therefore on 1st January 2022,100 options will be vested in the employee, and on 1st January 2023, another 100 options and another 100 options will get vested on 1st January 2024.

- As per the schedule of the ESOP, the exercise period is 5 years i.e. an employee has to exercise the options within five years from the date of vesting of those options. According to this the exercise period of options would be as follows –

|

No of options |

Vesting date |

Exercise within |

|

100 |

1st January 2022 |

1st January 2027 |

|

100 |

1st January 2023 |

1st January 2028 |

|

100 |

1st January 2024 |

1st January 2029 |

Now, if we consider the following scenarios –

- If the employee resigns on 24th September 2023, he will be entitled to the only a number of options vested in him till that date i.e. 200 and another 100 that were granted will lapse and if he resigns before 1st January 2022 all options granted will lapse and he won’t be entitled to anything.

- If the death of the employee occurs on 24th September 2023, his nominees/ legal heirs will be entitled to all the options vested i.e. 200 till date, and the another granted 100 options scheduled to be vested on 1st January 2024 will also immediately vest in them.

- If the employee suffers physical incapacitation while in employment on 24th September 2023, he will be entitled to all the options vested i.e. 200 till date and another granted 100 options scheduled to be vested on 1st January 2024 will also immediately vest in him/her.

Let us now assume that the employee decides to exercise his 100 options on 24th September 2023; he has to make an exercise application addressed to the company. The exercise price under the scheme was 10 per share, so the employee will pay the company 1000 Rs. And the company will allot 100 equity shares. As the scheme does not stipulate a lock-in period the employee is eligible to immediately sell those shares, but in some cases, the scheme stipulates, minimum of one year of lock-in period so in that case, the employee has to wait for one year to be able to sell those shares.

Potential scenarios when employees would not want to exercise ESOP

- In the case of unlisted companies as the shares are freely not transferable once the employee exercises his/her right under this scheme the money which the employee has used to buy the shares at a predetermined price get locked till the company gets listed or the promoters’ offers exit option to the employee. If such a lock-in period is not in consonance with the financial situation of such an employee he may not go further with the plan.

- In the case of listed companies if the market value of the share is lower than the predetermined price in ESOP.

The life cycle of ESOP

Taxability of ESOP

Taxability of ESOP

ESOPs are taxed at two instances

1. Prerequisite: at the time of exercise of an option.

When the employee exercises the option, the difference between FMV (fair market value) on the exercise date and the exercise price is taxed. It is deducted as TDS by the employer and is shown in the income from salary in the tax return.

Exception – Form FY 2020-2021, in startups the employees receiving ESOPs, are not liable to pay taxes in the year they exercise the option. This prerequisite is deferred to earlier of the following events –

1) Expiry of five years from the year of allotment of ESOPs,

2) Date of sale of the ESOPs by the employee or

3) Termination date of employment.

2. At the time of sale of shares

After exercising the options when the employee sells those shares, the difference between the selling price and FMV on the exercise date will be considered as capital gains and are taxable.

Now it depends if these gains are long-term or short-term capital gains on the basis of what period the employee had held the shares after allotment.

If the employee has held these shares for less than 12 months then the gains arising from this transaction will be considered as short term and will be taxed @ 15% and if such shares are held more than 12 months they are considered as Long term gains and are taxed at 10% if it exceeds Rs. 1 Lakh for listed equity and for unlisted short term gains are considered when the shares are held for 24 months or less and are taxed at the slab rate of the employee and Long term gains are when the shares are held for more than 24 months and are taxed at 20% rate.

How is FMV calculated?

- Listed companies – Average closing and opening price on the exercise date. If the day of the exercise of the option is trading holiday prices of immediately preceding day will be considered.

- Unlisted companies – Determined by a merchant banker on the date of exercise of the option.

Conclusion

ESOP gives ownership interest to the employees in the company, it helps to keep the employees focused on the corporate performance which consequently has an effect on share appreciation, these kinds of benefits when provided to the employees, attitude shifts from individual growth towards company’s growth i.e. these plans supposedly instill the feeling amongst the employees to do what’s best for companies i.e. ultimately to do what’s best for shareholders, since the employees are themselves the shareholders in this case. The employees exercise their rights pertaining to ESOPs on the vesting dates but there is no obligation on them and if he decides not to exercise the right, there shall be no tax implication.

However, there can be several challenges in the implementation of this exercise, especially pertaining to levying of tax on higher value if the share price falls at the time of exercise or the company performance becomes poor. In such cases, an employee may have to sell his shares under ESOP in order to pay for the taxes while disassociating with the company. Therefore, for the benefit of employees, it is important that the provision of taxation is applied only to real gain. Also, the companies need to have an efficient system with respect to the valuation and cost of ESOPs.

References

- Kartik Ganapathy and Ananta Krishna Iyer; Sweat, Stock, And Schemes; An overview of ESOPs in India, Mondaq, https://www.mondaq.com/india/shareholders/975390/sweat-stock-and-schemes-an-overview-of-esops-in-india#:~:text=The%20rule%20also%20prescribes%20that,equity%20shares%20in%20the%20company. Last seen on 25/05/2021.

- Getting ESOP as salary package? Know about ESOP Taxation, Cleartax, available on https://cleartax.in/s/taxation-on-esop-rsu-stock-options#:~:text=An%20employer%20and%20employee%20agree,or%20put%20simply%20%E2%80%93%20buy%20them. Last seen on 25/05/2021.

Students of LawSikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications