Kashish Khattar is a 4th year student at Amity Law School, Delhi. This article is a discussion revolving around the regulations regarding Small Finance Banks.

Introduction

Two types of licenses are granted by the RBI. They are universal bank licenses and differentiated bank licenses. Differentiated banks are the ones who services a certain demographic instead of the general public as a whole. Small Finance Bank (“SFB”) are said to be catering to a different type of customers, mainly the ones who are not being serviced by the big commercial banks. SFBs clientele is said to include small business units, small farmers, MSMEs and various other unorganised sectors. The Reserve Bank of India (“RBI”) issued guidelines for setting up SFBs in the country in 2014. SFBs are supposed to be a niche type of banks in India.

An experiment involving small banks was taken way back in 1996 when the central bank came up with the guidelines for setting up of Local Area Banks (“LAB”). LABs were supposed to be cost-effective, low maintenance which would mainly provide efficient and sophisticated services to a limited area of operation i.e. rural and semi-urban areas. LABs were required to have Rs. 5 Cr as minimum capital and an area operation consisting of three contiguous districts. There are only four functioning LABs in India, which exist in the form of non-scheduled banks.

What was the main objective of setting up a SFB?

The main objectives of setting up SFBs was to further financial inclusion of the country’s underserved population with the added benefits of –

- Provision of being a savings vehicle; and

- Supplying credit to stakeholders involved in various unorganised sectors of the country through high technology-low cost operations.

Who is eligible to apply for SFBs?

Eligible promoters of SFBs can be as follows:

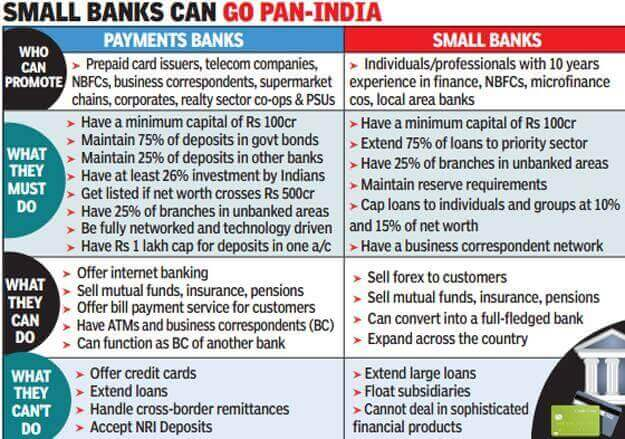

- Resident individuals/professionals with 10 years of experience in banking and finance and Companies and Societies which are owned and controlled by residents will be eligible as promoters to set up SFBs;

- Existing Non-Banking Finance Companies (“NBFCs”), Micro Finance Institutions (“MFIs”) and LABs that are owned and controlled by residents can also opt for conversion into SFBs; and

- Promoter/promoter groups should be ‘fit & proper’ with a similar record of professional experience or of running their businesses for at least a period of five years in order to be eligible to promote SFBs.

Capital requirement for SFBs

SFBs are required to have a minimum capital of Rs. 100 Cr and have to maintain capital adequacy of 15%. Furthermore, the initial minimum contribution to the paid-up equity capital of the SFB will be at least 40% and should be gradually brought down to 26% within 12 years from the date of the commencement of the business of the SFB.

Registration of SFBs

SFBs are registered as a public company under the Companies Act, 2013. They are licensed as under Section 22 (1) of the Banking Regulation Act, 1949 (“BR Act”). They are to be governed by the RBI Act, 1934; BR Act; Payments and Settlements Act, 2007; Credit Information Companies (Regulation) Act, 2005; Deposit Insurance and Credit Guarantee Corporation Act, 1961; and any other relevant guidelines and prudential norms issued by the RBI or any other regulators from time to time. SFBs are to be given the status of a scheduled bank once they start their operations and would be found relevant to Sec 42 (6) (a) of the RBI Act, 1934.

Norms of SFBs

The SFBs are subject to all the prudential norms and regulations of RBI as applicable to existing commercial banks including the requirements related to Cash Reserve Ratio (“CRR”) and Statutory Liquidity Ratio (“SLR”). The SFBs are required to extend 75 per cent of their Adjusted Net Bank Credit (ANBC) to the sectors eligible for classification as priority sector lending (“PSL”) by the RBI. At least 50 per cent of their loan portfolios should have loans and advances of up to Rs. 25 L.

FDI in SFBs

The foreign shareholding in SFBs will be per FDI policy for private sector banks as amended and notified from time to time. The FDI cap dictated by the consolidated FDI policy of 2017 (here) is 74% where the entry route is automatic till 49% and government route beyond 49% and up to 74%. At all times, at least 26 per cent of the paid-up capital will have to be held by residents.

Further, in the case of foreign institutional investors (“FII”)/ foreign portfolio investors (“FPIs”)/ individual FII/FPI holding is restricted to 10% of the total paid-up capital. Moreover, Qualified Foreign Investors are not allowed to hold more than 24% of the total paid-up capital, which can be raised to 49% of the paid-up capital with the approval from the Board of Directors through a resolution, followed by a special resolution to the effect by its general body.

What will be their transition path?

If any particular SFB would want to transition themselves to a universal bank, they would have to apply to the RBI and fulfil the requirements notified by the central bank from time to time. This transitioning is mainly based on the last five year’s performance of the SFB and the due diligence by the RBI. After being transitioned into a universal bank, the SFB will be subject to all the rules & regulations which are applicable to universal banks. (here)

Payments Banks v. Small Finance Banks

The operational SFBs in India are as follows:

- Ujjivan Small Finance Bank

- Jana Small Finance Bank

- Equitas Small Finance Bank

- AU Small Finance Bank

- Capital Small Finance Bank

- Fincare Small Finance Bank

- ESAF Small Finance Bank

- North East Small Finance Bank

- Suryoday Small Finance Bank

- Utkarsh Small Finance Bank

Conclusion

The main objective behind setting up SFBs was to cut down the cost of banking and serve the rural and semi-urban areas of the country. This would be done through the strategy of giving better rates to the consumer for savings and loans. SFBs are instituted to service the small business of the country which is hugely dependent on the high rate unorganised lending sector for their financial needs. SFBs is a huge step towards financial inclusion and financial literacy of the masses by the central bank. Only the time will tell if they are successful enough to help bring change in the banking sector.

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

Allow notifications

Allow notifications