This article is written by Pearl Narang, pursuing a Diploma in Advanced Contract Drafting, Negotiation and Dispute Resolution, and Amresh Tiwari, pursuing a Diploma in M&A, Institutional Finance and Investment Laws (PE and VC transactions) from Lawsikho. Here she discusses “All You Need to Know about Chit Funds”.

Table of Contents

Introduction

When a person has money, all he wants is a good investment scheme. But, how does he identify a good investment scheme? A scheme which generates high returns and also allows the investor to withdraw money whenever he needs, would qualify as a good investment scheme. Chit fund is one such scheme that allows even people of lower income bracket to invest and earn interest on their deposits.

Understanding Chit Funds

Section 2(B) of Chit fund Act 1982 defines it as a rotating savings and credit association system, a popular practice in India. Chit fund schemes may be organized by financial institutions and unorganized money market industries or informally among friends, relatives, or neighbors. In some variations of chit funds, the savings are for a specific purpose. It’s mostly popular in the areas where people have limited access to banking facilities therefore they prefer to invest their money in a Chit fund.

In a chit fund, a specific number of investors invest their money with a promise that their investment will be multiplied within a short span of time with surety and guaranteed return. Under this type of saving arrangement a specific number of subscribers contribute payments in installment over a defined period of time.

A chit fund works in such a manner which comprises a group of members, called subscribers. an organizer, a company or a trusted relative or neighbor, brings the group together and administers the activities of the group. For their efforts, the organizer is either compensated each month or at withdrawal time. The fee may be omitted in informal situations.

Let say as an example; consider an auction-type chit fund where Rs. 100 every month is contributed by 50 subscribers. The monthly pool is Rs 5,000 and this is auctioned on a monthly basis. The winning bid, say Rs. 1000, would be the discount and be distributed among the subscribers. The winning bidder would then receive Rs 4,000 (Rs 5,000 – 1,000) while the rest of subscribers would receive Rs 20 (1000/50). The winners will not participate in the auction again and will be liable to contribute to the monthly subscription as the process is repeated for the duration of the scheme. The company authorized to manage the chit fund would retain a commission from the prize amount every month. Collectively, the subscribers to a chit fund are referred to as a chit group and a chit fund company may run many such groups.

Other Names for Chit Funds

Chit funds are known by a number of names.

- Internationally, chit funds are known as Rotating Savings and Credit Associations (ROSCA), this is because they provide a facility of saving and borrowing simultaneously.

- In India, they are called,

- chit, or

- chitty, or

- Kuree.

After the amendment of the Chit Funds Act in 2019, the following names have also been added. These are,

- Fraternity Fund, or

- Rotating Savings, or

- Credit Institutions.

Features of Chit Funds

Chit funds have the following features:

- They have a predetermined value and duration.

- They work like microfinance institutions.

- They combine both, credits and savings in a single scheme.

- They cater to the financial needs of low income households.

- They allow the deposits made by the contributors to be turned into a lump sum. This is done by three mechanisms.

- Safe Deposits: A person can deposit the money in the present and enjoy the lump sum in future.

- Loans: A person can take a loan in the preset and continue to make payments in the future.

- Insurance: Allows the depositor to enjoy the lump sum in case of an emergency.

6. They offer loan at a lower interest rate than moneylenders.

What are Chit Funds Used For?

Chit funds are used for the following reasons:

- They address consumption needs.

- They help in case of an emergency such as a daughter’s marriage.

- They help a person to pay for education of their children, purchase property etc.

- They help pay for costlier loans from moneylenders.

- They address capital needs of small businesses.

How does a Chit Fund Work

Let’s understand how a chit fund works through an illustration.

Illustration: Rohan and Abhishek were friends.

Rohan was well educated and had a good job. Additionally, Rohan was also planning to start a business to sell fresh food to corporates online. For his business venture, Rohan needed capital. But banks and financial institutions charged too high rate of interest on a loan and required Rohan to fulfil a number of formalities. Rohan needed a capital of 8,00,000 rupees immediately. He couldn’t afford to wait to start his venture. He was stuck between Private money lenders and banks. These options require asset as collateral. They also accrue hefty amount interest.

Abhishek had a PhD. and was in a well paying job. He had no intention to start a venture but he was looking to save his earnings in a medium, where he can earn good interest and can withdraw money whenever he wants to. Abhishek was also finding it difficult to get an investment scheme that would allow him to deposit cash and withdraw money without any losses. No options were apt. Bank Accounts and Fixed Deposits had their own limitations. And investing in mutual funds and shares involved a lot of risks.

Chit Funds are a unique combination of saving cum loan investment. Investors can invest money in them and withdraw it anytime the need arises. Moreover, there is no interest charged on borrowings. The person can borrow anytime and for any purpose. A group of people pool in a fixed sum of money every month. Every month through competitive bidding, a contributor gets to win the pool. A contributor can win the pool only once.

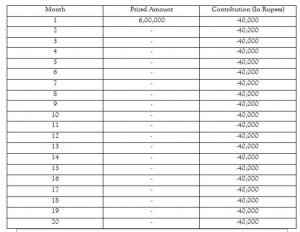

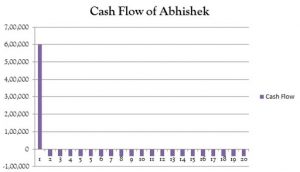

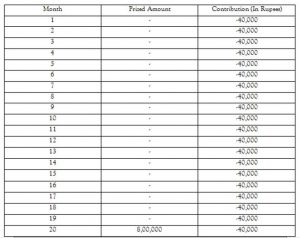

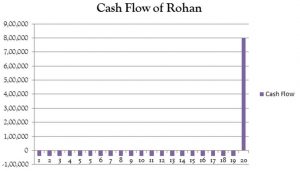

Rohan and Abhsehk decided to invest in a government funded chit funds scheme. The scheme included 20 members who contributed 40,000 each month for 20 months. The jackpot being 8 lakhs every month which would go to one member via competitive bidding till all members get to take the pot home once. Rohan and Abhsihek contributed 40,000 each in the first month. Since Rohan needed 8,00,000 for his capital he decided to participate in the bidding process in the first month itself. Rohan decided to forgo the maximum limit permitted which was 2,00,000 rupees or 25% of the total amount. Thereby taking back 6,00,000 rupees. The remaining 2,00,000 rupees was with the foreman. The foreman kept his fixed monthly commission that is 40,000 or 5% of the chit fund value, and distributed the remaining 1.6 lakh among all the 20 members.

Rohan opened his restaurant he couldn’t bid for the remaining months but he continue to deposit 40,000 every month. Abhishek, on the other hand, waited entire 40 months and got to take back the entire pot minus the foreman’s commision of 40,000 rupees. This way Abhishek earned extra amount since he didn’t have to forgo any amount and also earned the monthly dividends from the amount forgone by other bidders.

Cash Flow For Abhishek

Cash Flow For Rohan

Thus, chits funds helps people in a number of ways.

- They give freedom to the person use the funds however he wants.

- It provides a lump sum in case of emergency.

- It gives handsome returns in terms of dividends.

- It helps by inculcating the habit of saving money.

Types of Chit Funds

Chit funds are of different kinds. These are:

Organized Chit Funds: In northern India, a common type of chit fund is where small paper chits with each member’s names are gathered in a box. When all the members come together for a monthly gathering, the person who is in charge in front of all the present members picks a chit from the box. The member so selected gets to take home the day’s collection. Afterwards, that person’s chit is removed from the box. The person who was previously selected comes to the meetings and pays his/her share, but his/her name will not be selected again.

Special Purpose Funds: Some chit funds are organized for a specific purpose. For example, Christmas gifts fund which has a very specific end date which is about a week before Christmas. Such a fund can reduce the cost and relieves the members from extra work in the busy festival season. Nowadays, such special purpose chit funds are conducted by, ladies wear shops, jewellers etc. to promote their goods.

Online Chit Funds: With the popularity of e-commerce, Chit funds are being organized online as well. Online chit funds are conducted online, and contributors can make their monthly contributions and receive the prize through online transactions including electronic funds transfer system. Each member gets his or her own online account to manage and circulate chit funds.

Registered Chit Funds: Registered chit funds are those funds which are registered with the state government under the Chit Funds Act,1982. There are over 10,000 registered chit funds in India.

Unregistered Chit Funds: Unregistered funds are those which are not registered with any state government. They are not regulated under any law.

Registration of chit funds

The Chit Fund Act, 1982 regulates the Chit Fund business in India. According to the Act, a “chit” means a transaction whether it is called chit, chit fund, chitty, kuri or by any other name by or under which a person enters into an agreement with a specified number of individual that every one of them will subscribe to a certain sum of money (or instead a certain quantity of grain) by way of periodical installments over a definite time period and that each such subscriber will, in her/his turn, as determined by lot or by auction or by tender or in such other manner as may be specified in chit agreement, be entitled to prize amount.

A transaction cannot be called as a chit unless the members will not subscribe and pay for it to be entitled for the prize money. If some alone, but not all, of subscribers get the prize amount without any liability to pay the future subscriptions or all the subscribers get the chit amount by turns with a liability to pay future subscriptions, it can’t be a chit fund.

Though the chit fund companies are the type of a Non-Banking Financial Companies (NBFC), they are exempted from being registered with the Reserve Bank of India. The chit funds are a category of NBFC which are regulated by the other regulators and hence exempt from the requirement of registration under RBI Act.

To start this business in India, it is recommended that the promoters of the chit fund company should first incorporate a Private Limited Company with the objective of operating a chit fund business. Once a private limited company is constituted, the company then applies with the appropriate Chit Fund Registrar of the State to obtain the registration for operating a Chit fund company. A chit fund business can only be started after obtaining the chit fund business registration from the relevant Registrar of the State.

The registration will not be given to:

- Any individual or entity convicted of any offence under the Chit Fund Act or under any other Act regulating the business and sentenced to imprisonment for any such offence; or

- Any individual or entity who had defaulted in payment of the fees or the filing of any statement or the record required to be paid or filed under this Act or had previously violated any of the provisions of this Act or the rules made thereunder; or

- Any individual or entity had been convicted of any offence that involves moral turpitude and had been sentenced to imprisonment for any such offence unless a period of five years has elapsed since his/her release.

Relevant Statute Governing Chit Funds

Chit funds companies in India are governed by various State or Central laws. Organized chit fund schemes are required to be registered with the Registrar of Firms, Societies, and Chits. The chit funds are governed according to the following laws:

1) Union Government – Chit Funds Act, 1982 (Except the State of Jammu and Kashmir)

2) Tamil Nadu Chit Funds Act, 1961

3) The Chit Funds (Karnataka) Rules, 1983

4) Delhi Chit Funds Rules, 2007

5) Maharashtra Chit Fund Act, 1975

6) West Bengal Protection of Interest of Depositors in Financial Establishments Bill, 2013

7) Prize Chits and Money Circulation Schemes (Banning) Act, 1978

The Reserve Bank of India (RBI) is the regulator of banks and other non-banking financial companies, but it does not control the chit fund business. Despite the fact that chit funds are accepting deposits, the term ‘deposit’ as defined by the Reserve Bank of India Act, 1934 does not comprise the subscription to chits. However, the RBI can always guide State Governments on the regulatory aspects of the creation of rules or exemption of certain chit funds. The latest guidelines provided by the RBI regarding the Chit are given in RBI/2014-15/636.

Although, SEBI as the regulator and controller of the securities market regulates and manages collective investment schemes. But the SEBI Act, 1992 specifically precludes chit funds from their definition of collective investment schemes

Prevention of Money Laundering (Amendment) Act, 2012 has recognized Chit Funds in Section 2(l).

Under Prize Chits and Money Circulation Scheme (Banning) Act, 1978 (PCMCS) ‘Conventional Chit,‘ i.e., the chit mentioned above has been defined in Section 2(a). In this act, another type of chit has also been defined under Section 2(e) named as ‘Prize Chit’ and it is banned in the territory of India. Prize chit is different from conventional chit as prize chit involves the sale of certificates, units, and other instruments and there is an admission fee also, whereas, conventional chit does not contain any of those features.

Chit Funds Act, 1982

Important definitions in the Act

Chit Funds Act defines a number of important terms. They are:

- Chit Agreement: It is defined as a document which contains the articles of agreement between the foreman and the subscribers of the chit.

- Chit Amount: It is the sum-total of all the subscriptions payable by all the subscribers for any instalment of a chit without any deduction of discount.

- Discount: It is the sum of money which a prized subscriber is, under the terms of the chit agreement, required to forego and which is set apart under the said agreement to meet the expenses of running the chit or for distribution among the subscribers or for both.

- Foreman: The person who under the chit agreement is responsible for the conduct of the chit and includes any person discharging the functions of the foreman under section 39 of the Act.

Features of the Act

- The Act states that all registered chit funds should contain either of the words “chit fund”, “chitty”, or “Kuri” as part of their name. These names can only be used by chit funds, no other person or entity has the right to use these names.

- Registered chit funds are not allowed to conduct any business other than chit businesses.

- The foreman is allowed to start or run several chits simultaneously. However, prior approval of the state government is required before starting each chitty.

- It prohibits every kind of fund that does not have prior permission of the respective state government.

- The foreman needs to deposit 100% of the chit value with the Registrar of Chits prior to the commencement of the chit scheme. This deposit will be refunded to the foreman on the successful completion of the chit cycle.

- All Chit funds registered under this Act needs to have its accounts audited by a qualified Chartered Accountant.

- The Act requires that all registered chit funds impose a 40% cap on the bidding amount. This 40% is calculated on the chit value of the scheme. This bid-cap is administered to ensure that the bid does not rise uncontrollably leading to subsequent default by the bidder.

Chit Funds Amendment Bill, 2019

-

Application of the Act

Before

The Act did not apply to:-

(i) any chit started before the enactment of the Act, and

(ii) any chit (or multiple chits being managed by the same foreman) where the amount is less than Rs 100.

After

The Bill removes the limit of Rs 100, and also allows the state governments to specify the base amount over which the provisions of the Act will apply.

-

Addition of names for chit funds

Before

The Act specified various names which may be used to refer to a chit fund. These include chit, chit fund, and Kuri.

After

The Bill additionally inserts three more names, Fraternity Fund, Rotating Savings, Credit Institutions.

-

Video-Conferencing

Before

The Act specifies that a chit will be drawn in the presence of at least two subscribers.

After

The bill has a provision which allows subscribers to join through video conferencing.

-

Foreman’s Commission

Before

Under the Act, the foreman is entitled to a maximum commission of 5% of the chit amount.

After

The Bill seeks to increase the commission to 7%. The Bill also allows the foreman a right to a lien against the credit balance from subscribers.

-

Total Amount of Chit Funds

Before

The Act, chits may be conducted by firms, associations or individuals. The Act states the maximum amount of chit funds which may be collected. These limits are:

(i) one lakh rupees for chits conducted by individuals, and for every individual in a firm or association with less than four partners, and

(ii) six lakh rupees for firms with four or more partners.

After

The limit of chit fund has been increased to three lakh rupees and 18 lakh rupees.

-

Substitution of Terms

Before

The Act defines certain terms in relation to chit funds. It defines: (a) ‘chit amount’, ‘dividend’, ‘prize amount’.

After

The Bill changes the names of these terms to ‘gross chit amount’, ‘share of discount’ and ‘net chit amount’, respectively.

Advantages and Disadvantages of Chit Funds

Advantages

- Chit funds are easy to join.

- They promise high returns.

- The rate of interest of borrowing from chit funds is low.

- People of lower income households can also participate.

- Helps micro-enterprises to develop.

Disadvantages

- High transaction cost.

- Chit funds have known to be vulnerable to scams.

- Saradha Chit Fund Scam: The scam was run by Saradha Group. The group collected 200 to 300 billion rupees before it collapsed in 2013.

- Rose Valley Chit Fund Scam: The Rose Valley scam was a bigger financial fraud than the Saradha scam, more than Rs 15,000 crore was reportedly collected from depositors all across India.

3. Associated with a number of risks. They are:

- The biggest risk involving a chit fund is the misuse of the pooled funds by the foreman.

- Sometimes members stop paying the dues and have already taken the first bid.

- In certain chit funds, discount rate is rigged, and a desperate member ends up paying a higher discount.

Things to Keep in Mind while Investing in Chit Funds

When a person invests in chit fund, they should keep the following things in mind:

- Make sure the chit fund is registered: Before investing in a chit fund, a person should make sure that the chit fund is registered. This can be done by checking the certificate of registration from the Registrar of Companies.

- Check if the certificate is genuine: The certificate and registration number issued by the Registrar should also be checked.

- Check if the chit is approved: Every new chitty started by the chit fund should have prior approval.

- Know the promoters: Go through the list of the director of the Company to check whether the fund is financially sound.

- Complaints against the Fund: Complaints about the fund can be verified from the Office of the Registrar.

Rights available to a Subscriber of the Chit Fund

The subscriber has a right to:

- Get a proper receipt and copy of chit agreement for the payment of subscription.

- Get the amount when the chit is prized in his favour.

- Attend auction and bid during an auction.

Role of SEBI and RBI in chit funds

The Reserve Bank of India (RBI) is the regulator for banks and other non banking financial companies (NBFCs) but it does not regulate the chit fund business. While chit funds accept deposits, the term ‘deposit’ as defined under the Reserve Bank of India Act, 1934 does not include subscriptions to chits. However, the RBI can provide guidance to state governments on regulatory aspects like creating rules or exempting certain chit funds. SEBI regulates collective investment schemes as the regulator of the securities market. But the SEBI Act, 1992 specifically excludes chit funds from their definition of collective investment schemes. In the recent Saradha Group case, SEBI investigation discovered that Sarada were, in effect, operating as a collective investment scheme without SEBI’s approval.

Regulation imposed by RBI on chit fund business

- Chit fund business can be conducted only by a registered company. Running of Chit business by family and partnership firms are restricted.

- Chit companies must register with the Registrar of Chit Company in every state, furnishing full particulars about their chit company.

- The maximum discount that could be taken in a bid was restricted to 30% of the total chit amount. However, in 2001, the same has been enhanced to 40% (in the case of a chit for Rs. 1 lakh, not more than Rs. 40,000/- can be the bid amount).

- Details of each and every chit must be furnished to Reserve Bank of India along with the personal particulars of the subscribers.

- It is mandatory to keep one month’s chit amount of all the subscribers/members with the Reserve Bank of India till the end of a particular chit.

Conclusion

Above all, chit funds are not trustworthy unless it’s a person group formed by friends and relatives whom you trust a lot. I don’t think one should put money with chit funds which are not among their social circle. It might make sense for people in smaller cities to look up to them. As the last note, these chit funds are not investment vehicles where you park your hard earned money, so please avoid them unless you want to exactly take that kind of risk. Chit Fund is a unique way to save money because the tenure/maturity period is short and the subscription amount is small which is easily affordable in rural and middle/low income groups. There is no hard and fast rule to regulate it and can be organized in a very informal manner and designed according to one’s needs. Despite all these reasons one has to be careful about the kind of chit fund they are subscribing to or is participating and who is organizing it. In the light of the recent Saradha Group chit fund scam, the Hon’ble Supreme Court has passed many guidelines to govern and administer the business of Chit Funds.

Students of Lawsikho courses regularly produce writing assignments and work on practical exercises as a part of their coursework and develop themselves in real-life practical skill.

https://t.me/joinchat/J_0YrBa4IBSHdpuTfQO_sA

Follow us on Instagram and subscribe to our YouTube channel for more amazing legal content.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications