In this blog post, Rittika Chowdhary, pursuing M.A. in business law from NUJS, Kolkata, talks in detail about forward contracts.

We are living in the 21st century; the so-called virtual world, where barriers with respect to trading and business have now been reduced to a bare minimum. Of course it goes without saying that each country has its own set of rules and guidelines to safeguard its economic resources and interest of the country.

This brings us to the importance of trade and finance and the fact that all individuals, firms and business houses are exposed to various levels of risks on their business exposure. Hence the concept of risk mitigation came into practice.

One can mitigate various forms of risks with different types of methods and even can make a profit by managing the risk.

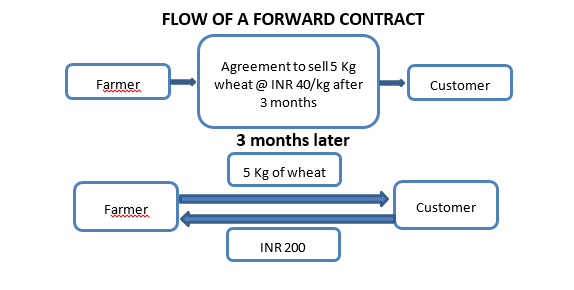

Consider a Punjab farmer who grows wheat and has to sell it at a profit. The simplest and traditional way for him is to harvest the crop in March or April and sell in the spot market then. However in this way the farmer is exposing himself to risk of downward movement in the price of wheat which may occur by the time crop is ready for sale.

In order to avoid risk, one way could be that farmer may sell his crop at an agreed upon rate now with the promise to deliver an asset i.e., crop at predetermined rate in the future. This will ensure the input cost and reasonable amount of profit to the farmer.

The transaction which farmer has entered is called a forward transaction and the contract which covers such transaction is forward contract. A forward contract is an agreement between buyer and seller, obligating the seller to deliver a specified asset of specified quality and quantity at the specified rate and at the specified place and the buyer is obligated to pay the price agreed upon.

The following depicts simple movement of forward transaction:

Flow Of A Forward Contract

- Scenario 1: After 3 months the spot rate goes up to Rs.42, customer will have a gain of Rs.10.

- Scenario 2: After 3 months if the spot rate drops to Rs.38, customer will incur a loss of Rs.10

- Scenario 3: After 3 months if the price is stagnant at Rs.40, neither of them incurs any profit or loss.

The above depicts a typical business transaction with the 3 possibilities; the same is more so evident in the foreign exchange market, owing to the dynamic nature and the number of currencies, and still more number of reasons which determine / influence the exchange rates.

An exchange rate change, in a more technical way is called as “exchange rate fluctuation”. For some businesses, the currency exposure is significant (and direct), while others are indirectly affected by foreign currency fluctuations.

Where there is a problem, we find a solution, and foreign currency fluctuation is one which entails cash losses. The market has therefore been ever evolving with a plethora of options for businesses to minimize (if not eradicate) the losses on account of foreign currency fluctuations.

Here, another point worth mentioning is that for forex, there is no physical market as such; rather these transactions take place “Over the Counter”, where we have bankers in dealing rooms who determine the foreign exchange rate. Now that in itself is a separate topic, which need not be spoken of now. Bankers are in such a position that they are always ready to buy/sell forex. Here comes our chance to reduce the foreign currency losses.

The reason “why” we need something like a forward contract is required was what we discussed above.

What is a Forward Contract

As explained above, it is a contract that obligates the holder to buy or sell an asset at a set price on a specified date in the future. Now that is what any dictionary or a google search will give you.

Let me break it down for you.

To understand what a forward contract is, we need to know what a forward rate is; and in order to know what a forward rate is, we need to know what a spot rate is!

Spot rate is the rate applicable for delivery on 2nd business day, and forward rate is the rate fixed for a forward contract. Such a contract essentially refers to contract to buy or sell a certain amount of foreign currency at a predetermined rate (which is but the forward rate) on a pre-determined date (maturity date).

For example: M/s A & Co. has exported iron ore to USA and the total value of the shipment is $ 100,000 which is due after 3 months. The current rate (spot rate) for exchange is $1 = INR 66.45. M/s A & Co. enters into an agreement with banker to realize the proceeds after 3 months at the rate of 66.67 per dollar. Agreed rate of $1=INR 66.67 shall be the forward rate for the particular transaction, and the entire transaction is a “Forward Contract”. By booking the forward contract, M/s A & Co. have done the following:

- Ensured that despite the spot rate is lesser, they will have a higher INR inflow.

- They will not be bothered about the unfavorable movement in the forex market.

- In the event that they see that the spot rate on the day of maturity is higher, they will still have the liberty to use the spot rate, provided they are able to rollover the current forward rate.

Forward rates are extensively used by exporters and importers to “hedge” their foreign currency payables and receivables.

Note: Both spot rate and forward rates are determined by demand and supply forces, in addition to the manner in which the macro-economic determinants like political conditions, monetary policy, fiscal policies of all concerned countries are being shaped up; the same is discussed in more detail ahead.

If a forward rate (F) is higher / lower than the spot rate (S), the denominator currency is said to be a forward premium / discount. In simple terms, we can say that one can earn profit or incur loss with the forward contract. When the future rate is higher than the spot rate, a transaction which involves the sales or inflow, it will contribute in earning the profit. And if the transaction involves monetary outflow or purchase, the same scenario can make the trader to incur loss.

If we put the above in a formula:

Annualized Forward Premium = {(F-S)/S}*100*12/n

A negative answer would imply a discount.

For example: Say spot rate is $1=62, and 6-months forward rate is 62.8, therefore annualized premium on $ = {(62.8-62)/62}*100*12/6 = 2.58%

Therefore, the USD is at a premium of 2.58% in the forward market with respect to the INR; likewise the INR is at a forward discount in the forward market with respect to the USD.

The difference between the spot rate and forward rate is called as “Swap Point”; if the currency is at a forward premium/discount, we add/deduct the swap points from the spot rate to get the forward rate.

And now the question arises why we have to use forward contract. The very basic reason is to manage the risk and to cover the probable loss that may arise in the course of execution.

What is risk

Risk is nothing but the exposure of the business to probable losses, which may get affected by general economic conditions or specific business scenario, and in turn which may cause monetary damage to the business.

For example: A general deflationary economy may cause slowdown in the growth of business environment and in turn a stake holder shall be affected by possible monetary loss on his investments.

The types of risk which are a business may be exposed have been broadly discussed here:

- When the loss to the exposure is caused by counterparty’s failure to perform obligation is called as credit risk.

- When the loss is caused by adverse changes in the market value of an instrument is known as market risk.

- When the loss is caused by failure of an institution to meet its funding requirements or to execute a transaction at a reasonable price is known as liquidity risk.

- Lastly if the loss is caused by inefficient internal control, human error, management failure or deficiencies in information systems is known as operational risk.

Now that we know what a forward contract is, and we can now have an overview on the features.

Features of a Forward Contract

Forward contracts are non-standardized contracts, which are not traded in an exchange. These are essentially over the counter trades, which are dealt with between the banks and its customers; this feature of forward contracts is called “Over the Counter”.

To explain in simpler words, it means that a forward contract is essentially a tailor made dress, versus another dress which is available off the shelf. This other product in forex parlance is called a future contract. Futures are standardized forward contracts which are traded on the exchange with Marked to Market features and Stringent Margin Requirements.

Forward Contracts are highly exposed to the counterparty risks. As Forward Contracts do not have any clearing house or other institutional agents in the contract, exposure to counterparty risk is substantial. Moreover forward contracts are not Marked to Market on daily basis; instead they are agreed to be settled at a future date at an agreed price; this leads to the high volume of risk.

Future contracts because of its standardization make it possible to be traded in the secondary market. However, the basic characteristic of the forward viz. customization prevents it from getting traded in the open market.

A host of new words were used in the above paragraphs, which need a clarification note:

- Marked to Market means that the product price changes at fixed intervals to reflect the impact of demand and supply of the same in the price of the product at the end of each day. Classic example of marked to market feature, which is relatable to one and all is the stock market prices.

- Going long/short in futures implies contracting to buy/sell.

- Margin requirement is essentially put in place for futures contract so that the risk of client defaulting in any contract is bare minimum. Going long/short in futures implies contracting to buy/sell. If there is an adverse price movement there is a possibility of default on the part of the trader. To mitigate the same, the clearing house requires every future trader to make a security deposit, which is called initial margin; and this margin requirement is strictly monitored in the case of a future contract.

- Arbitrage is the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset. It is essentially a profit making scheme for profit hungry investors who look for these differences in prices of same product in different markets. Goes without saying that any arbitrage opportunity is vigorously exploited by these investors, and therefore the same does not persist for a longer duration.

How is a Forward Rate Calculated

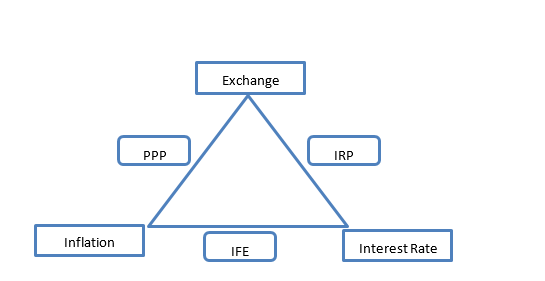

The answer to the above is fairly simple. Market forces, that is, demand and supply, determine the rates at which a particular currency which you want in the near future is determined. In a free floating exchange rate mechanism, exchange rates are determined by the demand and supply forces. These supply and demand in turn are influenced by a number of macroeconomic factors – interest rates, inflation, growth rate of GDP, monetary and fiscal policies, balance of payment situation, etc. Out of these many factors, inflation and interest rates are considered to be the most important.

The relation between the above three is christened in the market parlance as follows:

- Exchange Rate and Interest Rate – Interest Rate Parity (IRP)

- Exchange Rate and Inflation – Purchasing Power Parity (PPP)

- Interest Rate and Inflation – International Fischer Effect (IFE)

- IRP: To explain in simple terms, effect of interest rate change on foreign exchange, when other factors remain constant. Therefore, if in one country the interest rate is lower than the other, then the 1st country’s currency shall be at a forward premium. IRP in fact goes one step further, and it quantifies the premium vide a formula.

To explain the above with numbers, say if the $ interest rate is 4% and INR interest rate is 10%, then $ should be at a premium against INR approximately by 10-4=6%, and exactly by 6/1.04=5.77%; the corollary of the above shall be that INR should be at a discount against USD by approximately 6%, and exactly by 6/1.1=5.45%.

- PPP: Purchasing Power Parity theory expresses the relationship between the exchange rates and inflation, other factors remaining constant. Inflation causes a decline in the purchasing power of money. Thus if 1 country has a higher inflation than another, its currency should depreciate.

- IFE: This is a parity relationship between interest rates and inflation, and is derived from IRP and PPP. As per IFE, the real interest effect in all countries should be the same.

Among all above mentioned theories Interest Rate Parity theory considered to be more superior, as it considers the running interest rate in the economy. And in many cases, the forward rate is highly dependent on the interest rate and the expected income or reducing loss intention of the investor.

So, now again we are back to the main question: how will the forward rates be calculated and what provides the strong base for calculating the forward rate?

First let’s take an example of non-currency forward transaction. Suppose that-

Mr. A wants to buy a house a year from now. At the same time, suppose that Mr. B currently owns a INR 100,000 house that he wishes to sell a year from now. Both parties could enter into a forward contract with each other.

Suppose that they both agree on the sale price in one year’s time of INR 104,000 (more below on why the sale price should be this amount). Mr. B and Mr. A have entered into a forward contract. Mr. A, because he is buying the underlying, is said to have entered a long forward contract. Conversely, Mr. B will have the short forward contract.

At the end of one year, suppose that the current market valuation of Mr. B’s house is INR 110,000. Then, because Mr. B is obliged to sell to Mr. A for only INR 104,000, Mr. A will make a profit of INR 6,000. To see why this is so, one need only to recognize that Mr. A can buy from Mr. B for INR 104,000 and immediately sell to the market for INR 110,000. Mr. A has made the difference in profit. In contrast, Mr. B has made a potential loss of INR 6,000, and an actual profit of INR 4,000.

The similar situation works among currency forwards, in which one party opens a forward contract to buy or sell a currency (e.g. a contract to buy Canadian dollars) to expire/settle at a future date, as they do not wish to be exposed to exchange rate/currency risk over a period of time. As the exchange rate between U.S. dollars and Canadian dollars fluctuates between the trade date and the earlier of the date at which the contract is closed or the expiration date, one party gains and the counterparty loses as one currency strengthens against the other.

Sometimes, the buy forward is opened because the investor will actually need Canadian dollars at a future date such as to pay a debt owed that is denominated in Canadian dollars. Other times, the party opening a forward does so, not because they need Canadian dollars nor because they are hedging currency risk, but because they are speculating on the currency, expecting the exchange rate to move favorably to generate a gain on closing the contract.

How the Forward Price Should be Agreed Upon

Continuing on the example above, suppose now that the initial price of B’s house is 100,000 and that A enters into a forward contract to buy the house one year from today. But since B knows that he can immediately sell for 100,000 and place the proceeds in the bank, he wants to be compensated for the delayed sale. Suppose that the risk free rate of return R (the bank rate) for one year is 4%, then the money in the bank would grow to 104,000, risk free. So B would want at least 104,000 one year from now for the contract to be worthwhile for him – the opportunity cost will be covered.

So, the basic factors which influences on determining forward rates are as follows:

- Spot rate of the item

- Risk free interest rate

- Opportunity cost

- Market rate

- Storage cost (for commodity forward transaction)

All the points described above place the bridge for determining parity between spot and forward rates.

The idea of maintaining parity between the spot and forward rates is to eliminate the chances of arbitrage opportunities; in Indian market scenario, it is essentially not allowed as well. A person without having a valid underlying cannot enter into a forward contract.

So, what happens when you have a forward contract, but the underlying based on which you had entered into the contract is delayed for some reason? The answer to the same is ‘Rollover Contract’.

Extension, Cancellation and Early Delivery of Forward Contracts

In India, forward contracts are allowed only for hedging purpose. It may so happen that the underlying exposure (payable/receivable) which initiated the forward contract gets cancelled, extended or preponed. Hence the forward contract has to be cancelled, extended or delivered early.

Herein also comes the idea of a rollover contract, wherein the expected forex inflow/outflow is delayed for business reasons, and the underlying is still in place. In such cases, the forward contracts are “Rolled Over” to a further future maturity date.

Forward contracts are gaining prominence in the economy over the period. Judicial forward cover is helping the business houses to safeguard their exposures both domestic as well as of foreign exposures. In fact, common man has also started using forward these days. Forward contracts are now getting prominence as a mode of investment as well.

What are your views on this? Feel free to comment below & share the article.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications

Great Blog!

Thanks for sharing this blog!

[…] Gambar 6.2 Contoh Simulasi Kontrak Forward (blog.ipleaders.in) […]