This article is written by Col. Rajesh Tandon, pursuing Diploma in Intellectual Property, Media and Entertainment Laws by Lawsikho as part of his coursework. Col. Rajesh works with the Indian Army for the past 29 years and has been handling the legal matters for 2 years.

Introduction

The property rights have always played their role in promoting the social economic and political development in various societies. The concept of property includes a person’s legal rights of whatever description. The Honourable Supreme Court of India in R.C Cooper Vs Union of India has defined the property as the highest right a man can have to anything to include the right of a man to ownership, estate, interest in corporeal things, the right to land or tenements, goods or chattels, the right to trade Mark, copyright, patents and even rights in personam capable of transfer or transmission such as debts and something signifying a beneficial right thing considered as having a money value. Largely the property is either corporeal or incorporeal. Corporeal property is the right of ownership in material things. Incorporeal property is of two kinds namely Jura in re aliena i.e encumbrances ( like leases, Mortgages and servitudes) and Jura in repropi (i.e patents, copyrights and trademarks). Intellectual property is the product of the human mind and intellect which emanates from the exercise of the human brain, something that involves the visual expression of a mental conception. When we talk of the transfer of business, it is imperative to understand the scenarios under which the transfer of business takes place. The ownership in the course of transfer of businesses can take place by the sale of a business or through the addition of a partner or Lease purchase or Family Member Transfer or through the process of merger/amalgamation, demerger, acquisition or takeover, divestments, strategic alliances or slump sale. While the transfer of business occurs, the assets and liabilities also do get transferred. In such a scenario wherein, the assets and liabilities are being transferred, it is very important to get to evaluate the value of intellectual property. A thorough evaluation of the value of intellectual property puts in a clearer perspective of the assets and liabilities to those to whom the business is being transferred.

The intellectual property

The Convention establishing the world intellectual property organization (WIPO) concluded in Stockholm on July 14, 1967, provides that intellectual property shall include the rights relating to:-

- Literary, Artistic and scientific works

- Performances of Performing Artists, Phonograms and Broadcasts.

- Inventions in all fields of human endeavor

- Scientific discoveries

- Industrial designs

- Trademarks, Service Marks and Commercial Names and Designations

- Protection against unfair competition

- All such rights resulting from intellectual activity in the Industrial, Scientific, Literary Or Artistic Fields.

Branches of Intellectual property

Intellectual property is usually divided into two main branches as under

Necessity to assess the value of Intellectual Property of the Business

There are various reasons to carry out an evaluation of the IP assets to ascertain their value. Some of these are as under:

- Evaluating the value of IP for shareholders.

- Evaluating the value of IP for:

- Mergers

- Acquisition

- Divestment

- Strategic Alliance.

- Management Buyout or By in

In all these cases, the valuation of IP enables the parties to make an informed decision for the acceptable cost of Capital i.e the rate of return that could be expected from such Business transfers.

3. Fund Raising

4. IPO

5. Licensing and Franchising of Intellectual property assets: In the course of licensing and franchising of intellectual property assets, the valuation of the intellectual property assets is of prime importance on account of the following:

- Once the value of the intellectual property held by the owner/patentee is known to him, it facilitates an informed Negotiation and Decision making with the licensee.

- It facilitates the determination of fair and robust royalty rates.

6. Assignment of Intellectual property Assets: The valuation of intellectual property assets facilitates the determination of Royalty rates to be charged while assigning the intellectual property assets.

7. Corporate Finance: The valuation of the portfolio of patents held by the firm is often carried out to assess the value of the intangible or incorporeal property for the purpose of obtaining corporate finance. A new phenomenon of securitization called Royalty Interest Securitisation is the trend in the market for obtaining Finance using IP. The salient features of Royalty Interest Securitisation are:

- Selling of IP to the Holding Company.

- The Holding Company issues bonds backed by revenues of intellectual property rights.

- The owner of the intellectual property gets upfront cash in this process.

- The bondholders are paid off over a period of time with the royalties.

- The Future Royalty Payments from the intellectual property are the founding basis of such securitization.

- The licenses of the intellectual property become a basis for offering the security for obtaining the Finance i.e the Intellectual property is used as collateral for loans.

8. Litigation: Whenever the cases of infringement are filed by a patentee, a royalty is often awarded to compensate the pit and the poor the unauthorized use of the patent by the infringer. In such a scenario it is very important that the value of patent must be assessed and determining the damages in the case of patent infringement litigation and for the purpose of assessment of reasonable royalty.

9. Transfer Pricing: A transfer pricing is the rule/method for determining the price for pricing transactions within and between the enterprises under common ownership. In layman’s terms, the transfer pricing is the rule for determining taxable profits/losses of a company in a country. Wherever there is a transfer of tangible or intangible assets, the rules of transfer pricing get applicable to such transactions.

Essential Pre-requisites for Undertaking Evaluation of Intellectual Property

There are certain fundamentals which must be satisfied before taking an evaluation of the intellectual property. Therefore a checklist is warranted before going in for evaluation of the intellectual property. Such a suggested checklist is as under:

- Whether there is a recognizable description of the intellectual property that is owned by the business which can be identified appropriately?

- Whether the intellectual property used by the business is such which is used by business with or without the permission of others who own such intellectual property?

- Who is the owner of the existing intellectual property assets viz:

- The company or

- one or more employees or

- consultants or

- Business partners of the company/firm

4. Whether there is Tangible evidence of the existence of the asset in the form of intellectual property needs to be there in terms of the following:

- A Contract of intellectual property viz:

- Assignment of patents, trademarks, designs, copyrights and Geographical Indications.

- Technology Licensing and Technology Transfer Agreements.

- A license of intellectual property.

- A Registration Document signifying the registration of intellectual property like registration of trademark, patent, and copyright.

- Financial Statement in respect of Intellectual Property.

- A client list of intellectual property.

5. Whether there is an intellectual property that can be legally enforced and legally transferred?

6. Whether there is an intellectual property that is able to generate its income distinct from the other assets of the business?

7. Whether there is an intellectual property that can be sold without selling the other assets of the business?

8. Whether there is an intellectual property that has got a definite period of existence

9. What are the factors which can affect the value of intellectual property viz:

- Too short a legal span/life of the intellectual property

- Availability of any substitute product or/alternative technology for the intellectual property in question.

- The likelihood of a third party claiming the ownership of the intellectual property in question.

- The market strength of intellectual property i.e the level of competent winners of Intellectual Property.

- What are the marketing strategies of this intellectual property in terms of:

- Aggressive Marketing Strategy or

- Conventional Marketing Strategy.

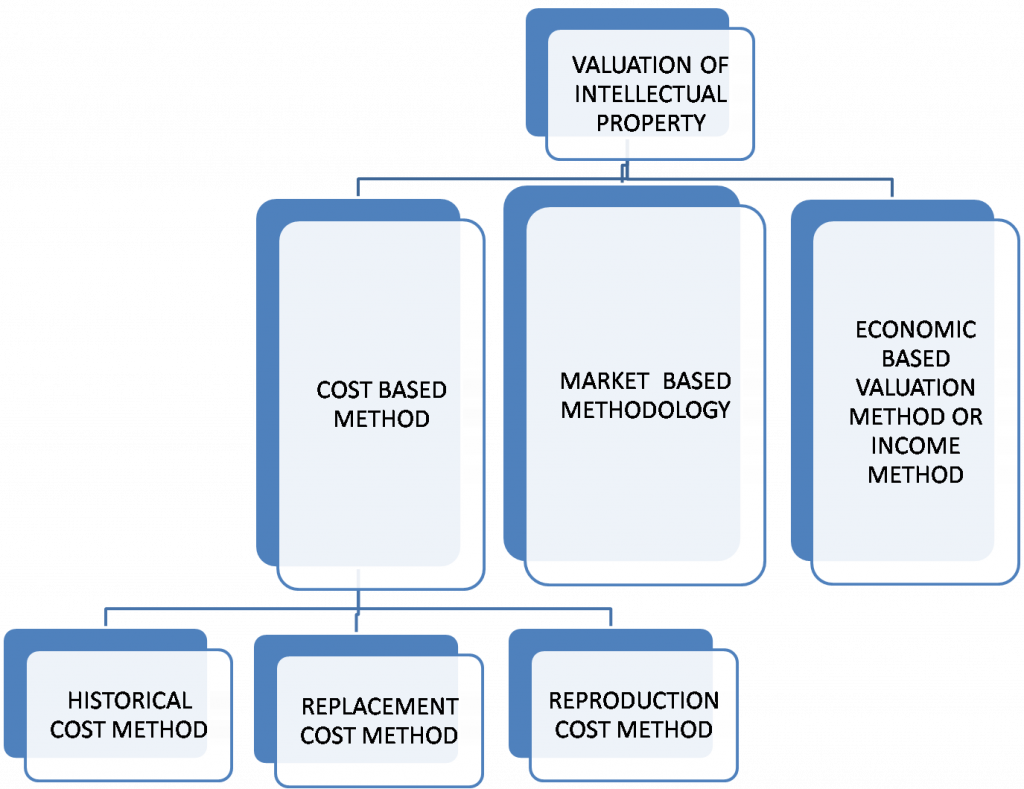

Method for valuation of Intellectual property

Normally one of the following methods for valuation of intellectual property are adopted:

Cost-Based Method

The different Cost Based methods are discussed below as under:

- Historical Cost Based Method: The salient features of this method along with the method of calculation are as under:

- Firstly, aimed at assessing the actual cost involved in the creation and development of intellectual property.

- Secondly, largely used for evaluation of IP assets in the research and development phase.

- Thirdly, the cost-based method works out the Actual costs incurred in creating and developing the intellectual property [H], and therefore takes into account the following parameters:

- Funds Invested- [F]

- The time cost of money [T] (based on a risk-free interest rate).

- Method of calculation with an Example: The formula for calculation of Cost Based Method is: H= F+T

- Parameter One: Let’s assume a situation wherein, an amount of Rupees 5 lakh per Annum is spent on research of a project for two years, whereby the total fund invested is Rs. 10 lakh. i.e F= 10,00000/-

- Parameter Two: Let’s Assume that the Time cost of money (T) involved is 5%

- The cost valuation of the IP would be H= F+T i.e 10,00000 +[(5,00000 x0.05) + (10,00000x 0.05)] i.e =10,00000 + 25000+50,000=Rs 10,75000/-

2. Replacement Cost Method: It is a method which calculates the cost involved in an recreating the functionality or utility of the IP in question. However, the IP so created by replacement may be in a form or pages that may be different from the IP in question. The salient features of this method along with the method of calculation are as under:

- Firstly, in this method the cost to replace the intellectual property is set to develop an alternative is worked out. In fact, in order to re-create the functionality or the utility of the IP in question, the use is made of the following:

- Modern Methods to develop the functionality of the IP in question.

- The state of the art design and layout.

- The new technology.

- Modern Methods to develop the functionality of the IP in question.

- Secondly, in this method, it involves assessing risk and estimates of future costs and benefits.

- Thirdly, the replacement cost method works out the Replacement cost valuation [R] and takes into account the following parameters:

- Funds Invested- [F]

- The time cost of money [T] (based on a risk-free interest rate).

- A Reasonable Risk Premium[M]

- The Utility of replacement cost method: Following are the instances under which the Replacement Cost Method can be used:

- To evaluate the value of IP in the case of negotiations.

- To work out the starting point/fundamental basis for charging the royalty rates.

- To settle on the transfer pricing

- To evaluate the value of IP in the case of negotiations.

-

Method of calculation with an Example: The formula for calculation of replacement cost Method is: R= (F+T) x M

- If the chance of failure as discussed in the example for Historical Cost Method is 30% i.e a situation where an there are 70% chances of success and 80% chances of failure than in M=100/ (100-30)=1.42.

-

Now taking the same example of F+T as discussed in the example of historical cost Method , wherein the value of F+T works out to be Rs 10,75000/-, we shall now work out the value of R (i.e Replacement Cost Method), since the formula applicable now is R= (F+T) x M. So the same is worked out as R=(10,75000) x1.42 = Rs1,526,500/-

3. Reproduction Cost Method: This method involves evaluating the price involved in creating an exact replica of the IP in question/a duplicate Asset. The salient features of this method are as under:

- Firstly, in order to reproduce and to create the same standard & Quality as that of IP in question the duplicate asset use is made of:-

- Same or Similar Materials

- Similar Design

- Similar Layout

- The utility of the reproduction cost method: Following are the instances under which the Reproduction Cost Method can be used:

- For the Purposes of Litigation.

- To assess the return on investment (ROI)

- For Tax Reporting Purposes like in the case of computer software.

- Method of calculation: Taking into account the current market value of following essential Parameters, the method of calculation is:

- The parameter of Cost Involved:

- Data Development- Rs D/-

- Labour/ Research Cost– Rs R/-

- Technology Development– Rs T/-

- Legal Fees– Rs L/-

- Others- Rs O/-

- The parameter of Cost Involved:

Reproduction Cost= D+R+T+L+O= Amount Rs X/-

The Concept Of Obsolescence

There are various kind of obsolescence which affect the value of the intellectual property:

-

- Functional Obsolescence: It is a case where the user of the IP has to incur taxes operational cost to use the IP depending upon the various alternatives including the state of the art to overcome the obsolescence so set in the IP.

- Technological obsolescence: It is a situation wherein on account of the advent of technology the better technological options are available in the market and the intellectual property becomes insignificant.

- Economic obsolescence: This is a situation wherein the intellectual property despite in its best form, yet it does not fetch adequate returns on the investment because of being unique, wherein the intellectual property has a little use beyond its particular function.

Alternative method of working out the cost taking into account the factor of Obsolescence, the reproduction cost, replacement cost

- Stage I: Initially in this stage, the replacement cost is worked out through the formula:

Reproduction cost-Curable Functional & Technological Obsolescence= Replacement cost

2. Stage II: In this stage, the replacement cost so worked out is used to estimate the value of IP as under:

Replacement Cost-Economic Obsolescence-Incurable Functional & Technological Obsolescence= Cost of IP

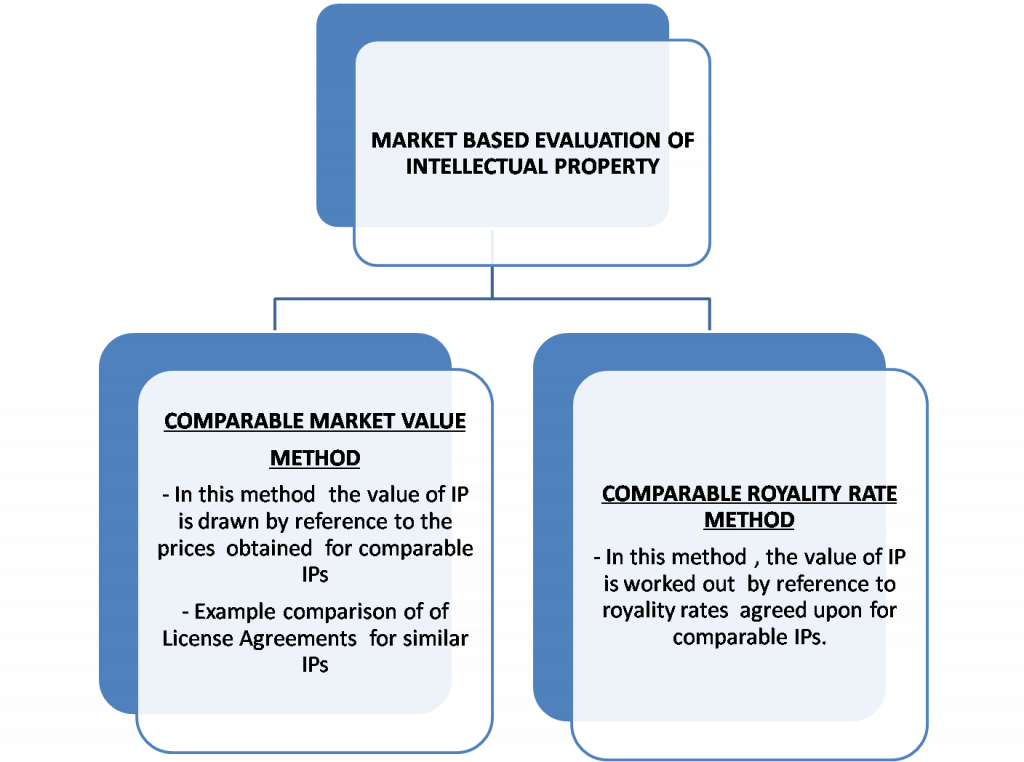

Market-Based Method

In this method, the valuation of IP, is worked out by drawing a comparison with the actual price paid for similar intellectual property asset under comparable circumstances (i.e whether the circumstances of cross-licensing or circumstances which make license agreed-upon in settlement of litigation). There are various factors which should be considered for the purpose of compatibility such as:

- What is the structure of the company of which the two IP assets are being compared

- What is the market size in relation to the two or more IP’s are being compared?

- What is the nature of Intellectual Property to be compared i.e:

- Whether it is copyright to be compared? or

- Whether it is a Patent to be compared? Or

- Whether it is A Trademark to be compared?

- Comparison of the extent to which intellectual property contributes to the market demand for the final product as different intellectual properties may conclude differently to the market demand i.e while comparing two copyrights or two patents or two trademarks, each such intellectual property may contribute differently to the market demand with a similar intellectual property. Therefore until and unless there is a near similarity between the two similar intellectual properties towards the contribution in the market demand, it may not be easy to compare the two similar intellectual properties.

- The licensor’s anticipated profitability from the use of the two intellectual properties being compared.

- The risk and profitability issues associated with the intellectual properties being compared.

- The Territory of operation/demand and geographical coverage of the two intellectual properties being compared.

- The substitutes available for the intellectual properties being compared.

- The scope of cross-licensing of the two intellectual properties being compared.

- The comparison of the legal protection of the two intellectual property is being compared.

- The state of development of the respective intellectual properties which are being compared.

- The market-based Method is of two types as depicted by the diagram under:

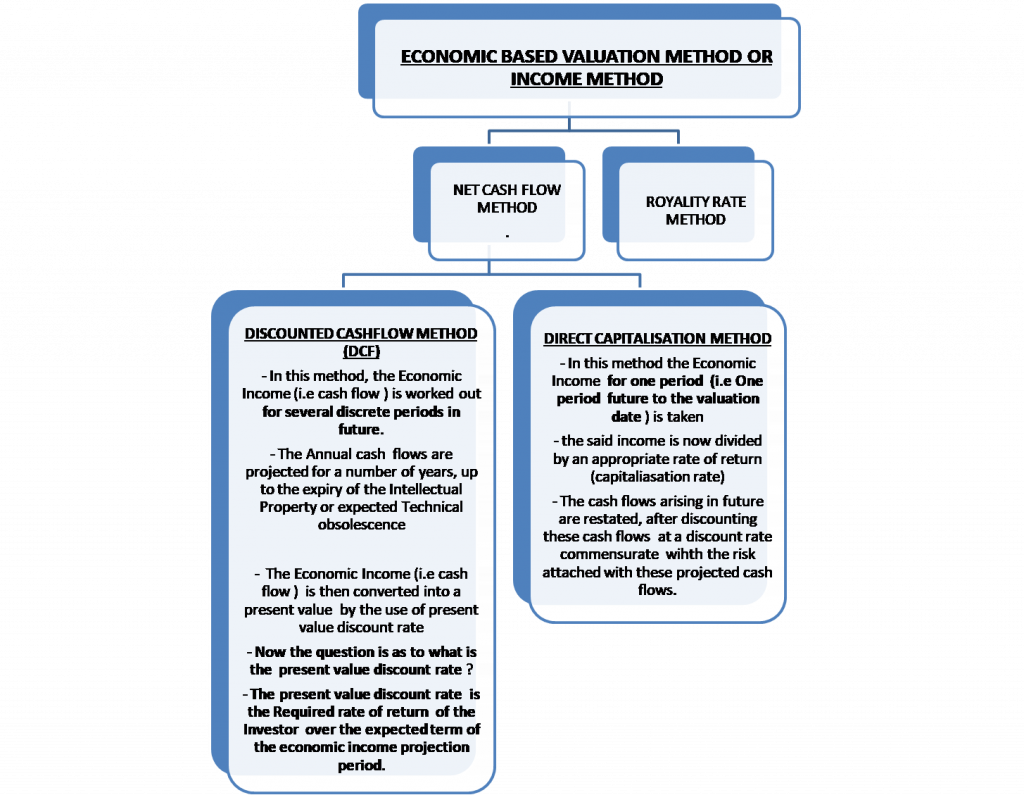

Economic Based Valuation Method or Income Method

Conceptually supposed to be the superior method as it addresses the issue of the contribution of the intellectual property. In this method, the amount of economic income that the IP as it is expected to generate is adjusted to its present-day value The two distinct components of this method are:

- Identification and Quantification of the cash flow for each intellectual property.

- The capitalization of these cash flows.

- The Economic Based Valuation Method is again of two types as depicted by the Diagram as under:

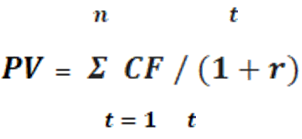

- Calculation of the present value under the Discounted Cash Flow Method (DCF)

- The Formula

Here,

Here,

PV= Present Value

CF= Cash Flow

t= time representing years of IP asset economic life

n=time that economic life is expected to end

r = Annual rate of discount(representing the risk factor) or time value of money and assumed.

- An Example of Working out the Present value with the above formula

- Let us assume that there is a company A which is negotiating to license the use of its patent.

- Let us assume that the current market value of the patent is Rs Ten lac (i.e Rs 10,000,00/-).

- It is expected by company A bad the royalty rates would turn out to be Rs 50,000/- [ Rs Fifty Thousand] annually over a period of five years (i.e the economic life of the patent).

- The risk-adjusted discount rate is estimated to be 5%.

- Accordingly, the present value of the patent will be as under:

1 2 3

PV= 50,000/ (1+0.05) +50,000/ (1+0.05) +50,000 /(1+0.05)

4 5

+50,000 /(1+0.05) + 50,000 /(1+0.05)

i.e

PV= 47619.04 +45351.47+43191.87+41135.12+39176.35=216,473.85

Thus , the company A would expect to receive at present, an amount of Rs 216,473.85/-, as Royalty Rate, if it licenses its patent for five years

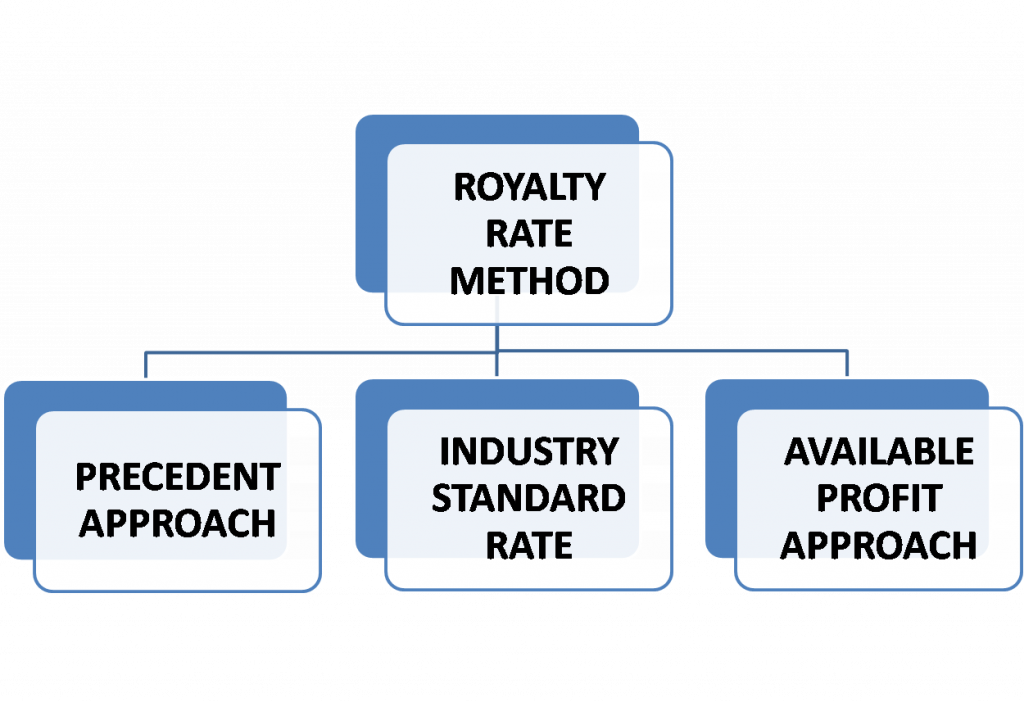

Royalty Rate method

In this method, the value of intellectual property is arrived by capitalising the post-tax royalty paid annually for the use of intellectual property under a hypothetical licensing arrangement.

There are three different approaches to work out the royalty rate method as under:

- The Precedent Approach: This approach involves:

- Examining previous licenses issued by the licensor for intellectual property.

- The royalty rates charged in previous licenses are generally the strongest evidence of royalty charged, provided that the previous licenses are similar to the licenses under consideration.

- The factors for comparison which should be considered to gauge whether the grant of previous licenses was carried out in similar circumstances are as under:

- The kind of technology and industry for which the previous licenses of IP were issued.

- The duration for which the previous licenses were issued.

- The Rights that were tagged with the previous licenses in terms of:

- Technical Support

- know-how

- Use of Trademarks

- The Territories Covered

- Any Reciprocal arrangements in the terms of Cross Licensing etc.

- The Industry Standard Approach: This approach involves factors like:

- The Terms of License.

- The Availability of Alternatives/substitutes.

- The capacity to make ancillary sales (i.e sale of non-patented/unbranded goods or services which are sold along with patented/branded items).

These factors are then considered in relation to the specific circumstances of the license.

- The Available profits approach: This method involves:

- Assessment of the Future Cash Flows.

- Consequently, the cash flows of the future are then compared for:-

- Situation with licenses

- Situation without licenses

The resultant comparison gives out the incremental cash flow that will arise from the grant of License. Such incremental cash flows can be divided between Licensor or licensee in terms of ratios like:-

- 25:75 or

- 33:67 or

- 50:50

Conclusion

In order to have effective decision-making, to negotiate the IP related contracts/agreements with a commanding position and to meet the legal accounting standard requirements and taxation liabilities, the evaluation of the intellectual property assets in a business enterprise is of prime importance and must be carried out from time to time.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

This is a good website we also inspired from Best lawyers in Chandigarh High Court.

Best explanation of intellectual property I have read so far. Thanks, Sir!