")

This article is written by Shruti Nair, pursuing Diploma in Advanced Contract Drafting, Negotiation, and Dispute Resolution from LawSikho.

Table of Contents

Introduction

Everyone knows what an insurance policy is. We have all seen an advertisement on television that shows two friends talking about how uncertain life is and one of them would suggest getting an insurance policy would be a wise idea. Have you ever wondered what contract is used in an insurance policy? I bet you haven’t! An insurance policy is a common example of an aleatory contract. The intention of this article is to un-pretzel your thoughts and enhance your understanding of aleatory contracts.

What is an aleatory contract?

Definition: “An agreement concerned with an uncertain event that provides for an unequal transfer of value between the parties.” An agreement between two parties in which the performance of the obligation of both the parties depends upon a fortuitous event. A fortuitous event is an event that is unforeseen or unpredictable. These fortuitous events are those that are beyond the control of either party. The fortuitous event could be an accident, natural disaster or death.

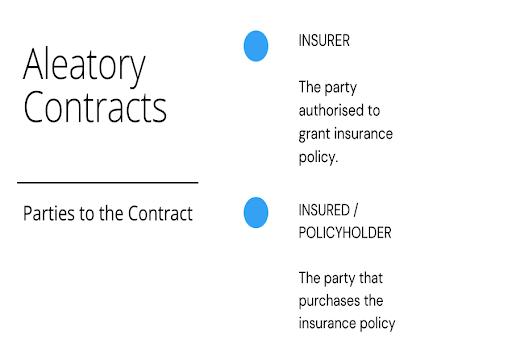

In other words, an aleatory contract is a contract between two parties, the insurer and the policyholder, in which the insurer does not have to perform the obligation of the contract unless an external triggering event occurs that is beyond the control of either party.

The person who insures is the insurer, i.e. the insurance company and the person who purchases the insurance is the insured. The insured is also known as a policyholder.

For example, A bets to B that if it rains tomorrow, he will pay B a sum of Rupees 10,000/- and if it does not rain, B has to pay Rupees 15,000/- to A. In this agreement, the parties do not have to perform the obligation unless an external triggering event occurs that is beyond the control of either party.

Understanding aleatory contracts

The term aleatory contract is developed in the later Medieval Roman law, where the lawmakers deemed it necessary to cover all contracts whose fulfilment depended on chance or on the occurrence of an external event. Depending upon the happening of the event by chance, or non-happening of the same, would determine if the contract would be used to the full benefit of the purchaser or policyholder. As the odds of the happening of the uncertain event are low and as the companies only have to pay if the event occurs, the companies are able to keep the money coming from multiple purchases of the policy. Other than an insurance policy, gambling, betting, and wagering use aleatory contract.

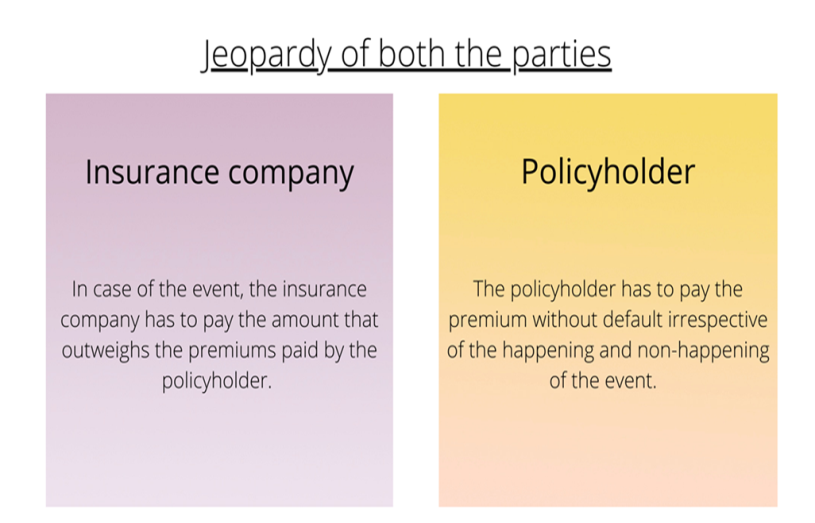

In aleatory contracts, both the parties accept jeopardy:

1. The insurance policyholder pays the premium for the assistance they might not get. So if you don’t ever have an accident, you would still pay for insurance in the event that the accident should happen. The contract is only valid as long as you are paying the premium. If you stop paying your premium, the insurance company will not be liable to cover the loss even though you have made payments in the past.

For example, an insurance company agreed to cover any loss that might happen to the protected property of the policyholder if the loss has occurred due to a natural disaster. For this purpose, the policyholder would pay the premium for the duration as agreed upon. The insurance company will not be liable to cover the loss that occurred on the said protected property if it was due to any other reasons other than a natural disaster.

2. The insurer’s hazard is that it has to cover you by paying an amount that far outweighs the premium in the event of a change occurring.

For example, say a person purchases a life insurance policy from the insurance company for Rupees 1,00,00,000/- and has to pay Rupees 5000/- towards the policy as a premium to the insurance company. However, tragically, the policyholder dies within a year after making payments for only one year. In this scenario, the life insurance company would have only received Rupees 60,000/- but the company has to pay Rupees 1, 00, 00,000/- to the beneficiary who claimed the amount after the death of the policyholder as agreed upon in the aleatory contract.

As death is an unpredictable event, the beneficiary may not receive anything if the policyholder lives until the date of maturity.

Characteristics of aleatory contract

- An aleatory contract is a contract where the exchange is uneven.

- The contract takes effect only after the occurrence of an uncertain event.

- The uncertain event should be beyond the control of either party.

Insurance policy as an aleatory contract

An insurance policy is an unequal contract. It is not a ‘value for value’ contract. It is basically an invisible promise that a company has to pay when the loss occurs. Insurance policies are considered aleatory contracts because the policy does not assist the policyholder unless the uncertain event occurs. Only after the fortuitous event occurs will the insurer grant the policyholder the agreed amount or services specified in the aleatory contract.

Who takes an aleatory contract?

Death is unpredictable and if you are the only source of income in your family, in the event of your death, your family will have no financial support. This contract is taken by an individual who needs to protect his or her family in the event of his or her untimely death.

Contents of aleatory contract

The contents of the aleatory contract are as follows;

- Full name of both the parties i.e. the insurer and the insured.

- The registration details of the insurer and office address.

- Complete and thorough communication details of the insured.

- Policy details including the type of policy, benefit amount, premium amount, term of the policy, etc.

- The date issued of the policy.

- Unique policy number of the policy.

- Risk class that mentions if the insured is a smoker or non-smoker.

- Additional riders are additional clauses to the contract for which an extra premium needs to be paid.

- Details of the beneficiary(s).

- A contestability period is a period after two years from the date of issuance of the policy where the insurer confirms the policy holder’s personal details and claims are contested or denied.

- Exclusions are certain situations where the claim will not be entertained. For instance, suicide.

Points to consider for drafting an aleatory contract

- Determine the parties to the contract and their relationship.

- Details of the insurance company including the year of formation, permissions for issuing the policies, complete official address and communication details.

- Details of the insured including age, beneficiary details, communication details, type of policy.

- Benefit amount and term.

- Additional riders and risk class.

Remedies in case of violation of terms of the agreement

For a policyholder to get the benefit of the policy insured to him, he must adhere to timely payments of the premium without defaults. The policyholder must read the terms and conditions of the policy as there is a provision of exclusion that captures details of what not to do to enjoy the complete benefit of the policy. If the policyholder defaults payment or does an act given under the exclusion clause or goes against the terms and conditions, the insurer is not liable to cover for the loss incurred to the policyholder.

On the other hand, if the policyholder has made a timely payment without any default and has complied with the terms of the agreement but the insurance company fails or refuses to cover the beneficiaries of the policyholder, the insurer has violated the terms of the policy. The insurer is liable to pay the claim and compensate the beneficiaries as decided by the court. In such an event, the beneficiary may also claim the legal cost incurred, from the insurer.

Annuity and aleatory contract

Definition: The term annuity means “a form of insurance or investment entitling the investor to a series of annual sums”.

An annuity contract is a contract between an insurance company and the annuitant in which the annuitant makes a lump-sum payment or series of payments and, in return, receives regular payments, either immediately or at some point in the future.

An annuitant is an individual who is entitled to collect the regular payments of annuity investment.

Understanding annuity contracts

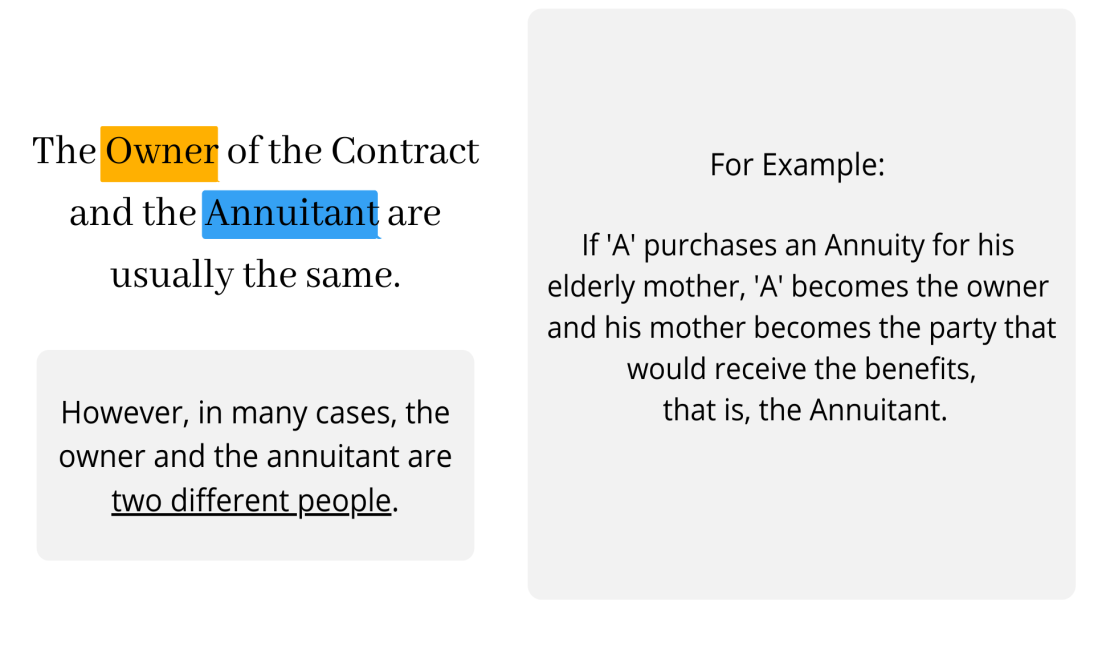

An annuity contract is a contractual obligation between the insurance company, the owner of the annuity, the annuitant, and the beneficiary.

- The owner is the person who purchases an annuity.

- An annuitant is a person whose life expectancy is used for determining the amount and timing when benefits payments will commence and cease. Usually, the owner and annuitant will be the same person.

- The beneficiary is the person who will receive any benefit in the event of the death of the annuitant.

The aim of an annuity contract is to deliver stable income ideally during retirement. The annuity contract can be tailored as per the annuitant’s needs. The annuitant gets the option of choosing between a lump-sum payment and a series of payments to the insurer. The annuitant decides when he wants to annuitize his contributions, that is, start receiving payments. Essentially, an annuity contract guarantees risk-free retirement income.

An annuity that commences payment immediately is referred to as an immediate annuity, while one that starts at a pre-established date in the future is called a deferred annuity.

Keeping in mind the following points when going for an annuity

- Annuities are complex, and so these contracts may not be very friendly to many investors due to unfamiliar concepts.

- The surrender period is the period during which an individual who owns an annuity is able to withdraw all their money without paying a penalty.

- Multiple-tier annuity contracts include Tier 1 that permits withdrawals over a lifetime. Tier 2 if the annuity owner takes out their entire balance at once, then the annuity seller may reduce the value of benefits by 10% or 20% and what penalties may be triggered if the owner wants to liquidate their annuity.

- High teaser rates to motivate buyers followed by far lower rates for the life of the annuity contract. The way around this matter is for the annuity seller to completely disclose the rate they will pay for the life of the annuity.

- Try to buy an annuity that permits a joint annuitant to be named, which gives owners and beneficiaries more flexibility with withdrawal timing and tax planning.

- Annuity contracts have different withdrawal amount policies. One has to make sure they are flexible. For example, most have a 10% withdrawal amount, but if you want to withdraw 20% after two years, make sure it is the one known as cumulative withdrawals, that is, an alternative without a penalty.

In other words, when a person is looking for a possibility to enhance their income in the event of retirement and/or has exhausted all savings, annuities work as a solid plan to receive a stable income. It is essential that one understands the complex patterns of the contract before investing in it. Although with due care and planning, an annuity may be the most fitting choice.

Why opt for annuities?

People typically purchase annuities to manage their income in retirement. Annuities provide for the following:

- Recurring payments for a specific amount of time: This can be for the rest of your life or the life of your spouse or another person.

- Benefits: The individual you have named as beneficiary would receive payments if you die before acquiring the said payments.

- Tax-deferred growth: Until you withdraw the money, you have to pay no taxes on the income and investment gains from the annuity until you withdraw the money.

Advantages and disadvantages of annuities

For some people, annuities are a way to ensure their retirement and to receive regular payments once they no longer obtain a salary. The two phases to annuities are;

- During the accumulation phase, you make payments that may be split among various investment options. In addition, variable annuities often allow you to put some of your money in an account that pays a fixed rate of interest.

- During the pay-out phase, you get your payments back, along with any investment income and gains. You may take the pay-out in one lump-sum payment, or you may choose to receive a regular stream of payments, generally monthly.

Expenditure incurred

Among the number of charges incurred, other than surrender charges are as follows;

- Mortality and expense risk charge.

- Administrative fees.

- Underlying fund expenses.

- Fees and charges for other features.

- Penalties.

(Be sure you understand all charges before you invest.)

Some of the types of annuities

- Fixed period annuities – Pay a fixed amount to the annuitant at periodic intervals for a specific duration of time.

- Variable annuities – Payments made to the annuitant varying in amount for a definite length of time or for life. The amounts paid may depend on profits earned by the pension or annuity funds or by cost-of-living indexes.

- Single life annuities – Pay a fixed amount at periodic intervals during an annuitant’s life, ending on his or her death.

- Joint and survivor annuities – A fixed amount paid to the first annuitant at regular intervals for his or her life. After the first annuitant’s death, the second annuitant would receive a fixed amount at regular intervals. The amount paid for the life of the second annuitant, may or may not be the same as was paid to the first annuitant.

- Qualified employee annuities – When an employer purchases a retirement annuity for an employee under a plan that meets certain Internal Revenue Code requirements.

- Tax-sheltered annuities – A special annuity plan or contract purchased for an employee of a public school or tax-exempt organization.

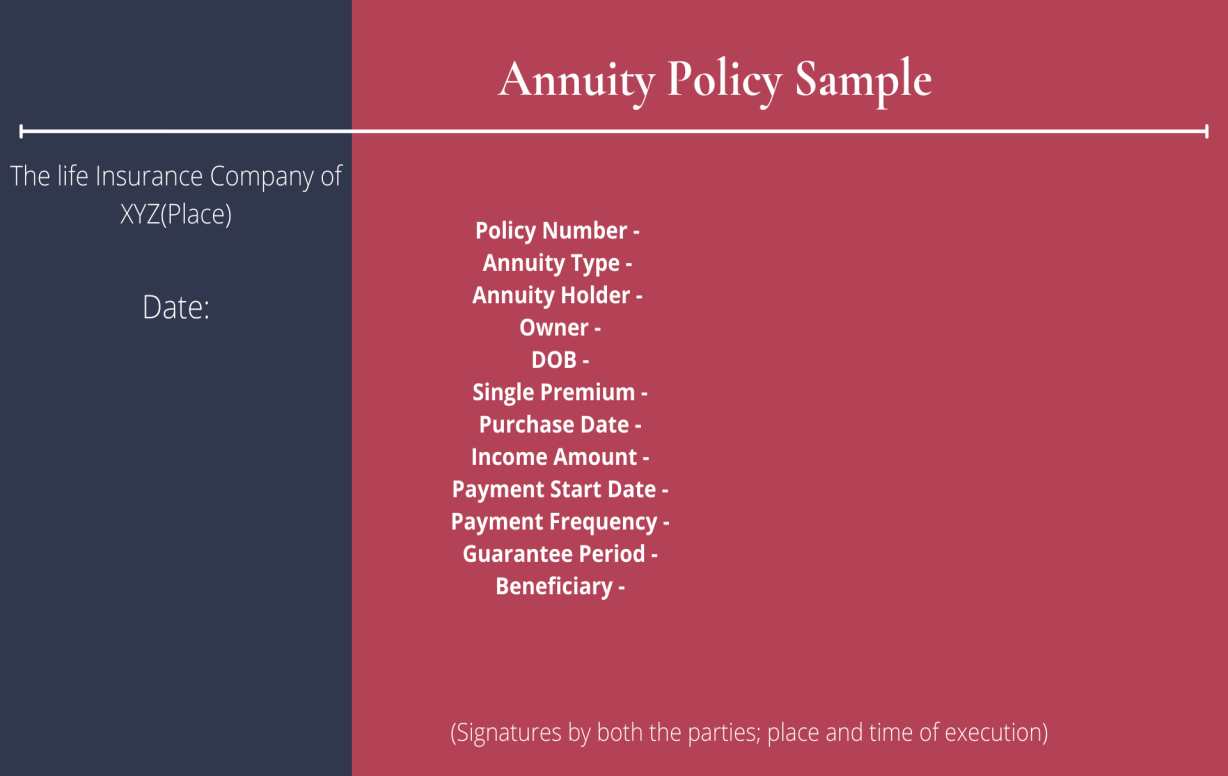

Contents of an annuity contract

-

Policy details

The policy details of the annuity contract include the annuity policy number, purchase date, policyholder, annuitant, joint annuitant, date of birth, payment start date, frequency, beneficiary, premium amount, date received and source.

-

Annuity details

The annuity details include the annuity type, source type, payment start date, annuity income payments, guaranteed periods, last guaranteed payment date, taxable amount per payment frequency, provisions that apply to this annuity contract.

-

Understanding your policy

A list of definitions describing the terms used in the annuity contract.

Commutative and aleatory contract

Definition: The commutative contract is one in which the contracting parties give and receive an equivalent or reciprocal value.

In other words, the contracting parties give and take something of equal value.

A common example is the contract of sale where the seller sells a thing and receives consideration equivalent to the thing he sold and the buyer pays the amount equivalent to the thing he wishes to purchase.

In a nutshell, an aleatory contract is one in which one party does not have to pay the other unless a specific event takes place. In a commutative contract, both the parties to the contract give and receive something similar or equivalent. In an aleatory contract, the premiums paid by the policyholder and the benefits by the insurer may not be the same. However, in a commutative contract, the values exchanged are similar or equivalent.

Conclusion

An aleatory contract is a contract where the exchange is uneven unlike a commutative contract, where the exchange is similar or equivalent. Insurance policy is a fitting example of an aleatory contract. The obligations of an aleatory contract are set off when a fortuitous event that is beyond the control of either party is triggered. In an aleatory contract, both the parties accept uncertainty, that is, the policyholder pays a premium to the insurer in the event an accident should occur while the insurer has to cover the policyholder by paying an amount that far outweighs the premium. An annuity contract, on the other hand, is known as a guaranteed risk-free retirement income. The idea behind an annuity contract is that an annuitant pays either a lump sum or a series of payments which after a point of time, ideally in retirement, receives regular payment.

Like the advertisement comes with a warning, read the schemes and related documents carefully, understand the terms and conditions before purchasing a policy.

References

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skills.

LawSikho has created a telegram group for exchanging legal knowledge, referrals, and various opportunities. You can click on this link and join:

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications