In this article, Himanshi Srivastava of Amity Law School Lucknow discusses All you need to know about Syndicate Loan

Introduction

A Syndicate Loan is one of a kind of loan which is provided by the group of lenders to a single borrower. These borrowers can be an association, any large project or a government. The group of people who are offering loan is known as Syndicate, who are working on providing loans to a single borrower. These loans involve a fixed amount of funds or a credit line.

The main function of a Syndicate loan is to provide a loan extended to a single borrower by multiple financial institution group, or “syndicate”, for that purpose. The same terms and conditions will apply to all of the lenders in the syndication process, and there is only one loan agreement.

Features of Syndicate loan

- Large amount and long t erm:- It can meet customer’s demand for funds of long term and large amount. It is generally used for new projects loans, large equipment leasing and enterprises, M&A financing in transportation, petrochemical, telecommunication, power and other industries.

- Less time and energy for financing:- It’s usually the responsibility of the arranger for doing the preparation work of creating the syndicate or cluster once the recipient and also the arranger have united on loan terms by negotiation

- Wide approaches to syndicated loans: The same loan syndications will embrace several sorts of loans, like fixed-term loans, revolving loans, standby L/C line on needs of the purchasers. Meanwhile, the receiver may select RMB, USD, EUR, GBP and different currency or currency portfolio, if needed.

- It will facilitate borrowers establish an honest market image: To become a roaring institution of the syndicate, comes from the participant’s full recognition of the borrower’s monetary and operational performance, by that the receiver will build up their name.

- Currency: Syndicate adopts mainly RMB but beside it USD,EUR,GBP and other currencies are also available. Multiple currencies can also be used in a syndicated group if demanded by a single borrower.

- Term: Three to five years term is for short term funds, seven to ten years for medium and ten to twenty years for long term funds.

- Interest Rate:The price of syndicated loan is composed of loan interest and fees.

Lending interest rate shall be set, according to different borrowers, in line with lending interest rate policies, lending interest rate regulations of and provisions of the syndicated loan contracts.

Charges: It includes arrangement fee, underwriting fee, agency fee, commitment fee etc.

Target Customers

- Customers who require long-term and large-amount loan.

- Customers with high reputation in the industry, whose operation ability as well as financial and technical strength are recognized by most banks.

Application Qualifications

- The receiver ought to be the legal persons of enterprises and public establishments additionally as alternative economic organizations approved and registered beneath the laws of its various State.

- The receiver should be qualified for basic terms and conditions on the borrowers of disposition General Provisions additionally as crediting management policy issued by the Bank.

- The borrower shall meet requirements of certain level after credit rating by the Bank or other recognized rating agency;

- The borrower shall be large and medium manufacturing enterprises or project companies with sound operation and finance as well as strong competition in respective industries, which shall be promising in the development.

- The borrower has established a regular and sound partnership with the lender.

- In the event of joining the syndicate set up by other banks, the arranger bank shall be a policy bank, state-owned holding bank or foreign bank with sufficient credit and operational strength.

Required Documents

- Relevant information on the borrower and their Indian and foreign shareholders and guarantors,

- Business license and articles of association of the borrower as well as joint venture or cooperation contracts of foreign-funded enterprises and inland associated enterprises,

- Project proposals, feasibility study reports, engineering estimates and other documents approved by government departments and approval documents, as well as the approval documents on the project provided by administrations of taxation, environmental protection, and customs,

- Purchase contracts, construction contracts, supply and sale contracts of project equipment.

- Other documents or information needed by the bank.

Syndication Loan Process

- Pre- sign language Process: It includes period covering following 2 phases:

- Pre-mandate stage: Throughout this era, the main points of the planned group is action which are mentioned in the association and finalized through an Indicative Term Sheet. On the completion of Term Sheet, a letter of Mandate is obtained from the recipient. This point of amount is never shorter than one month and may be as long as collectively in a year.

- Post-mandate stage: Throughout this era, loan syndication takes place and facility agreements square measure negotiated and finalized. it’s finished by a closing or linguistic communication ceremony. This section would possibly take six to eight weeks.

- Post- sign language Process: In this, the total amount covering the execution/ sign language of syndication loan and security documents until full and final adjustment of syndicated loan facility takes place.

Things to Remember

Business of syndicated loan in the main involves arranger, lead bank, manager, participant, agency bank, arranger and alternative members, World Health Organization can perform the duty, relish the correct and assume the chance in keeping with the contract or their various disposition proportion. Syndicate member banks area unit divided into 3main levels: initial, arranger (lead bank); second, manager; third, participants.

- The arranger, liable for organization and arrangement of the syndicated loan, could be a bank or banks that undertake preparation of syndicate and distribution on commission of consumers. The arranger sometimes can underwrite the entire issue of syndicated loan.

- The banking company underwrites a bigger share of the syndicated loan, ranking the very best among managers. Usually, the agent bank is additionally the arranger.

- The manager refers to the position granted by the agent bank in line with loan quantity and level undertaken by every bank within the syndicated loan with larger quantity and additional participants. it is a bank accountable for establishing syndicate throughout the preparation stage..

- Participants discuss with the banks World Health Organization settle for invite of the arranger to hitch the loan syndicate and supply loans consistent with shares determined through negotiation. variations with the managers: Less loan subscription, assume no responsibility for enterprise and alternative sensible preparation of the syndicate.

- The agency bank is chosen by syndicate members and approved by the receiver throughout the loan amount. when language the loan agreement, the agency bank, on behalf of Syndicate members, is accountable for withdrawal, reimbursement of principal with interest, post-loan management and alternative problems on loan management further as communication between syndicate members and also the receiver, handling contract breach, etc. within the light weight of terms of the loan agreement.

- The organiser refers to the bank, designated from lead banks, to supervise the complete syndicated loan and to part undertaken preparation tasks of the bank syndicate.

- advisor refers to the bank appointed by the recipient throughout the syndicated loan amount, that provides paid monetary consulting service for the receiver to form correct loan call in face of varied quotations and loan terms provided by alternative banks thus on facilitate all the loan work.

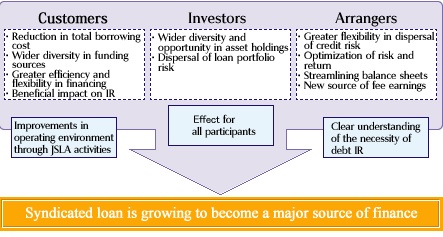

Benefits of Syndicate Loan

Economists and syndicate executives contend that there area unit alternative, less obvious blessings to going with a syndicated loan. These advantages include:

- Syndicated loan facilities will increase competition for your business, prompting alternative banks to extend their efforts to place market info ahead of you in hopes of being recognized.

- Flexibility in structure and rating.

- Syndicated facilities bring businesses the most effective costs in mixture and spare firms the time and energy of negotiating one by one with every bank.

- Loan terms will be abbreviated.

- Increased feedback. Syndicate banks generally area unit willing to share views on business problems with the agent that they might be reluctant to share with the borrowing business.

- Syndicated loans bring the recipient larger visibility within the open market.

Difference between a Consortium loan and a Syndicate Loan

Syndicate loan

While a loan syndication additionally involves multiple lenders and one receiver, the term is usually reserved for loans that involve international transactions, completely different currencies, and a necessary banking cooperation to ensure payments and cut back exposure. A loan syndication is headed by a managing bank that’s approached by the receiver to rearrange credit. The managing bank is usually accountable for negotiating conditions and transcription the syndicate. In return, the recipient usually pays the bank a fee.

The managing bank in a very loan syndication isn’t essentially the bulk investor, or “lead” bank. Any of the taking part banks might act as lead or assume the responsibilities of the managing bank counting on however the credit agreement is required.

Consortium loan

Like a loan syndication, syndicate funding happens for transactions that may not occur with one investor. many banks might comply with collectively supervise one receiver with a standard appraisal, documentation, and follow-up. Consortiums don’t seem to be designed to handle international transactions like a syndication loan; instead, a syndicate might arise as a result of the scale of the project at hand is solely overlarge or too risky for any single investor to assume. typically the collaborating banks type a replacement syndicate bank that functions by leverage assets from every establishment and disbands once the project is completed.

References

Serato DJ Crack 2025Serato DJ PRO Crack

Serato DJ Crack 2025Serato DJ PRO Crack

")

Allow notifications

Allow notifications