In this blog post, Garima Jain, a Research Associate and Academic Counsellor at iPleaders.in, gives a detailed analysis of the concept of leveraged buyouts and how they operate.

Introduction

Leveraged Buyouts (LBO) in the technology of globalization mergers and acquisitions have surmised sizeable consequentiality inside us and across borders. These sorts of acquisitions require a sizably voluminous amount of finance. Leveraged Buyouts have emerged as a mechanism to finance these acquisition deals. LBO is, therefore, a financing approach of purchasing personal service corporations with borrowed or debt capital. Cash is commonly borrowed through the acquiring company and the debt financing represents 50% or greater of purchase rate. Tangible belongings are utilized as security for borrowing with the aid of obtaining firm.

Because of the amount of debt involved in the purchase, LBO diverges from other types of acquisitions. A leveraged buyout is akin to buying a house utilizing a combination of a down payment and a mortgage – in both transactions we preserve cash by putting down a modicum in cash and then borrowing the rest. In an LBO, the “down payment” is called Equity (cash) and the “mortgage” is called Debt.

During the 1980s, as much as 90% of the acquisition charge was financed with debt, but degrees now are between 50% to 75% due to the higher requisites from the sources i.e. banks, excessive yield bonds and so on. The concept at the back of excessive debt level is that companies’ free cash drift is to be utilized to pay the debt payments and interest fees. High yield bonds and mezzanine debt have lower requisites than the financial institution mortgage. This implicatively insinuates that buyers having high yield bonds or mezzanine debt are less corresponding for having sizably voluminous loans. Certainly, the hobby quotes consequently are higher for such traders. Enterprise is moreover detailed to sell or exit in a span of five to 7 years after acquisition. LBOs can, therefore, be used by organizations to reap a lower tax protect through incremented debts.

In step with Jensen (1986 and 1989), LBO works as carrot and stick mechanism to improve the corporation’s cash float in addition to reducing fees. It is normally penned under Jensen’s incentive depth hypothesis. Management’s incremented possession and disposition to ameliorate fetches a right result; that is why the metaphor carrot is commonly applied. On the other hand, a high debt level and interest rate payments work as a “stick” to coerce the management to work harder. Jensen argues that accommodating debt payment acts as an incentive for managers to work strenuously.

Three special studies were made by Kaplan (1989), Muscarella and Vetsuypens (1988), and Smith (1989). They were fixated on working performance after the buyout. Studies revealed that the possession by management after two to four years led to an increment (lol, I think it should be increase) in operating profit by forty percent.

Decisions made by managers in the form of increasing investment options are important for valuation of the firm. If managers underinvest, there is a good risk of losing marketplace shares and advantages from the economics of scale (Grant, 1989). Alternatively, If the organization over-invests, it’ll lose price.

General rule or standard provisions on funds raised by private equity firms

Minimum Commitment:

Prospective constrained partners are required to commit a minimum amount of equity. Constrained partners make a capital commitment, which is then drawn down (a “takedown” or “capital call”) by the general partner to make investments with the fund’s equity.

Investment or Commitment Period:

During the term of the commitment period, constrained partners are obligated to meet capital calls upon notice by the general partner by transferring capital to the fund within a concurred-upon period (often ten days). The term of the commitment period customarily lasts for either five or six years after the closing of the fund or until 75 to 100% of the fund’s capital has been invested, whichever comes first.

Term:

The term of the partnership agreed upon during the fund-raising process is conventionally ten to twelve years, the first a moiety of which represents the commitment period, and the second a moiety of which is reserved for managing and exiting investments made during the commitment period.

Diversification:

Most funds’ partnership acquiescent stipulates that the partnership may not invest more than 25% of the fund’s equity in any single investment.

Characteristics of an LBO

- Strong Cash Flow: Stable cash flow is essential as debt investors look for firm’s ability to repay debts and shell out/give periodic interest payments. Buyers and investors monitor cash flow through due diligence.

- Low financial distress cost: Companies with high financial distress costs are not the best candidates for LBO as financial problem leads to bankruptcy.

- Strong Market Position:Buyer and debt investors prefer a firm with strong market position. Therefore, they look for customer relationships, brand name, and better product and service.

- Growth Opportunity: Growth increases will lead to an increase in sale which in turn will lead to an increase in cash flow. Thus, interest rates and debt repayments will be easier to meet.

- Low capital expenditures: Low investment need improves the ability to increase cash flow.

- Strong asset base:debt investors (usually banks) prefer firms with high asset base basically because it will work as a guarantee for their debt repayment.

Cash flow from operating and financial activities can be derived in the following manner:

- Cash flow from operating activities – Cash flow from Investing Activities= Cash Available for Debt Repayment.

- Mandatory debt, amortization, can differ but is normally 1% of the total debt. The remaining cash flow is used for optional debt repayments.

- Cash Available for Debt Repayment – Mandatory Repayment= Cash Available for Optional Debt Repayment

- The balance of the first year is the total debt, but for every year that passes and repayment is made.

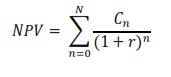

Formulas:

Return analysis is important while decision-making as it provides an answer to return on investment. IRR depends on many different things such as the future financial performance, growth rate, EBIT, the purchase price and the size of equity contribution.

C stands for cash flow at time n, and NPV is the present value of all future cash flow. The initial investment is C0 and NPV is the equity value at time N.

Cash return is the most important. It is a ratio of:

Equity value at exit ÷ Initial equity investment

Models of LBO Financing

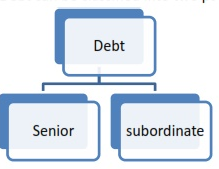

Debt:

Debt can be classified into two parts i.e.

Senior Debt: It is at the topmost rank. Specific assets secure debt. A breach of contract results in the takeover of assets automatically. The cost of debt is thus usually lower, and obligations imposed are quite stringent. Debt repayment for LBO requires a period of 7 years approximately through equal annual installments.

Subordinate Debt: In this type of debt terms are less stringent. At the end of the term, repayment is required in the form of one payment. Lending costs are typically higher as it offers less security to the lender. High yield bonds are publicly handed over to institutional investors using securities. Although they have stringent reporting requirements, they have a fixed rate and can be publicly traded.

High Yield Debts

| Ranking | Usually Subordinated or unsecured |

| Interest Rate | Varies with credit quality, semi-annual payments |

| Maturity | 10 years |

| Call ability | 35% equity |

| Fees for underwriters | 2.5 to 3% |

| Ratings | Usually B+ to CCC+ |

| Covenants | Governed by Indenture |

| Marketing | Sold via prospectus |

| Process | Due diligence, price, documentation |

-

Mezzanine Finance:

Mezzanine finance is utilized as an equity substitute to increment the financial leverage of transactions i.e. the ratio of debt to equity. Mezzanine capital is typically used to fund corporate magnification opportunities, such as an acquisition, incipient product lines, incipient distribution channels or plant expansions; for the company, owners to take mezzanine out of the company for other uses, or avail finance the sale of their business to management or another third party. Mundane features of all mezzanine instruments and products are that they offer a jeopardy/return profile that lies between debt and equity. Mezzanine investment may be more extravagant than traditional bank debt; it is not as stringent. It shares the same covenant package as a traditional bank deal, but the quantification characteristics are more tolerant. Mezzanine facilities are thus often customized or “engineered” to match the cash flow profile of each company

2. Loan Stock:

A term loan has a specified maturity and will during the period pay amortizations according to a schedule. On the date of maturity, a term loan is fully funded. An investigation should be carried out with company’s advisers whether or not loan stock is tax deductible.

3. Preference and Ordinary Share:

Preference shares provide a fixed dividend of the company’s equity which depends on the availability of adequate profits. Ordinary shares are the riskiest among the parts of an LBO capital structure. However, if the risk can be mitigated properly, then ordinary shareholders enjoy benefits.

4. Cash Sweep:

A cash sweep is simply a provision of certain debt covenants that stipulates that any excess cash (namely free cash flow available after compulsory amortization payments have been made) engendered by the bought-out business will be habituated to pay down principal. For those tranches of debt with provisions for a cash sweep, excess cash is utilized to pay down debt in the order of seniority.

5. Bank debt:

Bank debt has got the highest ranking and lowest cost of capital (interest rate). On the other hand, is has got a low flexibility because the borrower has to maintain a designated credit profile and keep certain financial ratios to get the impress. Bank debt, additionally referred to as senior secured credit debt, is a consequential part of the financial structure and will stand for the most astronomically immense part of the sources of mazuma. There are variants of loan inside the bank debt such as revolver credit facility and term loan facilities. They are not very different from each other. The revolver has the competency to recompense liberatingly and re-borrow during the time of the facility as long as it is in line with the conditions in the credit accidence. Homogeneous to the term loan, the revolver has amortizations and interest rate.

Conclusion

Frequently, in lieu of maintaining insolvency, the enterprise negotiates a debt restructuring with its lenders. The economic restructuring might entail that the fairness proprietors inject a few extra cash inside the business enterprise, and the creditors waive components of their claims. In different conditions, the creditors inject incipient coins and postulate the fairness of the corporation, with the existing fairness proprietors dropping their quotas and investment. The operations of the company are proof against the economic restructuring, despite the fact that economic restructuring requires paramount control interest and can result in clients losing faith within the organization.

The incapability to recompense debt in an LBO may be because of preliminary overpricing of the target company and its assets. Over-constructive forecasts of the sales of the organization to be bought out might also moreover result in financial misery after the acquisition..

Leveraged buyout is one of the intriguing routes for those investors who do not have high equity in their pocket and can acquire another target company. The investors can come up with control over the management of the target company. In case the investors have the experience to manage the target company business especially in the case of management buyout in which case the business of the target company will be run by insiders, then the investors can utilize the cash flow coming to such company to recompense the loan taken from the bank. However, there are certain risks if the investors cannot revive the business of the target company and conclusively the prospect of such cash flow for the interest repayment will not transpire. The high-interest rates from such loan may make it arduous for the investors to return the interest and the loan to the bank. In the case of management buyout, it can additionally cause conflict of interest among employees, executives, and the management team. Thus, the stability and experience of the investors are consequentiality factors for running the leveraged buyout investment.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications

A leveraged buyout is the acquisition of a company, which is either privately or publicly organized, as part of an independent business or a large company (subsidiary), to pay the company’s purchase price Using borrowed money. Thanks for sharing this great info.