This article is written by Keshav Bhardwaj, pursuing Diploma in Companies Act, Corporate Governance and SEBI Regulations from LawSikho.com. Here he discusses “LODR Regulations in relation to Corporate Governance”.

Introduction

The Stakeholders of the company deals with Corporate Governance matters in the daily phase of life. But, they face problems due to non-compliance with the requirements. The Listing Obligation and Disclosure Requirements 2018 come to existence on 5th October 2017. After this, the requirements become more ever strict made By SEBI. By this, we can analyze that the Requirements are pretty essential for proper corporate governance, It’s suggested by the Kotak Committee to make proper control and functioning Regulations for Company.

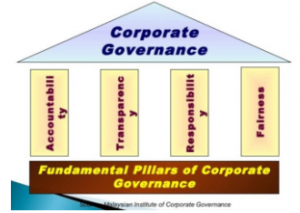

These 4 are the essential pillars of Corporate Governance which are necessary:-

- Accountability:- It means to accept all the liabilities that come from default made by any person himself, Not making any kind of excuse to avoid liability.

- Transparency:- It intends to hide nothing from another person and to disclose everything whatever necessary to prevent fraud of any kind.

- Responsibility:- It implies that Every person has to work as per the task is given to him and no to neglect any kind of duty given and Everybody being responsible is essential.

- Fairness:- It’s referred to as Everybody must be treated equally while distributing share and while providing any information, There must not be any kind of disparity in between.

These are the principles which are being taken essentially in Corporate Governance Activity, but these are not enough to complete the Governance, there is also a need for Listing Obligation and Disclosure Requirements 2018 being taken into consideration

But, the question which comes to arise is

Why SEBI Listing Obligation and Disclosure Requirements 2018 important for corporate governance?

To fulfill these aims the regulation comes into play:-

- Developing the position, no. of members and their working

- Assuring independence in the spirit of Independent Directors and their effective cooperation in the functioning of the company

- Improving protection and acknowledgment pertaining to Related Party Transactions

- Improving clarity in accounting and auditing exercises by the listed companies

- Directing problems faced by investors on polling and support in general meetings

- Efficient monitor by group entities

- Disclosure and transparency-related problems, if any.

The regulation is very important for the proper functioning of corporate governance

Statistics show How good Corporate Governance has an impact on company growth

By this, we come to know How Important is these regulations, So, the LODR Regulation 2018 being mandatory for every company for making safeguard environment of the Stakeholders.

What are the requirements of Listing Obligation Disclosure Requirements in relation to Corporate Governance?

There are ten basic requirements for proper corporate governance as per the regulations of LODR. For the explanatory document, you can visit this. These are given below:-

-

Composition and Role of the Board of Directors

The board of directors is being responsible for the whole company and the stakeholders related to the company all are under the head of the director

Minimum number of Directors

The minimum number of directors which was given 3 under the Company Act, 2013 is now 6 after the amendment of Sebi, 2018. It will come into effect from 1 April 2019 for top 1,000 listed entities and from 1 April 2020 for top 2,000 listed entities.

Gender diversity on the Board

At least one woman director to be required as a board of director. For top 500 listed entities by 1 April 2019 and for the top 1000 listed entities by 1 April 2020.

Disclosure of expertise/Skills of Directors

It also requires disclosure of those skills that it’s board members actually possess, without disclosing the names of the directors. This is to be made effective from the financial year ending 31 March 2019

Skills of each and every member of the board along with their names required from the financial year ending 31 March 2020.

-

Institution of Independent Directors

Definition of Independence Director

After amendments, the person excluding “promoter group” of a listed company to exclude the “board inter-locks” possibilities. The Non-independent directors even excluded from this definition.

Companies will need to comply with the amended definition of Independent Directors with effect from 1 October 2018.

Eligibility Criteria

This changed the criteria for evaluation of IDs by the board necessitating an evaluation If

- Working of the directors.

- Independence criteria as in the SEBI (LODR) Regulations and their independence from the management.

Alternate Directors for Independent Directors

The Amendments prohibit an alternative director to be designated or resume as an independent director of a listed entity by 1 October 2018.

-

Board Committees

There are many committees being established for the proper functioning of the company in various sectors by various groups like audit, remuneration, and risk management committee.

Audit Committee

It has to regularly keep an eye on the spending of loan and advances by the company from investor exceeding INR 100 CR or 10% of the asset size of a subsidiary by April 1, 2019.

Nomination and Remuneration Committee

Senior Management defined as All the member of management one level lower to the Chief Executive and Chief Financial Officer also Company Secretary.

Recommendation of all payment made being transferred to Senior Management.

Role of Risk Management Committee

It is now extended to 500 listed entities in the market. cover cybersecurity, given the increase in the use of cyber and digital technology. As the role increase the protection from cyber-attacks also increase.

-

Enhanced Monitoring of Group Entities

With the increase in the entities, globalization comes to happen which further leads to some technicalities that’s why monitoring comes into play

“Definition of “Material Subsidiary”

The Amendments widen the ambit of a material subsidiary to mean a subsidiary if income exceeds 10% (from the current 20%) of net worth, respectively, of the listed entity and its subsidiaries in the immediately preceding accounting year. That’s why independent director appoint in the listed entity for an unlisted material subsidiary, whether incorporated in India or not.

The company with a large number of subsidiaries need to have large numbers of monitoring mechanisms by April 1, 2019

-

Promoters/Controlling shareholders and RPTs

Most of the Indian Companies are dependent on the Promoters as their controller that’s why this amendment takes place to make changes in the Related Party Transactions.

Definition of “Related Party”

Any person or entity which belongs to the promoters group come under the Related Party, as per the observation certain promoter entity are not a related party.

Amendment of Disclosure

The listed company or promoter which holds 10% or more share need to disclose it by half-year ending 31 March 2019. Also, include in accounting standards of the annual year.

-

Disclosures and Transparency

The company should disclose with time and accuracy to the stakeholders, this is for building trust with stakeholders.

Submission of Annual Reports

Now it’s required to submit within the 21 working days, approved and adopted in AGM. It has to submit a report to AGM if any change, then inform within 48 hours.

Disclosures of key changes in Financial Indicators

It includes Debtors turnover 2. Inventory turnover 3. Interest coverage ratio 4. Current ratio 5. Debt equity ratio 6. Operating profit margin (%) 7. Net profit margin (%)

For significant changes of 25% or more.

-

Accounting and Audit-Related Issues

The accounts and auditing being the most essential parts of the company to show the actual position of the company, which influence stakeholders the most

Click Above

Auditor’s Qualifications

Amendment makes something mandatory which are not quantifiable:-

- Management makes an estimate, which auditor has to analyze and report.

- Notwithstanding the above, if Management does not provide going on or sub- juice concern for which the auditor make the report on the same.

Audit/limited review of quarterly consolidated financial results

The Amendments introduce a requirement for the listed entity to ensure quarterly consolidated monetary outcomes, that at least 80% of the total consolidated fund out of profit must be audited, in case of tamed limited review.

-

Investor participation in meetings of listed entities

More investor participation involves more they are being encouraged to enrich share in that listed entity

Timeline for annual general meetings of listed entities

Now it reduces the duration of holding of AGM to 5 months from the end of the financial year. This requirement is applicable to top 100 listed entities by market capitalization, determined as on 31 March of every financial year. This also reduces holding of AGM for Global Concern and to avoid bunching of AGMs (especially in August/ September), which further leads to fewer shareholders participation. Currently, the Companies Act requires listed entities in India to carry AGM within six months from the end of the monetary year. There are no specific provisions in SEBI (LODR) Regulations on this.

Also, webcast makes it more convenient to attend meetings in easy access anywhere.

-

Recommendations referred to other agencies

The group given below have necessary to take recommendation Includes

Group Audits, Internal Financial Controls (IFCs), Audit quality Indicators, Strengthening the role of review ICAI, Strengthening the independent functioning of the quality review board (QRB)

These all need to take advice and recommendation of the Kotak committee for better functioning and have a positive outcome.

-

Quorum and Separation of Roles

The quorum for board meetings

According to the Companies Act, A quorum of two board of director or one-third of the total. But there isn’t fixed quorum. Now it’s one-third of total directors or three directors, whichever is higher, at least one independent director. It takes place by Audio-Visual Method. The above amendment for top 1,000 listed entities shall come into effect from 1 April 2019 and for top 2,000 listed entities shall come into effect from 1 April 2020.

Separation of the roles of non-executive

Chairperson and managing director / CEO it also require the chairperson of the board as a non-executive director and not be related to the managing director or the chief executive officer as per Companies Act, 2013. The separation leads to a better and proper governance structure by enabling more effective supervision of the management. This amendment shall come into effect from 1 April 2020 for top 500 listed entities. But it’s not applicable to that listed entity in which there is promoter not identified.

By this, we can ensure that every company needs to take into consideration the requirements as per their qualifications to ensure better corporate governance as per Kotak committee. These include the recent amendment impact on requirements.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications