In this blog post, Chaminda Jayasundara guides our readers about how insurance companies make profit.

Insurance means a protection from monetary loss. Insurance helps to protect people against possible risks like fire, accident or burglary. This is mainly depending on the notion of the unforeseen that may happen in the future. Since the future cannot necessarily be presumed, it needs to protect the investments against the most foreseeable damages.

Insurance is a transfer of risk to a third party

This protection can be arranged by insurance companies, insurance brokers, attorneys, reserve analysts, etc. These institutions and personnel can collaboratively determine what types of losses any particular investment may face and how to protect the owners during and after a potential loss. Thus, insurance is a transfer of risk to a third party.

However, all risks cannot be transferred to a third party using insurance. Therefore, an insurable risk must have some characteristics such as –

- It is unpredictable and reasonably unlikely to occur. (Breckenridge, Farquharson, and Hendon, 2014)

- The policyholder has a genuine financial interest (usually called an insurable interest) in the risk, e.g. – it is not possible to take out a life assurance policy on a stranger’s life (Breckenridge, Farquharson, and Hendon, 2014).

- The loss that may arise from the risk can be expressed in monetary terms and is neither unimportant for the policyholder nor appallingly large for the insurer.

- Finally, it will be definite whether or not a loss has occurred and what is the monetary size of the loss. (Breckenridge, Farquharson, and Hendon, 2014)

What is Business Model?

Companies follow diverse business models be contingent with their products and services. They select or invent the model that will generate the most profit. The business model controls the trades and promotional strategies of the company including branding, pricing, sales networks and possible associates.

In The New, New Thing, Michael Lewis (2008) refers business model as “a term of art.” Like art itself, it is one of those things that many people feel and they can identify when they see it but cannot quite define.

Thus, he offers up a much simpler of definition, i.e. –

“Business model is how you planned to make money”.

Therefore, it is evident that a business model is nothing else than a representation of how an organization makes or intends to make money and/or profits.

Does Insurance Differ from other Business Models?

Insurance companies have a very different business model from most other types of business companies. One key aspect of insurers’ business models is the inverted production cycle.

- Inverted production cycle means policyholders pay premiums upfront and contractual payments are made only if and when an insured incident has happened.

This means that the large majority of insurance liabilities are not liable to unexpected claims. It means that insurers receive premiums upfront and deliver a service later.

- The inverted production cycle and the contractual premium payments of policyholders permit for a steady cash flow to insurers. However, in other business models, business has to market and sell the product first and then they receive money from the customers.

Due to this specific nature of insurance businesses, two main implications in business models can be easily identified –

- Insurers can earn an investment return over the period between premiums being paid in and claims being paid out.

- While most vendors can set prices based on a known cost of production, the price charged for insurance is set based on estimates of the future level of claims and expenses.

Thus, it is evident that the insurers can make profits mainly through good underwriting that means, by carefully selecting, costing and pricing the risks they take on and investment income that insinuates by investing premium income and making a return in excess of that needed to pay policyholder claims. Expense management and robust claims handling will also help to control the costs.

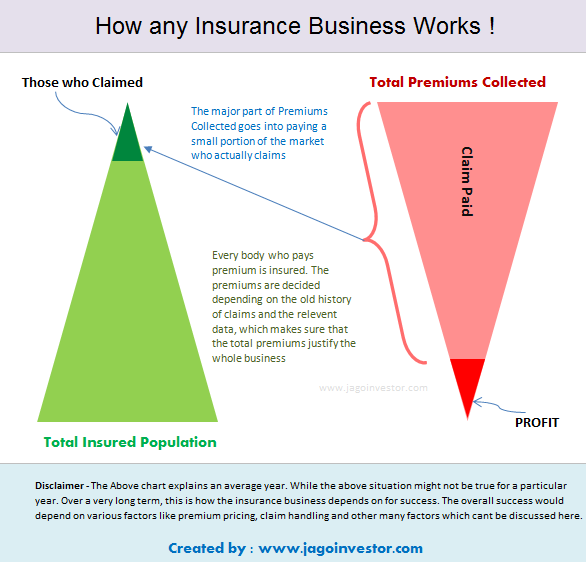

How To Make Profits (Business Model of Insurance Companies)

The following figure gives an overview of the business model in the insurance sector.

Source: Jago Investor

Principally, insurance is a contractual relationship between the insurer and the insured.

As discussed earlier, these contracts are different from normal commercial contracts. Most commercial contracts are subject to the principle of caveat emptor.

Under these contracts, there is no need to disclose information that is not asked for from the other party. Insurance contracts are usually different in that they are based on facts which are within the knowledge of the insured but of which insurers will not generally be aware (Belmont Virtual Academy (2013).

As the insurer is at a disadvantage, the law imposes a duty of uberrima fides or “utmost good faith” (Belmont Virtual Academy (2013).

- The principle of utmost good faith entails anyone seeking insurance to disclose all relevant facts. These are the facts that influence the judgment of an underwriter in calculating the premium or determining whether or not the company should take the risk. If insured doesn’t disclose all the facts relevant to the property and, if it can be proved, the insurance policy can be annulled. Thus, the business model is different from other models.

- In claiming the violation of utmost faith, insurance companies can be refraining of paying the claim to insured. Thus, the premium paid will be null and void for the insured and the total amount goes to the company as a net profit. However, if this utmost good faith requirement is fulfilled by the claimants and legitimacy of the claims, the company can make profits.

- Insurance companies realize profits by setting premium levels that are higher than might be necessary by including actuarial contingencies and by betting that actual benefit claims will be lower than the high estimates included in premium calculations ways (Hooper, 2009).

- Insurance companies also earn money from short-term investment of the premium money they collect as premiums are received at the beginning of a month but claims for services often are paid several months later ways (Hooper, 2009).

This implies that insurance companies are also like any other business in the world. They have to make a profit to stay in business. So that underwriting income and investment income are the main sources of profits in insurance companies.

Premium Collection

Insurance companies provide insurance by collecting premiums from policyholders and indemnifying those policyholders for covered losses that they suffered during the policy period. Because the actual cost of their product is unknown before the policy period elapses, they must calculate approximately their costs, usually with statistics and historical analysis.

If insurers have sufficient experience or knowledge of past events, they can use statistics to make high-level calculations. This process is called underwriting that involves calculating the probability of the risk for each insured or category of insured (University of Melbourne, 2015).

Based on the principle of large numbers, the larger the pool of policyholders, the more accurately the probability of the risk can be calculated (University of Melbourne, 2015).

The premiums charged are based on these calculations.

Certainly, there will be disparities in claim costs and the premiums collected which will enable the insurer to set a reserve to draw on in unhealthy years. This methodology is the focus on premium vs. claims.

However, this is most definitely not how insurance companies make money. Most insurers try to price their policies such that the total premiums collected each year are equal to the total amount of claims paid and expenses. Basically, this method called as combined ratio.

Combined ratio = Claims+Expenses = Premium.

The goal of a combined ratio of “1” is perceived as the perfect model because it means they are not over or under pricing their policies.

In other words, it means that they are underwriting the risks they want as pricing models to reach to their target market. However, it is evident that a little profit can be made through underwriting alone but insurers use these collections to build an investment pool.

Investment Income

This situation allows insurance companies to invest that money while it is not being used.

- When an insurer collects premiums they put that money into an investment pool.

- They use the premiums collected to fund investments usually in guaranteed or low-risk securities such as real estate, bonds and money market funds.

- When a claim is made, money is then taken from that pool and is put into a cash account to pay the claim once the adjustment of it is completed. Where insurers make their money is from the interest and return on investment earned from those premiums while they are in the investment pool.

One example of how insurance companies make money from real estate is by owning skyscrapers in the biggest cities in America (Hussain, 2015).

The company has their name on the building but they also rent out the offices to various businesses which provide them with a steady stream of rental income (Hussain, 2015).

If premiums and investment income exceed the cost of claims and expenses, the rest can be reserved as profit

If premiums and investment income exceed the cost of claims and expenses, the rest can be reserved as profit. In seeking profits, however, insurers must take certain risks. Poor underwriting can lead to losses if the estimates of future claims and expenses were used to price a policy.

According to Buffett (Creedy, 2011), the issue is less about annual profits than it is about the cost of underwriting and whether you are generating an underwriting profit or loss. Underwriting profit or loss consists of the earned premium remaining after losses have been paid and administrative expenses have been deducted. It does not include any investment income earned on held premiums.

But Buffett says (In Creedy, 2011) that – “The source of our insurance funds is “float” which is money that doesn’t belong to us but that we temporarily hold.

Most of our float arises because –

- Premiums are paid upfront, though, the service we provide – insurance protection – is delivered over a period that usually covers a year.

- Loss events that occur today do not always result in our immediately paying claims.

In such years, they are actually paid for holding other people’s money. For most insurers, however, life has been far more difficult. In aggregate, the property-casualty industry almost invariably operates at an underwriting loss. When that loss is large, float becomes expensive, sometimes devastatingly so.

Theory Behind Premium

The main course of income of insurance companies is premium collections, no matter whether they are invested or not. Thus, the theory behind premium is for the use of loss-sharing. It is called risk pooling.

In general, the size of the premium required by the insurer to assume risk is used to compensate those who incur covered losses.

Loss sharing is accomplished through premiums collected by the insurer from all insured—from those who may not suffer any loss to those who have large losses. In this regard, the losses are shared by all the risk exposures who are part of the pool. This is the essence of pooling.

The law of large numbers is a principle of probability according to which the frequencies of events with the same likelihood of occurrence even out, given enough trials or instances. As the number of experiments increases, the actual ratio of outcomes will converge on the theoretical, or expected ratio of outcomes (Gibilisco, 2012).

The Law of Large Numbers in insurance theory is based on the idea that larger numbers of policies written result in more accurate predictions of incidents resulting in the loss (Gibilisco, 2012).

This prediction also enables companies to estimate how many policies they need to write to cover the expected annual losses. If it were not for the law of large numbers, insurance would not exist. Both the transfer of risk to a third party and the pooling direct to decreased risk in society as a whole and a sense of reduced anxiety.

Potentiality of Avoidance of Paying Claims

There are many incidents where an insurer can refrain from paying claims.

As discussed earlier,

- One possible cause is if the claimant has violated the “utmost good faith”.

- Also, one of the main reasons for declining of claims is the illegitimacy of the claim.

Proximate Cause

Proximate cause is another problematic situation which may lead not to pay the claims. Basically, an insurance policy defines the hazards of insured events that cover is provided for.

For example, a building insurance policy covers different standards such as fire, lightning strikes and earthquakes and the cover for additional risks such as – escape of water, storm or accidental damage can be requested.

All contracts are subject to terms and conditions that will exclude certain causes of loss (Belmont Virtual Academy, 2013).

Therefore, at the time of a claim, it is imperative to decide the reason of the loss in order to control, if that cause is insured or excluded. There may be numerous parts involved in a claim so, it is the “proximate cause” that is taken into consideration. The proximate cause is the leading reason that sets in the act a chain of actions.

For example, if lightning damaged a building and deteriorated a wall, following which the weakened wall was blown down by winds, lightning will be deliberated proximate cause. If lightening has not been covered in the policy, a claim cannot be made.

Indemnity

Indemnity is considered to be the exact compensation required to restore the policyholder to the financial position they enjoyed immediately before a loss occurred (Belmont Virtual Academy, 2013). Indemnity settlements can be reduced where it can be proved that there is under-insurance and therefore, the insurers are only receiving a premium for a proportion of the entire value at risk. If this is the case, any claims payment will be reduced in direct proportion to the under-insurance. Thus, indemnity would lead to the profit margin of the company.

Moral Hazard

Moral hazard is the risk that the behavior of policyholders changes once they have entered into an insurance contract in a way that makes the risk event more likely to happen (Creedy, 2011).

For example, a car owner may drive less carefully once they have insurance that passes the risk of the car being damaged on to an insurer.

Moral hazard can result in more claims than the insurance company expected, based on its underwriting, and could result in premiums increasing for all policyholders if it is not managed effectively. This is why it is important for the terms and conditions of insurance contracts to be tightly worded. This will also lead to loss of profits for the insurance companies.

Adverse Selection

Adverse selection is a situation in which higher risk individuals are more likely to take out insurance. One of the objectives of underwriting is to avoid this by identifying relevant risk factors and setting premiums to correctly reflect the risks (Creedy, 2011).

For example, if smokers and non-smokers are offered life insurance price based on the average life expectancy for both groups at the same, the premium will be a good option for smokers than for non-smokers.

As a result, more smokers than non-smokers are likely to take out the insurance. The insurer will then end up with a higher rate of death and hence higher claims than it anticipated when it was pricing the premium. This will adversely affect reserves or the premiums it charges. However, by taking smoking into account as a fact in the underwriting process, insurers can offer lower life insurance premiums for non-smokers than smokers. Thus, adverse selection should be carefully handled by the insurers as it may adversely affect the ultimate business model of the company.

Reinsurance

Mostly, insurance companies can pay off the payout themselves. But in certain situations, they spread out the risk to reinsurance companies i.e. insurance companies that insure other insurance companies. Many large insurance companies also have reinsurance divisions.

An example of reinsurance is when the payout is too high and risk too great for a single company to handle. An example is when the risk is localized too much to one area instead of being spread out e.g. property insurance in Fiji before a hurricane. If there is one and only one insurance company that sold policies to one million people in Fiji, and a hurricane came by, it could bankrupt the company to pay out all the policies so, the company should spread out the risk by asking other companies to re-insure.

Thus, reinsurance affects the business model of the insurance companies to protect unusual situations.

Conclusions

Insurance plays an important role in the economy, supporting economic activity by helping organizations and individuals to manage their risks. Given the importance of this role, insurers have the potential to affect company’s financial stability.

Insurers’ business models allow the company to focus its activity, making the most effective use of its resources. In response, insurers will continue to develop and revise their business models, bringing both beneficial innovation and a new set insurance of risks.

Most businesses will only be paid when their customers have received a satisfactory product, creating an encouragement to offer a high-quality product and good customer service. But an insurer receives payment in advance. This combined with the comparatively low obstacles to entry to the insurance market and it has led to cases of falsified activities.

There have also been cases of overoptimistic insurers distributing excessively to their shareholders and not holding enough back to cover potential future claims. The majority of insurers will want to manage themselves safely and carefully for reputational reasons and to attract new policyholders.

There are two basic ways that an insurance company can make money. They can earn by underwriting income, investment income, or both. The majority of an insurer’s assets are financial investments, typically government bonds, corporate bonds, listed shares and commercial property. The assets generate investment income and are chosen carefully to reflect the nature and timing of the insurance liabilities that may need to be paid.

Expense management, pricing premiums and robust claims handling will also help to control costs. However, insurers must take certain risks of inflation, devaluation etc. when they seek profits. Thus, the business model of insurance companies is different from other conventional businesses in the market while having much recompense over other businesses in the trading.

How else do you think insurance companies generate profit? Drop a comment below & share the article.

LawSikho has created a telegram group for exchanging legal knowledge, referrals and various opportunities. You can click on this link and join:

https://t.me/joinchat/J_

References –

- Belmont Virtual Academy. (2013). The Six Key Principles. Journal of Insurance (1), 25-75.

- Breckenridge, John, James Farquharson, and Ruth Hendon. “The role of business model analysis in the supervision of insurers.” Bank of England Quarterly Bulletin (2014): Q1.

- Creedy, Alan (2011). How Insurance Companies Make Money: Wisdom From Warren Buffett. URL: http://funeralhomeconsulting.org/best-practices/customer-engagement/preneed/how-insurance-companies-make-money-wisdom-from-warren-buffett/(accessed on 6/12/2016)

- Gibilisco, Stan (2012). Law of large numbers.URL: http://whatis.techtarget.com/definition/law-of-large-numbers, /(accessed on 6/12/2016)

- Hooper, Stephen D. (2009). Unhealthy Profits The Three Ways Insurance Companies Make Money from Health Care. URL: http://www.heginc.com/pdfs/Unhealthy%20Profits%209-2009.pdf. (Accessed on 9/12/2016)

- Hussain, Syed (2015). The Secret to How Insurance Companies Make Their Money. URL: http://insurance.credio.com/stories/3670/how-insurance-companies-make-money. (Accessed on 9/12/2016)

- Michael Lewis (2008). The New Thing: A Silicon Valley Story, Coronet, London.

- Tsanakas, Andreas, and Evangelia Desli. (2003). “Risk measures and theories of choice.” British Actuarial Journal 9.04: 959-991.

- University of Melbourne (2015). How is a fair premium calculated as long as there… URL: https://www.coursehero.com/file/p2f1uca/How-is-a-fair-premium-calculated-As-long-as-there-is-suf%EF%AC%81cient-experience-or/ (accessed on 1/12/2016)

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

A lot of persons don’t have an idea of how insurance companies make money. Some even have the idea that these companies don’t make money at all. This isn’t true. See Why